The Strengthening of

Canada’s Funds Markets

by Iain McMurdo

Hold ‘Em or Fold ‘Em? - Basel II

by Alex Jurshevski and Irina Park

The Merits of Taking a Portfolio Approach in

Hedge Fund Investing

by Peter Klein

Hedge Funds 2006: The End of the Beginning

by Canadian Hedge Watch Staff

A Commentary on the Dialogue with the OSC

by Basil D’Souza

3

The Strengthening of Canada’s Funds Markets

by Iain McMurdo, Walkers

7

Hold ‘Em or Fold ‘Em? - Basel II, Higher Risk

Assets, and Portfolio Choices

by Alex Jurshevski and Irina Park, Recovery Partners

Performance Summary

Dec

2006

CHW HEDGE FUND INDICES (CHW-HF)

CHW-HF Composite Index

9

The Merits of Taking a Portfolio Approach in

Hedge Fund Investing

CHW-HF Equity Hedged Index

by Peter Klein, KCS Fund Strategies Inc.

CHW-HF Fund of Funds Index

12

Hedge Fund Performance Tables

19

Hedge Funds 2006: The End of the Beginning

by Canadian Hedge Watch Staff

24

Hedge Fund Snapshot: Picton Mahoney Long

Short Equity Fund Class A

25

A Commentary on the Dialogue with the OSC

by Basil D’Souza, Quadrexx Asset Management Inc.

27

Around the Hedge

A Review of Hedge Fund Happenings

Comprehensive

updates on

Canadian Hedge

Funds

ANNUAL

SUBSCRIPTION

December, 2006

(including December, 2006 Report):

$695 CAD

plus GST.

Canadian Hedge Watch Inc.

Tel: (416) 848-0277

Tel: (877) 249-9249

Fax: (416)848-0278

www.canadianhedgewatch.com

research@canadianhedgewatch.com

Contact Wilson Tseng at 416.848.0277 or

tseng@canadianhedgewatch.com

2

CHW-HF Notes Index

YTD

%

2.97

1.54

12.23

4.54

2.28

17.95

0.76

0.27

1.53

-0.26

1.38

1.24

Scotia Capital Canadian Hedge Fund Index

SC CDN HF Index Asset Weighted

4.53

1.70

17.57

SC CDN HF Index Equal Weighted

4.12

1.79

17.36

CSFB/Tremont Hedge Indices

CSFB/Tremont Hedge Fund Index

%

1.83

2.07

13.86

Convertible Arbitrage

1.49

1.06

14.30

Dedicated Short Bias

0.63

-5.46

-6.61

Emerging Markets

2.84

3.15

20.49

Equity Market Neutral

0.88

0.97

11.15

Event Driven

1.58

2.09

15.73

Distressed

1.68

1.59

15.58

Event Driven Multi-Strategy

1.59

2.39

16.38

0.49

3.01

8.15

Fixed Income Arbitrage

Risk Arbitrage

0.72

1.16

8.66

Global Macro

1.36

1.44

13.53

Long/Short Equity

2.08

2.60

14.38

Managed Futures

4.05

2.22

8.05

Multi-Strategy

1.77

2.26

14.54

GLOBAL HEDGE FUND INDICES

CHW Quarterly

Canadian Hedge Fund

Report

Nov

2006

%

Hennessee Hedge Fund Index

1.28

1.74

11.36

HFRI Fund Weighted Composite Index

1.48

2.10

12.93

HFRI Equity Market Neutral Index

0.86

0.45

7.35

HFRI Fund of Funds Composite Index

1.78

1.87

10.43

MARKET INDICES

%

MSCI World Index (C$)

4.13

4.24

20.90

MSCI World Index (US$)

2.06

2.50

20.65

MSCI Emerg. Markets Free Index (C$)

6.63

9.28

32.86

Dow Jones 30 Industrial Avg. (US$)

1.97

1.17

16.29

NASDAQ Composite Index (C$)

1.34

4.50

9.75

NASDAQ Composite Index (US$)

-0.68

2.75

9.52

S&P 500 Total Return Index (C$)

3.46

3.63

16.03

S&P 500 Total Return Index (US$)

1.40

1.90

15.80

S&P/TSX Comp. Index

1.50

3.52

17.26

www. c a n a dia n hedgewat ch.com

The Strengthening of Canada’s Funds Markets

by Iain McMurdo, Walkers

"

M

ore” was a word commonly used to sum up

market activity in 2006. Global markets saw

more hedge funds and private equity funds

involved in takeovers and buyouts, more varied use of

alternative investment vehicles, and more investment

activity in emerging markets last year.

One of the biggest market drivers was the increase in

buyouts of public companies by private equity firms and

bigger deals overall. As of December 2006, the value of

private equity buyouts in the United States and Canada

was on pace to almost triple, with U.S. deals approaching

US$370 billion for the year and Canadian deals climbing

to US$10.1 billion. In the UK, companies had announced

US$75 billion of takeovers in the first 11 months of 2006,

compared with US$34 billion in 2005. Globally, 2,262

private equity deals worth US$563.2 billion had been

struck by December 2006. In 2005, the total private equity

deals were worth US$350.1 billion.

Takeover targets represented a wide range of industries

and included brand names such as HCA Inc., Equity Office

Properties Trust, Home Depot, T-Mobile, the London

Stock Exchange Group, Dunkin' Donuts, Clear Channel

Communications, SunGard Data Systems, Neiman

Marcus, and Metro-Goldwyn-Mayer.

Some of Canada's best-known publicly-traded property

companies, such as Intrawest Corp. and Fairmont Hotels &

Resorts Inc., also got wrapped up into this trend. Fortress

Investment Group LLC paid $2.8 billion for Intrawest, while

Colony Capital LLC and Saudi Prince al-Waleed bin Talal

bought Fairmont in a deal worth US$3.3 billion.

There are several contributing factors to the growth in

number and size of these private equity deals. Some public

companies are trying to avoid the burden of SarbanesOxley regulations in the U.S. by going private. In addition,

private equity funds have billions of dollars to invest, which

is fueling the takeover activity worldwide.

For a third consecutive year, pension funds continued

to drive investments into hedge funds. This trend was

supported by companies such as Unilever, whose pension

funds in 42 countries will soon be able to invest into funds

of hedge funds. Traditional hedge fund investors including

New Jersey's state pension funds and the Indiana State

Teachers' Retirement Fund, upped their investments.

New Jersey increased its commitment to hedge fund

investment from US$800 million in 2006 to US$4.6 billion

in 2007. Even emerging markets got in on the activity.

China's state pension fund is preparing to make its first

investments abroad, putting up to US$1 billion into foreign

financial markets in an effort to improve returns on its

reserves.

The pension fund twist in 2006 was that private equity

investments were also being added to the mix. For

example, the governing agency for the San Diego City

Employee Pension Fund is weighing investment in private

equity funds for the first time. David Gamble, former head

of British Airways Pension Investment Management, one

of the UK's largest company pension plans, supported

investments in private equity as part of a diversified

portfolio. Britain's biggest pension fund, BT, is reportedly

switching about a third of its UK equity holdings – some

3 billion pounds – into hedge funds and private equity as

well.

Continued on page 4

Made to measure

Our comprehensive reports give you the information you need, when you need it.

To learn more about our Prime Brokerage services, call Katrina Rempel at

416.359.7524

www.corporate.bmo.com/pbs

w ww.ca nadi an h edgew a t c h .c om

3

Continued from page 3

Interest and investment by pension funds in hedge funds

is likely to continue in 2007 following the 2006 mid-year

amendments to the US Pension Protection Act. These

amendments have reduced the number of hedge funds

that need to operate in compliance with ERISA and eased

the compliance burden for hedge funds that manage the

'plan assets' of ERISA investors.

In the Cayman Islands, changes to the jurisdiction’s

Mutual Funds Law were enacted to improve certain

aspects of doing business in Cayman for outside

investors, including the introduction of innovative and

market-leading electronic audit and electronic reporting

procedures. Similarly, in the British Virgin Islands, the

segregated portfolio company (SPC) regulations were

enacted, thereby allowing the incorporation of SPCs for

Both the enormous amount of activity in the private equity

markets and the claim that the line between private equity

and hedge funds continues to blur, have encouraged

pension funds around the world to leverage alternative

investments as an influential part of their investment

strategies.

As is to be expected in financial markets, regulation was

also a big topic in 2006. While the Securities and Exchange

Commission (SEC)’s New Rule 203 was reversed earlier

in the year, the Commission continues to look for ways to

protect investors including the introduction of measures

to prohibit fraud by investment advisers and the raising of

the net-worth standard for investing in hedge funds. The

UK’s Financial Services Authority (FSA) is also looking

for ways to increase transparency and change access to

some types of funds.

mutual fund and insurance companies in the British Virgin

Islands. Further amendments were also made to the

recently enacted BVI Business Companies Act to fuel the

jurisdiction’s growth as an offshore financial center.

Canadians have started the new year with their own new

hedge fund regulations. Some experts blame scandals

Management Makes the Difference

FRONT STREET CANADIAN HEDGE

1.2%

22.8%

5.4%

5 year compound

annualized

Compound Annual

Growth

Raterate of return to February 28, 2005

13.2%

(unaudited)

*To January 31, 2005

Since Inception (July 29, 1999)

(as at January 31, 2007)

AVAILABLE TO ACCREDITED INVESTORS - RRSP ELIGIBLE

4

1-800-513-2832

www.frontstreetcapital.com

www. c a n a dia n hedgewat ch.com

such as the U.S. SEC’s recent anti-fraud charges against

Joseph Speigel who allegedly shorted securities through a

Canadian broker-dealer, and the 2005 collapse of Montrealbased Norshield Asset Management (Canada) Ltd. and

Toronto-based Portus Alternative Asset Management Inc.,

as the driving forces behind the changes.

Under the new regulations, which were announced by

the Canadian Securities Associations (CSA) in January,

hedge funds managers will be required to register with

provincial securities commissions. Currently individuals

who manage a specific investment portfolio are required

to register. The new rules will also require registration by

executives who set up and operate the fund management

companies. These executives will further be required to

meet standards regarding competence, financial backing,

integrity, and the ability to manage conflicts of interest.

The CSA is also considering introducing new regulatory

oversight for protected notes and new regulations for

referral rules.

NBCN Prime Brokerage, the prime brokerage arm of

Canadian investment bank, National Bank Financial,

released a survey in January that polled 35 Canadian

fund managers. It found that all of the hedge funds were

already registered. These findings suggest the new

regulations may not be too much of a change. Certainly

any growing market will need to work through challenges

as it matures.

The relatively young age of the Canadian market was

shown in the NBCN Prime Brokerage survey, which

reported that only 17% of the hedge funds polled have

been around for more than ten years.

It seems however, that what the market lacks in age

it makes up for in drive. Between 2005 and 2006, the

number of Canadian hedge funds grew by 25% to nearly

200. While that rate of growth is impressive, even more

noteworthy is the fact that during the same time period

assets under management grew 40%. Nearly 30% of the

Canadian funds in the survey reported assets between

$10 million and $50 million.

Despite the 40% growth, the assets under management

figures are still relatively small in comparison to funds

launched by U.S. fund managers, which typically start

with a minimum of $50 million for offshore funds and

can range into billions of dollars. It’s undeniable though,

that Canadian fund managers are moving in the right

direction.

The Canadian funds market has something to offer that

the markets in the U.S. and Western Europe are lacking.

The country’s rich natural resources – from lumber and

mineral ore to oil and gas – offer a vast array of commodity

investments for fund managers. According to the NBCN

Prime Brokerage study, more than half of the Canadianbased hedge funds leverage strategies for futures and

commodities.

Another change that will impact the Canadian market

is the Canadian government’s decision, announced in

October 2006, to tighten restrictions on companies which

want to convert to lightly-taxed income trusts. This change

Continued on page 6

Mark Your Calendar!

World Hedge Funds Summit 2007

will take place

November 5-7, 2007

in downtown Montreal at the Hilton Montreal Bonaventure,

conveniently located across from the Via Rail Train Station.

For early bird sponsorship opportunities please contact

Tony Sanfelice at 416.848.0277.

w ww.ca nadi an h edgew a t c h .c om

5

Continued from page 5

may also bode well for the funds market. Previously, the

income trust structure allowed companies to make large

payouts, sometimes the full sum, of their operating income

to shareholders. Unit holders benefited from high dividend

yields, but the federal government and the provinces,

according to government sources, lost out on sizeable

tax revenues. Under the revised rules, trusts will pay a

distribution tax set at the conventional corporate tax rate.

There is a four-year grace period during which existing

trusts can unwind. We can expect increased opportunities

for private equity houses looking to take over these trusts,

or a flurry of merger activities as the compliance deadline

approaches.

With all of these factors in place, we predict that the

Canadian hedge fund industry will continue to grow at

a rapid rate over the next five to ten years as the fund

managers form offshore funds to attract non-Canadian

investors to their domestic and international strategies.

Additional regulation will assist in the marketing campaigns

of these investment managers seeking to capitalize on the

attention that the Canadian economy is garnering.

As the CSA and other government agencies continue to

refine Canada’s regulatory environment, it is important

for investors and fund managers to keep an open mind

about what these changes can bring and understand that

legislation that will protect investors and help the industry is

good for everyone. As more private investors and pension

funds begin to look to hedge funds as an investment

vehicle, regulators are trying to create legislation that

takes into account the long-term security of investors of

all sizes.

With Walkers’ strong presence in the Cayman Islands, a

jurisdiction that has long-offered a solid base of lawyers,

accountants and fund administrators, and strict regulations

for investors and managers, we see great opportunities for

Canada with these new regulations.

As the global funds market continues to grow, and

investors look for new places for their money, being able

to add Canada as a viable jurisdiction for international

investments will help fuel the industry, not only in Canada,

but around the world from Cayman to Jersey to BVI and

beyond.

Iain McMurdo is an Investment Funds partner

with Walkers, a leading global offshore law firm

with offices in the Cayman Islands, BVI, Dubai,

Jersey, Hong Kong, London, and Tokyo.

For more information, visit www.walkersglobal.com.

Want to reach high-level hedge fund retail and institutional

executives, investors and brokers?

Advertise with Canadian Hedge Watch.

For information about advertising opportunities please contact

Tony Sanfelice at 416.848.0277 or

sanfelice@canadianhedgewatch.com.

6

www. c a n a dia n hedgewat ch.com

Hold ‘Em or Fold ‘Em? - Basel II, Higher Risk

Assets, and Portfolio Choices

by Alex Jurshevski and Irina Park, Recovery Partners Limited

Summary

Basel II is going to make holding distressed/non-performing

assets much more costly to maintain on the balance sheet

than in the past.

In previous credit down cycles, banks would automatically

send all of their distressed loans to their Special Loans

Groups to be worked out. Under the new Basel II

captain management regime, this is no longer the most

economically prudent approach.

With very few exceptions, the Bank is financially better

off by selling its distressed loans than working them out

internally. These results prove out for different workout

time horizons, credit concentrations and levels of interest

rates.

Our research and subsequent modeling work shows that

it is only when (1) loan sale prices are at a significant

discount to expected recovery values, (2) workout time

horizons are extremely short, (3) expected recovery is

high (over 98%), and (4) the size of the loan is large, that

the economics swing in favor of the “Hold” strategy.

Background

Traditionally Canadian banks have worked out their

nonperforming and high risk portfolios through utilization

of internal Special Loans Groups (SLG). Typically Special

Loans Assets are transferred to the SLG within the bank

for outsourced management. The assets are retained

on the books of the originating unit for capital and

MTR (the bank’s internal funds Marginal Transfer Rate)

considerations in respect of the funding position. An

agreement is typically reached with the SLG on the

estimated amount of recovery on the loan and the amount

of time it will take to effect recovery.

In many banks the performance measurement

methodologies currently applied to

SLGs exclude

consideration of the opportunity costs and capital costs

associated with maintaining on-balance sheet high-risk/

non-core and NPL exposures. It is therefore important

not to confuse how Banks rate the performance of their

Special Loans Groups with the overall cost to a Bank of

retaining “off-strategy” and NPL assets in-house. This is

because the performance measurement methodologies

currently applied to SLG activities exclude consideration

of the opportunity costs and capital costs associated with

w ww.ca nadi an h edgew a t c h .c om

maintaining these exposures.

We have constructed a model that allows for ready

analysis of the tradeoffs banks face in making the choice

between retaining high risk assets on the balance sheet or

mitigating the risk by selling them. In summary the costs

of retaining these assets on the books of the bank are:

•

The write-down and the capital hit associated with an

NPL exposure.

•

The increased capital allocation required to maintain

a lower-rated, down-migrating or NPL exposure and

potential continued underperformance over time (see

chart below).

•

Financing of the funding commitment to support the

facility.

•

The opportunity costs of not being invested in an

earning asset.

•

The cost of internal workout resources.

•

The cost of additional operational risk capital (a new

Basel II requirement) that must be borne by the SLG

unit dealing with the assets.

Continued on page 8

PRIME BROKERAGE

Our Prime Brokerage platform enables

alternative investment fund managers

to trade with multiple brokers while

consolidating one master account with

RBC Capital Markets.

We deliver the tools and resources

necessary to reduce the administrative

responsibilities of managing money so

that you can focus on maximizing

performance. Our fully interactive, webbased portfolio management system is

accessible anywhere, anytime and we

continually strive to set new boundaries

in service by adding new products and

technology.

As a Prime Brokerage client, you also

gain access to our entire firm. This

means

leading

research,

trade

execution and new issue participation.

416-842-6438

WWW.RBCCM.COM/PRIMEBROKERAGE

7

Results

Continued from page 7

•

The risk of further direct financial loss.

•

Reputational and other losses that might ensue (these

contingencies are not captured under the Basel II

Operational Risk Capital Charge allocation rules).

The traditional SLG performance benchmarking model

does not take all variables into account and therefore

significantly understates the cost to the bank of maintaining

this function for all NPL and off-strategy contingencies.

Our empirical analysis shows that ROE differentials

between the SELL and the HOLD strategies can differ

by over 100% per annum in favor of the SELL strategy

ceteris paribus. These ROE comparators speak for

themselves. In all cases where workouts are expected to

take 6-12 months or more the SELL Strategy dominates

and significantly outperforms the HOLD strategy. These

results hold for both watchlisted and NPL loans.

It is only when loans are sold at significant discounts to

expected recovery values or where the workout horizon

is short (3 months) AND expected recovery is high

(98-100%) AND the size of the loan is large that the

economics swing in favor of the

HOLD strategy. These are tail

Capital Charges Under Various Approaches

events and can be mitigated

1988 Accord

through agreement on post2002 Foundation IRB – Corporate Benchmark Risk Weights

2002 Standardized Corprate Risk Weights

closing conditions.

Regulatory Capital Requirement (%)

The chart below, reprinted courtesy of Fitch, illustrates the

direct-drive relationship between asset risk and required

bank capital ratios under Basel II relative to what existed

until recently under the Basel I framework.

30

25

Conclusion

20

15

10

5

0

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

Our research shows that when all of these costs and

considerations are taken into account, maintaining high

risk/non core or NPL exposures on the balance sheet

can only be justified under very restrictive assumptions

regarding outcomes and the ability of the SLG to deliver

compelling results within extremely narrow timeframes.

Our model is based around the behavior of the following

variables:

•

Immediate reduction for cash of impaired/high risk

loan portfolio.

•

Savings on capital allocations.

•

Redeployment of capital to productive uses and

avoidance of opportunity costs.

•

Increased profits and more optimal balance sheet

structure.

Financing of the funding commitment to support the

facility.

•

Savings on personnel costs.

•

More efficient tax planning related to asset disposals.

•

Workout time horizon

•

•

Recovery price arget

The possibility of bringing rehabilitated files back inhouse.

•

Market interest rates

•

Bank marginal transfer rate (MTR)

•

Credit concentrations and capital ratios

•

Credit migration probabilities

This article was written by Alex Jurshevski, the CEO

of Recovery Partners; and Irina Park, Intern, Recovery

Partners. Recovery Partners is a fund that invests in

off-strategy bank assets (www.recoverypartners.biz).

This version is an abridgment.

•

Bank workout costs

Copyright 2006 © Recovery Partners Limited

Probability of Default (%)

IRB – Internal ratings-based.

•

8

17

18

19

20

The financial analysis we

summarize above should

prompt banks to examine the

merits unloading off-strategy

and NPL mid-market assets

as opposed to retaining them

in-house. The advantages of

Active Portfolio Management

are significant:

www. c a n a dia n hedgewat ch.com

The Merits of Taking a Portfolio Approach in

Hedge Fund Investing

by Peter Klein, CFA

T

he theoretical foundation for taking a portfolio

approach to investing dates back to the pioneers of

modern finance – Harry Markowitz and Bill Sharpe.

The underlying theory, however, has been part of prudent

investment practice for a much longer time and is nothing

more than an application of the conventional wisdom “not

to put all your eggs in one basket”.

hopefully lead to a better return with equal or reduced risk

on the overall portfolio. The merits of this portfolio approach

when applied at the asset class level are particularly

evident as traditional investment markets continue to seek

direction while hedge funds outperform on a risk-adjusted

basis.

This approach should also be applied to investments

within each market sector. For example, it is prudent to

invest in a portfolio of equities instead of simply buying one

or two individual stocks because the risks of the individual

stocks will be offset to some extent. Surprisingly however,

the tendency for individual hedge fund managers to offset

each other is not well known by investors. Many investors

purchase only one or two individual managers and thus

ignore the potential benefits of diversification within the

hedge fund sector.

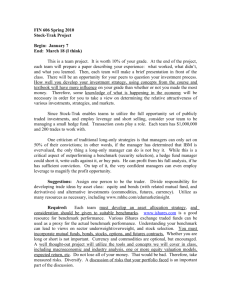

A single stock vs. a portfolio

In this light, the role of hedge funds as portfolio diversifiers

is becoming increasingly clear for many investors. Adding

non-directional investments should offset the risks in

traditional asset classes such as stocks and bonds and

w ww.ca nadi an h edgew a t c h .c om

For equity markets, the benefits of diversification can be

shown by comparing the risk in a single common stock

with the risk in a broadly diversified portfolio.

Continued on page 10

9

Continued from page 9

In Figure 1 we compare the risk in a single common stock

held by many Canadian investors – BCE Inc. – with the

risk in the overall S&P/TSX index which is a portfolio of

hundreds of stocks. In this comparison we measure risk

as standard deviation which is the most commonly used

– but not necessarily complete – method of measuring

risk. Conceptually, standard deviation tells us how much

actual returns will likely be scattered around the average

return. A low standard deviation means that the returns are

tightly clustered (low risk) while a high standard deviation

means that they are widely scattered (high risk). If all the

data values are equal – which would be the case if the

investment were riskless – then the standard deviation will

simply be zero.

standard deviations of 13.72% and 12.44% respectively.

In comparison, two popular hedge fund indices, CSFB/

Tremont Hedge Fund index and HFRI Fund of fund index,

Fig. 2: Annualized Standard Deviations of Hedge Funds

30.00%

25.00%

20.00%

13.72%

15.00%

26.27%

25.00%

16.40%

7.82%

10.00%

5.81%

5.00%

0.00%

10 Largest

Canadian

Hedge Funds

10 Largest

Global Hedge

Funds

CSFB/Tremont

Hedge Fund

HFRI Fund of

Funds

Sources: Globefund.com, Hedgefund.net, Credit Suisse/Tremont, Hedge Fund

Research, Inc. Based on monthly returns from May 1996 to June 2006.

Fig. 1: Annualized Standard Deviations of BCE and S&P/TSX

30.00%

12.44%

have much smaller standard deviations, 7.82% and 5.81%

respectively. This result suggests that diversification also

works in the hedge fund universe.

20.00%

A comment on overall risk

15.00%

It is interesting to note that hedge funds seem to be less

risky than stocks. Many investors are not aware of this

comparison. Both the individual hedge fund and hedge

fund index in Figure 2 have smaller standard deviations

than the individual stock and stock index in Figure 1. This

is a result of the tendency of hedge fund managers to

follow non-directional investment strategies which involve

significant hedging of positions and risks.

10.00%

5.00%

0.00%

BCE

S&P/TSX

Source: YAHOO! Finance. Based on monthly returns from May 1996 to June 2006.

Figure 1 shows the standard deviation of BCE Inc. is

roughly 60% higher than that for the S&P/TSX index. We

also calculated the standard deviation of other equities

commonly held by Canadian investors and found that on

average, it was roughly equal to that of BCE1. This implies

that buying a single Canadian stock will tend to expose

an investor to considerably more risk than a broadly

diversified portfolio.

A single hedge fund vs. a portfolio

Does diversification also work when it comes to hedge

funds? Let’s consider another example.

Figure 2 compares the standard deviations of single hedge

funds with those of diversified hedge fund indices. The risk

reported for the two categories of individual hedge funds is

actually the average of the ten largest Canadian hedge funds

and ten largest global hedge funds, which have annualized

1 From May 1996 to June 2006, the average annualized standard

deviation (based on monthly returns) of the 10 largest CDN stocks

since stock inception is 24.3% versus 26.3% for BCE. Source:

YAHOO!Finance

10

Implementing the portfolio approach

Prior to making an investment – in hedge funds or otherwise–

you must analyze your own needs and circumstances.

The following list provides typical considerations:

•

•

•

•

•

•

Investment knowledge, experience and expertise

Investment objectives

Risk tolerances

Time horizon

Size of allocation

Tax

There are literally thousands of hedge funds available for

investing. Not all are created equal. Many use complex

trading strategies. Assessing your investment knowledge,

experience and expertise, as well as the time you have

available, will let you know whether you need to solicit the

assistance of an investment advisor of some sort. If you do

not have the expertise to properly evaluate the strategies

employed by the hedge funds you would be considering

it may give you a bias towards outsourcing your due

diligence work to experts you trust. This is analogous to

www. c a n a dia n hedgewat ch.com

the decision to purchase an equity mutual fund instead of

picking stocks on your own.

Identifying your investment objectives and risk tolerances

may help to screen out many hedge funds from your

search, thereby making the job of selection somewhat

easier. It is critical to match the hedge fund(s) you invest in

with your objectives and risk profiles to ensure suitability.

Your needs and objectives may be best met by a single

strategy hedge fund, a multi-strategy hedge fund or a fund

of hedge funds.

Looking at your time horizon will further help you to

evaluate the suitability of the hedge fund for your needs

as some funds have low liquidity.

In addition to looking at your expertise, objectives,

tolerances and time horizon you must consider the size of

the investment you wish to make. Many hedge funds have

large minimum investment criteria, often exceeding US

$1,000,000. If you wish to ensure reasonable diversification

via roughly 20 hedge funds you may need an investment

of US $20,000,000 or more if you are to invest in the

hedge funds directly. You will also need a great deal of

time to analyze funds and build that portfolio.

An excellent alternative to building the portfolio yourself is

to invest in a fund of hedge funds which is a portfolio of

hedge funds built by seasoned professionals. This provides

you with diversification across funds and strategies with

much smaller allocations required.

Qualitative Analysis:

•

•

•

•

•

•

•

•

•

Clear strategy and the ability to implement it

Activities within scope of investment policy

Strength and experience of key personnel

Recent key personnel moves

Adequacy of risk controls and governance activities

Details of the Offering Memorandum and Subscription

Agreements

Macroeconomic drivers of returns and related

implications

Investment minimums and liquidity constraints

Fee structure and amounts

The Alternative Investment Management Association

(Canada) has generated a useful framework for evaluating

managers. The list can be found at:

http://www.aima-canada.org/doc_bin/AIMA_Investor_

Checklist-June14Final.pdf

The list includes the following sub-headings:

•

•

•

•

•

•

•

•

•

•

Due Diligence

Manager and Organization

Strategies and Risks

Performance

Liquidity

Fees and Commissions

Taxes

Principal Protected Notes

Offering Documents

Other Issues (Suitability, etc)

Your tax situation is also an important consideration. In

general, hedge funds are tax preferred as compared to

bond income. Some funds of hedge funds have a tax

structure that increases their attractiveness even further.

Armed with this information you are in a better position to

assess whether or not an investment in any hedge fund is

appropriate for your needs.

Analysis of hedge fund managers

Conclusion

Whether you choose to conduct the search yourself

or you rely on an investment consultant or fund of

hedge funds manager to develop the portfolio for you,

the evaluation of hedge fund managers includes many

steps. Typically the analysis of a manager can be broken

into two primary components: Quantitative Analysis and

Qualitative Analysis. This analysis must be conducted

prior to investment and should continue on a periodic

basis for as long as you own the fund.

The concept of diversification across and within asset

classes is well established. There is a strong case for

including hedge funds in an investment portfolio and good

reason to take a portfolio approach when doing so. We

expect investors will increasingly take this approach in

their hedge fund investments.

Quantitative Analysis:

•

•

•

•

•

Strategy review

Returns consistent with stated strategy

Track-record and volatility of returns

Returns expectations

Historical correlations with existing portfolio and other

asset classes

w ww.ca nadi an h edgew a t c h .c om

Peter Klein, Ph. D., CFA, CBV, CGA is co-portfolio

manager and principal of KCS Fund Strategies Inc. He

holds a Ph.D. in financial economics from the University

of Toronto, an MBA, LLB and B.Sc from the University

of Western Ontario. Prior to founding KCS, Dr. Klein

participated in a variety of capital markets activities for

a major Canadian Bank. He has priced, traded and

hedged billions of dollars in derivative securities and

developed trading models for a proprietary derivatives

trading desk. He is also a professor of finance at

Simon Fraser University. www.kcsfunds.com

11

Performance Tables

In addition to the investment style and asset size of each fund, performance is shown as a percentage increase or decrease: over 1, 3 and 6

months, current year-to-date, 1 year, 3 years and the life of the fund since inception. 3-year returns and Since Inception returns are calculated on

an annualized basis. The chart also shows the maximum drawdown, standard deviation over 1 and 3 years, the percentage high watermark and

the percentage of months in which the fund has realized positive returns.

Maximum Drawdown: Maximum percentage loss from the hedge fund's "peak to valley".

Standard Deviation: Statistical measure of volatility measuring the difference between the hedge fund's actual performance and its average

performance.

Percentage High-Water Mark: Expresses the current NAV as a percentage of the all-time high NAV for the fund.

Hedge Fund Performance Summary

November/December 2006

• Much has been said about the celebrated Canadian stock market performance in 2006 with the S&P/TSX Composite Index showing a

December gain of 1.22% and a 14.51% return for the year. The S&P/TSX 60 Index had an even more impressive year with a 1-month gain of

1.65% in December and annual return of 19.16%.

• CSFB/Tremont Hedge Fund Index was up 2.07% in November and 1.83% in December, pushing its annual return to12.85%. The breakdown by

style of the index in the November-December period shows the Emerging Market with the strongest performance, a 2.84% gain in November

and 3.15% in December, for a 20.49% annual return. During the same time period, only the Dedicated Short Bias showed a negative number

at -5.46% in November. It is also the only strategy among all hedging styles with a negative annual return of -6.61%.

• The CHW-HF Composite Index is showing similar gains: A November return of 1.54%, a December gain of 2.97% and a annual return of

12.23%. The CHW-HF Equity Hedged Index still shows the strongest performance at 17.95% annual return while the CHW-HF Fund-of-Funds

Index had the lowest annual return of 1.24%.

Changes in Rankings:

- •In the table for funds with the fewest negative months in 3 years, Arrow Goodwood Fund, One Financial Guaranteed Absolute Return Notes

and Hillsdale Canadian Long/Short Equity Fund have left the list. The new funds in the list are Tremont Core Diversified Fund, Dynamic

Alpha Performance Fund and Arrow WF Asia Fund.

• There are more than the usual number of changes to the top 13 list of the funds with the fewest negative monthly returns in a year. The funds

no longer on this lists are One Financial Guaranteed Absolute Return Notes, Dynamic Contrarian Fund, Millennium Bullion Fund, SciVest

US Equity Index Plus Fund, Focused Opportunities Fund and Dynamic Power Emerging Markets Fund. The ones that made the list this time

are Picton Mahoney Long Short Equity Fund, Lawrence Partners Fund LP, BNP - Mesirow Notes, Arrow Enhanced Income Fund,

Amethyst Arbitrage Fund and Trans IMS Global Market Neutral Fund.

• In the 3-year lowest volatility list, Abria Diversified Arbitrage Trust, Arrow Multi-Strategy Fund and Arrow High Yield Fund are replaced by

Tremont Core Diversified Fund, ONE Financial MSCI Hedge Invest Index Notes and Tremont Capital Opportunity Trust.

• Funds exiting the 1-year lowest volatility list are Abria Diversified Arbitrage Trust, TA3 – Hybrid No-Load, Abria Alternative Strategies Notes

and Horizons Tactical Hedge Fund. New funds on the list are Pro-Hedge Capital Preservation Fund, Arrow High Yield Fund, National

Life Multi-Strategy Fund, Redwood L/S Conservative Equity Fund and Tremont Core Diversified Fund.

• Four funds were removed from the highest 3-year return list: Lakeshore Financial Asset Account, Goodwood Fund, Front Street Canadian

Hedge Fund and Palos Income Trust Fund. They are replaced by The Friedberg Currency Fund, FG Limited Partnership, Sprott Bull/

Bear RSP Fund and Sprott Hedge Fund L.P. II.

• For the highest-return funds in 1 year, Skylon Global Resources Slpit Corp, Epic Limited Partnership, Epic Trust, Asset Logics US Long/Short

Equity Fund and SciVest US Equity Index Plus Fund were no longer on the top 13 list. The additions are Sextant Strategic Opportunities

Hedge Fund, Lawrence Partners Fund LP, Dynamic Power Emerging Markets Fund, Picton Mahoney Long Short Equity Fund and

Mineralfields/Energyfields Multi Series Fund

•

Of the funds reporting performance by the end of the year:

• DeltaOne Northern Rivers Fund L.P. had the highest most recent 3-month return of 45.06%.

• Sextant Strategic Opportunities Hedge Fund Ser F had the highest YTD return (116.87%) and the highest annualized standard deviation

(85.94%).

12

www. c a n a dia n hedgewat ch.com

H E D G E F U N D P E R F O R M A N C E (as of December 31, 2006)

Fund Name

Style

Asset

($MM)

1

month

3

month

6

month

YTD

1

year

3

year

Best 6mo.

(3 Year)

ITD

Worst 6mo.

(3 Year)

Max.

Draw Down

Std. Dev.

(1 year)

Std. Dev.

(3 year)

% High

Watermark

% Pos.

Month

Abria Alternative Combined Return Notes DSC

-

-

0.88

-3.58

-3.19

-2.90

-2.90

-

-1.52

2.50

-6.55

-6.55

5.93

-

94.27

78.26

Abria Alternative Strategies Notes Series 2

-

-

0.11

-4.10

-3.59

-6.17

-6.17

-

-3.69

1.10

-6.18

-10.16

4.89

-

89.94

66.67

Abria Alternative Strategies Notes Series 3 DSC

-

-

-0.54

-5.83

-5.44

-7.16

-7.16

-

-3.04

2.20

-7.77

-9.97

6.17

-

90.03

71.88

Abria Alternative Strategies Notes Series 3 FE

-

-

-0.54

-5.74

-5.15

-6.60

-6.60

-

-3.08

2.20

-7.50

-10.07

6.22

-

89.93

71.88

Abria Alternative Strategies Notes Series 4 FE

-

-

-0.33

-4.09

-3.59

-5.68

-5.68

-

-3.78

0.50

-5.66

-9.05

4.49

-

90.95

67.86

Abria Diversified Arbitrage Fund Class B $US

-

-

0.88

-6.26

-5.87

-1.19

-1.19

-

0.69

5.61

-5.97

-7.83

8.62

-

92.98

86.96

Abria Diversified Arbitrage Fund Class E $US

-

-

0.96

-5.97

-5.42

-0.26

-0.26

-

1.67

6.07

-5.45

-7.68

8.56

-

93.21

88.89

Abria Diversified Arbitrage Fund Class G $US

-

-

0.89

-6.24

-5.84

-1.15

-1.15

-

1.02

5.63

-5.94

-7.83

8.62

-

92.99

81.25

Abria Diversified Arbitrage Trust Class B $US

-

-

0.65

-6.76

-6.46

-1.93

-1.93

0.95

5.12

5.54

-6.46

-8.07

8.81

5.35

92.53

86.59

Abria Diversified Arbitrage Trust Class C $CAD

-

-

0.59

-6.92

-6.71

-3.00

-3.00

0.08

4.70

4.63

-6.87

-8.05

8.66

5.25

92.49

85.37

Abria Diversified Arbitrage Trust Class E $US

-

-

0.74

-6.42

-5.95

-0.91

-0.91

2.28

2.27

6.00

-5.95

-7.89

8.72

5.22

92.80

83.33

Abria Diversified Arbitrage Trust Class O $US

-

-

0.86

-6.02

-5.39

0.97

0.97

3.54

4.11

7.30

-5.39

-7.68

8.74

5.24

93.11

83.72

Abria Diversified Arbitrage Trust Class P $CAD

-

-

0.77

-6.27

-5.73

-0.32

-0.32

2.57

3.01

6.24

-5.73

-7.72

8.61

5.13

92.99

83.33

Abria Energy Trust Class C $CA

-

-

2.30

-2.33

-3.29

-5.06

-

-

-

-

-

-7.19

-

-

94.94

50.00

Abria Energy Trust Class F $CA

-

-

2.39

-1.99

-2.78

-4.47

-

-

-

-

-

-6.70

-

-

95.53

50.00

Abria Energy Trust Class O $US

-

-

2.63

-0.96

-1.34

-1.34

-

-

-

-

-

-3.87

-

-

98.66

57.14

Abria Energy Trust Class P $CA

-

-

2.53

-1.47

-2.00

0.14

-

-

-

-

-

-4.42

-

-

98.00

62.50

Abria Guaranteed Alternative Income Notes Ser 1 FE

-

-

0.45

-1.88

-5.24

-8.19

-8.19

-

-6.12

0.25

-7.11

-12.02

5.60

-

88.38

60.87

-6.12

Abria Guaranteed Alternative Income Ntes Ser 1 DSC

-

-

0.45

-1.88

-5.24

-8.19

-8.19

-

0.25

-7.11

-12.02

5.60

-

88.38

60.87

Adaly Opportunity Fund Class A

Enh. Eq.

-

1.71

0.15

-1.97

7.43

12.29

18.80

33.74

-5.22

-7.81

12.35

12.99

96.40

78.57

Adaly Opportunity Fund Class B

Enh. Eq.

6.72

11.30

17.57

32.47

-5.29

-7.72

12.08

12.78

96.29

74.36

AGF Managed Futures Fund

Dir.

-5.33

46.46

-51.43

-87.66

37.88

46.03

13.13

49.29

Amethyst Arbitrage Fund

13.11

-0.16

-2.71

6.10

-

97.29

88.24

31.50

-6.82

-10.84

22.33

16.03

89.16

68.75

72.34

-

1.66

0.02

-2.15

20.714

-12.50

-1.18

-29.41

-

-

-2.71

-1.43

-0.16

11.77

10.92

-

Arrow Clocktower Platinum Fund

-

38.876

-6.67

-1.09

-0.65

18.87

18.87

12.22

Arrow Clocktower Platinum Fund Class F

-

-

-5.46

0.33

0.99

21.31

21.31

9.80

20.12

-6.42

-16.02

21.90

17.34

90.76

Arrow Compass Fund U$

-

-

1.37

1.14

-0.22

7.94

9.43

-

5.42

11.73

-2.54

-3.20

5.04

-

98.80

75.76

Arrow Distressed Securities Fund Class A

-

37.116

2.33

7.79

-1.81

15.28

15.28

-

6.08

17.75

-6.89

-11.61

15.21

-

95.27

55.56

Arrow Distressed Securities Fund Class F

-

-

2.41

8.02

-1.39

16.26

16.26

-

6.86

18.22

-6.51

-11.37

15.23

-

95.74

55.56

Arrow Elkhorn U.S. Long/Short Fund

Enh. Eq.

-

1.00

5.34

4.40

17.54

17.54

9.45

8.02

14.08

-1.14

-8.17

5.67

6.71

100.00

64.00

Arrow Elkhorn U.S. Long/Short Fund Class F

Enh. Eq.

-

1.08

5.56

4.82

18.50

18.50

10.85

8.59

16.38

-0.72

-4.36

5.67

6.76

100.00

75.56

11.07

Arrow Elmwood Fund Class F

-

-

0.57

6.23

-2.99

-7.98

-7.98

-

-5.68

12.82

-23.11

-25.04

18.65

-

81.69

71.43

Arrow Enhanced Income Fund Class A

-

5.436

1.04

2.23

1.52

4.99

4.99

-

1.43

4.11

-2.19

-2.64

2.15

-

100.00

56.00

Arrow Enhanced Income Fund Class F

-

-

1.12

2.45

1.95

5.86

5.86

-

2.28

4.45

-1.76

-1.76

2.15

-

100.00

64.00

Arrow Enhanced Income Fund Class G U$

-

-

1.12

2.42

1.96

5.45

5.45

-

2.04

4.13

-1.73

-1.91

2.00

-

100.00

60.00

Arrow Enhanced Income Fund Class U U$

-

Arrow Enso Global Fund

Enh. Eq.

Arrow Enso Global Fund Class F

Arrow Epic Capital Fund

Arrow Epic Capital Fund Class F

Enh. Eq.

Arrow Focus Fund Class A2

Dir.

Arrow Focus Fund Class F2

-

-

1.04

2.21

1.51

4.64

4.64

-

1.10

3.32

-2.15

-2.54

2.02

-

100.00

56.00

49.933

2.17

7.62

5.02

13.34

13.34

9.46

11.62

12.44

-4.28

-6.14

9.37

7.05

100.00

66.67

Enh. Eq.

-

2.23

7.83

5.45

14.24

14.24

9.69

12.88

-3.91

-5.98

9.40

7.06

100.00

67.39

Enh. Eq.

69.621

7.30

9.48

11.27

28.51

28.51

23.83

41.74

-13.94

-13.94

21.12

19.22

100.00

69.09

28.09

-13.57

-15.71

21.14

21.11

100.00

59.57

11.73

-9.29

-17.74

9.13

14.09

98.89

53.73

16.47

-5.63

-6.37

9.31

-

99.51

64.29

70.59

Arrow Focus Fund Class U2

Dir.

Arrow Global Equity Long/Short Notes Series 1

-

Arrow Global Long/Short Fund

Enh. Eq.

-

7.38

9.70

11.72

29.60

29.60

8.99

15.817

2.17

6.05

3.69

11.02

11.02

4.80

-

2.24

6.28

4.13

12.25

12.25

-

3.99

15.817

2.15

6.03

3.65

11.07

11.07

13.03

23.77

-6.81

-9.70

9.15

12.26

98.87

-

1.34

4.91

5.29

5.55

5.55

-

2.52

7.87

-4.65

-6.25

7.38

-

98.70

75.00

33.896

2.26

7.08

5.38

10.76

10.76

9.82

5.46

16.08

-5.50

-15.83

8.76

6.90

99.87

59.70

Arrow Global Long/Short Fund Class F

Enh. Eq.

-

2.33

7.30

5.82

11.81

11.81

-

16.45

-5.02

-6.31

8.72

-

100.00

69.70

Arrow Global Long/Short Fund Class G U$

Enh. Eq.

-

0.24

2.65

1.17

11.74

11.74

-

22.79

-4.18

-6.07

11.26

-

96.55

72.73

Arrow Global Long/Short Fund Class U U$

Enh. Eq.

33.896

2.24

7.05

5.32

10.82

10.82

8.60

9.97

16.09

-5.46

-12.85

8.75

8.69

99.88

63.16

Arrow Goodwood Fund

Enh. Eq.

83.279

1.52

4.62

9.84

9.94

9.94

19.14

11.70

39.63

-7.53

-26.88

9.78

12.98

99.19

65.67

Arrow Goodwood Fund Class F

Enh. Eq.

-

-21.37

4.82

10.26

10.78

10.78

18.40

35.76

-7.18

-21.37

36.43

23.01

78.63

71.15

Arrow High Yield Fund

Dir.

118.311

0.76

4.19

6.53

8.11

8.11

3.85

5.64

8.39

-7.30

-8.46

3.24

5.25

100.00

62.07

Arrow High Yield Fund Class F

Dir.

-

0.82

4.42

6.98

9.02

9.02

4.10

6.03

8.89

-8.56

-9.82

3.26

5.61

100.00

63.83

Arrow Japan Long/Short Fund

-

15.000

-0.11

0.27

-0.65

-

-9.47

-0.65

-10.21

-12.01

5.57

-

89.12

38.46

w ww.ca nadi an h edgew a t c h .c om

13

H E D G E F U N D P E R F O R M A N C E (as of December 31, 2006)

Fund Name

Arrow Japan Long/Short Fund Class F

Style

-

Asset

($MM)

1

month

3

month

-

-0.05

0.48

6

month

YTD

1

year

3

year

-0.26

-9.58

-9.58

ITD

-

-8.87

Best 6mo.

(3 Year)

Worst 6mo.

(3 Year)

Max.

Draw Down

Std. Dev.

(1 year)

Std. Dev.

(3 year)

% High

Watermark

-0.26

-9.85

-11.48

5.54

-

89.77

% Pos.

Month

38.46

Arrow Multi-Strategy Fund

Dir.

106.797

2.18

5.31

3.17

10.49

10.49

7.83

6.36

13.38

-3.04

-4.45

6.60

5.26

100.00

65.52

Arrow Multi-Strategy Fund Class F

Dir.

-

2.25

5.53

3.61

11.38

11.38

8.65

9.42

13.84

-2.91

-4.11

6.58

7.22

100.00

68.09

Arrow Multi-Strategy Fund Class G U$ Class F

Dir.

-

2.23

5.53

3.49

11.40

11.40

-

9.30

13.94

-2.70

-4.18

6.64

-

100.00

63.64

Arrow Multi-Strategy Fund U$

Dir.

106.797

2.17

5.30

3.11

10.50

10.50

6.79

13.43

-3.29

-6.98

6.61

6.43

100.00

63.16

Arrow Multi-Strategy Notes Series 1

Dir.

-

2.15

4.83

3.78

11.35

11.35

6.43

7.34

13.04

-3.58

-4.15

6.52

5.50

100.00

67.44

Arrow Multi-Strategy Notes Series 2

Dir.

-

2.02

4.77

3.95

10.97

10.97

5.65

5.60

11.58

-3.14

-3.80

6.13

6.40

100.00

65.00

Arrow Multi-Strategy Notes Series 3

Dir.

-

1.97

4.76

4.30

10.24

10.24

4.49

4.49

10.79

-3.14

-3.72

6.07

5.78

100.00

63.89

Arrow Multi-Strategy Notes Series 3 (FE)

-

-

2.01

4.89

1.99

11.77

11.77

-

5.21

15.65

-4.87

-8.63

11.59

-

95.84

63.64

Arrow Multi-Strategy Notes Series 4

-

-

1.92

4.52

4.08

9.18

9.18

-

6.39

10.05

-3.24

-3.80

5.87

-

100.00

70.00

Arrow Multi-Strategy Notes Series 4 (FE)

-

-

1.96

4.63

1.86

9.64

9.64

-

6.63

8.81

-3.03

-3.63

5.40

-

100.00

63.33

Arrow Multi-Strategy Notes Series 5

-

-

1.83

4.33

3.91

8.34

8.34

-

5.23

9.15

-3.27

-3.76

5.64

-

100.00

73.33

Arrow Multi-Strategy Notes Series 5 (FE)

-

-

1.87

4.42

4.10

8.74

8.74

-

6.46

9.36

-3.08

-3.60

5.63

-

100.00

73.08

Arrow Multi-Strategy Notes Series 6

-

-

1.51

4.23

3.67

5.20

5.20

-

1.74

6.52

-3.59

-4.56

5.31

-

99.48

66.67

Arrow PMC Global Long/Short Fund Class A

-

10.592

-0.22

4.49

9.92

15.70

15.70

-

16.26

-0.83

-5.65

8.32

-

99.78

68.00

Arrow PMC Global Long/Short Fund Class F

-

-

-0.15

4.71

10.36

16.63

16.63

-

12.35

-0.52

-4.54

8.32

-

99.85

68.00

Arrow Voyageur Fund U$

-

-

1.98

3.73

0.19

9.56

12.09

-

16.46

-4.19

-6.18

7.86

-

97.98

84.85

Arrow WF Asia Fund

Enh. Eq.

31.031

3.49

16.76

16.29

18.60

18.60

14.20

18.57

-8.82

-18.50

16.81

13.56

100.00

66.15

19.12

19.12

Arrow WF Asia Fund Class F

Enh. Eq.

Asset Logics Managed Futures Hedge Fund

Dir.

Asset Logics Special Situations Fund

Asset Logics US Long-Short Equity Fund U$

5.72

-

3.53

16.92

16.61

0.134

-9.49

-11.62

-13.78

16.75

21.20

-8.68

-13.38

16.81

13.79

100.00

76.09

0.97

-26.99

-61.98

12.32

16.90

38.02

43.18

-

-

-2.19

17.19

18.53

35.80

35.80

-

1.461

-1.94

0.08

2.59

11.64

11.64

-

36.02

-1.33

-8.30

22.43

-

97.81

68.42

-

27.75

-1.90

-3.16

8.70

-

98.06

BDC Managed Futures Note Series N-8

-

150.000

0.84

1.68

2.41

0.05

0.05

-1.23

63.64

10.24

-11.12

-13.03

4.00

7.33

92.32

56.41

BDC Managed Futures Notes Series N-3

Dir.

11.000

0.39

1.06

-0.57

0.21

0.21

-2.07

0.41

5.31

-9.36

BDC Managed Futures Notes Series N-4

Dir.

32.000

1.06

2.05

0.48

0.02

0.02

-2.23

1.09

6.76

-10.59

-10.62

2.94

5.35

90.60

52.17

-12.58

3.57

6.11

89.54

49.18

BDC Managed Futures Notes Series N-5

Dir.

36.000

1.50

2.58

0.27

-0.27

-0.27

-1.84

2.93

8.51

-10.49

-12.23

4.01

6.42

90.66

53.45

BDC Managed Futures Notes Series N-6

Dir.

43.000

0.58

1.11

1.79

0.99

0.99

-1.17

0.09

9.14

-10.60

-12.48

3.27

6.58

92.50

55.56

BDC Managed Futures Notes Series N-7

Dir.

91.000

0.71

1.41

2.38

0.39

0.39

-1.11

-1.20

9.60

-10.82

-14.07

3.77

7.02

91.20

55.10

BDC Managed Futures Notes Series N-7A

Dir.

224.000

0.79

1.52

2.24

0.27

0.27

-1.23

-1.27

9.59

-10.89

-14.51

3.79

7.04

90.47

53.33

Belmont Dynamic Growth Fund

-

-

-0.50

-10.48

-

-

-

-

-

-

-10.48

-

-

89.52

33.33

BluMont Canadian Opportunities Fund

Enh. Eq.

-

1.08

-2.48

-5.73

-1.87

7.95

19.71

-8.89

-19.40

8.58

9.47

92.09

66.67

-23.46

-1.55

-8.76

-1.65

BluMont Hirsch Long/Short Fund

Non-Dir.

-

3.54

2.90

0.76

9.29

11.18

9.44

18.71

-6.25

-8.88

12.00

11.24

97.14

68.00

BluMont Hirsch Long/Short Fund F Series

Non-Dir.

-

3.56

3.11

1.14

10.01

12.06

10.03

19.16

-5.78

-8.52

11.88

11.33

97.62

65.38

BluMont Hirsch Performance Fund

-

-

2.79

2.17

1.92

9.81

11.74

11.99

20.51

-6.37

-20.73

13.02

11.45

97.17

64.86

BluMont MAN Multi-Strategy Notes Series 1

Dir.

-

2.80

3.36

1.80

6.45

6.87

4.58

4.46

13.77

-11.31

-12.29

9.38

8.67

96.59

62.16

BluMont MAN Multi-Strategy Notes Series A

Dir.

-

2.63

3.09

1.42

6.24

6.63

-

3.57

13.63

-10.38

-10.38

9.37

-

96.28

58.82

BluMont MAN Multi-Strategy Series 2 Notes

Dir.

-

2.76

3.37

1.94

6.37

6.88

-

3.87

13.72

-10.80

-10.80

9.28

-

96.68

58.82

BluMont MAN Multi-Strategy Series 3 Notes

-

-

2.69

3.28

1.82

5.89

6.37

-

7.54

13.04

-5.93

-8.59

9.11

-

96.60

66.67

BluMont MAN Multi-Strategy Series 4 Notes

-

-

2.68

3.21

1.75

5.58

6.09

-

5.39

13.00

-6.04

-8.71

9.11

-

96.48

60.00

BluMont MAN Multi-Strategy Series 5 Notes

-

-

2.57

3.09

2.11

4.22

4.48

-

5.14

9.72

-5.16

-7.97

8.02

-

97.28

65.00

BluMont MAN-IP 220 Series 1 Notes

Dir.

-

4.27

1.73

-4.30

-0.02

-0.80

7.81

6.51

20.84

-17.61

-19.18

15.92

15.64

88.56

55.56

BluMont MAN-IP 220 Series 2 Notes

Dir.

-

4.33

1.85

-4.11

-0.19

-0.96

7.78

5.55

20.56

-18.49

-20.04

15.90

15.66

88.58

57.14

BluMont MAN-IP 220 Series 3 Notes

-

-

4.31

2.90

-2.83

-2.83

-

-

-

-

-

-8.73

-

-

97.17

57.14

BluMont MAN-IP 220 Series 4 Notes

-

-

-1.26

-1.26

-

-1.26

-

-

-

-

-

-1.26

-

-

98.74

75.00

BNP - Mesirow Notes Series 1

Non-Dir.

-

1.42

3.08

4.33

6.21

6.21

2.92

3.48

4.33

-2.46

-2.49

2.70

2.63

100.00

72.34

BNP - Mesirow Notes Series 2

Non-Dir.

-

1.42

3.09

4.33

6.21

6.21

3.71

3.61

4.33

-1.34

-2.28

2.70

2.61

100.00

75.56

BNP - Mesirow Notes Series 3

Non-Dir.

-

1.42

3.08

4.33

6.21

6.21

3.69

3.54

4.33

-1.39

-2.28

2.70

2.61

100.00

74.42

CEO Fund

Enh. Eq.

10.492

2.64

-1.47

-2.14

-17.35

-5.60

25.87

-29.53

-68.76

31.90

21.33

38.75

51.96

CI Global Opportunities Fund

Dir.

23.500

-1.33

0.34

-7.25

-3.00

-3.00

-2.61

16.73

-14.42

-39.28

16.99

13.81

66.18

59.57

CI Global Opportunities Fund U$

-

-

-3.36

-3.78

-11.23

-3.30

-3.30

1.35

-0.86

23.66

-14.65

-46.22

21.57

18.46

79.80

45.88

CI Global Opportunities II Fund

Dir.

14.200

-0.85

0.99

-6.00

-0.85

-0.85

-1.93

5.81

15.38

-12.76

-38.03

15.83

12.83

68.74

53.06

Creststreet Energy Hedge Fund LP Series I

-

-

0.18

4.51

-3.67

-

2.69

44.34

-24.76

-31.32

18.76

-

72.17

57.14

14

www. c a n a dia n hedgewat ch.com

H E D G E F U N D P E R F O R M A N C E (as of December 31, 2006)

Fund Name

Style

Asset

($MM)

1

month

3

month

6

month

YTD

1

year

3

year

ITD

Best 6mo.

(3 Year)

Worst 6mo.

(3 Year)

Max.

Draw Down

Std. Dev.

(1 year)

Std. Dev.

(3 year)

% High

Watermark

% Pos.

Month

Creststreet Energy Hedge Fund LP Series II

-

-

0.10

4.26

-4.14

-

0.76

33.93

-25.12

-31.84

18.77

-

71.51

55.00

Creststreet Energy Hedge Fund LP Series III

-

-

0.10

4.26

-4.14

-

-3.24

32.23

-25.12

-31.84

18.77

-

71.51

52.63

Creststreet Energy Hedge Fund LP Series IV

-

-

0.12

4.32

-4.03

-

-9.25

20.63

-25.04

-31.72

18.77

-

71.67

50.00

Creststreet Energy Hedge Fund LP Series V

-

-

0.18

4.52

-3.66

-

11.50

-24.75

-31.31

18.76

-

72.19

47.06

Creststreet Energy Hedge Fund LP Series VI

-

-

0.11

4.31

-4.04

-

-4.04

-24.98

-32.14

18.78

-

71.22

43.75

Creststreet Energy Hedge Fund LP Series VII

-

-

0.18

4.52

-3.66

-3.66

-24.75

-31.31

18.76

-

72.19

46.67

Creststreet Energy Hedge Fund LP Series VIII

-

-

0.08

3.09

-

3.09

-

-

-

-

-

0.00

-

-

100.00

100.00

Criterion Divers Commodities Currency Hedged B

-

-

-4.88

3.83

-4.03

-4.03

-

-

-

-

-

-10.06

-

-

93.38

57.14

Criterion Divers Commodities Currency Hedged C

-

-

-4.86

3.88

-3.93

-3.93

-

-

-

-

-

-10.04

-

-

93.46

57.14

Criterion Divers Commodities Currency Hedged E

-

-

-4.92

3.87

-3.90

-3.90

-

-

-

-

-

-9.97

-

-

93.51

57.14

Criterion Divers Commodities Currency Hedged F

-

-

-4.79

4.16

-3.42

-3.42

-

-

-

-

-

-9.78

-

-

93.97

57.14

CWB Managed Futures Notes Series N-09

-

94.000

0.77

1.59

2.73

0.03

0.03

-

-0.92

9.19

-5.05

-7.43

4.13

-

95.82

57.58

CWB Managed Futures Notes Series N-10

-

46.000

1.43

2.69

1.49

-1.06

-1.06

-

0.11

3.45

-4.93

-7.27

4.34

-

95.22

55.56

CWB Managed Futures Notes Series N-11A

-

34.000

1.46

2.83

1.59

-1.34

-1.34

-

0.00

2.53

-5.26

-5.75

4.66

-

96.92

52.38

CWB Managed Futures Notes Series N-11B

-

6.000

1.58

3.20

2.25

-0.10

-0.10

-

1.10

3.12

-4.68

-5.27

4.66

-

97.76

61.90

CWB Managed Futures Notes Series N-12B

-

8.000

-0.49

1.25

0.54

-3.64

-

-

-

-

-

-4.83

-

-

96.36

44.44

DeltaOne Energy Fund LP

Dir.

5.500

-6.46

-26.01

-58.92

-26.84

-5.00

106.24

-60.97

-82.44

52.39

57.49

17.56

50.98

DeltaOne Northern Rivers Fund L.P.

Enh. Eq.

-

18.45

45.06

36.28

35.71

62.57

-13.34

-18.42

28.73

23.99

100.00

65.00

DeltaOne Strategic Energy Fund

Enh. Eq.

Dynamic Alpha Performance Fund

Dir.

Dynamic Alpha Performance Fund Series F

Dynamic Contrarian Fund

Dynamic Contrarian Fund Series F

-

7.000

-0.17

-8.06

-21.89

11.068

1.95

10.78

9.53

-

-

-

-

-

-29.81

-

-

70.19

40.00

5.94

13.80

9.02

13.58

-12.56

-15.50

13.01

10.27

99.12

63.64

-

0.830

2.30

11.74

10.81

-

101.876

6.91

10.40

15.86

7.03

7.03

-

7.03

10.81

-11.96

-15.12

13.52

-

100.00

58.33

50.41

50.41

-

68.61

3.58

-5.97

20.18

-

100.00

-

27.402

7.19

11.06

16.81

52.22

77.78

52.22

-

68.67

4.17

-5.83

20.22

-

100.00

77.78

5.94

Dynamic Power Emerging Markets Fund

-

28.343

7.48

27.33

31.47

51.70

51.70

-

54.24

-5.26

-13.42

22.78

-

100.00

76.47

Dynamic Power Emerging Markets Fund Series F

-

81.426

7.49

32.06

34.53

53.20

53.20

-

51.24

-6.46

-12.57

23.44

-

100.00

76.47

Dynamic Power Hedge Fund Class A

Dir.

80.277

15.42

44.35

38.59

72.56

72.56

-

78.16

-22.61

-22.61

40.76

-

100.00

66.67

Dynamic Power Hedge Fund Class F

Dir.

345.901

14.63

42.01

36.68

71.47

71.47

54.74

86.26

-21.94

-21.94

39.99

36.78

100.00

69.09

Epic Limited Partnership

Enh. Eq.

108.600

6.59

8.75

10.63

24.84

24.84

22.01

37.31

-9.90

-10.36

18.00

16.74

100.00

79.73

Epic Trust

-

12.100

4.72

6.76

8.56

22.29

22.29

-

37.07

-3.84

-10.62

17.58

-

99.30

62.50

FG Limited Partnership

-

-

4.93

9.87

7.35

13.48

13.95

19.20

23.82

-3.30

-9.04

9.32

11.98

100.00

68.75

Front Street Canadian Hedge Fund

Dir.

179.757

3.32

12.37

10.44

18.98

18.98

18.29

23.92

-4.11

-40.77

13.12

12.95

100.00

67.78

Front Street Mining Opportunities Fund

-

72.423

0.75

19.81

24.39

56.84

56.84

-

67.92

-5.78

-13.14

27.21

-

100.00

70.83

Front Street Performance Fund II

-

132.974

4.74

14.02

11.27

21.96

21.96

-

20.21

-3.69

-9.70

15.38

-

100.00

66.67

Front Street Rollover Fund Limited

-

33.656

0.55

17.91

7.43

2.63

-

-

-

-

-

-23.57

-

-

90.12

72.73

FrontierAlt All Terrain Global Commodities Fund

-

-

0.59

5.55

1.68

-3.47

-3.47

-

-6.07

12.60

-11.16

-18.47

12.84

-

86.05

50.00

Full Cycle Energy Limited Partnership I

Dir.

13.000

0.49

1.37

2.85

2.50

2.50

18.05

32.15

-6.45

-9.27

9.30

13.91

96.43

62.50

Goodwood Fund Class A

Enh. Eq.

67.270

1.52

4.65

10.14

10.73

10.73

18.01

32.23

-7.09

-26.08

8.82

11.24

99.72

66.67

Goodwood Fund Class B

Enh. Eq.

173.317

1.34

3.79

8.12

8.55

8.55

15.56

9.48

29.92

-6.75

-26.08

8.10

10.48

99.38

65.57

Guaranteed Investment Solutions Series 1

-

-

0.69

1.55

1.68

0.72

0.72

-

-0.42

1.68

-2.73

-4.38

2.43

-

98.19

68.00

Guaranteed Investment Solutions Series 2

-

-

0.70

1.48

2.14

1.76

1.76

-

0.31

2.14

-2.32

-3.08

2.13

-

99.49

71.43

Hillsdale Canadian Long/Short Equity Fund Class A

Enh. Eq.

45.197

-1.53

-2.35

-7.63

-8.85

-8.85

11.44

24.18

-7.63

-18.99

7.88

10.26

88.12

65.88

Hillsdale Canadian Long/Short Equity Fund Class I

Enh. Eq.

44.316

-1.42

-2.06

-7.08

-7.81

-7.81

13.30

25.88

-7.08

-18.27

7.85

10.54

89.05

64.62

Hillsdale Canadian Market Neutral Equity

Non-Dir.

5.439

2.60

4.56

-3.28

-1.68

-1.68

2.55

3.55

9.05

-6.78

-12.57

9.36

7.01

94.79

60.49

Hillsdale Canadian Market Neutral Equity Class I

-

4.865

2.68

4.82

-2.92

-0.89

-0.89

-

3.37

8.61

-6.42

-9.28

9.38

-

95.10

66.67

53.85

Hillsdale US Long/Short Equity Fund Class A U$

Enh. Eq.

8.740

2.62

4.24

5.22

13.41

13.41

11.05

2.98

13.24

-5.42

-37.56

8.04

8.40

100.00

Horizons Diversified Fund

-

0.607

3.36

3.92

1.87

3.51

3.51

-

2.12

5.95

-4.86

-6.78

8.45

-

97.88

62.96

Horizons Mondiale Fund

Dir.

51.963

0.87

3.30

3.79

9.09

9.09

2.04

7.81

5.11

-5.04

-7.74

4.62

4.50

100.00

61.06

Horizons Tactical Hedge Fund

Dir.

0.153

1.48

-0.44

-5.16

-6.99

-6.99

-0.90

-0.78

6.67

-8.24

-9.10

3.89

6.30

92.24

44.44

HRS Absolute Return Trust

-

-

3.06

3.67