An update on credit market conditions

advertisement

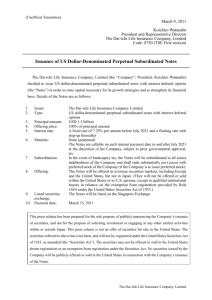

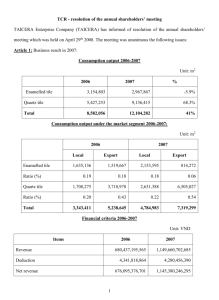

Insight An update on credit market conditions By Michael G. Wildstein November 18, 2015 In June, we commented in this space about the state of technicals and fundamentals for investment grade credit. The following notes provide a follow-up assessment of current credit conditions as of November 2015. As we point out, many of the prevailing macroeconomic conditions from mid‑2015 remain, including uneven global growth, diverging central bank policies, a weak commodity backdrop, and near-zero interest rates in developed countries. In the United States, however, the Federal Reserve is close to beginning its path toward policy normalization, with December seen as the most likely point of liftoff. State of the market Credit fundamentals for nonfinancial issuers continue to deteriorate, as evidenced by rising leverage and weakening levels of interest coverage. Nonetheless, as long as revenue growth remains positive and margins stay elevated, we expect issuers to be able to delever (especially as synergies are realized). Among the specific metrics that are informing our analysis: • Third-quarter earnings results have been favorable thus far, with 70% of companies in the S&P 500® Index beating estimates (admittedly with a low earnings bar). However, the number of companies that have missed revenue estimates now outnumbers those that have beat estimates, and many have issued cautious forward guidance. • Profit margins are at 15-year highs, thanks to minimal increases in employment costs. The tightening labor market should add pressure going forward. • Gross and net leverage have reached new 15-year peaks, even excluding energy and metals/ mining, clear examples of late-stage cycle behavior. • Interest coverage has been declining slowly as the benefit of lower coupons on newly issued debt is being overwhelmed by increased debt issuance. Levels are still strong though, remaining near pre-crisis levels. • Bank credit quality is significantly stronger compared to pre-crisis levels, driven by tighter Fed regulations; this is a positive for bondholders. INSIGHT-UCMC-PRINT 1511 [15542] Page 1 of 5 An update on credit market conditions November 18, 2015 Broad market technicals have yet to show any significant signs of stress, though issuance continues to be a major headwind (see chart) and one of the biggest factors weighing down spreads. Consider: • Year-to-date supply has been driven by merger-and-acquisition activity, refinancing requirements, and regulatory pressures across the healthcare, energy, financial, and technology sectors. • Issuance is on track for another record year, which would mark the fourth consecutive year of more than $1 trillion in investment grade issuance. • M&A activity is on pace to reach a historical peak this year. As deals tend to be funded three to nine months after they’re announced, the record pace of M&A in the third quarter of 2015 should ensure an active issue calendar into 2016. • Liquidity has become challenging. The effects of a smaller number of participating dealers (and tighter regulations in the wake of the financial crisis) are exacerbated by an increasing amount of absolute debt outstanding. Investment grade issuance on pace for record year A fourth consecutive year of investment grade issuance of more than $1 trillion has created “supply indigestion.” Source: Bank of America. Chart is for illustrative purposes only. INSIGHT-UCMC-PRINT 1511 [15542] Page 2 of 5 An update on credit market conditions November 18, 2015 We view the U.S. market as firmly in the expansion phase of the credit cycle, although it appears to be approaching the latter stages. That being said, leading indicators are not signaling an imminent end to the current cycle, and we believe there are still a few years left before we encounter the downturn phase. Notable data points include the following: • Leverage readings are on the high side, which is common in the latter stages of credit cycles, although above-average equity valuation multiples provide some offset. • Lending conditions remain relatively open, a key condition for continued expansion. • While defaults for high yield issues have risen as a result of commodity weakness, defaults still remain below historical averages. We expect default rates to increase during the next 12 months but remain in line (or below) long-term averages. • Refinancing has shrunk as a percentage of use of proceeds compared to pre-crisis years, although the mix is still favorable (lower leveraged-buyout activity). • Balance sheets are in much better shape as management teams have taken full advantage of the low rate environment. Putting a finer point on it We believe the balance of indicators support our assessment of the current stage of the credit cycle. That being said, we think there are sources of pressure that bear watching, and a good share of the negative data lie within the investment grade space. The most notable weakness stems from commodity-based sectors, but as mentioned above, some deterioration is also evident in the healthcare and technology sectors due to debt-financed M&A and share buybacks, which has led to year-to-date supply being at or above the prior full-year levels for those two sectors. As a result, nonfinancial leverage is at a 15-year high. If this trend continues, we think any earnings declines will be particularly painful for issuers who are nursing overleveraged balance sheets. Oversupply in the market continues to be one of the main risks for further risk premium compression. The investment grade market is expected to see further supply in the coming quarters, accompanying large potential M&A deals that have been recently announced, although they are not likely to affect supply until 2016. With recent hawkish Fed testimony and fed funds futures indicating that a December liftoff is now greater than a 50-50 probability, M&A activity may reach its peak in 2015. This should eventually provide some supply relief down the road, although the benefits will take time to be realized as the current excess supply pipeline is worked down. Once supply fades, we expect demand for investment grade credit to return, particularly from liability-driven investors and overseas investors (such as central banks that seek competitive yields). Lower expected supply from other fixed income asset classes (such as commercial mortgagebacked securities, residential mortgage-backed securities, and asset-backed securities) should further support investment grade technicals in time as well. INSIGHT-UCMC-PRINT 1511 [15542] Page 3 of 5 An update on credit market conditions November 18, 2015 Bringing it all together: Valuations and a re-emphasis on risk We were more optimistic on investment grade valuations at the beginning of the year as spreads had cheapened to what we believed were attractive levels; however, event risk, another year of record supply, and global growth concerns affecting commodity prices have created headwinds and are justifying wider risk premiums. At this point, there are no clear near-term catalysts for further tightening at the index level given Fed uncertainty, fourth-quarter supply expectations (heavy), event risk, weakening earnings growth, and global growth concerns (China). As such, investment grade risk premiums should remain volatile in the near term as pockets of stability will be met with additional supply, placing pressure on secondary levels. Apart from the fundamentals noted above, we are also concerned about some of the more prevalent macro risks that markets are facing, including: Uncertainty related to China’s growth outlook — This is already presenting a major overhang to market risk premiums. Further deterioration in China has the potential to derail the U.S. economic recovery and put more pressure on already-weakening corporate earnings. Our base case calls for additional China-driven market volatility that will be met with government or financial easing as an offset. Commodity weakness — Energy and metals prices have remained under consistent pressure for most of the year. Recent reports reflect an expected slowdown in U.S. oil production, which should bode well for future price action. We are taking a more cautious approach to the energy sector given fundamental deterioration, and supply and ratings risk, especially following price assumption changes. Regarding the metals and mining sector, we remain underweight and expect negative credit rating actions, resulting in forced selling to place further pressure on a weak technical backdrop. U.S. dollar strength — Continuation of a strong dollar would be a drag on corporate earnings and exports. Deflation concerns could resurface. Unprecedented stimulus from global central banks — At various phases (whether hiking or easing), ongoing monetary stimulus programs could lead to lower-for-longer yields on Treasurys and investment grade securities. A so-called “bull flattener” pattern in the Treasury yield curve would be an early indicator that global growth is deteriorating further. The views expressed represent the Manager’s assessment of the market environment as of November 2015 and should not be considered a recommendation to buy, hold, or sell any security, and should not be relied on as research or investment advice. Views are subject to change without notice and may not reflect the Manager’s views. Carefully consider the Funds’ investment objectives, risk factors, charges, and expenses before investing. This and other information can be found in the Funds’ prospectuses and summary prospectuses, which may be obtained by visiting delawareinvestments.com or calling 877 693-3546. Investors should read the prospectus and the summary prospectus carefully before investing. IMPORTANT RISK CONSIDERATIONS Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results. The S&P 500 Index measures the performance of 500 mostly large-cap stocks weighted by market value, and is often used to represent performance of the U.S. stock market. INSIGHT-UCMC-PRINT 1511 [15542] Page 4 of 5 An update on credit market conditions November 18, 2015 Asset-backed securities are bonds that are backed by pools of loans or accounts receivable that have been generated by credit providers such as banks and credit card companies. Commercial mortgage-backed securities are bonds that are backed by pools of mortgages on commercial properties. Any Macquarie Group entity noted on this page is not an authorized deposit-taking institution for the purposes of the Banking Act 1959 (Commonwealth of Australia) and that entity’s obligations do not represent deposits or other liabilities of Macquarie Bank Limited (MBL). MBL does not guarantee or otherwise provide assurance in respect of the obligations of that entity, unless noted otherwise. Delaware Investments, a member of Macquarie Group, refers to Delaware Management Holdings, Inc. and its subsidiaries, including the Fund’s investment manager (DMC) and the Fund’s distributor, Delaware Distributors, L.P. Macquarie Group refers to Macquarie Group Limited and its subsidiaries and affiliates worldwide. DMC, a series of Delaware Management Business Trust, is a U.S. registered investment advisor. © 2015 Delaware Management Holdings, Inc. [15545] INSIGHT-UCMC-PRINT 1511 [15542] Page 5 of 5