Financial Statement Analysis - McGraw

advertisement

13

“How Well Am I Doing?”—

Financial Statement Analysis

LEARNING OBEJECTIVES AND CHAPTER COMPETENCIES After studying Chapter 13, you should be able to demonstrate the

following competencies:

COMPETENCY

LO1

Know

Apply

•

•

PREPARE FINANCIAL STATEMENTS IN DIFFERENT FORMATS.

CC1

Prepare and interpret financial statements in comparative and common-size forms.

LO2

COMPUTE VARIOUS FINANCIAL RATIOS TO ASSESS FINANCIAL PERFORMANCE.

CC2

Compute and interpret financial ratios used to measure common shareholders’ well-being.

•

•

CC3

Compute and interpret financial ratios used to measure short-term creditors’ well-being.

•

•

CC4

Compute and interpret financial ratios used to measure long-term creditors’ well-being.

•

•

606

ON THE JOB

Canadians wake up to Tim Hortons coffee,

whether they buy a cup at one of the Tim’s

stores on their way to work or brew it at

home. Businesses like Tim Hortons,

McDonald’s, and other fast food restaurants

must pay close attention to the basics in order to make money. And the most basic element from a customer’s perspective is

getting value for money. Fresh food, low

price, and quick service are just some of the

attributes that are important to a customer.

What about the business?

Needless to say, increasing sales and managing costs are important for the business. Fast food restaurants must particularly

focus on quick turnover, especially because much of the food and

many of the ingredients are perishable. Managers must therefore

pay close attention to key ratios such as cost to sales (or gross

margin), inventory turnover, and (of course) sales growth. Although

Tim Hortons’ sales growth ranged between 4% and 19% from

2007 to 2012, operating income as a percentage of sales

remained fairly steady at about 20% (except for one year), and

inventory turnover ranged between 15% and 19%.

?

iStockphoto © Stacey Newman/iStockphoto

Great Coffee and

Profitable Business

Managers, investors, creditors, regulators, and other interested

stakeholders often keep a close eye on companies’ financial

statements. Financial analysis using ratios is an important tool for

stakeholders to assess a company’s performance.

Sources: Tim Hortons Annual Reports, 2007 to 2012, accessed from

http://www.timhortons.com/ca/en/about/reports.html.

Critical thinking question Do you think that financial ratios can be useful for all companies or only for selected

ones? What types of ratios do you think will be the most beneficial to calculate? Why?

Note to student: See Guidance Answers online.

A LOOK BACK

Chapter 12 introduced the concepts

of decentralization and performance

measurement to evaluate different

types of responsibility centres.

A LOOK AT THIS CHAPTER

In Chapter 13, we focus on the analysis of

financial statements to help forecast the

financial health of a company. We discuss the

use of trend data, comparisons with other

organizations, and the analysis of fundamental

financial ratios.

A LOOK AHEAD

We cover the cash flow statement in Chapter 14,

which is available on Connect. We address how

to classify various types of cash inflows and

outflows, and how to interpret information

reported on the cash flow statement.

607

608

Chapter 13

I

ncreasingly, firms have to look to the financial markets for much-needed financial capital. Companies must present their past performance and future expectations in accordance with established guidelines for financial reporting and clearly express their financial

prospects to the financial marketplace. This is accomplished using financial statements.

All financial statements are essentially historical documents. They explain what happened during a particular period. However, most users of financial statements are concerned about what will happen in the future. Shareholders are concerned with future

earnings and dividends. Creditors are concerned with the company’s future ability to repay

its debts. Managers are concerned with the company’s ability to finance future expansion.

Despite the fact that financial statements reflect the past, they can still provide valuable

information on all of these forward-looking concerns.

Financial statement analysis involves careful selection of data from financial statements

for the primary purpose of forecasting the financial health of the company. This is accomplished by examining trends in key financial data, comparing financial data across companies, and analyzing key financial ratios. In this chapter, we consider some of the more

important ratios and other analytical tools that financial analysts use.

Managers are also very concerned with the financial ratios discussed in this chapter,

as the ratios provide indicators of how well the company and its business units are performing. Some of these ratios would ordinarily be used in a balanced scorecard, as discussed in Chapter 12, although the specific ratios selected depend on the company’s

strategy. For example, a company that wants to emphasize responsiveness to customers

may closely monitor the inventory turnover ratio discussed later in this chapter. Similarly,

the gross margin ratio provides a strong signal regarding the outcomes of efforts to reduce

the cost of goods sold. In addition, since they must report to shareholders and may wish to

raise funds from external sources, managers must pay attention to the financial ratios used

by external investors to evaluate the company’s investment potential and creditworthiness.

Limitations of Financial Statement Analysis in Business Today

Although financial statement analysis is a highly useful tool, it has two limitations that we

must mention before proceeding any further. These two limitations involve the comparability of financial data between companies and the need to look beyond ratios.

Comparison of Financial Data

Comparisons of one company with another can provide valuable clues about the financial

health of an organization. Unfortunately, differences in accounting methods between

companies sometimes make it difficult to compare the companies’ financial data. For example, if one firm depreciates its assets using the double-declining balance method and

another firm by the straight-line method, then direct comparisons of financial data between the two firms may be misleading. Sometimes, enough data are presented in footnotes to the financial statements to restate data on a comparable basis, but the analyst

should evaluate the data’s comparability before drawing any definite conclusions. With this

limitation in mind, comparisons of key ratios with other companies and with industry

averages often suggest avenues for further investigation.

The Need to Look Beyond Ratios

An inexperienced analyst may assume that ratios are sufficient in themselves as a basis for

judgments about the future, but this may not be appropriate. Conclusions based on ratio

analysis must be regarded as tentative. Ratios should not be viewed as an end but, rather,

as a starting point, as indicators of what to pursue in greater depth. They raise many questions, but they rarely answer any questions by themselves.

In addition to ratios, other sources of data should be analyzed in order to make

judgments about the future of an organization. The analyst should look, for example, at

“How Well Am I Doing?”—Financial Statement Analysis

609

industry trends and changes in technology, in consumer tastes, in the economy at large,

and within the company itself. Recent turnover in a key management position, for example, might provide a basis for optimism about the future, even though the past performance of the company (as shown by its ratios) may have been mediocre.

WORKING TO ESTABLISH AND MAINTAIN CREDIBILITY OF THE

FINANCIAL STATEMENTS OF PUBLIC COMPANIES

IN BUSINESS

To restore public and investor confidence in the financial reporting by publicly traded

companies, the Ontario Securities Commission (OSC) over a decade ago took the initiative

to review the financial statements of 100 of the largest Ontario-based Toronto Stock

Exchange (TSX) companies for proper and sufficient disclosure. According to the OSC,

this investigation does not imply that serious problems exist; instead, it should be seen as

an acknowledgment of the importance of such companies to the capital markets and to

investor confidence.

Investor confidence is crucial even in the case of Canadian Crown corporations, which

are an integral part of the Canadian economy. This means that annual reports of Crown

corporations must provide information that is useful to users of the reports. In British

Columbia, the Crown Agencies Resource Office (CARO) is responsible for developing the

reporting framework; it determines the principles of reporting, the minimum requirements in annual reports, and the requirements of the management discussion and analysis

(MD&A) portion of the report. Over the past decade, several changes have been introduced to enhance the quality of the reports, and in 2011, CARO was authorized to review

annual reports at the request of the ministry responsible for a specific Crown corporation.

Sources: Ontario Securities Commission, Perspectives, 5(4) (Fall 2002), http://www.ontla.on.ca/library/

repository/ser/201230/2002/2002v05issue04.pdf; M. Gao, “The Effectiveness of the Disclosure

Regulations: A Case Study of Crown Corporations in B.C.” Undergraduate Honours Thesis, April 2013;

various documents from the Crown Agencies Resource Office’s website, http://www.gov.bc.ca/caro/

publications/.

CREDIT ANALYST

You work for a company that sells industrial products to businesses. Your company routinely sells products to customers on credit—expecting to be repaid within a specified

period. A potential customer has asked for an extension of the payment terms on a very

large sale to a date later than your company usually allows. You have been asked to determine the creditworthiness of this customer and have been provided with a copy of the

customer’s financial statements and accompanying footnotes that were included in the

customer’s most recent annual report. What other information should you obtain before

you begin your analysis?

DECISION POINT

Note to student: See Guidance

Answers online.

Statements in Comparative and Common-Size Forms

Few figures appearing on financial statements have much significance standing by themselves. It is the relationship of one figure to another—and the amount and direction of

change over time—that are important in financial statement analysis. How does the analyst focus on significant relationships? How does the analyst extract the important trends

and changes in a company? Three analytical techniques are widely used: (1) dollar and

percentage changes on statements, (2) common-size statements, and (3) ratios. The first

and second techniques are discussed in this section; the third technique is discussed in the

LO1

• Know

• Apply

CC1: Prepare and interpret financial

statements in comparative and

common-size forms.

610

Chapter 13

remainder of the chapter. To illustrate these analytical techniques, we analyze the financial

statements of Brickey Electronics, a producer of computer components.

Dollar and Percentage Changes on Statements

A good place to begin in financial statement analysis is to put statements in comparative

form. This consists of little more than putting two or more years’ data side by side. Statements cast in comparative form underscore movements and trends and may give the analyst valuable clues as to what to expect.

Examples of financial statements placed in comparative form are given in Exhibit 13–1 and

Exhibit 13–2. These statements of Brickey Electronics reveal that the company has been

experiencing substantial growth. The data in these financial statements are used as a basis

for discussion throughout the remainder of the chapter.

Comparison of two or more years’ financial data is

known as horizontal analysis or trend analysis. Horizontal analysis is facilitated by

showing changes between years in both dollar and percentage forms, as has been done

in Exhibits 13–1 and 13–2.

Showing changes in dollar form helps the analyst focus on key factors that have

affected profitability or financial position. For example, observe in Exhibit 13–2 that sales

for year 2 were up $4 million over year 1 but that this increase in sales was more than

negated by a $4.5 million increase in cost of goods sold.

Showing changes between years in percentage form helps the analyst gain perspective

and gain a feel for the significance of the changes taking place. A $1 million increase in sales

is much more significant if the prior year’s sales were $2 million than if the prior year’s sales

were $20 million. In the first situation, the increase would be 50%—undoubtedly a significant increase for any firm. In the second situation, the increase would be only 5%—perhaps

just a reflection of normal growth.

HORIZONTAL ANALYSIS

Horizontal analysis of financial statements can also be carried out by computing trend percentages. Trend percentages state several years’ financial

data in terms of a base year. The base year equals 100%, with all other years stated as some

percentage of this base. To illustrate, consider McDonald’s Corporation, the largest global

food service retailer, with more than 34,000 restaurants worldwide. McDonald’s enjoyed

consistent growth recently, as is shown by the following data:

TREND PERCENTAGES

2012

Sales . . . . . . . . . . . . . . . . . .

Net income . . . . . . . . . . . .

2011

2010

$27,567 $27,006 $24,075

$ 5,465 $ 5,503 $ 4,946

2009

2008

2007

2006

2005

2004

2003

$22,745

$ 4,551

$23,522

$ 4,313

$22,787

$ 2,395

$20,895

$ 3,544

$19,117

$ 2,602

$17,889

$ 2,279

$16,154

$ 1,471

By simply looking at these data, you can see that sales increased each year. But how

rapidly did sales increase, and did the increases in net income keep pace with the increases

in sales? It is difficult to answer these questions by looking at the raw data alone. The increases in sales and the increases in net income can be put into better perspective by stating them in terms of trend percentages, with 2003 as the base year. These percentages

(all rounded) are set forth below:

Sales . . . . . . . . . . . . . . . . . .

Net income . . . . . . . . . . . .

2012

2011

2010

2009

2008

2007

2006

2005

2004

2003

171%

372%

167%

374%

149%

336%

141%

309%

146%

293%

141%

163%

129%

241%

118%

177%

111%

155%

100%

100%

“How Well Am I Doing?”—Financial Statement Analysis

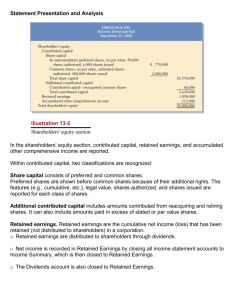

EXHIBIT 13–1

Comparative Balance Sheet

BRICKEY ELECTRONICS

Comparative Balance Sheet

December 31, Year 1 and Year 2

(dollars in thousands)

Increase

(decrease)

Year 2

Year 1

Amount

Percentage

$ 1,200

6,000

8,000

300

15,500

$ 2,350

4,000

10,000

120

16,470

$(1,150)

2,000

(2,000)

180

(970)

(48.9)%*

50.0%

(20.0)%

150.0%

(5.9)%

4,000

12,000

16,000

$31,500

4,000

8,500

12,500

$28,970

–0–

3,500

3,500

$ 2,530

–0–%

41.2%

28.0%

8.7%

$ 5,800

900

300

7,000

$ 4,000

400

600

5,000

$ 1,800

500

(300)

2,000

45.0%

125.0%

(50.0)%

40.0%

7,500

14,500

8,000

13,000

(500)

1,500

(6.3)%

11.5%

2,000

2,000

–0–

–0–%

6,000

1,000

9,000

8,000

17,000

6,000

1,000

9,000

6,970

15,970

–0–

–0–

–0–

1,030

1,030

–0–%

–0–%

–0–%

14.8%

6.4%

$31,500

$28,970

$ 2,530

8.7%

Assets

Current assets:

Cash. . . . . . . . . . . . . . . . . . . . . . . .

Accounts receivable, net . . . . . . .

Inventory . . . . . . . . . . . . . . . . . . .

Prepaid expenses . . . . . . . . . . . . .

Total current assets . . . . . . . . . . . . .

Property and equipment:

Land. . . . . . . . . . . . . . . . . . . . . . . .

Buildings and equipment, net . .

Total property and equipment . . . .

Total assets . . . . . . . . . . . . . . . . . . . .

Liabilities and

Shareholders’ Equity

Current liabilities:

Accounts payable. . . . . . . . . . . . .

Accrued payables. . . . . . . . . . . . .

Notes payable, short term. . . . . .

Total current liabilities . . . . . . . . . .

Long-term liabilities:

Bonds payable, 8%. . . . . . . . . . . .

Total liabilities . . . . . . . . . . . . . . . . .

Shareholders’ equity:

Preferred shares ($100 par;

20,000 shares issued) . . . . . . .

Common shares

(unlimited authorized, $12 par;

500,000 shares issued) . . . . . .

Additional paid-in capital . . . . .

Total paid-in capital. . . . . . . . . . . . .

Retained earnings . . . . . . . . . . . .

Total shareholders’ equity . . . . . . . .

Total liabilities and

shareholders’ equity. . . . . . . . . . .

611

*Since we are measuring the amount of change between year 1 and year 2, the dollar amounts for

year 1 become the base figures for expressing these changes in percentage form. For example, cash

decreased by $1,150 between year 1 and year 2. This decrease expressed in percentage form is

computed as follows: $1,150 4 $2,350 5 48.9%. Other percentage figures in this exhibit and

Exhibit 13–2 are computed in the same way.

The trend analysis is particularly striking when the data are plotted as in Exhibit 13–3.

McDonald’s sales growth was steady throughout the entire 10-year period, but it was outpaced by even higher growth in the company’s net income. A review of the company’s income statement reveals a dip in net income growth in 2007. We would now look at the

612

Chapter 13

EXHIBIT 13–2

Comparative Income

Statement and Reconciliation

of Retained Earnings

BRICKEY ELECTRONICS

Comparative Income Statement and Reconciliation

of Retained Earnings

for the Years Ended December 31, Year 1 and Year 2

(dollars in thousands)

Increase

(decrease)

Year 2

Year 1

Amount

Sales . . . . . . . . . . . . . . . . . . . . . . . . . .

Cost of goods sold . . . . . . . . . . . . . .

$52,000

36,000

$48,000

31,500

$4,000

4,500

Gross margin . . . . . . . . . . . . . . . . . .

Operating expenses:

Selling expenses . . . . . . . . . . . . . .

Administrative expenses. . . . . . .

16,000

16,500

(500)

(3.0)%

7,000

5,860

6,500

6,100

500

(240)

7.7%

(3.9)%

Total operating expenses. . . . . . . . .

12,860

12,600

260

2.1%

Net operating income . . . . . . . . . . .

Interest expense . . . . . . . . . . . . . . . .

3,140

640

3,900

700

(760)

(60)

(19.5)%

(8.6)%

Net income before taxes . . . . . . . . .

Less: Income taxes (30%) . . . . . . . .

2,500

750

3,200

960

(700)

(210)

(21.9)%

(21.9)%

Net income . . . . . . . . . . . . . . . . . . . .

Dividends to preferred

shareholders, $6 per share

(see Exhibit 13–1) . . . . . . . . . . . .

Net income remaining for

common shareholders . . . . . . . .

Dividends to common

shareholders, $1.20 per share. . .

1,750

2,240

$ (490)

(21.9)%

120

120

1,630

2,120

600

600

1,030

1,520

Net income added to

retained earnings . . . . . . . . . . . . .

Retained earnings, beginning

of year . . . . . . . . . . . . . . . . . . . . . .

Retained earnings, end of year. . . .

EXHIBIT 13–3

McDonald’s Corporation

Trend Analysis of Sales and

Net Income

6,970

5,450

$ 8,000

$ 6,970

Percentage

8.3%

14.3%

400%

300%

Sales

Net income

200%

100%

0%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

“How Well Am I Doing?”—Financial Statement Analysis

company’s financial statements and the related disclosures to know the cause. Special expenditures on projects and extraordinary charges are often typical reasons.

Common-Size Statements

Key changes and trends can also be highlighted by the use of common-size statements. A

common-size statement is one that shows items in percentage form, as well as in dollar

form. Each item is stated as a percentage of some total of which that item is a part. The

preparation of common-size statements is known as vertical analysis.

Common-size statements are particularly useful when comparing data from different

companies. For example, in one recent year, Wendy’s net income was about $10 million,

whereas McDonald’s was $5,503 million. This comparison is somewhat misleading, because of the dramatically different sizes of the two companies. To put this in better perspective, the net income figures can be expressed as a percentage of the sales revenues of

each company. Since Wendy’s sales revenues were $2,431 million and McDonald’s were

$27,006 million, Wendy’s net income as a percentage of sales was about 0.4% and

McDonald’s was about 20.4%. While the comparison still favours McDonald’s, the contrast

between the two companies has been placed on a more comparable basis.

One application of the vertical analysis idea is to state the

separate assets of a company as percentages of total assets. A common-size statement of

this type is shown in Exhibit 13–4 for Brickey Electronics.

Note from Exhibit 13–4 that placing all assets in common-size form clearly shows the

relative importance of the current assets as compared with the noncurrent assets. It also

shows that significant changes have taken place in the composition of the current assets

over the last year. Note, for example, that the receivables have increased in relative importance and that both cash and inventory have declined in relative importance. Judging from

the sharp increase in receivables, the deterioration in the cash position may be a result of

inability to collect from customers.

THE BALANCE SHEET

Another application of the vertical analysis idea is to

place all items on the income statement in percentage form in terms of sales. A commonsize statement of this type is shown in Exhibit 13–5. By putting all items on the income

statement in common size in terms of sales, you can see at a glance how each dollar

of sales is distributed among the various costs, expenses, and profits. And, by placing successive years’ statements side by side, you can easily spot interesting trends. For example,

as shown in Exhibit 13–5, the cost of goods sold as a percentage of sales increased from

65.6% in year 1 to 69.2% in year 2. Or, looking at this from a different viewpoint, the gross

margin percentage declined from 34.4% in year 1 to 30.8% in year 2. Managers and investment analysts often pay close attention to the gross margin percentage, since it is considered a broad gauge of profitability. The gross margin percentage is computed as follows:

THE INCOME STATEMENT

Gross margin percentage 5

Gross margin

Sales

The gross margin percentage tends to be more stable for retailing companies than for

other service companies and for manufacturers, since the cost of goods sold in retailing

excludes fixed costs. When fixed costs are included in the cost of goods sold figure, the

gross margin percentage tends to increase and decrease with sales volume. With increases

in sales volume, the fixed costs are spread across more units and the gross margin percentage improves.

While a higher gross margin percentage is generally considered to be better than a

lower gross margin percentage, there are exceptions. Some companies purposely choose a

strategy emphasizing low prices (and hence low gross margins). An increasing gross margin in such a company might be a sign that the company’s strategy is not being effectively

implemented.

613

614

EXHIBIT 13–4

Common-Size Comparative

Balance Sheet

Chapter 13

BRICKEY ELECTRONICS

Common-Size Comparative Balance Sheet

December 31, Year 1 and Year 2

(dollars in thousands)

Common-Size

Percentages

Assets

Current assets:

Cash. . . . . . . . . . . . . . . . . . . . . . . . .

Accounts receivable, net . . . . . . . .

Inventory . . . . . . . . . . . . . . . . . . . .

Prepaid expenses . . . . . . . . . . . . . .

Total current assets . . . . . . . . . . . . . .

Property and equipment:

Land. . . . . . . . . . . . . . . . . . . . . . . . .

Buildings and equipment, net . . .

Total property and equipment . . . . .

Total assets . . . . . . . . . . . . . . . . . . . . .

Liabilities and

Shareholders’ Equity

Current liabilities:

Accounts payable. . . . . . . . . . . . . .

Accrued payables. . . . . . . . . . . . . .

Notes payable, short-term . . . . . .

Total current liabilities . . . . . . . . . . .

Long-term liabilities:

Bonds payable, 8%. . . . . . . . . . . . .

Total liabilities . . . . . . . . . . . . . . . . . .

Shareholders’ equity:

Preferred shares ($100 par;

20,000 shares issued) . . . . . . . .

Common shares

(unlimited authorized, $12 par;

500,000 shares issued) . . . . . . .

Additional paid-in capital . . . . . .

Total paid-in capital. . . . . . . . . . . . . .

Retained earnings . . . . . . . . . . . . .

Total shareholders’ equity . . . . . . . . .

Total liabilities and

shareholders’ equity. . . . . . . . . . . .

Year 2

Year 1

Year 2

Year 1

$ 1,200

6,000

8,000

300

15,500

$ 2,350

4,000

10,000

120

16,470

3.8%*

19.0%

25.4%

1.0%

49.2%

8.1%

13.8%

34.5%

000.4%

056.9%

4,000

12,000

16,000

$31,500

4,000

8,500

12,500

$28,970

12.7%

38.1%

50.8%

100.0%

13.8%

029.3%

043.1%

100.0%

$ 5,800

900

300

7,000

$ 4,000

400

600

5,000

18.4%

2.8%

1.0%

22.2%

13.8%

1.4%

002.1%

17.3%

7,500

14,500

8,000

13,000

23.8%

46.0%

027.6%

044.9%

2,000

2,000

6.4%

6.9%

6,000

1,000

9,000

8,000

17,000

6,000

1,000

9,000

6,970

15,970

19.0%

3.2%

28.6%

25.4%

54.0%

20.7%

003.5%

31.1%

024.0%

055.1%

$31,500

$28,970

100.0%

100.0%

*Each asset account on a common-size statement is expressed in terms of total assets, and

each liability and equity account is expressed in terms of total liabilities and shareholders’

equity. For example, the percentage figure for cash in year 2 is computed as follows: $1,200 4

$31,500 5 3.8%.

Common-size statements are also very helpful in pointing out efficiencies and inefficiencies that might otherwise go unnoticed. To illustrate, in year 2, Brickey Electronics’

selling expenses increased by $500,000 over year 1. However, a glance at the common-size

income statement shows that on a relative basis, selling expenses were no higher in year 2

than in year 1. In each year, they represented 13.5% of sales.

“How Well Am I Doing?”—Financial Statement Analysis

615

EXHIBIT 13–5

Common-Size Comparative

Income Statement

BRICKEY ELECTRONICS

Common-Size Comparative Income Statement

for the Years Ended December 31, Year 1 and Year 2

(dollars in thousands)

Common-Size

Percentages

Sales . . . . . . . . . . . . . . . . . . . . . . . . . . .

Cost of goods sold . . . . . . . . . . . . . . .

Gross margin . . . . . . . . . . . . . . . . . . .

Operating expenses:

Selling expenses . . . . . . . . . . . . . . .

Administrative expenses. . . . . . . .

Total operating expenses. . . . . . . . . .

Net operating income . . . . . . . . . . . .

Interest expense . . . . . . . . . . . . . . . . .

Net income before taxes . . . . . . . . . .

Income taxes (30%) . . . . . . . . . . . . . .

Net income . . . . . . . . . . . . . . . . . . . . .

Year 2

Year 1

Year 2

Year 1

$52,000

36,000

16,000

$48,000

31,500

16,500

100.0%

69.2%

30.8%

100.0%

065.6%

034.4%

7,000

5,860

12,860

3,140

640

2,500

750

$ 1,750

6,500

6,100

12,600

3,900

700

3,200

960

$ 2,240

13.5%

11.3%

24.7%

6.0%

1.2%

4.8%

1.4%

3.4%

13.5%

012.7%

026.2%

8.1%

001.5%

6.7%

002.0%

4.7%

Note: The percentage figures for each year are expressed in terms of total sales for the year.

For example, the percentage figure for cost of goods sold in year 2 is computed as follows:

$36,000 4 $52,000 5 69.2%.

HELPFUL HINT

Common-size balance sheets express each asset account as a percentage of total assets,

and each liability and equity account as a percentage of total liabilities and shareholders’

equity. Common-size income statements express each income statement account as a

percentage of sales.

Ratio Analysis—The Common Shareholder

A number of financial ratios are used to assess how well the company is doing from the

standpoint of the shareholders. These ratios naturally focus on net income, dividends, and

shareholders’ equities.

Earnings per Share

An investor buys a share in the hope of realizing a return in the form of either dividends or

future increases in the value of the share. Since earnings form the basis for dividend payments, as well as the basis for future increases in the value of shares, investors are always

interested in a company’s reported earnings per share. Probably no single statistic is more

widely quoted or relied on by investors than earnings per share, although it has some inherent limitations, as discussed below.

Earnings per share is computed by dividing net income available for common shareholders by the average number of common shares outstanding during the year. “Net income available for common shareholders” is net income less dividends paid to the owners

of the company’s preferred shares:1

Earnings per share 5

Net income 2 Preferred dividends

Average number of common shares outstanding

LO2

• Know

• Apply

CC2: Compute and interpret financial

ratios used to measure common

shareholders’ well-being.

616

Chapter 13

Using the data from Exhibits 13–1 and 13–2, we see that the earnings per share for

Brickey Electronics for year 2 is computed as follows:

$1,750,000 2 $120,000

5 $3.26

1500,000 shares 1 500,000 shares2/2

HELPFUL HINT

IN BUSINESS

The number of common shares outstanding is calculated by taking the dollar amount of

common stock shown in the balance sheet and dividing it by the common stock’s par value

per share.

DO ANALYSTS BIAS THEIR EARNINGS FORECASTS?

Research from Penn State University suggests that Wall Street analysts’ earnings per share

(EPS) forecasts are intentionally overstated. The study examined analysts’ long-term (three

to five years) and short-term (one year) EPS forecasts from 1984 through 2006. Over this

22-year period, the analysts’ average estimated long-term EPS growth rate was 14.7%, as

against an actual average long-term growth rate of 9.1%. The analysts’ average short-term

EPS projection was 13.8%, compared with an actual annual EPS growth rate of 9.8%. The

professors who conducted the study claim that “analysts are rewarded for biased forecasts

by their employers, who want them to hype stocks so that the brokerage house can garner

trading commissions and win underwriting deals.”

Source: Andrew Edwards, “Study Suggests Bias in Analysts’ Rosy Forecasts,” The Wall Street Journal,

March 21, 2008, p. C6.

Price–Earnings Ratio

The relationship between the market price of a share and its current earnings per share is

often quoted in terms of a price–earnings ratio. If we assume that the current market

price for Brickey Electronics’ shares is $40 each, the company’s price–earnings ratio is

computed as follows:

Market price per share

Earnings per share

$40

5

$3.26

5 12.3

Price–earnings ratio 5

The price–earnings ratio is 12.3; that is, the shares are selling for about 12.3 times their

current earnings per share.

The price–earnings ratio is widely used by investors as a general guideline in gauging share values. A high price–earnings ratio means that investors are willing to pay a

premium for the company’s shares—presumably because the company is expected to

have higher than average earnings growth. Conversely, if investors believe a company’s

earnings growth prospects to be limited, the company’s price–earnings ratio will be

relatively low. For example, not long ago, the share prices of some dot-com companies—particularly those with little or no earnings—were selling at levels that gave rise

to unprecedented price–earnings ratios. However, these price–earnings ratios were unsustainable in the long run and the companies’ share prices eventually fell.

“How Well Am I Doing?”—Financial Statement Analysis

617

Dividend Payout and Yield Ratios

Investors hold shares in a company because they anticipate an attractive return. The return

sought is not always dividends. Many investors prefer not to receive dividends, but instead

to have the company retain all earnings and reinvest them internally in order to support

growth. The shares of companies that adopt this approach, loosely termed growth shares,

may enjoy rapid upward movement in market price. Other investors prefer to have a dependable, current source of income through regular dividend payments. Such investors

seek out shares with consistent dividend records and payout ratios.

The dividend payout ratio gauges the portion of

current earnings being paid out in dividends. Investors who seek growth in market price

would like this ratio to be small, whereas investors who seek dividends prefer it to be

large. This ratio is computed by relating dividends per share to earnings per share for

common shares:

THE DIVIDEND PAYOUT RATIO

Dividend payout ratio 5

Dividends per share

Earnings per share

For Brickey Electronics, the dividend payout ratio for year 2 is computed as follows:

$1.20

5 36.8%

$3.26

There is no such thing as a “right” payout ratio, even though it should be noted that the

ratio tends to be similar for companies within a particular industry. Industries with ample

opportunities for growth at high rates of return on assets tend to have low payout ratios,

whereas payout ratios tend to be high in industries with limited reinvestment opportunities.

THE DIVIDEND YIELD RATIO The dividend yield ratio is obtained by dividing the

current dividends per share by the current market price per share:

Dividend yield ratio 5

Dividends per share

Market price per share

The market price for Brickey Electronics’ shares is $40 each, and so the dividend yield

is computed as follows:

$1.20

5 3.0%

$40

The dividend yield ratio measures the rate of return (in the form of cash dividends

only) that would be earned by an investor who buys the common shares at the current

market price. A low dividend yield ratio is neither bad nor good by itself. As discussed

previously, a company may pay out very little in dividends because it has ample opportunities for reinvesting funds within the company at high rates of return.

IBM RAISES ITS DIVIDEND BY 25%

In the early 1990s, IBM nearly collapsed and was forced to slash its dividend payout. However,

since then the company has rebounded nicely. In 2008, IBM raised its quarterly dividend per

share by 25%, increasing the company’s annual payout to about $2.5 billion. The 25% increase

marked the 13th straight year that IBM had increased its dividend per share. Total cash dividends paid out in 2012 increased by 76% compared to 2007. During the same period, earnings per share doubled.

Source: William M. Bulkeley, “IBM, Flush with Cash, Raises Dividend 25%,” The Wall Street Journal,

April 30, 2008, p. B7; IBM annual reports from 2009 and 2012, http://www.ibm.com/annualreport/.

IN BUSINESS

618

Chapter 13

Return on Total Assets

Managers have both financing and operating responsibilities. Financing responsibilities

relate to how one obtains the funds needed to provide for the assets in an organization.

Operating responsibilities relate to how one uses the assets once they have been obtained. Both are vital to a well-managed firm. However, care must be taken to separate

the two when assessing the performance of a manager. That is, whether funds have

been obtained from creditors or from shareholders should not be allowed to influence

one’s assessment of how well the assets have been employed since being received by

the firm.

The return on total assets is a measure of operating performance that shows how well

assets have been employed. It is defined as follows:

Return on total assests 5

Net income 1 3 Interest expense 3 11 2 Tax rate2 4

Average total assests

Adding interest expense back to net income results in

an adjusted earnings figure that shows what earnings would have been if the assets had

been acquired solely by selling shares. With this adjustment, the return on total assets

can be compared for companies with differing amounts of debt, or over time for a single

company that has changed its mix of debt and equity. Thus, the measurement of how

well the assets have been employed is not influenced by how the assets were financed.

Note that the interest expense is placed on an after-tax basis by multiplying it by the

factor (1 2 Tax rate).

The return on total assets for Brickey Electronics for year 2 is computed as follows

(from Exhibits 13–1 and 13–2):

AVERAGE TOTAL ASSETS

Net income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Add back interest expense: $640,000 3 (1 2 0.30) . . . . . . . . . . . .

$ 1,750,000

448,000

Total (a) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

$ 2,198,000

Assets, beginning of year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Assets, end of year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

$28,970,000

31,500,000

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

$60,470,000

Average total assets: $60,470,000 4 2 (b) . . . . . . . . . . . . . . . . . . . .

Return on total assets, (a) 4 (b) . . . . . . . . . . . . . . . . . . . . . . . . . . . .

$30,235,000

7.3%

Brickey Electronics earned a return of 7.3% on average assets employed over the

last year.

Return on Common Shareholders’ Equity

One of the primary reasons for operating a corporation is to generate income for the benefit of the common shareholders. One measure of a company’s success in this regard is the

return on common shareholders’ equity, which divides the net income remaining for

common shareholders by the average common shareholders’ equity for the year. The

formula is as follows:

Net income 2 Preferred dividends

Return on common

5

shareholders’ equity Average common shareholders’ equity

where

Average common

Average total shareholders’ equity

5

shareholders’ equity

2 Average preferred shares

“How Well Am I Doing?”—Financial Statement Analysis

619

For Brickey Electronics, the return on common shareholders’ equity is 11.3% for year 2,

as shown below:

Net income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Deduct: Preferred dividends . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

$ 1,750,000

120,000

Net income remaining for common shareholders (a) . . . . . . . . .

$ 1,630,000

Average total shareholders’ equity . . . . . . . . . . . . . . . . . . . . . . . . .

Deduct: Average preferred shares. . . . . . . . . . . . . . . . . . . . . . . . . .

$16,485,000*

2,000,000†

Average common shareholders’ equity (b) . . . . . . . . . . . . . . . . . .

$14,485,000

Return on common shareholders’ equity, (a) 4 (b). . . . . . . . . . .

11.3%

*$15,970,000 1 $17,000,000 5 $32,970,000; $32,970,000 4 2 5 $16,485,000

†$2,000,000 1 $2,000,000 5 $4,000,000; $4,000,000 4 2 5 $2,000,000

Compare the return on common shareholders’ equity above (11.3%) with the return on

total assets computed in the preceding section (7.3%). Why is the return on common

shareholders’ equity so much higher? The answer lies in the principle of financial leverage,

which is discussed in the following section.

When the numerator of a financial ratio contains an amount from the income statement and

the denominator contains an amount derived from the balance sheet, the denominator must

be expressed as an average. This averaging process is done because the income statement

summarizes performance for a period of time, whereas the balance sheet reflects a company’s financial position at a point in time. The average for a balance sheet account is typically

computed by taking the account’s beginning balance plus the ending balance and dividing

this sum by two.

Financial Leverage

Financial leverage (often called leverage for short) involves acquiring assets with funds

that have been obtained from creditors or from preferred shareholders at a fixed rate of

return. If the assets in which the funds are invested are able to earn a rate of return greater

than the fixed rate of return required by the funds’ suppliers, then the company has

positive financial leverage and the common shareholders benefit.

For example, suppose that Bell Media is able to earn an after-tax return of 12% on its

broadcasting assets. If the company can borrow from creditors at a 10% interest rate to

expand its assets, then the common shareholders can benefit from positive leverage. The

borrowed funds invested in the business will earn an after-tax return of 12%, but the aftertax interest cost of the borrowed funds will be only 7% (5 10% interest rate 3 [1 2 0.30]).

The difference will go to the common shareholders.

We can see this concept in operation in the case of Brickey Electronics. Note from

Exhibit 13–1 that the company’s bonds payable bear a fixed interest rate of 8%. The aftertax interest cost of these bonds is only 5.6% (5 8% interest rate 3 [1 2 0.30]). The company’s assets are generating an after-tax return of 7.3%, as we computed earlier. Since this

return on assets is greater than the after-tax interest cost of the bonds, leverage is positive,

and the difference accrues to the benefit of the common shareholders. This explains, in

part, why the return on common shareholders’ equity (11.3%) is greater than the return on

total assets (7.3%).

Unfortunately, leverage is a double-edged sword. If assets are unable to earn a high

enough rate to cover the interest costs of debt and preferred dividends (negative financial

leverage), the common shareholder suffers.

HELPFUL HINT

620

Chapter 13

Debt and preferred shares are not equally efficient in generating positive leverage because interest on debt is tax-deductible, whereas

preferred dividends are not. This usually makes debt a much more effective source of

positive leverage than preferred shares.

To illustrate this point, suppose that the Nursing Home Corporation of Canada is considering three ways of financing a $100 million expansion of its chain of nursing homes:

THE IMPACT OF INCOME TAXES

1. $100 million from an issue of common shares

2. $50 million from an issue of common shares, and $50 million from an issue of preferred shares bearing a dividend rate of 8%

3. $50 million from an issue of common shares, and $50 million from an issue of bonds

bearing an interest rate of 8%

Assuming that the Nursing Home Corporation of Canada can earn an additional

$15 million each year before interest and taxes as a result of the expansion, the operating results under each of the three alternatives are shown in Exhibit 13–6.

If the entire $100 million is raised from an issue of common shares, then the return to the

common shareholders will be only 10.5%, as shown under alternative 1 in the exhibit. If half

of the funds are raised from an issue of preferred shares, then the return to the common

shareholders increases to 13%, due to the positive effects of leverage. However, if half of the

funds are raised from an issue of bonds, then the return to the common shareholders jumps

to 15.4%, as shown under alternative 3. Thus, long-term debt is much more efficient than

preferred shares in generating positive leverage. The reason for this is that the interest expense on long-term debt is tax-deductible, whereas the dividends on preferred shares are not.

THE DESIRABILITY OF LEVERAGE Because of leverage, having some debt in the

capital structure can substantially benefit the common shareholder. For this reason, most

companies today try to maintain a level of debt that is considered to be normal within the

industry. Many companies, such as commercial banks and other financial institutions,

rely heavily on leverage to provide an attractive return on their common shares.

Book Value per Share

Another statistic frequently used in attempting to assess the well-being of the common

shareholder is book value per share. Book value per share measures the amount that

EXHIBIT 13–6 Leverage from Preferred Shares and Long-Term Debt

Alternatives: $100,000,000 Issue of Securities

Alternative 1:

$100,000,000

Common Shares

Alternative 2:

$50,000,000

Common Shares;

$50,000,000

Preferred Shares

Alternative 3:

$50,000,000

Common Shares;

$50,000,000

Bonds

Earnings before interest and taxes. . . . . . . . . . . . . . . . . . . .

Less: Interest expense (8% 3 $50,000,000) . . . . . . . . . . . .

$ 15,000,000

....... ...—........

$15,000,000

....... .—........

$15,000,000

4,000,000

Net income before taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Less: Income taxes (30%) . . . . . . . . . . . . . . . . . . . . . . . . . . .

15,000,000

4,500,000

15,000,000

4,500,000

11,000,000

3,300,000

Net income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Less: Preferred dividends (8% 3 $50,000,000) . . . . . . . . .

10,500,000

...... .. —........

10,500,000

4,000,000

7,700,000

..... ...—........

Net income remaining for common shareholders (a) . . .

$ 10,500,000

$ 6,500,000

$ 7,700,000

Common shareholders’ equity (b). . . . . . . . . . . . . . . . . . . .

$100,000,000

$50,000,000

$50,000,000

Return on common shareholders’ equity (a) 4 (b) . . . . .

10.5%

13.0%

15.4%

“How Well Am I Doing?”—Financial Statement Analysis

would be distributed to holders of each common share if all assets were sold at their balance sheet carrying amounts (i.e., book values) and if all creditors were paid off. Thus,

book value per share is based entirely on historical costs. The formula for computing it is

as follows:

Common shareholders’ equity

Number of common shares outstanding

Total shareholders’ equity 2 Preferred shares

5

Number of common shares outstanding

Book value per share 5

Total shareholders’ equity (see Exhibit 13–1) . . . . .

Deduct preferred shares (see Exhibit 13–1). . . . . . .

$17,000,000

2,000,000

Common shareholders’ equity. . . . . . . . . . . . . . . . . .

$15,000,000

The book value per share of Brickey Electronics’ common shares is computed as follows:

$15,000,000

5 $30 per share

500,000 shares

If this book value is compared with the $40 market value of Brickey Electronics’ shares,

then the shares appear to be somewhat overpriced. However, as we discussed previously,

market prices reflect expectations about future earnings and dividends, whereas book

value largely reflects the results of events that occurred in the past. Ordinarily, the market

value of a share exceeds its book value. For example, in a recent year, Microsoft’s common

shares often traded at over 4 times their book value, and Coca-Cola’s market value was

over 17 times its book value.

To illustrate the computation and interpretation of financial ratios that are used to assess the company’s performance from the standpoint of its shareholders, consider Tim

Hortons, Inc. The data set forth below relate to the year ended December 30, 2012.

(Averages were computed by adding together the beginning- and end-of-year amounts

reported on the balance sheet, and dividing the total by two.)

Net income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Interest expense . . . . . . . . . . . . . . . . . . . . . . . . . .

Tax rate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Average total assets . . . . . . . . . . . . . . . . . . . . . . .

Preferred share dividends. . . . . . . . . . . . . . . . . .

Average common shareholders’ equity. . . . . . .

Common shares dividends per share . . . . . . . .

Earnings per share. . . . . . . . . . . . . . . . . . . . . . . .

Market price per share—end-of-year . . . . . . . .

Book value per share—end-of-year . . . . . . . . .

$402.8 million

$33.7 million

27.7%

$2,244 million

$0 million

$1,172.2 million

$0.84

$2.60

$48.58

$2.84

$402.8 1 3 $33.7 3 11 2 0.2772 4

5 19%

$2,244

$402.8 2 $0

Return on common

5 34.4%

5

shareholders’ equity

$1,172

$0.84

Dividend payout ratio 5

5 32.3%

$2.60

$0.84

5 0.57%

Dividend yield ratio 5

$48.58

Return on total assets 5

621

622

Chapter 13

The return on common shareholders’ equity of 34.4% is higher than the return on total

assets of 19%, and therefore the company has positive financial leverage. (About half of the

company’s financing is provided by creditors; the rest is provided by common and preferred shareholders.)

Ratio Analysis—The Short-Term Creditor

LO2

• Know

• Apply

CC3: Compute and interpret financial

ratios used to measure short-term

creditors’ well-being.

Short-term creditors, such as suppliers, want to be repaid on time. Therefore, they focus

on the company’s cash flows and on its working capital, since these are the company’s primary sources of cash in the short run.

Working Capital

The excess of current assets over current liabilities is known as working capital. The

working capital for Brickey Electronics is computed as follows:

Working capital 5 Current assets 2 Current liabilities

Year 2

Year 1

Current assets. . . . . . . . . .

Current liabilities . . . . . . .

$15,500,000

7,000,000

$16,470,000

5,000,000

Working capital . . . . . . . .

$ 8,500,000

$11,470,000

The amount of working capital available to a firm is of considerable interest to shortterm creditors, since it represents assets financed from long-term capital sources that do not

require near-term repayment. Therefore, the greater the working capital, the greater the

cushion of protection available to short-term creditors, and the greater the assurance that

short-term debts will be paid when due.

Although it is always comforting to short-term creditors to see a large working capital balance, a large balance by itself is no assurance that debts will be paid when due.

Rather than being a sign of strength, a large working capital balance may simply mean

that obsolete inventory is being accumulated. Therefore, to put the working capital figure into proper perspective, it must be supplemented with other analytical work. The

following four ratios (the current ratio, the acid-test ratio, the accounts receivable turnover, and the inventory turnover) should all be used in connection with an analysis of

working capital.

Current Ratio

The elements involved in the computation of working capital are frequently expressed in

ratio form. A company’s current assets divided by its current liabilities is known as the

current ratio:

Current ratio 5

Current assets

Current liabilities

For Brickey Electronics, the current ratios for year 1 and year 2 are computed as follows:

Year 2

Year 1

$15,500,000

5 2.21 to 1

$7,000,000

$16,470,000

5 3.29 to 1

$5,000,000

“How Well Am I Doing?”—Financial Statement Analysis

Although widely regarded as a measure of short-term debt-paying ability, the current

ratio must be interpreted with great care. On the one hand, a declining ratio, as seen above,

might be a sign of a deteriorating financial condition. On the other hand, it might be the

result of eliminating obsolete inventories or other stagnant current assets. An improving ratio might be the result of an unwise stockpiling of inventory, or it might indicate an improving financial situation. In short, the current ratio is useful but tricky to interpret. To avoid a

blunder, the analyst must take a hard look at the individual assets and liabilities involved.

The general rule of thumb calls for a current ratio of 2 to 1. This rule is subject to many

exceptions, depending on the industry and the firm involved. Some industries can operate

quite successfully with a current ratio of slightly over 1 to 1. The adequacy of a current

ratio depends heavily on the composition of the assets. For example, as we see in the table

below, both Worthington Corporation and Greystone Inc. have a current ratio of 2 to 1.

However, they are not in a comparable financial condition. Greystone is likely to have difficulty meeting its current financial obligations because almost all of its current assets

consist of inventory, rather than more liquid assets, such as cash and accounts receivable.

Worthington

Corporation

Greystone,

Inc.

Current assets:

Cash. . . . . . . . . . . . . . . . . . . . . .

Accounts receivable, net. . . . .

Inventory . . . . . . . . . . . . . . . . .

Prepaid expenses . . . . . . . . . . .

$ 25,000

60,000

85,000

5,000

$ 2,000

8,000

160,000

5,000

Total current assets (a) . . . . . . . .

$175,000

$175,000

Current liabilities (b). . . . . . . . . .

$ 87,500

$ 87,500

Current ratio, (a) 4 (b). . . . . . . .

2 to 1

2 to 1

Acid-Test (Quick) Ratio

The acid-test (quick) ratio is a much more rigorous test of a company’s ability to meet its

short-term debts. Inventories and prepaid expenses are excluded from total current assets,

leaving only the more liquid (or “quick”) assets to be divided by current liabilities:

Acid-test ratio 5

Cash 1 Marketable securities 1 Current receivables*

Current liabilities

*Current receivables include both accounts receivable and any short-term notes receivable.

The acid-test ratio is designed to measure how well a company can meet its obligations

without having to liquidate or depend too heavily on its inventory. Since inventory may be

difficult to sell in times of economic stress, it is generally felt that to be properly protected,

each dollar of liabilities should be backed by at least $1 of quick assets. Thus, an acid-test

ratio of 1 to 1 is usually viewed as adequate.

The acid-test ratios for Brickey Electronics for year 1 and year 2 are computed below:

Year 2

Year 1

Cash (see Exhibit 13–1) . . . . . . . . . . . . . . . . . . . . . . . .

Accounts receivable (see Exhibit 13–1) . . . . . . . . . . .

$1,200,000

6,000,000

$2,350,000

4,000,000

Total quick assets (a) . . . . . . . . . . . . . . . . . . . . . . . . . . .

$7,200,000

$6,350,000

Current liabilities (see Exhibit 13–1) (b) . . . . . . . . . .

$7,000,000

$5,000,000

Acid-test ratio, (a) 4 (b) . . . . . . . . . . . . . . . . . . . . . . . .

1.03 to 1

1.27 to 1

623

624

Chapter 13

Although Brickey Electronics has an acid-test ratio for year 2 that is within the acceptable range, an analyst might be concerned about several disquieting trends revealed on the company’s balance sheet. Note in Exhibit 13–1 that short-term debts are

rising, while the cash position seems to be deteriorating. Perhaps the weakened cash

position is a result of the greatly expanded volume of accounts receivable. One wonders why the accounts receivable have been allowed to increase so rapidly in so brief

a time.

In short, as with the current ratio, the acid-test ratio should be interpreted with one eye

on its basic components.

Accounts Receivable Turnover

The accounts receivable turnover is a rough measure of how many times a company’s

accounts receivable have been turned into cash during the year. It is frequently used in

conjunction with an analysis of working capital, since a smooth flow from accounts receivable into cash is an important indicator of the quality of a company’s working capital

and is critical to the company’s ability to operate. The accounts receivable turnover is

computed by dividing sales on account (that is, credit sales) by the average accounts receivable balance for the year:

Accounts receivable turnover 5

Sales on account

Average accounts receivable balance

Assuming that all sales for the year were on account, the accounts receivable turnover

for Brickey Electronics for year 2 is computed as follows:

$52,000,000

Sales on account

5

5 10.4 times

Average accounts receivable balance

$5,000,000*

*$4,000,000 1 $6,000,000 5 $10,000,000; $10,000,000 4 2 5 $5,000,000 average

The turnover figure can then be divided into 365 to determine the average number of

days being taken to collect an account (known as the average collection period):

Average collection period 5

365 days

Accounts receivable turnover

The average collection period for Brickey Electronics for year 2 is computed as follows:

365 days

5 35 days

10.4 times

This simply means that on average, it takes 35 days to collect on a credit sale. Whether

the average of 35 days taken to collect an account is good or bad depends on the credit

terms Brickey Electronics is offering its customers. If the credit terms are 30 days, then a

35-day average collection period would usually be viewed as very good. Most customers

will tend to withhold payment for as long as the credit terms will allow and may even go

over a few days. This factor, added to ever-present problems with a few slow-paying customers, can cause the average collection period to exceed normal credit terms by a week or

so and should not cause great alarm.

On the other hand, if the company’s credit terms are 10 days, then a 35-day average collection period is worrisome. The long collection period may result from many old unpaid

accounts of doubtful collectability, or it may be a result of poor day-to-day credit management. The firm may be making sales with inadequate credit checks on customers, or perhaps no follow-ups are being made on slow accounts.

“How Well Am I Doing?”—Financial Statement Analysis

625

Inventory Turnover

The inventory turnover ratio measures how many times a company’s inventory has been

sold and replaced during the year. It is computed by dividing the cost of goods sold by the

average level of inventory on hand:

Inventory turnover ratio 5

Cost of goods sold

Average inventory balance

The average inventory figure is the average of the beginning and ending inventory figures. Since Brickey Electronics has a beginning inventory of $10,000,000 and an ending

inventory of $8,000,000, its average inventory for the year is $9,000,000. The company’s

inventory turnover ratio for year 2 is computed as follows:

Cost of goods sold

$36,000,000

5

5 4 times

Average inventory balance

$9,000,000

The number of days being taken to sell the entire inventory one time (called the

average sale period) can be computed by dividing 365 by the inventory turnover figure:

365 days

Inventory turnover

365

5

4 times

1

5 91 days

4

Average sale period 5

The average sale period varies from industry to industry. Grocery stores tend to turn

their inventory over very quickly, perhaps as often as every 12 to 15 days. On the other

hand, jewellery stores tend to turn their inventory over very slowly, perhaps only a couple

of times each year.

If a firm has a turnover that is much slower than the average for its industry, then it may

have obsolete goods on hand, or its inventory stocks may be needlessly high. Excessive

inventories tie up funds that could be used elsewhere in operations. Managers sometimes

argue that they must buy in very large quantities to take advantage of the best discounts

being offered. But these discounts must be carefully weighed against the added costs of

insurance, taxes, financing, and risks of obsolescence and deterioration that result from

carrying added inventories.

Inventory turnover has been increasing in recent years as companies have adopted justin-time (JIT) methods. Under JIT, inventories are purposely kept low, and thus a company

utilizing JIT methods may have a high inventory turnover as compared with other companies. Indeed, one of the goals of JIT is to increase inventory turnover by systematically reducing the amount of inventory on hand.

The information in the table below is available to two companies, Mackey Corporation and

Crocus Corporation. In addition to the information in the table, assume the following:

a. On average, 60% of Mackey’s sales are on credit; for Crocus, this ratio is 40%.

b. Numbers presented in the table below are reasonably steady year-over-year for the last

four years.

Required:

Compute all the ratios that short-term creditors are most likely to use to guide their analysis

of Mackey Corporation and Crocus Corporation.

WORKING IT OUT

626

Chapter 13

A

B

1

2

3

C

D

E

F

G

MACKEY CORPORATION

Selected Financial Data

Assets and Liabilities as at December 31, 2014; Income Statement Data for the Year Ended December 31, 2014

4

5

Current Assets:

Current Liabilities:

6

Cash

7

Accounts receivable, net

$ 386,000

245,600

Accounts payable

$176,800

8

Inventory

458,000

Accrued payables

355,600

9

Prepaid expenses

12,500

10

Notes payable, short-term

86,700

$ 1,102,100

$ 619,100

11

12

Sales

13

Cost of goods sold

14

Gross margin

$ 6,348,800

4,965,800

$1,383,000

15

16

17

CROCUS CORPORATION

18

Selected Financial Data

19

Assets and Liabilities as at December 31, 2014; Income Statement Data for the Year Ended December 31, 2014

20

21

Current Assets

Current Liabilities:

22

Cash

23

Accounts receivable, net

$1,836,000

764,500

Accounts payable

24

Inventory

354,000

Accrued payables

855,600

25

Prepaid expenses

121,600

Notes payable, short-term

578,600

26

$2,176,800

$3,076,100

$3,611,000

27

28

Sales

29

Cost of goods sold

$9,634,800

30

Gross margin

5,647,800

$3,987,000

Solution

The ratios are presented in the table; detailed calculations are shown below the table for

Mackey Corporation. A quick comparison based on the ratios suggests that even though

Crocus has a higher gross margin, Mackey Corporation is a better performer with respect to

four out of six ratios listed below. Crocus is a better performer in terms of inventory turnover

and average sale period.

A

B

C

D

1

2

3

Mackey

Crocus

4

5

Working capital

6

Current ratio

1.8

0.9

7

Acid-test (quick) ratio

1.0

0.7

8

Accounts receivable turnover

15.5

5.0

9

Average collection period

23.5

72.4

10

Inventory turnover

10.8

16.0

11

Average sale period

33.7

22.9

12

$483,000 $(534,900)

“How Well Am I Doing?”—Financial Statement Analysis

627

Working capital 5 $1,102,100 2 $619,100 5 $483,000

Current ratio 5

$1,102,100

Current assets

< 1.8

5

Current liabilities

$619,800

Cash 1 Marketable securities 1 Current receivables

Current liabilities

$386,000 1 $245,000

< 1.0

5

$619,800

Acid-test ratio 5

Sales on account

Average accounts receivable balance

60% 3 $6,348,800

< 15.5 times

5

$245,600

Accounts receivable turnover 5

Average collection period 5

Inventory turnover ratio 5

Average sale period 5

365 days

365 days

5

< 23.5 days

Accounts receivable turnover

15.5 times

Cost of goods sold

$5,647,800

< 10.8

5

Average inventory balance

$458,000

365 days

365 days

5

< 33.7 days

Inventory turnover

10.8 times

VICE-PRESIDENT OF SALES

DECISION POINT

Although its credit terms require payment within 30 days, your company’s average collection

period is 33 days. A major competitor has an average collection period of 27 days. You have

been asked to explain why your company is not doing as well as the competitor. You have

investigated your company’s credit policies and procedures, and have concluded that they are

reasonable and adequate under the circumstances. What rationale would you consider to

explain why (1) the average collection period of your company exceeds the credit terms and

(2) the average collection period of your company is longer than that of its competitor?

Note to student: See Guidance

Answers online.

1. Total sales at a store are $1,000,000, and 80% of those sales are on credit. The beginning

and ending accounts receivable balances are $100,000 and $140,000, respectively. What

is the accounts receivable turnover?

a. 3.33

c. 8.33

b. 6.67

d. 10.67

CONCEPT CHECK

Note to student: See Guidance

Answers online.

2. A retailer’s total sales are $1,000,000, and the gross margin percentage is 60%. The beginning and ending inventory balances are $240,000 and $260,000, respectively. What is

the inventory turnover?

a. 1.60

c. 3.40

b. 2.40

d. 3.60

Ratio Analysis—The Long-Term Creditor

The position of long-term creditors differs from that of short-term creditors in that they

are concerned with both the near-term and the long-term ability of a firm to meet its commitments. They are concerned with the near term, since the interest they are entitled to is

normally paid on a current basis. They are concerned with the long term, since they want

to be fully repaid on schedule.

LO2

• Know

• Apply

CC4: Compute and interpret financial

ratios used to measure long-term

creditors’ well-being.

628

Chapter 13

Since the long-term creditor is usually faced with greater risks than the short-term

creditor is, firms are often required to agree to various restrictive covenants, or rules, for

the long-term creditor’s protection. Examples of such restrictive covenants include the

maintenance of minimum working capital levels and restrictions on payment of dividends

to common shareholders. Although these restrictive covenants are in widespread use, they

are a poor second to adequate future earnings from the point of view of assessing protection and safety. Creditors do not want to go to court to collect their claims; they would

much prefer to base the safety of their claims for interest and eventual repayment of principal on an orderly and consistent flow of funds from operations.

Times Interest Earned Ratio

The most common measure of a firm’s ability to protect the long-term creditor is the times

interest earned ratio. It is computed by dividing earnings before interest expense and income taxes (i.e., net operating income) by the yearly interest charges that must be met:

Times interest earned ratio 5

Earnings before interest expense and income taxes

Interest expense

For Brickey Electronics, the times interest earned ratio for year 2 is computed as follows:

$3,140,000

5 4.9 times

$640,000

Earnings before income taxes must be used in the computation, since interest expense

deductions come before income taxes are computed. Creditors have first claim on earnings. Only those earnings remaining after all interest charges have been provided for are

subject to income taxes.

Generally, earnings are viewed as adequate to protect long-term creditors if the times

interest earned ratio is 2 or more. Before making a final judgment, however, it is necessary

to look at a firm’s long-term trend of earnings and evaluate how vulnerable the firm is to

cyclical changes in the economy.

Debt-to-Equity Ratio

Long-term creditors are also concerned with keeping a reasonable balance between the

portion of assets provided by creditors and the portion of assets provided by the

shareholders of a firm. This balance is measured by the debt-to-equity ratio, which is

calculated for Brickey Electronics in the table below:

Debt-to-equity ratio 5

Total liabilities

Shareholders’ equity

Year 2

Year 1

Total liabilities (a) . . . . . . . . . . . . . . . . . . . . . . . . . .

$14,500,000

$13,000,000

Shareholders’ equity (b) . . . . . . . . . . . . . . . . . . . . .

$17,000,000

$15,970,000

Debt-to-equity ratio, (a) 4 (b). . . . . . . . . . . . . . . .

0.85 to 1

0.81 to 1

The debt-to-equity ratio indicates the amount of assets being provided by creditors for

each dollar of assets being provided by the owners of a company. In year 1, creditors of

Brickey Electronics were providing 81 cents of assets for each $1 of assets being provided

by shareholders; the figure increased only slightly to 85 cents by year 2.

Creditors would like the debt-to-equity ratio to be relatively low. The lower the ratio,

the greater is the amount of assets being provided by the owners of a company and the

greater is the buffer of protection to creditors. By contrast, common shareholders would

like the ratio to be relatively high, since through leverage, common shareholders can benefit from the assets being provided by creditors.

“How Well Am I Doing?”—Financial Statement Analysis

629

In most industries, norms have developed over the years that serve as guides to firms in

their decisions as to the “right” amount of debt to include in the capital structure. Different

industries face different risks. For this reason, the level of debt appropriate for firms in one

industry is not necessarily a guide to the level of debt appropriate for firms in another.

3. Total assets are $1,500,000, and shareholders’ equity is $900,000. What is the debtto-equity ratio?

a. 0.33

c. 0.60

b. 0.50

d. 0.67

CONCEPT CHECK

Note to student: See Guidance

Answers online.

Summary of Ratios and Sources of Comparative Ratio Data

Exhibit 13–7 contains a summary of the ratios discussed in this chapter. The formula for

each ratio and a summary comment on each ratio’s significance are included in the exhibit.

Exhibit 13–8 contains a listing of published sources that provide comparative ratio data

organized by industry. These sources are used extensively by managers, investors, and

EXHIBIT 13–7 Summary of Ratios

Ratio

Formula

Significance

Gross margin percentage

Gross margin 4 Sales

Broadly measures profitability

Earnings per share

(of common shares)

(Net income 2 Preferred dividends) 4 Average

number of common shares outstanding

Tends to have an effect on the market price per

share, as reflected in the price–earnings ratio

Price-earnings ratio

Market price per share 4 Earnings per share

Shows whether a share is relatively cheap or relatively

expensive in relation to current earnings

Dividend payout ratio

Dividends per share 4 Earnings per share

Shows whether a company pays out most of

its earnings in dividends or reinvests the

earnings internally

Dividend yield ratio

Dividends per share 4 Market price per share

Shows the return in terms of cash dividends being

provided by a share

Return on total assets

{Net income 1 [Interest expense 3

(1 2 Tax rate)]} 4 Average total assets

Measures how well assets have been employed by

management

Return on common

shareholders’ equity

(Net income 2 Preferred dividends)

4 Average common shareholders’ equity

(Net income 2 Preferred dividends) 4

(Average total shareholders’ equity

2 Average preferred shares)

When compared with the return on total assets,

measures the extent to which financial leverage

is working for or against common shareholders

Book value per share

Common shareholders’ equity 4 Number of

common shares outstanding

(Total shareholders’ equity 2 Preferred shares)

4 Number of common shares outstanding

Measures the amount that would be distributed to