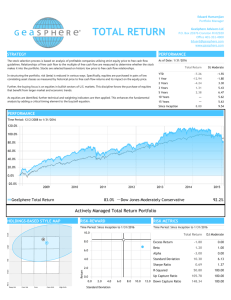

Beating the Market with ETFs and Tactical Asset Allocation

Beating the Market with ETFs and Tactical Asset Allocation

Marvin Appel, M.D., Ph.D.

CEO, Appel Asset Management Corp.

Great Neck, NY www.appelasset.com

516-487-7146

Beating the Market--outline

• Navigating the market: A simple way to optimize risk and reward

• Take the easy way out: The only portfolio you will ever need for long term investing

• Where the money is: Relative strength as a tactical asset allocation tool.

• Conclusion—Some new ETFs that look promising.

A Simple Way to Measure Risk

240

220

200

180

160

140

120

100

80

Growth of $100

3/10/99-3/10/2000

Nasdaq 100 Tracking Stock (QQQQ)

First Eagle Global (SGENX)

200

150

100

50

0

400

350

300

250

Growth of $100

3/10/99-2/27/2007

Nasdaq 100 Tracking

Stock (QQQQ)

First Eagle Global

(SGENX)

120

115

110

105

100

11722 on Jan. 14, 2000

95

90

85

Dow Jones

Industrial Average

80

75

70 x100

1999 2000

7286 on Oct. 9, 2002

2001 2002

2000-2002

37.8% drawdown

2003 2004

75

2

70 x100

95

90

85

80

120

115

110

105

100

150

140

130

120

110

100

90

80 iShares MSCI Emerging

Market Index Fund (EEM)

April 2003-May 2006

70

60

50

May-June 2006

26% drawdown

October 2005

12% drawdown

March-April 2005

10% drawdown

July-Aug. 2007

18% drawdown

150

140

130

120

110

100

90

80

70

60

50

40 40

2003

April-May 2004

18% drawdown

2004 2005 2006 2007

155

150

145

140

135

130

125

120

115

110

105

100

95

150

100

50

S&P 500 Index and worst drawdowns

(overall gain 14%/year)

8% drawdown iShares MSCI Emerging

Market Index Fund (EEM)

April 2003-May 2006

(overall gain 40%/year)

7% drawdown

5% drawdown

8% drawdown

6% drawdown

Feb.-March 2007

12% drawdown

9% drawdown

155

150

145

140

135

130

125

120

115

110

105

100

95 x10

90

150

100

July-Aug. 2007

18% drawdown

April-May 2004

18% drawdown

March-April 2005

10% drawdown

2004 2005

October 2005

12% drawdown

May-June 2006

26% drawdown

2006 2007

50

Different areas of the stock market

Market capitalization

• Value of all a company’s shares = market capitalization.

• Large-cap = $10 billion and over

• Small-cap = $2 billion and under

• As a general rule, compared to small-caps, largecap stocks have tended to be

– safer

– slightly less profitable

– Better when the U.S. dollar is weaker (large-caps have more of their earnings from sales abroad)

Value versus growth stocks

• Value stocks appear to be good bargains based on the current situation of the company.

• Growth stocks appear expensive based on the current situation but the price is potentially justified by the future situation.

• As a general rule, compared to growth stocks value stocks have tended to

– Pay higher dividends

– Be less risky

– Gain less during strong market climates

– Hold up better during weak market climates

Value and growth stocks (cont.)

• Industries more likely to have value stocks

– Financials

– Large oil companies

– Utilities

• Industries more likely to have growth stocks

– Technology

– Healthcare

– Consumer discretionary (homebuilding, media, entertainment)

Value

Large-cap

Large-cap value

Growth

Large-cap growth

Small-cap

Small-cap value

Small-cap growth

Diversification:

Improve safety by not putting all your eggs in one basket.

A properly diversified portfolio should have a better balance between risk and reward than any of its individual components

3

2.5

2

Real estate (REIT's)

Small cap value

S&P 500

Diversified

April, 2004:

REIT's lose 14%.

0.5

0

1.5

1

1998-2000: REIT's fall, S&P 500 pulls portfolio higher.

2002: Portfolio loses less than any of its separate components.

REITs and Small-cap Value have not always been more profitable than the S&P 500

70.00%

60.00%

50.00%

REIT fund average

Russell 2000 Value Index

S&P 500 Index Fund

Diversified equity mix

40.00%

30.00%

20.00%

10.00%

0.00%

-10.00%

-20.00%

Diversification in action:

The One-decision portfolio

Cash

60% of income half (30% of total portfolio)

Income half of portfolio

Stock half of portfolio

S&P 500

40% of stock half (20% of total portfolio)

Bonds

40% of income half (20% of total portfolio)

Small cap value

20% of stock half (10% of total portfolio)

REITs

40% of stock half (20% of total portfolio)

Compounded annual gains for the components of the one-decision portfolio 1980-2007

16%

14%

12%

10%

8%

6%

4%

2%

0%

9.0%

6.4%

14.3%

11.5%

12.7%

10.3%

US Bonds T-bills Russell

2000 Value

S&P 500 REITs

11.9% onedecision portfolio onedecision, no cash

0%

-5%

-10%

-15%

-20%

-25%

-30%

-35%

-40%

-45%

Drawdowns of the one-decision portfolio and its components

US Bonds T-bills

Russell

2000 Value S&P 500 REITs onedecision portfolio onedecision, no cash

-9%

-1%

-33%

-45%

-21%

-11%

-16%

0.025

0.02

Risk-adjusted performance

1980-2007

0.015

0.01

0.005

0

US

Bonds

T-bills Russell

2000

Value

S&P 500 REITs onedecision portfolio onedecision, no cash

Implementing the one-decision portfolio

Vanguard portfolio

• 20% S&P 500 Index fund

(VFINX)

• 10% Small-cap value index fund (VISVX)

• 20% REITs (VGSIX)

• 20% U.S. investment grade bonds (VBMFX)

• 30% cash (Vanguard

Prime Money Market or

NJ Tax-exempt money market if tax bracket is above 30%)

ETF/Fund portfolio

• 20% S&P 500 Index ETF

(SPY)

• 10% iShares S&P 600 Value

Index ETF (IJS)

• 20% iShares Cohen & Steers

Realty Majors (ICF)

• 20% U.S. investment grade bonds (AGG)

• 30% Highland Floating Rate

(XLFAX—only through discount brokerage with no load)

Trend-Following Strategies

• Attempt to recognize new long-term trends after they have begun (but early enough to be able to profit)

• Can outperform a broadlybased benchmark when a strong trend is in force.

• Can trail a broadly-based benchmark when the prevailing trend is in the process of changing or when there is no major trend.

240

220

200

180

160

140

120

100

Russell 1000 Value (large cap value)

Russell 1000 Growth (large cap growth)

1.3

1.25

Russell 1000 Value / Russell 1000 Growth

1.2

Rising means value stronger than growth.

Falling means growth stronger than value.

1.15

1.1

1.05

1

0.95

0.9

Sept. 2003-July 2006

Trend favored value.

180

160

140

120

100

240

220

200

Russell 1000 Value (large-cap value)

Russell 1000 Growth (large-cap growth)

Half value / half growth

2000

1800

1600

1400

1200

1000

800

600

400

200

MSCI Emerging Markets Index

MSCI Europe Index

4

3.5

3

2.5

2

1.5

1

0.5

0

0

1988-1994:

Emerging markets stronger

1994-1998:

Europe stronger

Rising = Em. Mkts stronger

Falling = Europe stronger

1998-2007:

Emerging markets stronger

Example: Selecting Which Part of the World in which to Invest

• iShares MSCI Emerging Market ETF (EEM)

• iShares MSCI Japan (EWJ)

• iShares S&P Europe 350 ETF (IEV)

On the last day of each quarter, select the single one of the three ETFs above that gained the most. Hold that for the upcoming quarter.

1800

1600

1400

1200

1000

800

600

400

200

0

Emerging Mkts

Europe

Japan

Active strategy average

Source: http://www.mscibarra.com

200

150

100

50

0

450

400

350

300

250

EEM

MSCI Em. Mkt

IEV

MSCI Europe

EWJ

MSCI Japan

Emerging markets: index and ETF

Europe: index and ETF

Japan: index and ETF

500000

450000

400000

350000

300000

250000

200000

150000

100000

50000

0

Hypothetical Growth of $10,000 1979-2008

Using Russell 1000 Value, Russell 1000 Growth

Russell 2000 Value, Russell 2000 Growth

Top 2 styles each quarter

Top style each quarter

Average of four styles

Implementing the U.S. Equity

Style Allocation Model

• iShares Russell 1000 Value ETF (IWD)

• iShares Russell 1000 Growth ETF (IWF)

• iShares Russell 2000 Value ETF (IWN)

• iShares Russell 2000 Growth ETF (IWO)

Advanced strategy

• Use iShares S&P 500 Growth ETF (IVW) and S&P 600 Growth ETF (IJT) instead of

IWF and IWO.

Current model recommendations for the first quarter of 2008

• Among U.S. equity investment styles, small and large cap growth are selected (IJT and

IVW)

• Among foreign markets, emerging markets are selected (EEM)

New ETFs That Can

Work for You.

Future investment results cannot be guaranteed.

Pros and cons of new ETFs

• New asset classes

(commodities and currencies).

• More international exposure.

• Higher dividend income

(Wisdom Tree, iShares DVY and PFF)

• New indexing methodologies might perform better than float weighting in certain investment climates

– Equal weighting (Rydex)

– Fundamental weighting (Wisdom

Tree)

• Specialized funds (PHO)

• Lower liquidity

• Higher expenses than original ETFs

• Unproven methods of index construction.

• Little real-time trading experience.

• Less transparency

(proprietary indexes such as Claymore,

Power Shares)

Promising New ETFs

• Exchange-traded Notes (ETNs) for commodity and currency exposure

• Investment income

– Equities with high dividend yields

– High-yield bond ETFs: PFF and HYG

– Tax-free bonds

iPath Exchange-Traded Notes (ETNs)

• These track investments that you otherwise could not buy or short directly.

• ETNs track a variety of commodity indexes and foreign currencies.

• Unlike ETFs, ETNs do not represent proportional ownership of a portfolio. Rather, ETNs are derivatives with Barclays as the counter-party.

• For now, ETNs enjoy better tax treatment if held for more than a year.

• Commodity ETNs have an expense ratio of

0.45%.

Example—DJ AIG Commodity

Index Total Return

• Goal is to match the return of an unleveraged investment in the underlying future including interest on cash collateral.

Energy

8%

9%

34%

Agriculture

16%

33%

Industrial metals

Precious metals

Livestock

59

57

55

53

51

49

47

45

DJP has closely tracked its benchmark iPath ETN (DJP, left scale)

DJ-AIG Commodity Index plus interest less 0.75%/yr (right scale)

206

196

186

176

166

156

30

25

20

15

10

5

0

-5

-10

-15

65

60

55

50

45

40

35

An example of poor ETF tracking: USO versus spot crude

Price Change (%) from 12/29/2006 to 1/15/2008

Crude oil spot

US Oil Fund (USO)

35

30

25

20

15

10

-10

-15

5

0

-5

65

60

55

50

45

40

2006 Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 2008

25.0%

20.0%

15.0%

10.0%

5.0%

0.0%

-5.0%

-10.0%

-15.0%

-20.0%

Entire DJ-AIG Index

Agricultural

Industrial Metals

Energy

Mutual Fund Alternatives

• Oppenheimer Commodity Strategies Total

Return (QRAAX)—Active strategies to invest in commodities

• Pimco Commodity Real Return Fund

(PCRAX)—Invests in a passive mix of DJ-

AIG Commodity Index (same as DJP) and

TIPS.

250.00

200.00

150.00

100.00

50.00

0.00

Oppenheimer (QRAAX)

Pimco (PCRAX)

DJP (back-generated)

ETFs for Investment Income

• Preferred stocks: PFF has yielded 7%/year so far.

• High-yield foreign and U.S. stock ETFs from Wisdom Tree yield more than 5%/year

• Bonds

– Junk bonds (iShares HYG)

– Muni bonds (TFI, MUB)

5

0

-5

Preferred Stock ETF (PFF)

-10

Financial Sector SPDR (XLF)

-15

-20 Price changes since 3/30/20007

(%,excluding dividends)

-25

2007 May June July August September November December2008

5

0

-5

-10

-15

-20

-25

Selected Wisdom Tree Funds

• High Yield Emerging Market (DEM)—Energy, materials, telecom (yield 5.4%, expense 0.6%)

• Pacific Ex-Japan High Yield (DNH)—Mainly

Australian/New Zealand banks (yield 5.5%, expense 0.6%)

• Small-cap Dividend Fund (DES)—Majority financials (yield 5.9%, expense 0.4%) source: http://www.wisdomtree.com/etfs/estimated-dividend-yield.asp

High-Yielding Emerging Market Stocks

(DEM)—not overweighted in financials

Total Return (%) 7/13/2007-2/1/2008

20%

15%

10%

5%

0%

-5%

-10%

-15%

-20%

Wisdom Tree HY Emerging Market (DEM) iShares MSCI Emerging Market (EEM)

Less volatile compared to EEM (but history is very short).

80%

70%

60%

50%

40%

30%

20%

10%

0%

Watch your style exposure

Total Return (%) 6/2006 - 1/2008

Wisdom Tree Pacific ex-Japan High Yield (DNH) iShares Pacific ex-Japan (EPP)

Both EPP and DNH are heavily weighted in Austrialian banks.

High dividends from small caps

25%

0%

-5%

-10%

20%

15%

10%

5%

Wisdom Tree Small Cap Dividend (DES) iShares Russell 2000 Value (IWN)

DES: 56% financials, IWN 34% financials. Yet, the investment behavior has been very similar (6/19/2006-2/1/2008)

Municipal Bond ETFs—Low costs should be a big advantage.

• iShares S&P National Muni Fund (MUB)—expenses

0.25%, SEC yield 3.4%, average maturity 8.9 years, 56 holdings.

• SPDR Lehman Muni Bond ETF (TFI)—expenses 0.2%,

SEC yield 3.3%, average maturity 9.3 years, 81 holdings.

• Tough competition: Vanguard Intermediate-term

Tax Exempt (VWITX)—Same yield, lower expenses, less interest rate risk, more diversification-expenses

0.15%, SEC yield 3.4%, average maturity 6.7 years,

1365 holdings

Miscellaneous ETFs

• Water resources (unavailable as a mutual fund)

• Utilities

– Large-cap: stick to basics

– Small-cap: Use Rydex Equal-Weight (RYU)

Water resources—a unique ETF (PHO) that is like a mutual fund in disguise.

50%

PowerShares Water

Portfolio (PHO) 40%

30% iShares S&P 400 Growth

Index ETF (IJK)

20%

10%

0%

-10%

0.7% expense ratio. Tracks the Palisades Water Index (?), whose component stocks are mostly mid-cap and small-cap growth.

Sometimes simple is best (utilities)

15%

10%

5%

0%

-5%

40%

35%

30%

25%

20%

Total Return (%) in Two U.S. Large-Cap

Utilities Sector ETFs, 9/21/2006-2/1/2008

PowerShares FTSE/RAFI Utilities (PRFU)

Utilities Sector SPDR (XLU)

Expenses: 0.23% for XLU; 0.75% for PRFU

For a free trial to our bi-weekly market newsletter,

Systems and Forecasts , visit us at www.systemsandforecasts.com

Appel Asset Management Corp.

www.appelasset.com