Recent Successful Sales of Plaskolite and Nudo

advertisement

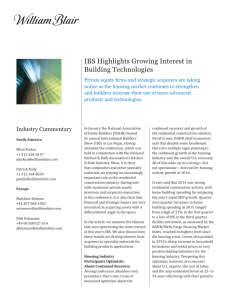

Recent Successful Sales of Plaskolite and Nudo Highlight Growing Attractiveness of Specialty Materials for Building Products Applications Amid an ongoing recovery in construction activity, companies offering products or materials in the building products sector are generating strong interest from strategic acquirers and financial investors. Industry Commentary North America Elliot Farkas +1 312 364 8157 efarkas@williamblair.com Samuel Tinaglia +1 312 364 8086 stinaglia@williamblair.com Patrick Nally +1 312 364 8634 pnally@williamblair.com Europe Matthew Zimmer +44 207 868 4502 mzimmer@williamblair.com Dirk Felsmann +49 69 509527 614 dfelsmann@williamblair.com The continued recovery of the construction industry has served as a tailwind for growth of manufacturers and distributors of building products. This growth has been particularly strong for composites and other specialty materials that offer greater value from superior performance attributes and lower total lifecycle costs. As a result, companies offering these differentiated building products are generating widespread interest from strategic acquirers and financial sponsors alike. William Blair has recently completed two transactions that illustrate this trend, advising Plaskolite, Inc. on its sale to Charlesbank Capital Partners and Nudo Products, Inc. (NPI) on its sale to Grupo Verzatec, the parent company of Glasteel and Stabilit America. Since 2012, William Blair has completed 26 transactions in the building products and specialty materials sectors. In this article, we examine trends driving growth of the specialty materials and building products industries and the characteristics of companies in those industries that are receiving premium valuations. We also provide an overview of the Plaskolite and NPI transactions and identify the value drivers within these specific transactions. Overview of Specialty Building Products Specialty building products companies provide composites or other specialty materials that offer superior performance, strength, and/or durability, resulting in an improved value proposition over the product’s entire lifecycle. Often through proprietary material science, production technologies or services, these companies offer products that provide benefits to builders and contractors such as easier installation, reduced maintenance, improved weather resistance, or enhanced color retention. Because of these differentiated, valuable attributes and the associated superior market position, specialty building products companies have significantly outperformed companies selling general or commodity building products over the past decade and have superior financial profiles, making them more attractive investments for both strategic acquirers and financial sponsors. During the recession, specialty building products companies experienced a more moderate decline and a quicker, stronger recovery than general or commodity building products companies. Since 2005, stock prices for publicly traded specialty building products manufacturers are up 135%, compared with 35% for manufacturers of general building products. We typically see specialty building products companies with longer-term revenue growth of 10%plus and consistent profitability in excess of approximately 15% EBITDA margins. Tailwinds for Growth The construction industry is in the midst of an ongoing postrecession recovery. Residential and nonresidential construction activity is trending up, yet remains well below pre-recession peaks. Activity in both segments is expected to see continued growth through 2019. With the housing market leading the way, the construction industry appears to provide more attractive growth prospects than the broader U.S. economy. The Commerce Department reported that housing starts in November jumped to 1.17 million units. This marked the eighth consecutive month of more than 1 million housing starts, the longest stretch since 2007. In addition, President Obama’s signing of a five-year, $305 billion highway bill in December 2015 provides a positive backdrop for infrastructure spending. The law, which is the first long-term national transportation spending deal in a decade, calls for $205 billion of spending on highway projects and $48 billion of spending on transit projects. Specialty Building Products Equities Outperform General Building Products and Broader Market As demand for composites and other specialty building products has steadily increased over the past decade, stock prices of manufacturers of specialty products have significantly outperformed general (non-specialty) product manufacturers and the broader equity market. 250 134.8% 200 68.7% 150 34.6% 100 50 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 General Specialty S&P 500 Source: Public filings, FactSet, and Capital IQ as of Dec. 31, 2015. Specialty manufacturers index comprises: Acuity Brands, Apogee Enterprises, Headwaters, James Hardie, PGT Industries, Simpson Manufacturing Company, and Trex. General manufacturers index comprises: American Woodmark, Armstrong, Fortune Brands Home & Security, Gibraltar Industries, Griffon Industries, Lennox International, Masco, Owens Corning, Ply Gem, Nortek, Quanex Building Products, Saint-Gobain, and USG. Value Drivers in Specialty Building Products M&A Within the increasingly attractive specialty building products industry, companies that are able to command premium valuations often have several of the following characteristics: • Differentiated product properties and brands • Materials science capabilities • Scale advantages • Advanced, unique manufacturing capabilities • Entrenched, leading market positions • Organic and/or inorganic growth opportunities • Price leader/pass-through ability • Superior purchasing ability • Top management teams Plaskolite and Nudo Acquisitions Highlight Increased Interest in Premium, Leading Specialty Building Products Assets As a result of the growing market opportunity for specialty building products and the relatively strong financial performance of these companies, strategic acquirers and financial sponsors have been aggressively pursuing acquisition opportunities of this nature. In late 2015, William Blair completed highly successful sale processes for Plaskolite and NPI. Plaskolite Acquired by Charlesbank Capital Partners Not Disclosed has been acquired by November 2015 William Blair advised Plaskolite in connection with the company receiving a controlling investment U.S. Housing Starts (000s of units) Housing starts in November jumped to 1.17 million units. This marked the eighth consecutive month of more than 1 million housing starts, the longest stretch since 2007. Residential activity typically serves as a leading indicator of nonresidential activity. 2,500 1,500 1,000 500 0 1995 2000 2005 2010 Based in Columbus, Ohio, Plaskolite is one of North America’s largest manufacturers of rigid plastic sheet, with the No. 1 market position in most of its core product categories. The company manufactures and sells a broad range of value added ABS, acrylic, polycarbonate, PETG, and polystyrene sheet, along with related sheet coatings and specialty polymers. Plaskolite has world-class, highly automated manufacturing capabilities that enable nimble and safe, run-tosize production. Charlesbank Capital Partners is a private equity firm focused on a broad array of industries, including manufacturing, distribution, media and communications, financial services, energy, healthcare products and services, and consumer products. The transaction provides Plaskolite additional growth capital and financial expertise needed to pursue larger and more international acquisitions, as well as accelerate organic growth initiatives. The acquisition also provided diversification for Plaskolite’s family owners. 2,000 1990 from Charlesbank Capital Partners. The transaction closed on November 3, 2015. Nudo Acquired by Grupo Verzatec 2015 Source: Federal Reserve Bank of St. Louis Not Disclosed Nonresidential Construction Confidence Index The index reflects U.S. construction contractors’ perceptions of the business environment over a six-month period, in addition to the prospects for commercial and industrial construction spending growth. Any number above 50 represents a favorable outlook. ® has been acquired by December 2015 75 70 65 60 55 50 2012 1H 2012 2H 2013 1H Sales Source: Associated Builders and Contractors 2013 2H 2014 1H Profit Margins 2014 2H 2015 1H William Blair advised NPI on its December 2015 sale to Grupo Verzatec. NPI was a portfolio company of RFE Investment Partners. Grupo Verzatec, a Mexico-based strategic acquirer, is the parent company of Stabilit America and Glasteel. Based in Springfield, Illinois, NPI is a leading provider of composite panel solutions primarily for building products applications. NPI’s Marlite brand provides innovative composite sheet and laminated interior panel solutions for commercial markets and is one of the most widely specified decorative wall panel brands. Nudo and Prime Panels provide sheet and laminated functional panels for the building products, signage, transportation, and other commercial markets; the brands are among the largest laminators in the United States. Based in Monterrey, Mexico, Grupo Verzatec is one of the largest producers of highquality fiberglass reinforced plastic (FRP), polyvinyl chloride (PVC), and polycarbonate panels used in the building construction and transportation industries. The acquisition of NPI is highly strategic for Grupo Verzatec. The transaction provides Grupo Verzatec the opportunity to vertically integrate key aspects of its operations and expand its geographic footprint in the United States. The transaction also broadens Grupo Verzatec’s manufacturing capabilities in the decorative and specialty wall panels space and places the company closer to its end-customers by gaining access to Nudo’s extensive architectural specification and distribution network. William Blair’s Leading Building Products and Specialty Materials Franchises Through ongoing dialogue with strategic acquirers and extensive relationships with the most active financial sponsors in the industry, William Blair has developed deep sector expertise in building products and specialty materials. Our understanding of industry trends and buyers’ strategic and financial road maps has allowed us to conduct highly competitive sale processes on behalf of our clients. Since 2014, we have completed 13 M&A transactions in the building products and specialty materials industries. To learn more about trends shaping the deal-making landscape in building products and specialty materials, please do not hesitate to contact us. Selected Building Products and Specialty Materials Transactions Not Disclosed Not Disclosed Not Disclosed has been acquired by has been acquired by has been acquired by December 2015 December 2015 November 2015 Not Disclosed $225,000,000 $110,000,000 has been acquired by has divested its Asian Operations and Brand Name to has been acquired by October 2015 April 2015 February 2015 Not Disclosed $400,000,000 Not Disclosed has been acquired by has been acquired by has been acquired by July 2014 April 2014 November 2014 ® Castle Harlan “William Blair” is a trade name for William Blair & Company, L.L.C., William Blair Investment Management, LLC and William Blair International, Ltd. William Blair & Company, L.L.C. and William Blair Investment Management, LLC are each a Delaware company and regulated by the Securities and Exchange Commission. William Blair & Company, L.L.C. is also regulated by The Financial Industry Regulatory Authority and other principal exchanges. William Blair International, Ltd is authorized and regulated by the Financial Conduct Authority (“FCA”) in the United Kingdom. William Blair only offers products and services where it is permitted to do so. Some of these products and services are only offered to persons or institutions situated in the United States and are not offered to persons or institutions outside the United States. This material has been approved for distribution in the United Kingdom by William Blair International, Ltd. Regulated by the Financial Conduct Authority (FCA), and is directed only at, and is only made available to, persons falling within COB 3.5 and 3.6 of the FCA Handbook (being “Eligible Counterparties” and Professional Clients). This Document is not to be distributed or passed on at any “Retail Clients.” No persons other than persons to whom this document is directed should rely on it or its contents or use it as the basis to make an investment decision.