One step forward, two steps back

advertisement

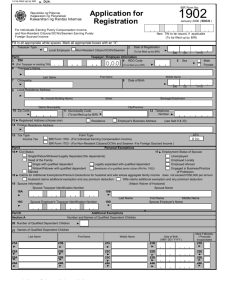

“MAPping The Future” Column in the INQUIRER – 28 November 2011 “One step forward, two steps back: The revised BIR Form 1700” by Anthony Alden S. Aguilar Taxation has never had a good reputation. We need look no further than the example of St. Matthew himself, who was a tax collector before he was called to become one of the Twelve Disciples, and is often held up as an example of a reformed sinner. It also doesn’t help that until as recently as the early 20 th Century, taxes were more often seen as an instrument of oppression and harassment, than as a means to support economic development. By and large, therefore, it is the people’s attitude towards taxation that is perhaps the biggest challenge that a tax agency has to face in its efforts to collect taxes. In recent years, many efforts have been made by the Bureau of Internal Revenue (BIR) to encourage the public’s voluntary compliance with tax laws, and these endeavours have ranged from the re-engineering of tax processes to the development of information programs and strategies. Experience teaches us, however, that one of the most effective ways to get a person to file and pay his taxes is to reduce the so-called “compliance burden” that he must shoulder, that is, the various requirements and processes he must address in the act of paying his taxes. Reducing the compliance burden is the primary reason behind the BIR’s efforts, over the years, to simplify the various tax forms used in the filing and payment of taxes. However, since these forms also serve as the means through which the BIR can obtain information on a taxpayer, the BIR must seek a happy balance between providing the taxpayer with a form that is easy to fill out, and allowing the revenue service to gather as much accurate information as possible from the taxpayer. The recent revision of the 1700 series of income tax forms, however, may yet put this principle to the test. Just how dramatic this revision to the most widely-used tax forms distributed by the BIR can be seen in the fact that Form 1700, the Income Tax Return for Pure Compensation Income Earners, has been transformed into a four-page (two sheets printed back-to-back) document, with one entire page devoted to instructions on how to fill out the form. Setting aside the thought that printing copies of this particular form will surely cost the BIR millions in public funds, perhaps the biggest argument against the use of this revised Form is that it will add to the taxpayer’s compliance burden and negate the BIR’s hard-won efforts over recent years to simplify the tax system’s most important tax forms. A quick glance at Form 1700 – which is accomplished by salaried employees, perhaps the single biggest category of taxpayers – would intimidate most taxpayers with the sheer number of data fields to be read and understood. It is only after the hapless employee has attempted to absorb the instructions on how to fill up the form that he will realize that he may – and this is but an option – no longer have to fill up the form if he qualifies for substituted filing. Then again, however, how many ordinary employees know what “substituted filing” means, and who can be considered as “substituted filers”? The employee will then be compelled to consult with the company’s finance officers, thereby placing an additional burden on both him and the persons he will consult with. Take this situation and multiply it many times over, and one begins to sense the magnitude of the upheaval and inconvenience that the use of the revised Form 1700 will cause throughout the business community and the working public. Let us now presume that, after addressing the challenge of determining whether he is required to use the revised Form 1700, the employee discovers that he is indeed required to use this Form. He now faces an uphill battle in attempting to understand the types of additional income he is supposed to provide information for, to say nothing of trying to gather the data itself. Let us consider as an example the interest income earned from deposit accounts. The ordinary bank depositor will most likely simply entrust to the bank whatever portion of his disposable income he manages to save, and no longer bother to monitor the interest his deposit account earns – and in an age when most banks are discouraging the use of passbooks in order to save on printing costs, many small depositors no longer possess printed information on the movement of their bank accounts. But since data on interest income is required by Form 1700, the employee must then attempt to secure such information from his bank – an action that is yet another addition to his compliance burden. Now that we have seen that Form 1700 will surely increase the compliance burden of the ordinary taxpayer, the question now arises as to whether such onerous consequences are commensurate to the data that the BIR hopes to secure from the use of the revised Form. Where the previous Form 1700 required only information on an employee’s income from his employer, this present incarnation of Form 1700 provides fields for data on what is collectively known as “passive income”, which includes, among others, interest from bank deposits, royalties, proceeds from the sale of real property or from shares of stock sold outside the Philippine Stock Exchange, prizes and other winnings, and dividends. While it is not unknown for some individuals to realize gains from transactions such as these, it is nonetheless true that only a very small margin of the taxpaying public actually earn income from these sources that is significant enough to warrant special attention by the BIR. Indeed, while many of the “working class” endeavour to save money and maintain deposit accounts (as well as the occasional time deposit account), such bank accounts are not of so considerable an amount as to generate interest income that is significant enough to constitute part of a person’s household budget. Given the present value of money and the prevailing interest rates, only deposit accounts in millions of pesos would be able to generate interest income that is significant enough to supplement a family’s income. Gains from transactions involving the sale or exchange of shares of stock should also be seen in a similar light – only those proceeds realized from the sale of a large volume of shares are truly worthy of note by the BIR. How indeed could one compare the few shares of stock distributed by PLDT to its subscribers to the entire blocks of shares held by certain members of Manila’s 400? It may be conjectured that the BIR wishes to acquire more information on the passive income of the country’s wealthier individuals, perhaps as a prelude to efforts aimed at determining whether these well-todo citizens have in fact paid the correct amount of taxes. While this aim is laudable, the means through which it is to be achieved nonetheless leave much to be desired, in terms of practicality, feasibility, and the ultimate benefits to the public and to the government. Indeed, one may well ask whether it is fair to burden the greater majority of the taxpaying public with complicated tax forms simply to obtain data from a select group of citizens. Compelling the public to make use of these revised – and significantly more complex – tax forms will ultimately negate the progress made in previous years to reduce the problems and difficulties of filing and paying taxes. “Magbabayad na nga ako, pahihirapan n’yo pa ako?” Much time and effort has gone into making this taxpayer complaint a thing of the past. Now, however, with the looming implementation of the BIR’s Revenue Memorandum Circular No. 40-2011 mandating the use of the revised 1700 series of forms, this cry of exasperation may yet be heard once again. And in a time when tax revenues are more urgently needed by the Government than ever before, burdening the taxpayer with complicated forms that demand data that is difficult and time-consuming to secure can only dismay and disillusion a public already fed up with “red tape” and all the inefficiency, delays and unreasonable requirements that the phrase entails. It is hard enough to convince people that taxes are not evil. But then again, it is harder convincing taxpayers to part with their hard-earned money and pay their taxes – making the process even more difficult is certainly not a step in the right direction. (The author is a Senior Partner of The Tax Offices of Romero, Aguilar & Associates and member of the MAP National Issues Committee and MAP Task Force for Taxation. Feedback at map@globelines.com.ph. For previous articles, please visit <map.org.ph>) :G\mapping\ mapping - aaguilar - 28November2011 - One step forward, two steps backward.doc:mel