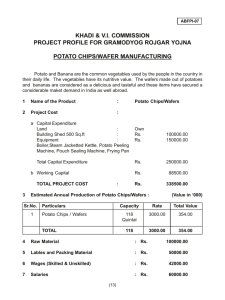

preview case

advertisement

preview case Amaizer: it tastes awful, but we’re working on it Amaizer is a new savoury snack made from maize. Its method of manufacture is similar to Cornflakes breakfast cereal, but it is to be sold as a savoury snack. Amaizers look like potato crisps, but are more golden and regular in shape. Raw materials and manufacturing costs are higher than for potato crisps, but they are healthier – in their basic form, they contain the same calories, but are low in saturates and cholesterol. Amaizer is sweeter than potato crisps, but it can be flavoured. Unfortunately, consumer trials showed that the Amaizer versions of popular crisp flavours – salt and vinegar, cheese and onion, etc. – ‘taste awful’. The R&D department was still working on the taste of these flavours. Meanwhile, the aim was to launch the product with four flavours that consumers did like: regular, sweet and sour, honey roasted ham and ‘1,000 Islands’ dressing. Although originally designed to use spare breakfast cereal capacity, the developed product needed dedicated plant. This produces Amaizer for a direct cost of [***]1,500 per tonne, excluding the cost of capital. With potato snacks selling for [***]3,000 per tonne, the brand manager was confident about the product’s profitability. The brand manager’s confidence crashed, however, when sales, finance and market research each came up with recommended prices. The finance officer demanded that the price be set to cover the usual 100 per cent overhead charge plus a 20 per cent margin. His suggested price of [***]3,600 per tonne gave a very satisfactory [***]180,000 profit for the targeted 300 tonne annual sales. Unfortunately, the finance officer’s view conflicted with the sales manager’s, who wanted the price to be [***]100 per tonne below potato crisps already sold by the company and several competitors. The sales manager claimed that only with a price advantage could they achieve the target sales against the established competition. The sales manager added that a low initial price would also compensate traders for the extra shelf space Amaizer used. Amaizer was bulkier than potato crisps and therefore needed about 20 per cent extra shelf space. The marketing researcher’s contribution to the pricing debate confused the brand manager even more. Rather than giving a price, the researcher gave a string of prices and sales and, to the annoyance of the finance officer, some financial information: Price ([***]000) 2.5 3.0 3.5 4.0 4.5 Sales (tonnes) 400 350 280 200 100 The researcher also estimated [***]300,000 annual fixed operating cost for the product and capital investment that depended upon the annual volumes produced: Annual sales 400 350 280 200 100 2,250 2,000 1,650 1,200 600 (tonnes) Capital investment ([***]000) ‘I assume you know that our average cost of capital is 15 per cent’, commented the finance officer. ‘All very impressive’, said the brand manager, ‘but what price should we charge?’ ‘That all depends on what you want to achieve’, replied the researcher. Questions 1. Evaluate the pricing suggestions of the sales, finance and market research officers. 2. What criteria should be used to select the best price? 3. Calculate the prices that give the highest gross margins, return on investment, economic value added (EVA), net contribution, sales value and sales volume (Marketing Highlight 16.2 shows how to calculate these). Based on these results, what price would you choose and why? What do you notice about the room to manoeuvre around the optimum prices? SOURCES: Adapted from in-company information. Names and figures have been changed for commercial reasons.