Corporate Reorganization

advertisement

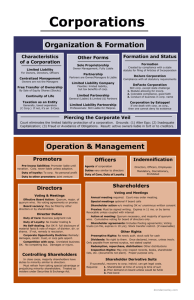

Corporate Reorganization Key in these issues to keep straight who is buying or selling. Is it the Corp., or is it a shareholder. Dissolution o One corporation is involved. o Voluntary dissolution requires a majority vote by shareholders, plus filing with the state. Courts can order involuntary dissolution in certain cases, deadlock, inappropriate use of corp. funds. o Control = majority vote by shareholders o Liability = all present creditors must be paid, but potential future liability is absolved. o Shareholder Rights = all shareholders get pro rata share of residual, no dissenter’s appraisal rights. Sale of Majority of Assets o Requires two corps. X corp. purchases majority of assets from Y corp. o Control X corp., if paying in cash, only management approval required. Y corp. requires approval by majority of shareholders. o Liability X only acquires liabilities that attach to the purchased assets. Y retains it liabilities unless it contracts them to X corp. (w/ appropriate creditor approval). o Shareholder Rights X shareholders have same rights as before, but hopefully a high dividend Y shareholders retain dissenter’s appraisal rights, and pro rata of residual of Y corp. Merger/Consolidation o Requires two corps. One purchases the other, or both dissolve and become a new corp. The law treats them the same. o Control X corp. requires approval by majority of shareholders Y corp. requires approval by majority of shareholders o Liability The surviving, or new, corp. retains all rights and all liabilities (including unknown ones) of both corps. However, the surviving or new corp. can reorganize the equity of the old corp. by eliminating preferred stock and the cumulative dividends that might be owed. o Shareholder Rights X & Y shareholders retain dissenter’s appraisal rights o Short-Form merger. If X corp. owns 90% -95% of Y corp. shares, then X can merge with Y (X surviving) without the approval of X shareholders. Technically, need approval of Y shareholders, but X corp. votes those shares. Freeze-Out o Majority, controlling shareholder(s) wish to purchase the shares of a minority shareholder. Only one corp. is involved. o Control = Controlling majority via that board approves the action. o Liabilities = remain with the corp. o Shareholder rights = even if the offered price is unfair, appraisal rights are the only remedy available. Weinberger v UOP Stock for Assets o Requires 2 corps. X corp buys Y corp assets for X shares. Y then dissolves passing assets (shares in X) to Y shareholders, or is run as essentially a holding company (holding X shares). o Control X corp. management approval Y corp., majority of Y shareholders b/c sale of majority of assets o Liabilities X corp. gets liabilities that attach to the assets. Y retains it liabilities unless it contracts them to X corp. (w/ appropriate creditor approval). o Shareholder Rights X shareholders have same rights as before, but hopefully a high dividend Y shareholders retain dissenter’s appraisal rights, and pro rata of residual of Y corp. Stock for Stock o Requires two corp. X corp. buys shares in Y corp. directly from Y shareholders. Y corp. is then dissolved passing its assets to X corp., Y corp. is merged into X corp. or is run as a subsidiary of X corp. o Control If new stock must be created, a majority of X shareholders are required for the creation. The selling of X stock only requires management approval. Each individual Y shareholder may buy at his will. X corp. usually conditions its offer upon obtaining a controlling percentage of Y shares. o Liabilities Upon the purchase of Y shares, X corp has limited liability in terms of Y corp. X corp. further liability depends upon later actions with Y corp. (is it left as a sub, is it merged, etc.) Y corp. is left with all its liabilities until later actions (is it left as a sub, is it merged, etc.). o Shareholder Rights X shareholders have same rights as before, but hopefully a high dividend Most Y shareholders are now X shareholders. Those who did not sell retain dissenter’s appraisal rights, and will probably be froze out. Tender Offer o Same as stock for stock, except X corp. offers Y shareholders money for their shares. X corp. then has controlling block of Y shares. Y is then dissolved, merged or run as a sub. o Control X corp. usually borrows to finance the purchase, this only needs management approval. The buying of Y stock only requires management approval. Each individual Y shareholder may sell at his will. X corp. usually conditions its offer upon obtaining a controlling percentage of Y shares. o Liabilities Upon the purchase of Y shares, X corp has limited liability in terms of Y corp. X corp. further liability depends upon later actions with Y corp. (is it left as a sub, is it merged, etc.) Y corp. is left with all its liabilities until later actions (is it left as a sub, is it merged, etc.). o Shareholder Rights X shareholders have same rights as before, but hopefully a high dividend Most Y shareholders are no longer shareholders, no rights. Those who did not sell retain dissenter’s appraisal rights, and will probably be froze out. Triangular Merger o Requires at least three corps. X corp. forms X-sub corp. whose only assets are X shares. X-sub then does a Stock for Assets or stock for Stock with Y Corp or Y shareholders. Then Y corp. mergers or dissolves. De Facto Merger Doctrine o Some courts treat stock for stock, stock for assets and triangle, as if it were a true merger. Thus, giving purchaser shareholders dissenter’s rights. This is especially true in an ‘upside-down merger,’ change in business, assumption of liabilities or there is self-dealing. But, many states don’t follow this. Delaware follows the independent legal significance doctrine: if there are two legal ways to combine, then corps may choose b/w them at will. Williams Act o SEA 14(d)(1). Those making a tender offer in hopes of gaining more than 5% of the stock of target must register with the SEC. Offeror must (1) give the background and identity of the bidder (2) the source and amount of the funds being used (3) the plans for the target corp. (4) amount of stock in target already owned (5) details of contracts or arrangements with target shareholders.