Comp SM_Ch03

advertisement

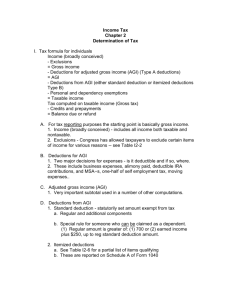

CHAPTER 3 TAX DETERMINATION; PERSONAL AND DEPENDENCY EXEMPTIONS; AN OVERVIEW OF PROPERTY TRANSACTIONS SOLUTIONS TO PROBLEM MATERIALS CHECK FIGURES 28.a. 28.b. 28.c. 28.d. 29. 30. 31.a. 31.b. 31.c. 31.d. 31.e. 32.a. 32.b. 32.c. 32.d. 33.a. 33.b. 33.c. 34.a. 34.b. 34.c. 34.d. 34.e. 35. 36. 37.a. 37.b. 39. $46,600. $37,900. $27,350. $22,350. $19,550. $54,200. $4,850. $3,450. $800. $850. $3,250. Three. Four. Three. Two. Three. Two. Three. Four. Two. Three. Three. Two. $25,420. $67,100. $900. $90. Transferring the duplex saves $2,277. 40.a. $5,390. 40.b. $9,963. 40.c. $13,400. 41. $11,750. 42. 43. 44. 45.a. 45.b. 45.c. 45.d. 46.a. 46.b. 46.c. 46.d. 46.e. 47.a. 47.b. 47.c. 47.d. 48.a. 48.b. 48.c. 48.d. 49. 50. 51.a. 51.b. 52.a. 52.b. 53. 54. 55. 3-1 Taxable income $1,550; tax $185. $9,500. Filing separately yields same result as filing jointly. Sam and Lana need not file. Bobby is not required to file. Mike is required to file. Marge must file. Ben must file. Anita must file. Earl must file. Karen is not required to file. Pat must file. Joint return. Head of household. Surviving spouse. Head of household. Head of household. Single. Head of household. Single. 2002 married filing joint; 2003 surviving spouse; 2004 head of household. Head of household; one. $3,180. $1,400. $1,460. $600. Yes; saves $587. Taxable income $70,900. Refund due $799. 3-2 2005 Comprehensive Volume/Solutions Manual DISCUSSION QUESTIONS 1. b. i. h. d. c. f. g. a. Income (broadly conceived) Exclusions Gross income Deductions for AGI Adjusted gross income The greater of the standard deduction or itemized deductions Personal and dependency exemptions Taxable income Otherwise stated: b. – i. = h. – d. = c. – f. – g. = a. The child tax credit (choice e.) is subtracted from any income tax liability to arrive at the tax due (or refund). p. 3-2 and Figure 3-1 13. Roberto should definitely encourage his parents and aunts to move to Mexico. As residents of Mexico, they will now qualify as dependents. Needless to say, being able to claim four additional dependency exemptions is bound to help Roberto’s income tax situation. p. 3-14 18. a. It causes some married couples to pay a larger income tax than if they were single. See the results of Example 30 in the text and compare Example 31. b. The standard deduction was increased, and the reach of the 15% tax bracket was extended for married persons filing a joint return. p. 3-27 c. Lower-income couples who claim the standard deduction will benefit the most. See Tax in the News on p. 3-27. 24. Of the loss, $3,000 ($2,000 short-term and $1,000 long-term) is deducted against ordinary income with the short-term loss being used first. The remaining $1,000 of long-term capital loss is carried over to 2005 as a long-term capital loss. p. 3-31 and Example 40 26. a. If the parties live in New York, Marcie can claim Audry as her dependent. The fact that Audry filed a joint return does not matter when the purpose of the filing is to recover amounts withheld. However, Marcie cannot claim Jamie because he fails the gross income test. But since Marcie can claim Audry, she qualifies for head of household filing status. pp. 3-14 and 3-28 b. If the parties live in Arizona, Marcie can claim both Jamie and Audry. Jamie’s income now becomes $1,750 (50% X $3,500), and he now satisfies the gross income test (not in excess of $3,100). As in part a. above, Marcie qualifies for head of household filing status. p. 3-33 and Example 43 PROBLEMS 28. a. AGI Less: Itemized deduction Personal and dependency exemptions (4 X $3,100) Taxable income $70,000 (11,000) (12,400) $46,600 No additional standard deduction is allowed for a dependent age 65 or over (one of Emily’s parents). Tax Determination; Exemptions; Overview of Property Transactions 3-3 b. AGI Less: Standard deduction Personal and dependency exemptions (4 X $3,100) Taxable income $60,000 (9,700) (12,400) $37,900 c. AGI Less: Standard deduction (head of household) Personal and dependence exemptions (5 X $3,100) Taxable income $50,000 (7,150) (15,500) $27,350 d. AGI Less: Standard deduction (head of household) Additional standard deduction (Abigail) Personal and dependency exemptions (3 X $3,100) Taxable income $40,000 (7,150) (1,200) (9,300) $22,350 pp. 3-9, 3-10, 3-26 to 3-29, Table 3-1 and 3-2 29. Salary Interest on GMC bonds Alimony Capital loss IRA contribution Office pool AGI Standard deduction Personal and dependency exemptions (3 X $3,100) Taxable income $40,000 1,200 (2,400) (3,000) (3,000) 3,200 $36,000 (7,150) (9,300) $19,550 The child support payments are nondeductible. The gift is a nontaxable exclusion. Only $3,000 of the capital loss is deductible—the balance of $1,000 is carried over to 2005. pp. 3-5 to 3-8, 3-31, Figure 3-1, Exhibits 3-1 and 3-2, and Table 3-1 31. a. $4,850. Although $4,800 (earned income) + $250 = $5,050, the amount allowed cannot exceed that available in 2004 for single taxpayers. b. $3,450. $3,200 (earned income) + $250. c. $800. The greater of $800 or $400 (earned income) + $250. d. $850. The greater of $800 or $600 (earned income) + $250. e. $3,250. $1,800 (earned income) + $250 + $1,200 (additional standard deduction). pp. 3-9, 3-10, Tables 3-1 and 3-2, and Examples 8 to 11 34. a. Four. Two personal exemptions (Miles and Macy) and two dependency exemptions (Macy’s parents). The parents need not live with Miles and Macy as they meet the relationship test. b. Two. The ex-wife does not meet the relationship test although her brother (Rhett’s ex-brother-in-law) does. 3-4 2005 Comprehensive Volume/Solutions Manual c. Three. The ex-wife now satisfies the member of the household test. The exbrother-in-law meets the relationship test. d. Three. One personal exemption and two dependency exemptions. Nephews and nieces meet the relationship test and do not have to live with the taxpayer (although the niece does). e. Two. One personal exemption and one dependency exemption (the nephew). The niece does not meet the gross income test. The full-time student exception applies only to a child of the taxpayer. pp. 3-10 to 3-14 35. Exemption amount (10 X $3,100) $31,000 Step 1: AGI $235,000 Phase-out threshold (214,050) Excess amount $ 20,950 Step 2: $20,950 ÷ $2,500 = 9 (rounded up) X 2 = 18% (phase-out percentage) Step 3: Less: $31,000 X 18% (5,580) Step 4: Deduction for personal and dependency exemptions $25,420 p. 3-15 39. If Don kept the duplex, the annual tax thereon would generate an income tax liability of $3,300 (33% of $10,000). If Don transfers title to the duplex to Sam, the income tax consequences would be as follows: (1) Sam would be limited to an $800 standard deduction and would have taxable income of $9,200 ($10,000 – $800 standard deduction), which would be taxed at his own rate because he is not under 14 years of age. (2) Sam would pay $1,023 tax on the $9,200 taxable income [($7,150 X 10%) + ($2,050 X 15%)]. The tax saving to the family unit in 2004 if Don transfers the duplex would be $2,277 ($3,300 – $1,023), assuming Sam had no other income or expenses. In addition, the phase-out of Don’s exemptions would be reduced. However, there are other tax consequences to be considered. If the state in which the family resides imposes a state income tax, a further tax saving might result from the transfer. Another consideration is the possibility of Federal and state gift taxes that the transfer might generate. pp. 3-9 and 3-17 42. Unearned income Minus: $800 base amount + $800 standard deduction Unearned income taxed at parents’ rate $1,800 (1,600) $ 200 Ginni’s parents are in the 25% bracket, so her unearned income would generate $50 of tax (25% X $200). Computation of Ginni’s taxable income and tax: Earned income Interest income Gross income $2,100 1,800 $3,900 Tax Determination; Exemptions; Overview of Property Transactions Less: Personal exemption Less: Standard deduction [greater of $800 or $2,100 (earned income) + $250] Taxable income Less: Unearned income taxed at parents’ rate Income taxed at Ginni’s rate Ginni’s tax rate Tax at Ginni’s rate 3-5 -0(2,350) $1,550 (200) $1,350 X 10% $ 135 Ginni’s total tax: $50 (unearned income taxed at parents’ rate) + $135 (taxed at Ginni’s rate) = $185. pp. 3-20 to 3-22 and Example 28 45. a. Sam and Lana need not file since their gross income of $16,500 is less than the $17,800 filing requirement. b. Bobby is not required to file. Although he can be claimed as a dependent on his parents’ return, his earned income and gross income is less than $4,850 (his standard deduction). c. Mike is required to file since his gross income of $9,200 is more than the $9,150 filing requirement. d. Marge is required to file. Her gross income is less than $7,950, but her net earnings from self-employment are more than $400. Taxpayers in a. and b. should file, even if a return is not required, to obtain a refund if any income tax was withheld. pp. 3-22, 3-23, and Table 3-4 52. a. The loss on the Crow Corporation stock of $8,000 is first applied to the gain on the painting of $10,000. The painting is a collectible taxed at a 28% rate. After this combination, the end result is: Tax on remaining collectible gain (28% X $2,000) Tax on land gain (15% X $6,000) Total tax on all gains b. $ 560 900 $1,460 Use the same netting procedure, then tax the net collectible gain at 15% and the land gain at 5%. Thus, $300 (15% X $2,000) + $300 (5% X $6,000) = $600. pp. 3-30, 3-31, and Example 39