Interrelation

advertisement

Sequentiality versus Simultaneity:

Interrelated Factor Demand

Magne Krogstad Asphjell*

Wilko Letterie**

Øivind A. Nilsen***

Gerard A. Pfann****

May 2010

JEL Codes: D92, E22, E24, J23, L60

Key Words: Factor Demand, Interrelation, Nonconvex Adjustment Costs

* Norwegian School of Economics and Business Administration, Department of Economics,

Hellevn. 30, NO-5045 Bergen, Norway; Email: magne.asphjell@nhh.no.

** Maastricht University, Faculty of Economics and Business Administration, Department of

Organization and Strategy, P.O. Box 616, 6200 MD Maastricht, The Netherlands, Email:

w.letterie@maastrichtuniversity.nl; Tel: +31 43 3883645; Fax: +31 43 3884893.

*** Norwegian School of Economics and Business Administration, Department of

Economics, Hellevn. 30, NO-5045 Bergen, Norway; Email: oivind.nilsen@nhh.no.

**** Maastricht University, Faculty of Economics and Business Administration, Department

of Econometrics, P.O. Box 616, 6200 MD Maastricht, The Netherlands, Email:

g.pfann@maastrichtuniversity.nl.

Abstract:

In this paper we investigate a firm that has to decide about the timing of factor demand

adjustments. A structural model is developed to describe a firm’s demand for two production

factors which is subject to the presence of nonconvex adjustment costs. In this model the two

factor demand decisions are interrelated. That means that simultaneous adjustment of these

two production factors may either increase or decrease the total costs incurred by the firm. In

case simultaneous adjustment lowers the total costs, firms are more likely to conduct their

input factor changes simultaneously. On the other hand if simultaneous adjustment increases

the total costs incurred, firms are inclined to change the two input factors sequentially. One

reason for the first case, i.e. synchronisation of the two types of adjustments, is when

simultaneous adjustment reduces the time of disruption to the production process. On the

other hand, one could also think of a case where it would be efficient to implement input

changes subsequently. For instance, when introducing a new technology, it might be

economically reasonable to hire and train new workers prior to investing, such that the new

technology becomes productive as soon as possible after installation. Our model also shows

that flexible production factors, not being subject to fixed costs, may still exhibit intermittent

adjustment lumps, due to the cost of interrelation. Moreover, the importance of interrelation

on the decision thresholds increases when fixed costs are smaller. This implies that when

thresholds are being estimated for a single factor demand model alone, the model’s structural

parameters will be biased, especially if the factor is rather flexible. We apply the model to

investigate empirically the optimal timing of labour and capital demand changes. We develop

a maximum likelihood routine to estimate the structural parameters of the model. Plant level

data from Statistics Norway are used to estimate the cost or benefits of simultaneous

adjustment. The data concern plants operating in manufacturing industries and cover the

period 1993-2005. The estimates indicate that it is advantageous to adjust the stock of labour

and capital simultaneously. The cost advantage of changing labour and capital simultaneously

is small compared to the fixed adjustment cost of capital but is large compared to the fixed

cost of adjusting labour. Moreover, fixed costs of changing labour are much smaller than the

fixed costs of conducting investment. Our empirical results suggest that when estimating

single factor demand models the bias of parameter estimates is likely to be most severe in

case of labour demand.

2

1. Introduction

Firms have been observed to adjust the stock of their most productive factors, such as capital

and labour, in a lumpy fashion. Thus, they tend to concentrate big changes into short periods

while inaction dominates between these spikes. Such a pattern suggests that the smooth

adjustment of the important input factors is precluded by nonconvex, for instance linear or

fixed, costs leading to partial irreversibility of factor input decisions. With a few exceptions,

the existing literature on the irreversibility of production factors, has only considered separate

adjustment of one quasi-fixed production factor alone.1 Abel and Eberly (1998) note that the

observed lumpy employment pattern may not solely be due to a fixed cost component of

labour adjustment. They show that lumpy investment behaviour causes simultaneous large

employment adjustments in a model where labour demand is a fully flexible production

factor. Bloom (2009) finds that ignoring labour adjustment costs, as is typical in the

investment literature, is a reasonable approximation when modelling investment, while a

model with labour adjustment costs only, as is typical in the dynamic labour demand

literature, is problematic in the sense that the estimated parameters are far away from the true

ones found in a model that included both investment and labour adjustment costs. These

results indicate that controlling for investment dynamics is important when analysing the

more flexible labour input decisions.

Earlier research on multivariate factor input decisions suggests that the decisions

about changing several input factors are mutually dependent. Interrelation was initially

addressed using sector-level data in a linear setting by Nadiri and Rosen (1969). This study

was not based on a structural model with adjustment costs but it inspired others to investigate

the issue of interrelated factor demand decisions more deeply. Shapiro (1986) expands upon

1

For capital adjustment, see recent studies by Abel and Eberly (2002), Cooper and

Haltiwanger (2006), Letterie and Pfann (2007) and Nilsen and Schiantarelli (2003). For labour

adjustment, see the seminal contribution by Hamermesh (1989), and the more recent ones of Abowd

and Kramarz (2003), Rota (2004), and Nilsen et al. (2007).

3

Nadiri and Rosen (1969) and estimates a structural dynamic model of factor demand with

interrelation derived from the Euler equations. Galeotti and Schiantarelli (1991), and, more

recently, Merz and Yashiv (2007), have studied the topic of interrelation in a framework

without nonconvex costs of adjustment. Thus, from these findings it is hard to learn much

about the source of the lumpiness often seen in micro data. There is a substantial amount of

inaction observations for both labour and capital adjustments. This lumpiness may reflect the

existence of nonconvexities in the adjustment costs of the input factors. Contreras (2006)

investigates interrelation for a glass mould firm using simulated moments and calibration. He

finds that it is more costly for the firm to adjust capital and employment at the same time

rather than sequentially. Descriptive statistics from simultaneous analyses indicate positive

correlation between hiring and investment decisions. Recent empirical studies based on micro

data by Sakellaris (2004), Letterie et al. (2004), and Nilsen et al. (2009) have indeed revealed

that in the context of lumpy adjustment the dynamics of labour and capital demand are

interrelated. In particular, these papers have shown that at the micro level investment and

labour spikes are synchronized to a large extent. This may indicate complementarities in the

production process. Additionally, it may indicate that firms prefer synchronization, which

may stem from reduced adjustment costs when adjusting input factors simultaneously. Of

course, the described pattern may also reflect the nature of shocks to the shadow values of the

input factors. Note however, the studies by Sakellaris, Letterie et al., and Nilsen et al. op. cit

are all using non-structural and explorative approaches to analyse interrelateness. It is

therefore hard to identify whether the synchronisation is due to the nature of the changes in

the shadow values of the factors inputs, or whether it is caused by interrelated adjustment

costs. One of the goals of this paper is to build a structural model that incorporates

nonconvex adjustment costs together with interrelated adjustment costs that could either be

negative or positive (i.e. reduced costs due to synchronisation) or positive (making

4

simultaneous adjustments more costly). The advantage of a more structural model is that one

could potentially disentangle these two effects. It would also make it possible to identify

whether lumpy investment behaviour for one input is the effect of fixed costs for this factor,

or caused by interrelations in the adjustment cost function.

In this paper we investigate the consequences of interrelation where adjustments of

quasi-fixed input factors involve nonconvex costs. We refer to these factors as capital and

labour but it can also describe the behaviour of a firm deciding about any two different input

types (for instance R&D and natural resources). Our model deviates from work by Eberly and

Van Mieghem (1997), Dixit (1997), Abel and Eberly (1998), and Bloom (2009) in the sense

that we allow for the possibility that adjustment costs decrease or increase when the firm

decides to adjust two factors simultaneously. The occurrence of simultaneous adjustment

(synchronization) depends on the interrelation and especially on the question whether or not

interrelation adds to the costs of changing inputs or lowers those costs. One reason for the

latter case, i.e. synchronisation of the two types of adjustments, is when simultaneous

adjustment reduces the time of disruption to the production process. On the other hand, one

could also think of a case where it would be efficient to implement input changes

subsequently. For instance, when introducing a new technology, it might be economically

reasonable to hire and train new workers prior to investing, such that the new technology

becomes productive as soon as possible after installation.

We apply the model to investigate empirically the dynamics of joint labour and capital

demand decisions. Using Norwegian plant level data covering the manufacturing sector from

1993-2005 we obtain estimates of the adjustment costs parameters of the model by employing

a maximum likelihood routine and assess whether simultaneous adjustment of labour and

capital is beneficial or not. The paper proceeds as follows. In section 2 we develop the

theoretical model. In section 3 we discuss the role of fixed costs in relation with the cost of

5

interrelationship. Next, in section 4 we develop the econometric model. The data are

described in section 5. The empirical results are presented in section 6. Finally, section 7

concludes.

2. The model

Consider a firm that employs two production factors (capital Kt and labour Lt in year t) to

produce a non-storable output. The firm’s management maximizes V(.) denoting the present

discounted value of the cash flow resulting from its business operations. The objective

function is given by the value of the firm represented by

s

V

E

F

A

,

K

,

L

w

L

C

I

,

K

,

H

,

L

t

t

t

s

t

s

t

s

t

s

t

s

t

s

t

s

t

s

t

s

s

0

(1)

The term Et indicates that expectations are taken with respect to information available at time

t. The discount rate is given by with 0 1. The variable wt denotes the wage paid by

the firm to a full time worker. Investment and hiring (or firing) are denoted by It and Ht

respectively. Sales are given by the expression FAt ,Kt ,Lt where the term At represents a

variable capturing randomness in technology or stochastic behaviour of the demand

conditions the firm is facing.

When adjusting the stock of capital or the number of workers the firm incurs

adjustment costs defined as:

2

k

I

b

I

I

K

t

It,K

C

,

H

,

L

p

I

I

0

p

I

I

0

I

0

K

t

t t

t t

t

t t

t

t

t

2

K

t

2

L

(2)

H

b

H

H

L

t

p

H

H

0

p

H

H

0

H

0

L

t

t

t

t

t

t

t

L

t

2

t

KL

It

H

0

0

t

6

It,Kt,H

In the adjustment cost function C

t,L

t the indicator function . assumes the value

1 if the condition in brackets is satisfied and equals zero otherwise. The purchase price of

I

capital is given by pt . In case the firm sells capital we assume that the price received for one

I

I

I

unit of capital equals pt . Due to irreversibility of investment decisions pt pt . This

costly reversibility of factors arises when a firm faces firing costs or when there is lemon’s

market for used capital such that the firm cannot sell its capital for the same price as when

bought. Note that the actual investment costs are incorporated in the adjustment costs

function in its linear part. Linear adjustment costs with respect to hiring and firing are

H

H

denoted by pt when H t 0 and pt when H t 0 . The convex costs are represented by

conventional quadratic functions in

It

Ht 2

and

. The fixed costs associated with adjusting

Kt

Lt

capital and labour are represented by K and L respectively and we assume that both

parameters are nonnegative and do not depend on whether I t and H t are positive or negative.

Fixed costs can be a result of the firm’s production processes being disrupted when

adjustment of capital or labour takes place.3 Alternatively, the firm’s management may have

to spend costly time guiding these organizational changes. We also assume that if the firm

adjusts labour or capital, then the adjustment costs of the other factor demand component are

affected. The term KL is positive if simultaneous adjustment of capital and labour forces the

management to spend additional time and effort on the joint adjustment, or that the

adjustment causes a more severe production interruption compared to when capital or labour

2

It is straightforward to extend this adjustment cost function with a term capturing convex

costs of interrelation like

IH

K

Lwhere

0

1

.

We abstract from this possibility

K

L

1

to facilitate notation and hence enhance readability of the paper, but the extension is available upon

request. We note that in the figures presented later in this paper the area where simultaneous

adjustment (I≠0 and H≠0) takes place becomes defined by curved boundaries rather than straight lines

if 0.

3

Fixed costs are used as a simple way of introducing non-convexities.

7

adjustments are undertaken at separate points in time. On the other hand, the

expression KL is negative if the firm’s managers save time or if the firm can save on costs of

disruption when adjusting the factors jointly.4

The firm decides upon the optimal size of the capital stock, K t , by setting

K

investment I t at the appropriate level. Since capital depreciates at rate , the stock of capital

evolves according to the law of motion

K

K

I

1

K

i,t

1

i

,t

i

,t

(3)

Simultaneously, the firm determines the optimal value for the number of workers Lt by

choosing the desired and hence optimal level of hiring or firing denoted by H t . The amount of

labour evolves according to

L

H

1LL

i,t

1

i,t

i,t

(4)

L

where measures the autonomous quit rate of workers.5 To obtain the optimal values for

I t and H t equation (1) can be optimized with respect to these decision variables subject to the

laws of motion governing the dynamics of capital and labour as given by equations (3) and

K

L

(4). Before proceeding we note that the variables t and t are the conventional shadow

values of an additional unit of capital and labour, respectively. We provide a derivation of the

shadow values in the appendix. It is easy to show that this is the expected present discounted

value of the marginal product of capital or labour plus the reduced adjustment costs in future

4

Note that we will assume that

K

L

K L

m

in

(

, ). The economic meaning of such an

assumption is that the cost of interrelation KL do not completely offset the fixed cost of adjustment

K or L . If the assumption does not hold, for instance if KLL 0, ( KLK 0), this

implies that the firm will always adjust labour (capital) when it invests (hires or fires). This regularity

is unlikely to hold in reality.

5

We assume without any loss of generality that changes in capital and labour materialize with

a lag.

8

periods. Using the Lagrangean provided in the appendix the first order conditions for

investment and labour adjustment are

I

p

I

0

p

I

0

b

0

and

K

KI

t

t

t

I

t

t

K

t

(5)

t

H

p

H

0

p

H

0

b

0

L

LH

t

t

t

H

t

t

Lt

t

respectively. Similarly to Abel and Eberly (1994, 2002) the optimal amount of investment and

hiring or firing are

I t tK ptI

Kt b K

Ht tL ptH

Lt b L

(6)

I

I

I

p

I

0

p

I

0

In this latter set of equations we use the notation that p

and

t

t

t

t

t

HH

H

p

p

H

0

p

H

0

.6 Due to the presence of fixed costs of adjustment the

t

t

t

t

t

firm will not always follow the decision rules presented in equation (6). Sometimes it may be

optimal to abstain from adjusting capital and or adjusting labour. The threshold values for the

K

L

shadow values t and t can be derived by finding the value for which a change in I t and or

H t generates non-negative profits. The equation determining whether to change the stock of

capital and or to adjust labour is

I

H

C

I

,

K

,

H

,

L

K

t t

L

t t

t

t

t

(7)

t

The left hand side of (7) measures the expected benefits of changing capital and or labour,

whereas the right hand side denotes the cost associated with the firm’s decisions. Note that

tK and tL are the Lagrange multipliers (i.e. shadow values of capital and labour) employed in

6

We have made this as a notational simplification. It does not affect the qualitative findings in

this paper.

9

our optimization problem subject to constraints given by equations (3) and (4) depicted in the

appendix. Hence, they measure how the value of the firm changes if the constraints (3) and

(4) are relaxed or, equivalently, if capital and labour are increased by one unit. Therefore, the

K

L

expression t It t Ht represents an appropriate estimate of the benefits of input

adjustments. In a continuous time framework with one production factor a similar expression

holds exactly.

Using equation (6) it can be shown that equation (7) holds if

2

1K I2

1L H

p

I

0

p

H

0

t K

t

t

t L

t

t

Kt

Lt

2

b

2

b

I

0

H

0

I

0

H

0

K

L

t

KL

t

t

(8)

t

To solve the optimization problem of the firm we derive the conditions necessary for various

adjustment decisions.

3. Factor input decisions

The

firm

regards

adjusting

the

stock

of

capital

goods

to

be

desirable

if

1 K I2

K

p

. Hence, a necessary condition for changing the amount of capital is

t K

t

K t

2

b

2

b

p

A

KK

K

t

I

t

K

(9)

K

t

A similar necessary condition for hiring or firing workers is

1 L H2

L

p

L

implying

t

t

L t

2

b

2

b

p

A

LL

L

t

H

t

L

(10)

L

t

Equations (9) and (10) show that if the net benefits of adjusting capital and labour do

not exceed a certain minimum threshold, the firm decides to abstain adjusting. These two

K

L

thresholds are caused by the existence of the fixed adjustment costs and .

10

Consider now the case where both necessary conditions to adjust capital and labour

are satisfied as given in equations (9) and (10). Hence, the firm has an incentive to adjust at

least one factor of production. However, due to the cost of interrelation the firm may need to

select adjusting only one factor to maximise its objective function. It is optimal to adjust the

number

of

workers

rather

than

the

stock

of

capital

if

2

2

1

LH

L1

KI

K

p

p

. This holds when

t

t L

t

t

t K

t

L

K

2

b

2

b

K

b

2

b

p

p

L

L

L

L

2

2

LH

LK

t KI

t

t

t

K t

t

t

b

(11)

We can also rewrite this condition as:

K

2

b

b

2

b

p

p

L

L

L

2

LH

t

t

L

L

L

2

L

I

K

t K

t

K t

t

t

t

b

(11’)

The first term on the RHS of this expression is positive given our assumptions about the

adjustment costs parameters and the content in the squared bracket is also positive according

to eq. (9). Thus, the sum of the two terms is positive. Hence it is optimal to adjust labour

rather than capital if

L

L

K

2

2

b

L Hb

LK

t KI

|t

p

|

p

t

t

K t

L

L

b

t

t

(12)

Under certain conditions it is optimal to adjust only one input factor, because of the

cost of interrelation. It is optimal to adjust an additional factor of production if the net benefits

K

L

associated with that adjustment exceed the fixed costs of that second input ( or ) plus

KL

the cost of interrelation 0 . Hence, it is worth also adjusting the stock of capital (given

that adjusting labour yields a higher value of the firm if only one input needs to be selected)

as soon as

1 K I2

K KL

p

α

t K

t

Kt

2

b

(13a)

11

Similarly, labour will also be adjusted (given that changing capital yields a higher firm value

if only one input is selected) as soon as

2

1L H

L KL

p

L

α

t

t

L t

2

b

(13b)

Hence, the boundaries determining when the firm will adjust both factors of production are

tK ptI

2bK K KL

BK

Kt

tL ptH

2b

Lt

L

L

3a. Adjustment decisions when

(14)

B

KL

KL

L

0

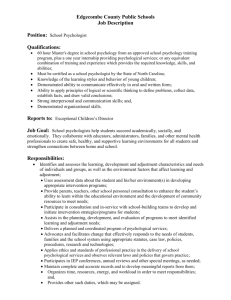

The analysis of firm level capital and labour demand decisions is summarized in figure 1.7

Starting with the inaction area, we see that this area is bounded by AK and AL and -AK and -AL.

As already noted, this inaction is caused by the presence of the fixed adjustment costs, K

and L , meaning that the shadow value of a new unit of capital (labour) has to move beyond

the thresholds defining area I. The firm only adjusts the two factors of production

simultaneously in the area indicated by III. These areas move further away from the origin if

KL increases decreasing the area where simultaneous adjustment occurs. In fact, higher

KL

interrelated adjustment costs, , increase the distance between AK and BK, and between AL

and BL. This means that the net benefits of changes need to be significant before a firm

chooses to change both input factors simultaneously. Demand for both factors is non-zero if

K

I

L

H

the benefits of change (i.e. | t pt | and | t pt | ) are high. For instance, a high positive

K

L

demand shock may increase the shadow values t and t simultaneously and hence provide

7

Our figures deviate from the ones by Dixit (1997), Eberly and van Mieghem (1997), and

Bloom (2009) in the sense that we have the marginal value of an additional unit on the axes, while the

authors op. cit. have productivity A normalized with K and L , respectively.

12

the firm an incentive to expand the scale of the firm by increasing both factors of production.

On the other hand, a firm may be increasing one input and decreasing the other input at the

same time if shadow values move in opposite directions. Such a situation may arise due to a

policy change affecting the relative price of the two factors of production or due to a

technology shock changing the optimal share of the inputs to produce a certain level of

output. But whether the adjustments of the input factors are made simultaneously or

sequentially depend on the size of the interrelated adjustment costs.

[Insert Figure 1 about here]

To see the importance of the interrelated costs, it might be helpful to see what

happens when the interrelated costs would be nonexistent, i.e. where KL 0 .8 That means

that AK BK , and AL BL . In this case the areas where only one type of change would take

place, area II, would become much smaller. The do-both-changes area III would at the same

time be larger. Thus, the presence of positive interrelated costs would increase the area where

a firm would only involve in one type of investment activity at the time.

The curved boundary in the upper right corner in figure 1 crosses the rectangular areas

at AL AK and BL BK . This curve, corresponding to the right hand side of equation (12),

K

I

L

H

is concave if K L in the area where t pt 0 and t pt 0. Hence in figure 1 we

depict the case K L where the curved boundary crosses the horizontal axis (i.e.

K K L

2

b

(

)

where p 0) at x

. If K L the right hand side of equation

K

K

t

L

t

H

t

K

I

(12) is convex and the curved boundary crosses the vertical axis (i.e. where t pt 0) at a

8

This is the case analysed by Dixit (1997).

13

L L

K

2

b

(

)

point defined as y

. Note that if K L , the boundary determining

L

L

t

whether to invest or adjust labour becomes a straight line. The three other curves in the figure

are analogous to the one just discussed.

Here we illustrate the importance of αKL assuming that K L . It is straightforward

i

to show that the distance between the thresholds decreases as increases:

i

i

1

1

B

A

i

KL

i

2

2

0

i

(15)

i

i

lim

B

A

0for i {K, L}. This means that in figure 1 the area where the firm

and that

i

completely abstains adjusting, area I, and the area where both factors are adjusted

simultaneously, area III, tend to move closer to each other as the fixed costs become larger

relative to the interrelated cost, αKL. Hence, large fixed costs will suppress the importance of

interrelation.9

Omitting the interrelated costs when estimating a single factor demand model with

adjustment costs may introduce a bias in the estimates of the fixed costs. Given a proxy for

the shadow value of capital, when estimating a single factor q model, the threshold will be

located between A K and B K for investment, since it is the presence of zeroes that identifies

the threshold. For labour demand the threshold will lie between A L and B L in a model

considering labour only. This indicates that when interrelation is important then a single

factor model is likely to produce biased and imprecise estimates for the adjustment costs in

i

particular for a flexible production factor with a low adjustment cost .

Our analysis also shows that a lumpy adjustment pattern may be caused by the

existence of interrelated adjustment costs, and not by fixed adjustment costs for the factor

KL

i is small with large

In addition, the relative importance of interrelation measured by

fixed costs. In such a circumstance, interrelation will not play a major role in the dynamics of factor

demand.

9

14

L

K

KL

itself. Suppose for instance that 0 and that 0 and 0 . Note that

L

L

given 0 , A 0 here. Though in this case labour is fully flexible, the firm will not

K

I

K

L

H

L

K

I

always adjust labour when it invests (if |

t p

t |A ; |

t p

t |B and both | t pt |

L

H

and | t pt | are located at point (i) and (ii) in figure 1 for instance). Hence, labour

adjustment may appear intermittent with a large number of zero hiring / firing observations

even if it does not involve the firm incurring fixed costs for labour itself. Abel and Eberly

(1998) also argue that a flexible factor can be subject to lumpy dynamics due to large

adjustments of a less flexible factor. Our model reveals that the cost of interrelation is an

additional reason why flexible factors may exhibit intermittent patterns.

3b. Adjustment decisions when KL 0 (and still K L ).

If KL 0 firms actually benefit from adjusting both input factors simultaneously. The above

analysis can be applied to a large extent here as well. The main difference is that the choice

between investment or labour adjustment as presented below equation (12) has become

irrelevant in this case. This is due to the fact that the thresholds BL and BK are smaller than AL

and AK respectively if KL 0 (also see equations 9, 10 and 14).

[Insert Figure 2 about here]

Figure 2 indicates that if the firm incurs lower adjustment costs because of

simultaneous adjustment area III where this event occurs becomes larger. If KL decreases

then area III representing the situation that the firm changes both labour and capital move in

the direction of the origin of the figure. If LKL 0, the horizontal threshold at BL will lie

at the horizontal axis of figure 2. This means if the firm invests it will also change its labour

15

force, i.e. the area I 0,H0disappears. If KKL 0 then the firm will always invest

as soon as it alters its number of workers because the vertical threshold at BK will hit the

vertical axis of the figure and the area I 0,H0 vanishes. If both conditions KKL 0

and LKL 0 hold then the firm will always change the two factors of production at the

same time.

Like in section 3a we find that the distance between the thresholds decreases for

larger fixed costs:

i

i

1

1

A

B

i

i

KL

2

2

0

i

(16)

i

i

lim

A

B

0for i {K, L}. Again this implies that interrelation is less likely to

and that

i

be a main determinant for factors that involve large fixed adjustment costs. But single factor

demand models for flexible inputs may be misspecified when interrelation is important.

4. The econometric specification

The investment decisions are dependent on the shadow values of investment and labour.

These represent the present discounted value of the marginal product of capital plus the

adjustment cost savings in future periods due to the higher level of capital, and

correspondingly for labour, the present discounted value of the marginal product of labour

plus the adjustment cost savings due to an increase in the stock of workers. See the appendix

for a derivation of the shadow values. The econometrician will be able to observe firms’

L

K

investment decisions. However, marginal values it and it are not observable. Thus, in

order to make the model estimable, we need to approximate these shadow values. For

simplicity we assume these to be linear functions of some observables, ZK and ZL.10 In

L

K

addition we add stochastic error terms it and it to the definition of the shadow values to

10

In the appendix a detailed discussion is provided on the variables included in ZK and ZL.

16

capture idiosyncratic factors not observable. It should be noted that this will also introduce

error terms in the two demand equations, equations (6).

p

Z

(17)

p

Z

(18)

K

it

L

it

I

it

H

it

K

0

L

0

KK

1 it

LL

1 it

K

it

L

it

K

L

We will assume that it and it are bivariate normally distributed with zero means, variance

K and L , and correlation coefficient :11

K2

0

,

~ N

,|

Z

,K

,

Z

,L

0

KL

it it

K

it it

L

it it

L2

(19)

Thus, with the approximation described in equations (17) and (18), and the thresholds

equations (9), (10) and (14), we have all the necessary information to build up a bivariate

ordered probit model. That is, we simplify the problem by saying that every firm decides

between three options per input factor in period t; no change, decrease, or increase.

To illustrate the derivation of the likelihood function we can consider Figure 1 which

KL

assumes a positive interrelation cost, 0 . The firm has a set of nine possible choices

concerning adjustment of capital and labour. In the area denoted I the firm will abstain from

adjustment of any factor, in the four areas denoted II the firm will adjust one of the two

factors separately, while in the four areas denoted III, the optimal decision is to adjust the

levels of capital and labour simultaneously. The horizontal- and vertical-axis measure the

marginal benefit of capital and labour respectively. The optimal investment decisions for

K

I

L

H

each factor change as it pit and it pit move across their respective thresholds.

We note that the value of the correlation coefficient has a clear economic interpretation. If

this parameter is positive, shocks to marginal values of capital and labour are positively correlated as

we would expect for demand shocks. If is negative, it would indicate a negative correlation in

shocks to marginal values as we would expect to see for some types of technological shocks.

11

17

The fact that each observation is assigned to one of the regimes, based on the values

of I/K and H/L makes identification of our parameters of interest possible. Specifically, we

are able to estimate two different sets of threshold levels for separate and joint adjustments

because we allow for different thresholds to apply conditional on the adjustments being made

sequentially or simultaneously. Graphically, this means that we need observations such as

that represented by point (i) in Figure 1.

If we, as in figure 1, assume interrelation costs to be positive, we will in some cases

see marginal values for both factors exceed the thresholds for sequential adjustment, but not

for joint adjustment. That is, cases where marginal values exceed threshold level AK and AL,

but not BK and BL. This situation can be represented by the point denoted (ii) in figure 1, and

there will exist four different areas where similar situations can arise. According to equation

(12) the firm will invest in labour rather than in capital if

L

L

K

2

2

b

L Hb

KI

LK

it

|it

p

|

p

it

K it it

L

L

b

it

it

The values that give equality in the above expression are represented by curved lines in the

K

I

L

H

figure. Substituting with approximations as given by (17) and (18) for it pit and it pit ,

we can rewrite the condition as follows

K

b

2

b

(

Z

)

(

Z

)

b

L

L

2

LL

K

K

K

L

KL

L

L

i

t K

L

i

t

01

i

t i

t

0

1

i

t

K

i

t

i

t

(20)

L

K

Because the error terms it and it both enter in this inequality, the decision rule to be

implemented in a likelihood function would introduce significant complexity. We therefore

18

simplify by assuming that the four curved lines in figure 1 can be approximated by straight

lines.12

When the interrelated adjustment costs turn out to make synchronisation costKL

efficient, i.e. 0 , the limits of the investment regimes become somewhat different. This

is illustrated in Figure 2. Under the conditions in figure 2, we have no areas where the firm

must decide between investments in two adjustments that are separately profitable but not

jointly, and no approximation like the one discussed above needs to be made. Because of the

difference between cases with positive and negative interrelation costs represented by Figure

1 and 2, it is not possible to apply the same likelihood function in both cases. This can be

seen as the thresholds that limit the nine areas of the figure are not the same. This makes it

KL

necessary to specify slightly different likelihood functions conditional on the sign of .

The main structure of the function though, is identical.

The likelihood function to be used in the ML estimation follows a standard setup for

discrete variables.13 It can be written as a sum of 9 different probability expressions for the

nine different outcomes summarized over periods t and firms i. The probabilities are given by

the standard cumulative bivariate normal distribution function. The expression below is an

abbreviated version of the full log likelihood.

12

When we assign probabilities to observations, we calculate the integrals of the four areas

where the decision rule should be applied, and due to the approximation by a straight line we divide

the integrals by two. Each part is then assigned to the appropriate action space. Thus, it is possible to

write the likelihood using only values of the univariate and bivariate cumulative normal distribution

functions.

13

Admittedly, we could have developed a model to use more information from the data, as in a

Tobit-type model. Our choice is based on reasons of computational simplicity. Regardless, our chosen

model identifies our parameters of interest, so that there would only be efficiency gains from the

alternative approach.

19

ˆ

ˆ

KK

K

L

L

Lˆ

K

L

ˆ

ˆ

ˆ

b

2

b

2

ˆ

ˆ

Kˆ

K

K

Lˆ

L

L

ˆ

L

o

g

L

l

o

g

Z

Z

,

2

0

1

i

t,

0

1

i

t

,

K

L

t

1

i

i

t

i

,

t

t

T

T

T

T

l

o

g

.

l

o

g

.

.

.

.

l

o

g

.

,

0

t

1

i

t

,

t

1

i

t

,

t

1

i

t

(21)

2 denotes the standard cumulative bivariate normal distribution function, where the

,

,0

,

,

...,

subscript 2 indicates a bivariate function.

denote the sets of firms that

t , t , t ,

t

in period t are allocated in the different investment regimes.14 A tilde above the parameters

indicates that as in standard models of discrete outcomes, we estimate the ratio between the

K

L

original parameter and standard deviations and . We will refer to these ratios as

normalized parameters.

K

K

L

L

The model allows us to recover normalized estimates of 0 ,

1 ,

0,

1 , pseudo-

K

K

L

L

K

L

LL K

L

,

b

,

b

a

n

d

b

KK

in addition to an estimated

thresholds b

correlation coefficient, .15

We are, in other words, not able to identify convex and

nonconvex cost parameters directly. However, estimates of the normalized pseudo-thresholds

enable us to identify ratios of fixed cost parameters. Say that we have recovered estimates of

the parameters16

14

Superscripts -, 0 or + denote negative, zero and positive adjustments of capital and labor,

,

respectively. I.e. t is the set of observations with negative adjustment of both factors in period t,

t ,0 is the set of observations with negative adjustment of capital and zero adjustment of labour, etc.

15

We call them pseudo thresholds, since the estimates do not include the terms

2

16

K

K

L

L

Lit , while the thresholds A , B , A , and B do.

Asterisks in the superscripts denote that these values are pseudo thresholds.

20

2

K it and

K

K

K

L

L

L

KL

bKK ˆ*L bLL ˆ*K b

B

ˆ

ˆ*L b

A*K

A

B

2

2

and

K 2,

L 2,

K

L

(22)

Because of the differences between the thresholds for separate and joint adjustments, we can

find the ratios between fixed cost parameters that are not normalized.

*

K*

K

K

K

L K

L

b

b

B

A

b

K

2

K

K

K K

*

K

K b

b

A

2

K

KK

L K

KK

*

L*

Lb

L

K

L K

L

b

B

A

b

L

2

L

L

K L

*

L

L b

b

A

(23)

2

LL K

L L

L L

*

K *

K *

L

L K

L

L

BA

A

.

L

K

*

L *

L *

K K K

B

A

A

(24)

(25)

Since it is possible to derive these ratios after estimation of pseudo-thresholds, it is

also possible to estimate cost parameters directly as parameters in the likelihood function by

changing the parameterization. We chose to follow a step-wise procedure when carrying out

estimations on simulated data. In the first step, we apply to different likelihood functions, and

obtain two different sets of estimates. One conditional on a positive interrelation cost

KL

KL

parameter , and one assuming that 0 . By reviewing the estimates of pseudo

thresholds and comparing Aˆ * K with Bˆ * K and Aˆ * L with Bˆ * L , we get an indication of the sign

KL

of , and thus which is the appropriate likelihood function to apply. In the second step,

after changing the parameterization, we use the applicable likelihood function to obtain direct

estimates of parameter ratios in equations (23) – (25).

5. Data

21

5a. Sample construction

The empirical evidence in this work is based on plant level information from Norway for

plants in the manufacturing industry, covering the period 1993-2005. The data are collected

by Statistics Norway. Focusing on manufacturing gives access to detailed information about

production and production costs, together with detailed information about investment and

employment. Investment is defined as purchases minus sales of fixed capital. Expenditures

related to repairs of existing capital goods are excluded from the definition of investment. We

focus on equipment which includes machinery, office furniture, fittings and fixtures, and

other transport equipment, excluding cars and trucks. We have restricted our attention to

plants with 10 or more employees. Some data might be available for also smaller plants. Note

however, that these observations may be associated with measurement errors since some of

the information from these types of plants often are imputed by Statistics Norway. For our

purpose it should not be critical, rather on the contrary. For these smaller plants it would be

very hard to disentangle the effects of indivisibility from the effects caused by nonconvex

adjustment costs. We have excluded all auxiliary units which do not take part directly in

production, such as separate storage and office units. Plants in which the central or local

governments own more than 50% of the equity have also been excluded from the sample, as

well as observations that are reported as “copied from previous year”. This actually means

that a data entry is missing. The remaining data were trimmed to remove outliers.17

Capital stock was built up using the perpetual inventory formula, using information

about initial capital stock and net investments (see the Data Appendix for details about the

initial capital stock). Finally, we include only plants for which we have 6 or more consecutive

observations. For the analysis we only use the fifth or higher usable observations for each

plant, reserving the first periods for each plant for the initial stock of capital. Our final sample

We excluded observations where the investment rate, I/K, the net workplace changes (L/L),

and wage per employee, w, were outside “reasonable” limits.

17

22

used in the maximum likelihood estimations include 2460 plants with a total of 14759

observations from the period 1997-2005.18

5b. Descriptives

Table 1 presents a number of summary statistics. The average firm in the sample employs

approximately 75 individuals, L. In 1996 prices the average stock of capital, K, is about 60

million NOK or €7.5 million. This reflects that in manufacturing industries firms are

relatively capital intensive. We observe that investment and hiring rates, I/K and ΔL/L, are

significantly positively correlated to the capital and labour productivity respectively. Also the

hiring rate is positively correlated to the wage rate, w, and this correlation is significantly

different from zero. This finding is not so obvious at first sight. However, it may be the case

that firms start hiring workers when the economy is booming and that hence higher wages

reflect that expansion efforts are worthwhile. Wage rates are also positively related to labour

productivity, Y/L which is what one would expect to happen if labour markets operate well.

[Insert Table 1 about here]

In table 2 we report the frequency distribution of the hiring and firing rates. We

observe that hiring is zero in 11.2 percent of the cases, supporting the notion that non convex

costs play a role in determining labour adjustments. A similar argument can be put forward

for capital adjustment for which we report 15.1 percent zeroes. At least one adjustment is

being made very often as both hiring and investment are zero at the same time in only 2.2

percent of the observations. We find that just one adjustment is made (hiring or investment is

18

The criterion that these plants are only included if they have at least six or more useable

observations, might introduce some selection issues. Probably larger and more successful plants are

more likely to be present in our data.

23

non zero) in 21.9 percent of the cases. For sequential adjustment a necessary condition is that

in a period only one adjustment must take place. Hence, this finding is suggestive of the

advantage of simultaneous adjustment. In fact in our data we find that 75.9 percent of the

observations are cases where firms adjust labour and capital simultaneously.

[Insert Table 2 about here]

Table 3 reports the correlations between contemporaneous, lagged and forwarded investment

and hiring rates. It appears that contemporaneous hiring rates and their lagged and forwarded

counterparts are negatively correlated at -0.08 (-0.083 and -0.078 in the table). This indicates

that labour adjustments in two consecutive years are less likely. For investment we find that

contemporaneous investment is positively correlated with lagged and forwarded investment

rates with a coefficient of 0.148 and 0.131 respectively. This means that large investments are

spread over at least two consecutive years. We observe that the correlation coefficient

between contemporaneous investment and hiring rates is about 0.116. In line with cost

advantages of simultaneous adjustment of labour and capital the table indicates that the

correlation of contemporaneous hiring (investment) with lagged or forwarded investment

(hiring) is lower at 0.08 (ranging between 0.070 and 0.090).

[Insert Table 3 about here]

6. Results

The descriptive statistics so far indicate that firms in our sample tend to implement labour

and capital adjustments simultaneously. To get a better understanding of what drives the

synchronization of labour demand and investment the structural model is estimated to

24

identify whether interrelations in the adjustment cost function are causing this phenomenon.

Table 4 presents the estimation results. It shows that the thresholds satisfy: AK BK and

AL BL . This result is consistent with the notion that simultaneous adjustment yields cost

KL

advantages: 0 and that interrelation is far more important for labour than for capital.

KL

KL

0

.

27

In fact the results imply that

and that K 0 . The fixed adjustment costs of

L

capital exceed those for labour a lot. The estimates indicate that

L

0 . In section 3 we

K

observed that the cost of interrelation matters most when an input factor is flexible or, to put

it differently, is associated with relatively small fixed adjustment costs. The estimates

indicate that primarily the dynamics of the flexible input (i.e. labour demand) is affected by

the cost of interrelation, whereas capital demand remains rather insensitive to it. This is in

line with Bloom (2009) who states that ignoring labour demand when investigating

investment is not very harmful. However, when estimating a demand model for labour,

ignoring capital adjustment yields biased estimates.

[Insert Table 4 about here]

L

K

The shocks to the marginal value of labour and capital it and it have a positive correlation

coefficient (ρε=0.17). This means that shocks to the fundamental variables driving labour and

capital demand tend to move in the same direction. This may be due to demand shocks that

induce a firm to adjust labour and capital in the same direction. A precise interpretation of the

shocks is cumbersome as they are picking up misspecification of the model, technology

shocks, or other shocks unaccounted for by the model.

25

We have also estimated the model using the maximum likelihood routine using the

KL

assumption that simultaneous adjustment is costly: 0 . The estimates of this analysis

KL

indicate that the assumption 0 does not hold. The results show that the estimated

thresholds are consistent with cost advantages of simultaneous adjustment of labour and

capital. We do not report the results to save some space.19

7. Conclusion

If it is costly to adjust two factors of production at the same time a firm has an incentive to

conduct a one at a time policy: adjust only one factor. The firm is inclined to adjust

simultaneously if there are cost advantages of doing so. Recent empirical studies indicate that

large adjustments tend to be synchronized in some data sets, but in others they are not. In this

paper we show that this feature of the data may be consistent with the hypothesis that joint

adjustment increases or reduces the overall costs of adjustment. We also find that when fixed

costs of adjustment are large then the role played by the cost of interrelation may be minor.

Hence, synchronization may occur because large fixed costs dampen the relative importance

of interrelation. One prediction from our theoretical model is that when one factor is more

flexible than the other, in a model neglecting interrelated costs serious omission bias will

occur in the estimated adjustment costs for the most flexible production factor. We also show

that a production factor may be subject to intermittent dynamics even though adjusting this

factor does not raise a fixed cost. Lumpiness may just occur due to the presence of cost of

interrelation. If costs of interrelation are high, at times the firm changes the least flexible

production factor, it will leave the flexible factor unchanged.

19

Asphjell et al. (2010) investigate whether the maximum likelihood routine employed

in this paper is capable of retrieving the true parameters from a simulated dataset. All

simulations indicate the routine has satisfactory properties when the data set has the size of

the data used for the estimations in this paper.

26

Using Norwegian plant level data concerning the manufacturing industry in the period

1993-2005 we obtain insight into the deep structural parameters of a labour and capital

demand model. The maximum likelihood routine we employ reveals that simultaneous

adjustment of the two production factors yields cost advantages. The estimates indicate that

the fixed cost of capital is large compared to both the fixed cost of adjusting labour and the

cost advantage of simultaneous adjustment. However, the benefits of synchronizing labour

and capital demand are large relative to the fixed adjustment cost of labour. These results

imply that when estimating single factor demand models the parameters are likely to be

biased most severely in case of labour demand.

27

References

Abel, A.B., Eberly, J.C., 1994, “A unified model of investment under uncertainty”, American

Economic Review, 84, 1369-1384.

Abel, A.B., and Eberly, J.C., 1998, “The Mix and Scale of Factors with Irreversibility and

Fixed Costs of Investment”. Carnegie-Rochester Conference Series on Public Policy,

48, 101-135.

Abel, A.B., and Eberly, J.C., 2002, Investment and Q with fixed costs: an empirical analysis.”

Mimeo, The Wharton School, University of Pennsylvania.

Asphjell, M.K., Ø.A. Nilsen, W. Letterie, “Estimating Interrelated Nonconvex Adjustment

Costs by Maximum Likelihood.” Mimeo

Bloom, N., 2009, “The impact of uncertainty shocks”, Econometrica, 77, 623-685

Contreras, J.M., 2006, “Essays on factor adjustment dynamics.” PhD Thesis, University of

Maryland, Department of Economics.

Dixit, A., 1997, “Investment and employment dynamics in the short and the long run”, Oxford

Economic Papers, 49, 1-20.

Dixit, A., and R. Pindyck, 1994, Investment under Uncertainty, Princeton University Press,

Princeton, New Jersey.

Eberly, J.C., van Mieghem, J.A., 1997, “Multi-factor dynamic investment under uncertainty”,

Journal of Economic Theory, 75, 345-387.

Galeotti, M. and F. Schiantarelli, 1991, “Generalized Q Models for Investment”, Review of

Economics and Statistics, 73, 383-392.

Letterie, W.A., Pfann, G.A., Polder, J.M., 2004, “Factor adjustment spikes and interrelation:

an empirical investigation”, Economics Letters, 85, 145-150.

Merz, M., Yashiv, E., 2007, “Labor and the value of the firm”, American Economic Review,

97, 1419-1431.

28

Nadiri, M.I., Rosen, S., 1969, “Interrelated factor demand functions”, American Economic

Review, 59, 457-471.

Nilsen, Ø.A, A. Raknerud, M. Rybalka and T. Skjerpen, 2009, “Lumpy Investments, Factor

Adjustments and Labour Productivety”, Oxford Economic Papers, 61, 104-127.

Sakellaris, P., 2004, “Patterns of plant adjustment”, Journal of Monetary Economics, 51, 425450.

Shapiro, M., 1986, “The dynamics of demand for capital and labor", Quarterly Journal of

Economics, 51, 513-542.

29

K

L

Appendix: Derivation shadow values t and t :

K

L

The terms t and t represent the Lagrange multipliers for capital and labour respectively,

associated with constraints given by equation (3) and (4). Using equation (1), The

Lagrangean for this optimization problem is:

K

L

L

V

E

I

1

K

K

I

1

L

L

t

t

tt

t

K

t

t

1

t

t

L

t

t

1

s

0

To obtain the Lagrange multiplier for capital we solve

L

E

F

K

,

L

,

w

L

C

I

,

K

,

H

,

L

K

K

t

t

t

1

t

1

t

1

t

1

t

1

t

1

t

1

t

1

t

1

E

1

0

t

t

K

t

1

K

K

t

1

t

1

In the next, P refers to a probability of an event occurring. For this probability, the

superscript K refers to the event of only capital adjustment, L refers to only labour

adjustment, B refers to adjustment of both labour and capital and N indicates the event of no

adjustment at all.

Lt

tK Et 1KtK1

Kt1

2

K

It1

b

K

I

K

P

p

I

K

t1

t1 t1

t1

FK ,L ,

2

K

t1

t1 t1 t1

Kt1

Kt1

2

bL Ht1

L H

L

P

p H

Lt1

t1 t1 t1

2 Lt1

Et

Kt1

2

2

K

L

I

H

b

b

B pI I K t1 K pH H L t1 L KL

t1

t1 t1

P

t1

t1

t1 t1

2

2

Kt1

Lt1

Kt1

30

2

K

b Its1

K I

K

P

I

ts

1 p

ts

1

K

ts1 ts1

2 K

FK ,L ,

ts

1

ts

1 ts

1 ts

1

K

K

ts

1

ts

1

2

bL H

L H

L

ts

1

P

p H

ts

1

L

ts1 ts1 ts1

2

L

ts1

K

K s s

1

t Et

1

K

s0

ts

1

2

K

I

b

I

K

ts

1

p I

ts

1

K

K

ts1 ts1

2

ts1

B

P

ts

1

2

L

H

b H

L

KL

ts

1

ts

1

ts

1

L

pts1H

2

ts

1

L

K

ts

1

Similarly we can show

2

K

Its1

b

K I

K

P

p

I

K

ts

1

ts

1 ts

1

ts

1

2 K

FK ,L ,

ts

1

ts

1 ts

1 ts

1

w

ts

1

L

L

ts

1

ts

1

2

bL H

L H

L

ts

1

P

p

H

L

ts

1

ts

1 ts

1

ts

1

2L

ts

1

L

L s s

1

t Et

1

L

s0

ts

1

2

bK Its1

K

pI I

K

ts

1

ts1 ts1

2 K

ts

1

B

P

ts

1

2

L

H

b H

L

KL

ts

1

p

H

L

t

s

1

t

s

1

t

s

1

L

2

ts1

L

ts

1

31

As shown in the above equations the shadow values of capital and labour are a function of the

expected value of the future marginal productivity of capital and labour and the changes in

the expected value of future adjustment costs. These features reflect that current decisions

affect future properties of the firm’s optimization problem. Current factor demand affects the

production scale and hence productivity of next periods and it determines the size of the

adjustment costs and the probability of adjustment. Hence, our derivations indicate that to

proxy the shadow values of labour and capital one needs to capture information on how

current decisions affect the future marginal productivity of factor inputs, the future

probability of adjustment and the change in the size of adjustment costs. The future marginal

productivity of input, the probability of future adjustment and the change in the size of future

adjustment costs in

next periods t+s are a function of the state variables

I

H

w

,

p

,

p

,t

,

K

and

L

and future decisions concerning investment and hiring (It+s

t

s

t

s

t

s

s

t

s

t

s

and Ht+s). At the beginning of a period t when the investment and hiring decisions are set,

K

L

information is available on w

t,p

t,p

t,

t,

tand

t. There are no other variables in the

I

H

model that are relevant to the optimization problem of the firm. Of course future realizations

of these quantities are relevant to the firm’s optimization problem, but these realizations are

governed by either a stochastic process (i.e. w

t

s,p

t

s,p

t

s,

t

s) or the optimal decision of the

I

H

Lts ). Hence, the firm derives expectations on these future

firm in the future (i.e. Kts and

realizations using information it has on the current realizations. The history of these variables

is irrelevant as we assume that all past information on them is contained in their current

K

L

realizations. Using the information set available to the firm (i.e. w

t,p

t,p

t,

t,

tand

t) its

I

H

management will determine both the cost of the factor demand decisions and the proceeds

K

L

K

L

given by t and t . Hence, we conjecture that t andt are a function of the state

32

K

L

variables w

t,p

t,p

t,

t,

tand

t. Hence, to obtain a proxy for the two shadow values

I

H

tK andtL we need variables that capture information on these state variables.

Suppose first that the revenue function is Cobb Douglas with constant returns to scale

1

YvK

L

then

1

YK

YL

v

1

Therefore, we suggest that the shadow values are proxied by

Y

Y

H

time

dummies,

sector

dummies

,

w

, ,

K

L

KK

t

t t

t

t t

Y

Y

H

time

dummies

,

sector

dummies,

w

, ,

K

L

L L

t

t t

t

t t

We use time dummies to capture the dynamics of investment and hiring prices. In

principle we have information on investment prices, but lack a proper variable to measure

hiring prices. To capture both we employ time dummies. Note that due to multicollinearity

we cannot use both the investment price and the time dummies. Together the latter two

variables in these functions contain information on ε, K and L. The variables used to proxy

the shadow values concern beginning of the period information. In the estimations we use

lagged values of these variables. We assume that it is easier for the firm’s management to

observe lagged rather than contemporaneous information.

K

Note that the shadow value of capital t is also a function of the marginal

productivity of labour (Y/L) and the wage rate (w). In single factor models it is usually

K

assumed that this is not the case. However, from the expression above concerning t it can

K

be seen that t is affected by expectations on future realizations of the hiring rate. Hence,

tK is a function of expectations on future outcomes of tL . As a consequence, also from this

33

K

perspective it makes sense to include Y/L and w in t . A similar argument holds for why Y/K

L

is included in t .

Real Replacement Value of Capital Stock at the end of period t (Kt): The replacement value is

computed using the perpetual inventory method. This method requires a starting value for the

capital stock. Our data do not provide information on insurance or book value of the capital

stock. Therefore we estimate the starting value as follows. The real stock of capital at the end

of year m=t0+n, where n is an integer larger than or equal to 1, is given by

Km = Im+(1-)Im-1+...+(1-)nKt0

where is the rate of depreciation set equal to 0.06. If we assume that in year t the firm

grows at a rate equal to gt then investment in the n periods should be approximately sufficient

to ensure that

Km = (1+gt0)...(1+gm)Kt0.

Given the values gt it is possible to solve for the value of Kt0. We approximate gt by

calculating the firm’s real production growth from time t-1 to t. The value of n is set equal to

5. The reason is that we need a sufficiently long period to estimate the starting value of

capital, because firms tend to concentrate investment in a relatively short period of time. If n

is very small the probability of underestimating the starting value of the capital would be

considerable. This procedure requires an uninterrupted sequence of data on production and

investment during at least five years. As our data start in 1993 and run until 2005, the starting

year for the data needed to construct the capital stock for a plant can vary between 1993 and

2000. We drop observations for which we find a negative stock of capital as these are poorly

estimated. Given the initial value the replacement value of the capital stock at the beginning

of year t is calculated using the perpetual inventory formula Kt= It-1+(1-)Kt-1.

34

KL

Figure 1: Investment Regimes, 0

35

KL

Figure 2: Investment Regimes, 0

36

Table 1: Descriptive statistics

Mean

St.dev

Correlations

I/K

L/L

(Y/K)-1

(Y/L)-1

I/K

L/L

(Y/K)-1

0,134

0,004

7,389

0,251

0,175

8,646

1,000

0,116

0,263

1,000

0,061

1,000

(Y/L)-1

1362,2

1453,3

0,002

0,067

0,179

1,000

294,6

82,6

59127,5 436941,0

75,5

130,0

-0,028

-0,039

0,006

0,106

-0,011

0,030

0,031

-0,079

-0,042

0,341

0,107

0,129

w-1

K

L

Notes: Wages, w , are defined as total wage expenditure per employee, including pay-roll taxes

Capital, K , is given in 1000 NOK (≈ € 125) in 1996 prices

w-1

K

L

1,000

0,075

0,159

1,000

0,216

1,000

Table 2: Distribution of I/K and L/L

I/K

<-0.667,-0.167]

<-0.167,0.000>

=0

<0.000,0.167]

<0.167, +>

L/L

<-0.667,-0.167] <-0.167,0.000>

=0

<0.000,0.167] <0.167, +>

0,2

0,8

1,6

5,0

1,2

0,2

1,5

3,9

23,3

6,6

0,1

0,5

2,2

9,0

3,3

0,1

0,8

2,4

19,6

8,4

0,1

0,2

1,0

4,6

3,3

0,7

3,8

11,2

61,5

22,8

8,8

35,5

15,1

31,3

9,2

100,0

38

Table 3: Correlation in timing

(I/K)+1

(I/K)-1

I/K

(I/K)+1

I/K

(I/K)-1

1,000

0,131

0,071

1,000

0,148

1,000

L/L)+1

L/L

L/L)-1

0,108

0,080

0,043

0,070

0,116

0,090

0,036

0,083

0,117

L/L)+1

1,000

-0,083

0,004

L/L

L/L)-1

1,000

-0,078

1,000

39

Table 4: Estimation Results

Investment

Hiring

0.00757

0.00644

(0.00190)

(0.00131)

(Y/L)-1

0.00000530

-0.0000107

(0.0000123)

(0.00000786)

w-1

0.000540

0.00193

(0.000185)

(0.000143)

constant

1.457

-0.381

(0.0639)

(0.0493)

Threshold Estimates

327.2

AK

(16.72)

(Y/K)-1

AL

0.918

(0.0914)

BK

327.2

(16.72)

BL

0.675

(0.0286)

Parameter Ratios

L

K

KL

K

Other Parameter

0.000179

(0.0000200)

-0.0000475

(0.0000188)

0.171

(0.0144)

N

14759

Note: Standard errors are in parentheses. Year and sector

ρε

dummies are included in the estimation but not reported here

to conserve space.

40