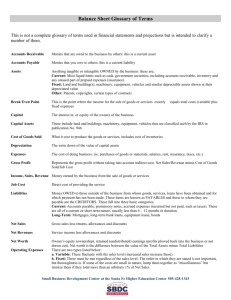

Financial Management Terms

advertisement

A-133—See OMB A-133. Account number—An assigned number providing numerical control over accounts and providing a convenient means of referring to the account. See also chart of accounts. Asset—A resource, object, or right of measurable financial value such as cash, securities, accounts receivable, land, buildings, or equipment. Audit—A series of procedures followed by a professional accountant to test, on a selective basis, transactions and internal controls in effect, all with a view to forming an opinion on the fairness of the organization’s annual financial statements. Balance sheet—See statement of position. Budget—A financial plan that estimates the monetary receipts and expenditures for an operating period. Budgets may be directed toward project or program activities and are primarily used as a comparison and control feature against the actual financial results. Capital Assets—Assets with a relatively long useful life, such as land, buildings, or equipment. See fixed assets. Capitalizing an asset—The process of recording the cost of land, buildings, and equipment as fixed assets, rather than expensing them when they are initially acquired. Cash basis accounting—An accounting system that records only those events which involve the exchange of cash and ignores transactions not involving cash. Cash flow—The difference between cash receipts and disbursements over a given period. Change in net assets—The difference between total income and total expenses, representing the surplus or deficit an organization has at the end of the year. See also Increase (decrease) in net assets Chart of accounts—A list organizing the agency’s accounts in a systematic manner, usually by account number, to facilitate the preparation of financial statements and periodic financial reports; drives the reporting capacity of an organization. See also account number. Contribution—A transfer of cash or other assets to another entity in which the transfer is unconditional, made or received voluntarily, and nonreciprocal. Credit—See debit and credit. Current assets—Assets that can reasonably be expected to turn into cash or be consumed within one year. Current liabilities—Liabilities that can reasonably be expected to be paid within one year. Current ratio—A comparison of an organization’s current assets to its current liabilities; indicates the ability to pay bills and meet financial obligations. See also current assets and current liabilities. Debit and credit—Technical bookkeeping terms referring to the two sides of a financial occurrence. Debit entries are listed on the left side of the ledger page and credit entries are listed on the right. The increase or decrease effect on the account depends on the type of account. The total value of debits must equal the total value of credits for any given financial occurrence. Debt—Borrowed funds from individuals, banks, or other institutions, generally secured with a note, which in turn may be secured by a lien against property or other assets. Ordinarily, the note states repayment and interest provisions. Deferred revenue—Revenue received before it is earned (advance ticket sales or membership dues). Deficit—Expenses and losses in excess of related income; an operating loss, as refers to an accumulation of operating losses (“negative” retained income). Depreciation expense—Accounting process to allocate the cost of capital or fixed assets to expense in a systematic and rational manner to the period the organization will benefit from the use of the asset. Diversification—In reference to nonprofit income, this means having a variety of funding types and sources so an organization is not unduly dependent on a handful of sources. Earned revenue—The amount received for goods or services delivered and for which no future liability is anticipated. Exempt employee—An exempt employee is one whose job duties fall under the executive, administrative, professional, and outside sales exemptions of the Fair Labor Standards Act (FLSA). Such employees are exempt from the overtime provisions of the FLSA. (Note: The FLSA is a complex regulation; the determination of exempt employees should be discussed with an appropriate resource). See also non-exempt employee. Fiduciary relationship—A relationship between persons based on trust and confidence. A fiduciary, such as a trustee, owes a duty of utmost good faith. Financial Accounting Standards Board (FASB)—The governing board that formulates authoritative accounting standards for nongovernmental agencies. These standards, which encompass accounting rules, procedures, and applications, define accepted accounting practice and are referred to as generally accepted accounting principles (GAAP). Fiscal year—The organization’s business year, that is, January through December or July through June. Fixed asset—An asset that has a relatively long useful life, usually several years or more, such as land, buildings, or equipment. See capital asset. Form 990—The Federal tax return required to be filed annually by most nonprofits. GAAP—See generally accepted accounting principles. General ledger—A book or file containing individual accounts in which all the transactions from journals are summarized; this is the information reported in an organization’s financial statements. Generally accepted accounting principles (GAAP)—Accounting standards for nongovernmental agencies encompassing accounting rules, procedure, and applications, and defining accepted accounting practice. See also Financial Accounting Standards Board. Grants—An unconditional promise to give assets to an organization by an individual or another organization. Grants must be recognized in the year the unconditional promise to give is received. See also multiyear grant. Income—Assets received from contributions or revenue earned from services performed. Income statement—See statement of activities. Increase (decrease) in net assets—The difference between total income and total expenses representing net financial results of operations for the period. See change in net assets. In-kind contributions—Noncash donations of voluntary services, property, equipment, or materials to which the organization can assign value. Internal controls—The plan of organization, procedures, and records designed to enhance the safeguarding of assets and reliability of records of an organization. Journal—A book of original entry in which all financial transactions are initially recorded. All journal entries are subsequently posted to individual accounts in the ledger. Liability—A claim on the assets by an outsider representing a financial obligation. Liabilities include accounts payable, accrued expenses, and loans. Liquid assets—Cash in banks and on hand, and other cash assets not set aside for specific purposes other than the payment of a current liability or a readily marketable investment. Liquidity—The quality that makes an asset quickly and easily convertible into cash. Long-term liabilities—Financial obligations extending over a number of years. Market value—The realizable amount for which an asset can be sold in the open market. Modified cash basis accounting—The same as cash basis accounting except for certain items, most typically depreciation and payroll taxes, treated on an accrual basis. This is also known as a “hybrid method.” Multiyear grant—An unconditional promise to give grant assets to an organization by an individual or another organization extending beyond one year. These grants must be recognized in the year the unconditional promise to give is received and must be recorded using a discount rate to measure the present value of the estimated future cash flow. Net assets—The difference between total assets (what is owned) and total liabilities (what is owed); “net worth.” Non-exempt employee—A non-exempt employee is one whose job duties fall under the wage and overtime provisions of the Fair Labor Standards Act (FLSA). (Note: The FLSA is a complex regulation; the determination of exempt employees should be discussed with an appropriate resource). See also exempt employee. OMB A-133—The principles for complying with federal contract awards. The A-133 audit is required of all nonprofits spending more than $500,000 in federal awards in a year. Ratio—The comparison of two numbers to create a financial indicator. See also current ratio. Reserve—The accumulated unrestricted net assets available for the organization’s use. See also net assets. Statement of activities—The financial statement summarizing the financial activity of an organization for a given period. It presents the income, expenses, and changes in net assets for the period. Also known as the income statement or profit and loss statement in the for-profit world. Statement of cash flows—The financial statement providing relevant information about the cash receipts and cash payments of an organization during a given period. Statement of functional income and expenses—This report matches income and expense by function. It details the specific types of expenses by object (rent, salaries, etc.) incurred in each of the programs and supporting activities delineated on the statement of activities. This report is used to evaluate surplus/deficit status of each activity. Statement of position—The financial statement presenting an organization’s financial position as of a specific date. It lists assets, liabilities, and net assets. Also referred to as the balance sheet. Support—Income from voluntary contributions and grants. Temporarily restricted contributions—Grants and contributions to be spent for a specific purpose or during a restricted period of time. Unrelated business income—Income generated for a nonprofit organization through an activity not substantially related to the purpose for which the nonprofit received taxexempt status. The activity must be a trade or a business; and it must be regularly carried out. Unrelated business income tax (UBIT)—A tax nonprofit organizations are required to pay on income generated through an activity not substantially related to the organization’s tax-exempt purpose.