Will Korean Companies Increase Their Overseas Investment

advertisement

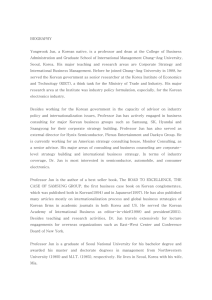

Will Korean Companies Increase Their Overseas Investment in the ALADI Countries?: Implications of Investment Success Cases Hong, Uk Heon Division of Public Administration, Uiduk University Contents I. Introduction: Small at Present but Great Potential II. What Promoted Korean Companies to Invest in Latin America and the Caribbean? 1. Which Korean Companies Invested in What Industries and How? 2. Why the ALADI Countries? III. How Did Korean Overseas Companies Operate in ALADI? 1. KOBRASCO Case 2. Samsung Tijuana Park Case IV. Conclusion: More Active for the Manufacturing of El Dorado Reference I. Introduction: Small at Present but Great Potential Latin America and the Caribbean, especially the ALADI (Asociación Latinoamericana de Integración) countries, have emerged as an important overseas investment market for the Korean companies since the late 1980s. For example, the Korean accumulated overseas investment in Latin America and the Caribbean until the end of 1985 amounted only to 10.8 million US dollars at current price, 1.6% of that in the world. But the figures increase rapidly up to 3,479 million dollars, 7.8% of the Korean total accumulated overseas investment at the end of Jan. 2004 (See Table 1). In the late 1980s and again the late 1990s when world foreign direct investment (FDI) was booming to go to China, Korean overseas investment grew more rapidly in Latin America and the Caribbean than in the world (See Table 2). Korean companies are expected to expand their overseas investment in Latin America at a considerably high speed in the coming decades. Why? First, the size of Korean overseas investment is relatively small compared to that of Korean economy. While Korean overseas investment was about 3.0 billion dollars in 2002, its share in the world FDI captured only 0.4%. Korean overseas investment also grasped 0.4% of the world FDI in Latin America and the Caribbean. However, Korea attracted 2.6% of the world FDI inflow. The share of Korean GDP and trade in the world was 1.4% and 2.3% respectively. Second, Korean overseas investment in the world is riding on the wave of growing. It has increased rapidly since the late 1980s. As seen in Graph 1, Korean overseas investment increased 6 times during the five years from 1986 to 1990, 4 times from 1991 to 1995, and 2 times from 1996 to 2000 respectively, compared to the previous five years. In the midst of world recession from 2001 to 2003, the annual average of Korean overseas investment amounted to 3.9 billion dollars. Third, Korean companies are highly exportoriented. The share of trade in the Korean GDP reached over 80% in 2002. Under a situation of forming regional free trade blocs, such as NAFTA and MERCOSUR, Korean companies are likely to choose overseas investment to keep up with export market share. Korean overseas investment occupied 0.8% of its GDP, but Latin American one was 3.7%, much higher with less dependence on export. Fourth, increasing domestic labor costs propel various manufacturing industries to search for cheaper labor outside. For example, Korean light industries such as textile and clothing are moving their production facilities rapidly to China to reduce labor costs. Although Korean and Latin American general economic environments are unfolded to interdependent investment, its actualization seems to depend on complex processes. This paper intends to present some information that may help enhance Korean overseas investment in Latin America and the Caribbean, especially in the ALADI countries, by observing the Korean recent overseas investment experiences. This paper does not aim at proving any investment theory. Rather, it tries to present their implications. My observation shows that Korea and the ALADI countries, though they locate far away and have different cultures, have great potential to become important economic partners for development. 2 Table 1. Composition of Korean Accumulated Overseas Investment Value by Area, until Jan. 2004 1980 (% ) Asia Middle East North America Latin America & the Caribbean Europe Africa Oceania Total (1,000 US$) 1985 (% ) 1995 (% ) 2000 (% ) 2003 (% ) Jan. 2004 (% ) 33.9 16.0 22.4 21.6 9.7 31.8 42.4 5.1 30.4 40.8 2.3 29.9 41.0 1.8 28.9 41.0 1.8 28.8 3.3 3.6 17.3 3.4 100.0 145,986 2.0 11.2 5.1 18.6 100.0 546,915 3.8 13.0 2.5 2.9 100.0 11,924,464 9.0 13.3 2.1 2.5 100.0 32,791,497 7.8 16.5 1.7 2.3 100.0 44,401,401 7.8 16.6 1.7 2.3 100.0 44,658,820 Source: Export-Import Bank of Korea, “Overseas Investment Information,” 2004. Table 2. Annual Growth Rates of Korean Overseas Investment Value in the World and Latin America & the Caribbean from 1981 to 2003 W orld (%) Year 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 19.4 58.2 39.7 13.1 26.0 33.4 56.2 19.0 42.3 49.8 38.7 30.5 24.2 35.5 35.7 37.0 22.0 23.7 13.3 17.4 15.4 8.1 8.5 Latin America & the Caribbean (%) 20.0 18.1 4.5 10.2 35.9 25.1 31.2 80.0 173.3 76.4 27.0 18.6 18.8 18.1 37.4 59.6 39.2 24.4 18.4 102.3 3.3 8.1 4.9 Source: Export-Import Bank of Korea, “Overseas Investment Information,” 2004. 3 4,500,000 4,173,407 4,000,000 3,869,968 3,500,000 1,000 US$ 3,000,000 2,500,000 2,000,000 1,807,594 1,500,000 1,000,000 467,915 500,000 80,186 0 1981-85 1986-90 1991-95 1996-00 2001-03 Period Graph 1. Annual Average of Korean Overseas Investment Dollars during 1981-03 II. What Promoted Korean Companies to Invest in Latin America and the Caribbean? Few can deny that Korean companies will invest in Latin America and the Caribbean region to maximize their profit. However, the reasons why Korean companies evaluate the area to be profitable may differ from company to company and from country to country. Characteristics of recent Korean overseas investment experiences can help to clarify them. Among others, which Korean companies participated in overseas investment in Latin America and the Caribbean? In which industries were they engaged? In what size project did they invest? Which countries were attractive to them? 1. Which Korean Companies Invested in What Industry and How? Up to January 2004, over 500 Korean overseas projects invested 3,480 million US$ in Latin America and the Caribbean, except Belize (See Table 3). It is Korean large companies that were dominant investors. In terms of realized investment value, Korean large companies occupied more than 70% in manufacturing, construction, hotels and restaurants (See Table 4). However, Korean small and medium companies played a major role in business services and clothing. For example, Littawatech, a Korean small internet venture, invested 1,376 million dollars in internet business in Bermuda in 2000, which was the largest project among all the Korean investment there. Korean small and medium companies were concentrated in textile and clothing industries (See Table 5). They also contributed over a half of the total Korean overseas investment in some other manufacturing industries, such as assembled machines, nonmetallic minerals, paper and printing, and machines (See Table 6). 4 Table 3. Korean Accumulated Investment Cases and Amount in Latin America, until Jan. 2004 Projects AlADI Mexico Peru Brazil Argentina Venezuela Chile Bolivia Colombia Ecuador Paraguay Uruguay Central America The Caribbean Others Total Amount % 46.7 15.5 3.6 7.9 7.7 1.3 4.5 1.3 2.1 1.1 0.9 0.9 38.3 14.4 0.6 100 250 83 19 42 41 7 24 7 11 6 5 5 205 77 3 535 (1,000 US$) 1,196,759 283,741 282,689 277,836 136,417 66,491 61,761 59,316 19,309 5,336 3,260 603 394,689 1,883,792 4,265 3,479,505 % 34.4 8.2 8.1 8.0 3.9 1.9 1.8 1.7 0.6 0.2 0.1 0.0 11.3 54.1 0.1 100 Source: Export-Import Bank of Korea, “Overseas Investment Information,” 2004. Table 4. Share of Korean Overseas Investment Value by Large Firms in the Total, up to Jan. 2004 Asia Middle North Latin America Europe Africa Oceania & the East America Agriculture, Forestry & Fishing 34.2 Mining 93.6 Manufacturing 59.8 Construction 79.6 Wholesale & Retail 84.7 Transportation & Storage 71.3 Communication 91.6 Banking & Insurance 0 Restaurants & Hotels 86.1 Real Estates & Business Services 69.3 Others 0.0 Total of Large Firms 66.7 Caribbean 100.0 100.0 83.3 77.6 90.2 95.1 0 52.6 71.0 86.8 68.7 86.8 41.5 61.5 18.0 65.8 57.7 97.0 73.1 90.7 93.4 74.8 8.7 0.3 97.5 87.4 97.2 46.9 0 80.4 1.7 0 45.1 40.3 84.8 95.2 100.0 98.3 94.2 100.0 0.0 96.9 74.5 95.3 Total of Large Firms 2.1 98.9 90.1 87.3 97.4 0 99.9 99.9 85.4 63.6 49.8 55.9 89.7 5.8 79.4 30.5 58.6 89.8 73.4 75.3 89.7 65.4 75.9 12.4 79.3 36.3 95.5 77.0 69.9 40.6 0 74.9 Source: Export-Import Bank of Korea, “Overseas Investment Information,” 2004. 5 Table 5. Composition of Korean Total Overseas Investment in Manufacturing Industries in Latin America & the Caribbean by Company Size, until Jan. 2004 Food & Beverage Textile & Clothing Shoes & Leather Timber & Furniture Paper & Printing Petroleum & Petrochemical Nonmetallic Mineral Iron & Steel As s embled Metal Machine Electronic Communication Equipments Trans portation Machines Others Total Small and Medium Large Companies (%) 4.3 74.3 2.9 1.3 0.1 3.7 0.3 0.0 3.5 1.7 Companies (%) 4.6 19.7 1.9 0.4 0.0 8.6 0.1 13.2 0.0 0.4 All Companies (%) 4.5 34.2 2.2 0.7 0.0 7.3 0.2 9.7 0.9 0.8 5.5 1.1 1.3 100.0 49.5 1.2 0.4 100.0 37.8 1.2 0.7 100.0 Source: Export-Import Bank of Korea, “Overseas Investment Information,” 2004. Table 6. Composition of Korean Companies in Manufacturing Industries in Latin America & the Caribbean, by Accumulated Investment Value up to Jan. 2004 Small and Medium Large Companies All Companies Companies (%) (%) (%) Food & Beverage 25.2 74.8 100.0 Textile & Clothing 57.7 42.3 100.0 Shoes & Leather 35.1 64.9 100.0 Timber & Furniture 52.6 47.4 100.0 Paper & Printing 100.0 0.0 100.0 Petroleum & Petrochemical 13.3 86.7 100.0 Nonmetallic Minerals 49.0 51.0 100.0 Iron & Steel 0.1 99.9 100.0 Assembled Metals 100.0 0.0 100.0 Machines 59.8 40.2 100.0 Electronic Communication 3.8 96.2 100.0 Equipments Transportation Machines 24.1 75.9 100.0 Others 51.7 48.3 100.0 Total 26.5 73.5 100.0 Source: Export-Import Bank of Korea, “Overseas Investment Information,” 2004. In which industry did Korean companies invest? Business services drew the largest project from Korean investors. The tax-free Caribbean islands were popular to them as good places to locate a corporate headquarter. Manufacturing and mining are the next most attractive industries to Korean companies. In terms of realized investment dollars, Korean companies tended to invest in manufacturing and mining second to business services (See Table 7). Wholesale and retail services attracted Korean companies much less in Latin America and the Caribbean than in North 6 America and Europe. What size projects were Korean companies willing to invest in? Compared to Asia and Oceania, Latin America and the Caribbean had a larger share of large firms over 50 million US$ (See Table 8). Korean companies tended to invest in large projects of over 50 million dollars. Until 1985, there were no projects over 5 million US$ by the Korean companies (See Table 9). However, they have financed projects with over 50 million US$ after 1995. Korean investment projects with 50 million US$ and over occupied about 60 % of all the projects’ value at the end of Jan. 2004 (See Table 10). Table 7. Composition of Korean Accumulated Overseas Investment Value by Area and Industry, up to Jan. 2004 (%) Asia Middle North Latin America & the America Caribbean Europe 3.4 14.2 26.8 0.8 7.6 0.1 2.6 53.8 0.1 34.5 0.9 25.2 23.4 0.2 16.6 14.1 26.3 9.5 7.6 25.7 1.0 6.2 53.2 1.8 21.8 1.1 4.1 0.3 3.5 0.1 2.6 0.4 0.1 0.6 3.1 0.0 0.0 0.0 0.0 0.0 0.1 1.4 30.3 7.7 2.5 East Agriculture, Forestry & Fishing 0.6 0.0 0.4 Mining 3.3 84.1 2.7 Manufacturing 67.7 7.5 47.7 Construction 2.5 4.3 1.4 Wholesale & Retail 13.4 1.1 31.6 Transportation & Storage 0.8 0.2 0.5 Communication 3.0 0.0 3.2 Banking & Insurance 0.0 0.0 0.1 Restaurants & Hotels 1.9 0.1 2.9 Real Estates & Business Services 6.8 2.6 9.5 Others 0.0 0.0 0.0 Total (%) 100.0 100.0 100.0 Amount 18,307,625 811,309 12,881,444 Africa Oceania Total Areas 41.9 3.7 0.8 8.7 9.7 0.0 0.0 0.0 0.0 0.0 100.0 100.0 100.0 100.0 100.0 3,479,505 7,404,797 751,808 1,022,332 44,658,820 Source: Export-Import Bank of Korea, “Overseas Investment Information,” 2004. Table 8. Composition of Korean Overseas Investment Value by Project Size, until Jan. 2004 (%) Less than Less than Less than Less than Over 50 Total 1 million 5 million 10 million 50 million US$ US$ US$ US$ million US$ Asia 13.3 17.6 9.6 28.2 31.3 100.0 Middle East 2.7 5.0 1.5 14.1 76.7 100.0 North America 7.1 8.6 6.3 18.3 59.7 100.0 Latin America & the Caribbean 2.9 9.1 4.8 23.4 59.8 100.0 Europe 1.8 4.0 4.5 28.0 61.8 100.0 Africa 2.5 5.5 3.3 58.0 30.7 100.0 Oceania 11.5 13.6 8.8 36.3 29.8 100.0 Total 8.4 11.6 7.2 25.4 47.6 100.0 (1,000 US$) 3,729,480 5,170,774 3,195,858 11,325,707 21,237,001 44,658,820 Source: Export-Import Bank of Korea, “Overseas Investment Information,” 2004. Table 9. Korean Overseas Investment in Latin America and the Caribbean, 1985 (1,000 US$) 7 ALADI Chile Argentina Brazil Mexico Uruguay Venezuela Ecuador Central America Panama Honduras El Salvador Costa Rica The Caribbean Bermuda Dominican Rep. Cayman Irslands Puerto Rico Others Surinam Total Projects Projects' of Less Value of than I Less than Million I Million US$ US$ 11 714 0 0 2 107 2 269 4 153 1 66 1 60 1 59 23 4,691 20 3,531 1 450 1 410 1 300 2 844 1 500 1 344 0 0 0 0 1 20 1 20 37 6,269 Projects Projects' of Less Value of than 5 Less than Million 5 Million US$ US$ 2 4,558 1 2,500 1 2,058 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 2 4,558 Total Total Projects' Projects 13 1 3 2 4 1 1 1 23 20 1 1 1 2 1 1 0 0 1 1 39 Value 5,272 2,500 2,165 269 153 66 60 59 4,691 3,531 450 410 300 844 500 344 0 0 20 20 10,827 Source: Export-Import Bank of Korea, “Overseas Investment Information,” 2004. Table 10. Composition of Korean Investment Project Size in Latin America and the Caribbean, up to Jan. 2004 (%) A lA D I M exico P eru B razil A rgentina V enezuela C hile B olivia C olom bia E cuador P araguay U ruguay C e n tra l A m e ric a T h e C a rib b e a n O th e rs Total (% ) (1,000 U S $) P rojects of Less than 1 M illion U S $ P rojects of Less than 5 M illion U S $ P rojects of Less than 10 M illion U S $ 3.5 4.3 1.1 2.6 4.3 2.4 7.7 1.9 19.8 22.6 14.4 100.0 10.5 0.9 100.0 2.9 100,464 10.0 15.2 1.5 6.0 16.4 3.0 22.6 7.7 28.2 77.4 85.6 0.0 37.4 2.5 0.0 9.1 317,623 4.7 2.0 5.9 3.1 13.5 10.1 0.0 0.0 0.0 0.0 0.0 0.0 15.0 2.8 0.0 4.8 168,674 P rojects of P rojects of Less than 50 O ver 50 M illion M illion U S $ US$ 46.5 78.5 16.3 52.1 65.8 0.0 69.6 0.0 52.0 0.0 0.0 0.0 20.9 9.3 0.0 23.4 813,734 Total P rojects' V alue 35.3 100.0 0.0 100.0 75.3 100.0 36.2 100.0 0.0 100.0 84.5 100.0 0.0 100.0 90.3 100.0 0.0 100.0 0.0 100.0 0.0 100.0 0.0 100.0 16.2 100.0 84.5 100.0 0.0 100.0 59.8 100.0 2,079,010 3,479,505 Source: Export-Import Bank of Korea, “Overseas Investment Information,” 2004. 2. Why the ALADI Countries? 8 Korean overseas investment in Latin America and the Caribbean had increased remarkably from 1986 to 1990 and from 1996 to 2000. As shown in Table 11, about 6 % and 12% of the total Korean overseas investment went to Latin America and the Caribbean countries respectively. Manufacturing industries absorbed most of investment dollars. Brazil and Mexico held its lion’s share in the late 1990s (See Tables 12 and 13). Latin America was attractive to Korean companies for three reasons: the expansion of export market, the development of raw materials, and the reduction of labor costs. Korean overseas investment in Peru and Chile was mainly for the development of raw materials. The Caribbean countries were attractive because of their tax-free policies and low labor costs. Dominican Republic, Guatemala and other Middle American countries were known for low labor costs. Korean overseas investment in Mexico and Brazil aimed to expand export market. Before NAFTA, Mexico’s Maquiladora program allowed Korean companies to utilize free customs zone for assembling and exporting their products to North America. Recent Korean investment in Mexico and Brazil aimed to expand domestic market. Korean companies had been interested in Middle America much more than in ALADI until the early 1990. For example, Guatemala and Panama topped the Korean overseas investment in Latin America until 1994. Textile and clothing were a major industry into which Korean investors thronged. Its target market was not Middle America but North America. The former was attractive as production bases because they provided with free trade zone and their products could get an easy access to the North American market. After NAFTA, the ALADI countries attracted more Korean overseas investment than other neighbors. ALADI countries were especially attractive in manufacturing industries, such as electronic communication equipments, to Korean investors. Table 11. Korean Total Overseas Investment by Region and Years, up to Dec. 2003 (Unit: 1,000 US$, %) Up to Jan. 1981- Jan. 1986- Jan. 1991- Jan. 1996- Jan. 2001Total 1980 Dec. 85 Dec. 90 Dec. 95 Dec. 00 Dec. 03 (1981-03) Asia 49,533 68,525 599,287 4,335,996 8,326,397 4,811,042 18,190,780 Middle East 23,393 29,630 264,292 289,413 141,452 59,606 807,786 North America 32,727 141,372 1,088,542 2,362,048 6,183,551 3,031,117 12,839,357 Latin America & the Caribbean (Share in Total) Europe Africa Oceania Total 4,879 3.3 5,213 25,266 4,975 145,986 5,948 1.5 56,099 2,740 96,615 400,929 143,396 6.1 111,107 36,941 96,012 2,339,577 293,641 3.2 1,378,370 233,000 145,504 9,037,972 2,516,187 12.1 2,806,834 403,386 489,226 20,867,033 507,081 4.4 2,965,550 48,128 187,380 11,609,904 3,471,132 7.8 7,323,173 749,461 1,019,712 44,401,401 Source: Export-Import Bank of Korea, “Overseas Investment Information,” 2004. Table 12. Composition of Korean Total Investment in Manufacturing in Latin America and the Caribbean by Project Size, up to Jan. 2004 (%) 9 P ro jects o f P ro jects o f P ro jects o f P ro jects o f P ro jects o f Less than Less than O ver 5 0 Less than 1 Less than 5 1 0 M illio n 5 0 M illio n M illio n M illio n U S $ M illio n U S $ US$ US$ US$ ALAD I 3 6 .1 3 3 .9 2 8 .9 6 7 .7 7 1 .0 B razil 5 .7 2 .8 0 .0 3 8 .0 4 5 .5 M exico 1 7 .1 1 9 .2 9 .2 2 9 .7 0 .0 Venezuela 0 .1 0 .0 1 0 .7 0 .0 2 5 .5 C hile 4 .5 5 .5 0 .0 0 .0 0 .0 Argentina 1 .6 4 .4 0 .0 0 .0 0 .0 P eru 0 .2 0 .0 9 .0 0 .0 0 .0 C o lo m bia 3 .5 1 .2 0 .0 0 .0 0 .0 P araguay 0 .1 0 .8 0 .0 0 .0 0 .0 B o livia 1 .5 0 .0 0 .0 0 .0 0 .0 E cuado r 1 .1 0 .0 0 .0 0 .0 0 .0 U ruguay 0 .8 0 .0 0 .0 0 .0 0 .0 C entral Am erica 5 5 .5 5 8 .6 4 3 .3 8 .5 2 9 .0 The C aribbean 8 .3 7 .5 2 7 .8 2 3 .8 0 .0 To tal 1 0 0 .0 1 0 0 .0 1 0 0 .0 1 0 0 .0 1 0 0 .0 Source: Export-Import Bank of Korea, “Overseas Investment Information,” 2004. To tal Investm ent D o llars 5 6 .3 2 7 .3 1 8 .1 6 .7 1 .5 1 .1 0 .6 0 .5 0 .2 0 .1 0 .1 0 .1 2 9 .9 1 3 .8 1 0 0 .0 Table 13. Composition of Korean Total Investment Dollars in Latin America and the Caribbean by Industry, up to January 2004 (%) Agriculture, Mining Manufac Wholesale Communi Others* Total Forestry & Fishing turing & Retail cation 0.2 0.0 59.6 14.4 17.4 8.3 100.0 0.0 93.5 2.0 4.2 0.0 0.2 100.0 0.0 3.1 91.7 2.7 0.8 1.8 100.0 24.7 0.0 50.6 20.1 0.0 4.6 100.0 Mexico Peru Brazil Panama British Virgin 5.1 0.0 67.5 1.8 0.2 25.5 100.0 Islands Argentina 21.6 28.6 7.5 40.8 0.0 1.5 100.0 Cayman Islands 0.4 4.0 0.7 0.8 61.3 32.7 100.0 Honduras 12.5 0.0 86.2 0.6 0.0 0.6 100.0 Guatemala 0.0 0.0 99.9 0.0 0.0 0.1 100.0 Puerto Rico 0.0 0.0 0.0 100.0 0.0 0.0 100.0 Venezuela 0.1 0.0 94.6 5.3 0.0 0.0 100.0 Chile 4.8 50.5 23.0 21.5 0.2 0.0 100.0 Bolivia 2.4 90.3 1.6 5.7 0.0 0.0 100.0 Bahamas 0.0 0.0 6.6 0.0 0.0 93.4 100.0 Costa Rica 11.9 0.0 83.8 1.8 0.0 2.4 100.0 Colombia 0.0 0.0 23.8 75.3 0.4 0.5 100.0 El Salvador 0.0 0.0 100.0 0.0 0.0 0.0 100.0 Jamaica 0.0 0.0 100.0 0.0 0.0 0.0 100.0 Nicaragua 23.9 0.0 76.1 0.0 0.0 0.0 100.0 Ecuador 79.3 0.0 12.2 8.6 0.0 0.0 100.0 Uruguay 19.6 0.0 80.4 0.0 0.0 0.0 100.0 Bermuda 0.0 6.2 0.0 0.0 0.9 92.9 100.0 Others 43.9 4.6 48.4 3.1 0.0 0.0 100.0 Total 3.4 14.2 26.8 7.6 4.1 43.9 100.0 *: Includes construction, transportation & storage, banking & insurance, real estate, & business services, and hotels & restaurants. Source: Export-Import Bank of Korea, “Overseas Investment Information,” 2004. III. How Did Korean Overseas Companies Operate in ALADI? 10 Although Latin America is unfamiliar to Koreans, their overseas investment results show that the region has no evidence of disadvantage to Korean economic activity compared to other areas. Actually, Korean overseas investment in Latin America has been remarkably successful. For example, the ratio of liquidated Korean overseas investment among the realized was quite low. The percentage of realized investment value among the planned was higher than the Korean average. In the ALADI countries, except Uruguay and Chile, the liquidated rates were about 10% or lower (See Tables 14 and 15). Most Korean overseas investment cases in Latin America had a type of 100 % stockholding. Investment dollars by joint venture firms were only 5% of the total. While American or European overseas investment was for merge and acquisition, Korean one was mainly for production and export (See Table 16). In the operation, Korean investors were much concerned with a high turnover rate of employees. To reduce it, salary was paid at different days in group. Another concern was that Labor market was considerably inflexible. Although labor regulations became less tight, it is desirable that they still become more flexible. The following two investment success cases may help to understand how to operate Korean overseas investment more effectively. One case is Kobrasco, a joint venture by POSCO and CVRD. The other is Samsung Tijuana Park, all of whose stocks Samsung Group owns. Table 14. Korean Accumulated Overseas Investment by Area and Project Status, up to Jan. 2004 N um ber of Project Investm ent Am ount Realized/Pl Invested/P Liquidated/ Realized/Pl Invested/Pl Liquidated/ anned lanned Realized anned anned Realized Projects Projects Projects (% ) (% ) (% ) Dollars (% ) Dollars (% ) Dollars (% ) Asia 83.6 79.5 4.8 58.1 79.6 24.3 M iddle East 78.3 49.6 36.6 82.0 34.7 63.7 N orth Am erica 90.4 79.5 12.1 73.6 78.2 25.7 Latin Am erica & the C aribbean 81.7 67.3 17.6 68.8 88.6 9.5 Europe 84.6 71.4 15.6 71.1 81.6 18.7 Africa 74.2 55.6 25.2 62.4 74.6 30.7 O ceania 84.2 73.5 12.7 30.4 85.5 25.7 A verage 84.8 78.3 7.7 63.7 79.8 23.5 Source: Export-Import Bank of Korea, “Overseas Investment Information,” 2004. Table 15. Ratios of Korean Realized, Liquidated Investment Cases and Amounts over the Planned in Latin America, until Jan. 2004 11 Total Realized Cases/Total ALADI Peru Mexico Brazil Argentina Chile Venezuela Bolivia Colombia Ecuador Paraguay Uruguay Ce n tr a l Ame r ic a T h e Ca r ibbe a n Oth e r s Total Planned (%) 80.8 86.4 80.8 79.2 85.4 78.1 87.5 77.8 73.3 75.0 85.7 71.4 82.4 82.1 100.0 81.7 Total Total Total Realized Liquidated Liquidated Amounts/Tot Cases/Total al Planned Amounts/Total Realized (%) (%) Realized (%) 13.0 52.4 10.0 5.3 54.3 8.1 7.1 67.1 12.8 16.7 44.3 1.3 14.6 42.6 12.3 8.0 87.9 43.7 28.6 67.3 10.2 14.3 34.8 1.1 9.1 56.0 8.3 33.3 30.7 1.9 16.7 41.7 3.6 80.0 61.2 85.9 23.3 68.1 27.4 16.7 86.3 5.4 33.3 79.2 0.5 17.6 68.8 9.5 Source: Export-Import Bank of Korea, “Overseas Investment Information,” 2004. Table 16. Korean Investment in Latin America and the Caribbean by Financing Type, Jan. 2004 Investment Cases (%) Investment Dollars (%) Joint Venture 1.1 5.1 Loan 1.1 9.0 Private Financing 1.5 0.0 Stock Investment 96.3 85.9 Total 100.0 100.0 Source: Export-Import Bank of Korea, “Overseas Investment Information,” 2004. 1. KOBRASCO Case A. Brief Introduction of Kobrasco ○. Company Name: Companhia Coreano-Brasileira De Pelotizacao (KOBRASCO). Located in Vitoria, Espirito Santo, Brazil. Connected to Tubarao port. ○. Major Business: Production and sale of 4 million tons of pellet a year. ○. Foundation: March 6, 1996. ○. Total Investment Amount: 220 million US$ ○. Investment Capital: 77 million US$ ○. Investment Type: Joint venture. POSCO: 50%, CVRD (Companhia Vale do Rio Doce): 50%. ○. Representative: Co-executive. One from CVRD, another from POSCO ○. Employees: 80 persons. ○. Management: Only CVRD is in charge of operation. B. Short History ○ July 29, 1995: Agreement signing of joint venture and stock-holding type 12 ○ Sept. 28, 1995: Firm site began to be constructed at CVRD’s yard. ○ March 6, 1996: A joint venture corporation was established. ○ Sept. 9, 1996: Main facility began to be constructed. ○ Oct. 9, 1998: Production began. ○ Nov. 16, 1998: Ceremony held for the completion of construction. C. POSCO and CVRD Pohang Iron and Steel Co., Ltd. (POSCO), established April 1968, is the largest steel mill in the world in terms of crude iron production. POSCO has two steel works at Pohang and Gwangyang, which had expanded their production capacity until 1992. POSCO, privatized completely on Oct. 2000, produces some 26 million tons of iron and steel each year, enough to produce about 100,000 compact cars a day. Today, POSCO exports its products to over 60 countries around the globe. Its major products include hot rolled sheet, plate products, steel wire rods, cold rolled sheet, electrical sheet, and stainless steel CVRD, a Brazilian conglomerate, produces iron ore and pellets, operates logistics, and runs three hydroelectric power plants. CVRD was privatized in 1977 E. Why Did POSCO Decide to Build Kobrasco? From the late 1980s, POSCO has been little interested in expanding production facilities for crude iron, because of its world oversupply. However, it was concerned with improving its quality, its international competitiveness, and its value-added products, such as stainless steel and electrical sheet. In the early 1990s, POSCO increased its direct overseas investment actively in Southeast Asia and China to promote the export of value-added steel products. Why did POSCO decide to invest in Brazil for pellet? POSCO’s overseas investment in pelletmaking is intended to secure its stable import. Pellet, processed iron ore, can increase in the productivity of crude-iron making. In POSCO’s view, the success of its overseas investment depended not on maximizing profit but on obtaining low-priced quality pellet. POSCO had invested in Australia and Canada to secure the import of other raw materials from the early 1980s. POSCO has achieved surplus net profit after depreciation every year since 1974, which means that it has financial capacity for overseas investment in pellet-making. What mattered was where to invest. India, Australia, and Brazil were known to be good places to produce pellet. Although India was blessed with pellet material, it was not chosen as the best place to invest because of poor transportation infrastructure. Australia also owned affluent materials for pellet, but was already one of the largest suppliers of iron ore to POSCO. Brazil was chosen for pellet site, because it had affluent quality iron ore and adequate transportation infrastructure. Brazil could be an alternative supplier of iron ore. Moreover, Brazil was less regulative to pellet production. 13 Kobrasco was a success to POSCO in several aspects. First, Kobrasco took only one year of experimental operation before reaching its full operation. Compared to Nabrasco, a Nippon SteelCVRD joint venture, Kobrasco took two years less for the full operation. Second, it took only three years from making contract to finishing Kobrasco plants, which was shorter period than expected. Since steel industry took considerably long period from plant construction to production, the shortening of construction period was important to reduce production costs. Third, Kobrasco operated at full capacity for 6 years and provided POSCO with pellet. Although Kobrasco did not expand production capacity, it achieved stable production and sale to POSCO. What contributed to the stable production of pellet at Kobrasco? Among others, the localization of operation is the most important. While POSCO’s representative participated in executive, the Brazilian partner, CVRD, was in full charge of operation. Second, Brazilian partner, CVRD, participated fully in preparation stages for joint venture, which allowed POSCO to save time and man power. POSCO sent only two professionals for preparing the joint venture. However, there were some bottlenecks in POSCO’s investment in Brazil. First, Brazil’s high interest rates, high country risk and strict foreign exchange regulation impeded local financing. For example, POSCO chose to borrow 220 million US$ from Citibank by project financing instead of borrowing from Brazilian Banks. It is because Brazilian interest rate was 3% higher than the Libor rate, and Brazil applied interest rates of hot money to loans with less than 7 years of maturity. Continuous devaluation of Real reduced Kobrasco’s asset to a half. Second, insecurity in city life made foreigners to be reluctant to reside in Brazil. POSCO’s correspondents in Brazil mentioned that they seldom went out at night. Third, Brazilian labor conditions were still conceived strict in hiring and firing. For example, the rule of six months’ paid leave to pregnant employees made foreigners cautious about recruiting women. 2. Samsung Tijuana Park Case A. Brief Introduction - Samsung Tijuana Park is composed of three Samsung plants: ○ Samsung Mexicana (Samex): Produces television sets, computer monitors, cellular phones and computers. ○ Samsung Display Interface Mexicana (SDIM): Manufactures the cathode-ray tube (CRT) monitors. In 1997, the plant began to produce Liquid Crystal Display (LCD) monitors. ○ Samsung Electro-Mecánicos Mexicana (SEMSA) Produces electronic components for televisions, monitors, which are used in the above two plants. - The three plants are located in Tijuana, Baja California. 14 - Major Figures in 2003 ○ Employment: 6,000 full-time employees. ○ Operation rate: 96.2%. ○ Sales: 2,059 million US$ ○ Production: Monitor, 4 million sets (CDT models: 5, LCD models: 9); TV production, 3 million sets (TV models: 90); Assembled PCs, 100 thousand; HHP production, 900 thousand. - Investment amount: Over US$ 200 million. Samsung Group owns 100% of stocks. - Samsung Electronics is also operating two other plants in Querétaro and Mexico City. B. Samsung Electronics and Samsung Group Samsung Electronics is a global company, which operates everywhere in the world. Among others, it operates 28 overseas production facilities and 11 research institutes. Samsung Electronics is a major company of Samsung Group. C. Brief History of Samsung Tijuana Park Samsung Electronics initiated its overseas investment in Tijuana in 1988. SAMEX aimed entirely at the North American Market and utilized merits of Maquiladora program. SAMEX started with investment of 3,700 million US$ and assembled television sets. After NAFTA became effective, Samsung Electronics changed its target market from North America to Mexico. It also adopted the strategy of localization of electronic parts. In 1994, Samsung Group inaugurated Samsung Tijuana Park, and integrated the production of components and finished products vertically. Over 200 million US$ was invested. Until 2001, five new plants and renovation continued. Samsung Display Interface (SDI) and Samsung Electro-Mechanics (SEM) invested respectively in SDIM and SEMSA. D. How Did Samsung Tijuana Park Run? Samsung Group succeeded in its overseas investment in Samsung Tijuana Park in terms of market expansion and of regional development in Mexico. The Park sold about 30 percent of its products inside Mexico in 2003. Turnover rates of employees there recorded only 3% in 2003 and labor union was not organized yet. What contributed to the Samsung Group’s investment success in Tijuana? In general, Samsung Group’s management experiences became congruent with Mexican investment conditions. Among the Samsung Group’s experiences, active risk-taking management was important. Samsung Group makes it a management principle to invest and sale anywhere there is a market. Second, Samsung Group emphasizes the importance of employee welfare and community services. Samsung Tijuana Park was not exceptional. For example, the Park provided various cultural, sports events for employees regularly. It also organized community service teams with 15 volunteer employees to help local communities frequently. Daycare Center and clinic were built in 2000. Samsung Tijuana Park made a commitment to provide handsome scholarship to Mexican students from 2000. Lat year, 20 university students received benefits. These students have job offers from the Park after their graduation. Third, Samsung Tijuana Park gave a special importance to employee training and education. In 2003, it supported 16 employees to enroll to MBA program. The emphasis on human resources is an old management principle of Samsung Group. Samsung Group employs over three thousand professionals with doctorate degrees. Its present President says, “One excellent person can supports one hundred thousand people to hold jobs,” and “Ten second-grade Go players cannot beat one professional first-grade one.” Fourth, the localization and decentralization of management contributes to the perfection of products. Samsung Group has a tradition to scrutinize all the aspects of applicant, but provide with best salary and autonomy when hired. Samsung Tijuana Park filled most of managerial positions except CEO with the Mexicans. Fifth, the Park invested actively in Mexico to localize its components. Unlike traditional Maquiladora assembly plants, the Park has three major vertically integrated plants of components and finished products. Now it is sourcing most of its materials locally. Over 900 of all materials are procured locally. Sixth, Mexico’s investment environments also contributed to the success of Samsung Tijuana Park. The formation of NAFTA was a turning point for foreign capital to invest in Mexico. Its domestic market is much more favorable to foreign direct investors. Tijuana is also a good industrial park to get components for electronic equipments with cheap price and to cooperate with other electronic companies. Tijuana is the television capital of the world, churning out sets for all the top brands. Tijuana has numerous foreign production and sales subsidiaries of the globally famous electronic companies. However, there are some barriers for Korean investors in expanding their investment in Mexico. Among others, Mexico needs to provide more industrial sites for groups of component producers to cooperate and supply other companies. Mexico has tax-free zones but does not have many industrial parks deep inside border. IV. Conclusion: More Active for the Manufacturing of El Dorado Korean and Latin American general economic environments encourage vital, interactive overseas investment. First, Korean companies are highly export-oriented, which makes them to expand overseas market for further growth. While many Korean companies invest in China, they also tend to diversify overseas investment markets. Second, Latin America and the Caribbean countries tend to open their domestic markets to FDI and trade as well as to form exclusively preferential regional economic blocs within and together with North America after NAFTA. Korean 16 overseas investment in the ALADI countries receives a favorable response from the latter in terms of beneficial economic cooperation. In 2001, President Vicente Fox remarked at the summit meeting with President Kim Dae-Jung that “the recent expansion of trade and investment between Korea and Mexico is positive to economic growth of both countries, and Mexico wants further Korean support for improving Mexican information technology and education.” Third, statistics of Korean overseas investment show that Latin America and the Caribbean is not especially difficult place for Korean companies to do their businesses, although they are far away from each other and have a different cultural tradition. Fourth, Korean companies have high quality technologies and financial capacities enough to diversify their overseas investment in Latin America and the Caribbean. While the population of Latin America and the Caribbean is 1.5 times larger than that of North America, Korean overseas investment in the former is only a fifth of that in the latter. Korean overseas investment was concentrated in a few countries, Brazil and Mexico and a few manufacturing industries, such as in IT and clothing industries. Various guidelines have already been published for successful overseas investment in Latin America and the Caribbean. Instead of adding another checkpoints and going into details, I will make several remarks based on previously-mentioned statistics and investment stories. First, industrial park with favorable business environments can promote Korean companies to invest in Latin America. Industrial park, like Tijuana, can bring various component producers to be gathered so that any related firms can get easy, cheap supplies of parts. Industrial park can also increase intra-industry interdependence, which leads to broader, advanced economic cooperation. Foreign small and medium firms are as important members as large companies to industrial parks. A survey of foreign investors in Seoul shows that a third of them chose Seoul because of abundant components. Second, the localization of business operation as well as preparation should be conducive to an effective management. In case of Kobrasco, co-partner CVRD managed Kobrasco, which allowed POSCO to reduce its manpower. While Samsung Electronics owned 100% stocks of Samsung Electronics at Querétaro, its management is entrusted to other professional managerial firm. While joint venture was not a preferred investment type to Korean investors, it seems to be an effective alternative to total ownership. Third, business information about Latin America is out of sight, which discourages Korean businessmen to go there and instead to China. Latin America is still unfamiliar place to most Korean businessmen and women. To them, China is incomparably closer than Latin America is. Regular business forums in Seoul and Montevideo will be helpful for Korean businessmen and women to consider overseas investment in Latin America. For demonstration effect, ALADI companies, rarely seen in Korea, may establish some business subsidiaries in Korea. Fourth, while IT industry is the major Korean overseas investment in the ALADI now, other Korean competitive technologies, such as construction and food industries, may be alternatives. Korean construction industry has success stories in Middle East and Africa, which can be useful in Latin America. 17 Fifth, Latin American countries have been marching toward free-market economy, especially after the late 1980s, but many Korean investors are still suspicious of its further development. According to an economic freedom index, which rates countries' policies against free-market principles (for example, small government, low taxes, sound money, secure property rights and free trade), most of Latin American countries, except Chile, rank low in the world. Latin America Trade and Transportation Study points out several barriers for Latin American countries to attract foreign investors. One of them is incoherent economic and administrative policies. “Some Latin American countries are well known for frequent changes in economic and administrative regulations. This makes the economic climate very uncertain and risky from foreign investor’s point of view.” Another is domestic insecurity. Uncertain future regarding terrorism and homeland security in some Latin American countries can be a barrier. 18 Reference “Enhancing Economic Cooperation between Korea and Mexico in the Area of IT Industry,” Maeil Business Newspaper (Korean), June 5, 2001. Kim, Young-Suk, “Latin America and the Caribbean: Increase in M&A due to Expected Economic Recovery,” EXIM Overseas Economic Information (Korean), pp. 41-44 (March 2004) Lee, Young-Soo), “A Financial Analysis of Korean Overseas Corporations),” (EXIM Bank Overseas Economy), Dec. 2002: 19-36. Interview with POSCO’s managers of overseas investment, April 2004. Interviews with Samsung Electronics’ managers of overseas investment, April 2004. James Gwartney and Ian Vasquez, “Why Latin America Needs a Free-Trade Zone?,” National Post (Canada), April 18, 2001. Cato Institute, http://www.cato.org/dailys/04-21-01.html Korea Institute for International Economic Policy, Free Trade Area of the Americas: Current Issues and Implications (Korean), 2003. Lee. Se-Gu, The Inducement of Foreign Direct Investment in Seoul, (Research Institute for Seoul Municipal Administration, 1997). “Life after debt,” Economist, Apr. 1, 2004. Ministry of Foreign Affairs and Trade, A Comprehensive Survey of the Trade Environment (Korean), 2003. Overseas Economic Research Institute, Export-Import Bank of Korea, “What is the Problem of the Latin American Economy?,” EXIM Korean news, April 2002. -------------, “Mexico: Continuing Decline in Maquiladora Industries,” EXIM Korean news, March 2003. -------------, “Argentine Investment Environments,” 2003 -------------, “Mexican Investment Environments,” 2003 -------------, “Brazilian Investment Environments,” 2003 -------------, “Chilean Investment Environments,” 2003 -------------, “An Analysis of World FDI in the late 1990s,” 2004. POSCO, Building Steelworks for a quarter Century, 1992 19