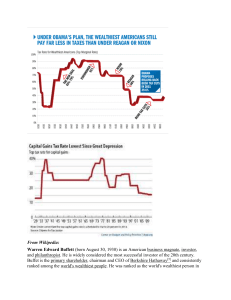

Notes from 2004 Annual Meeting

advertisement