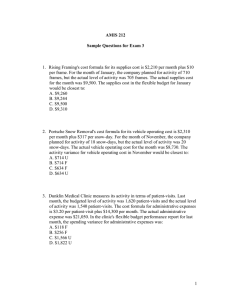

Chapter 8 Questions

Chapter 8 Problems

Use the following information to answer the first question: Cox Manufacturing Company prepared the following static budget income statement for 2004:

Sales Revenue

5000 units

$125,000

Variable Costs

Contribution Margin

Fixed Cost

Net Income

(75,000)

50,000

(30,000)

$ 20,000

The budget was based on an expected sales volume of 5,000 units. Actual production was 6,000 units.

1. The amount of net income based on a flexible budget of 6,000 units would have been a. $24,000. b. $26,000. c. $30,000. d. $45,000.

$50,000 / 5,000 = $10 CM per unit

$10 * 6,000 = $60,000 CM

$60,000 – 30,000 = $30,000

2. Marjorie Jewels, a maker of fashionable rings, produced and sold 6,000 rings during the recent accounting period. The company had expected to sell 5,600 rings. Because of competition, the company priced the rings at $20 each, $2 lower than the budgeted selling price. Based on this information, there is

Sales Price Variance = $22 – 20 = $2 * 6,000 = $12,000 U

Sales Volume Variance = 6,000 – 5,600 = 400 * $22 = $8,800 F

Total Sales Variance = $3,200 U a. a favorable $8,000 sales volume variance. b. an unfavorable $800 total sales variance. c. an unfavorable sales price variance. d. all of the above.

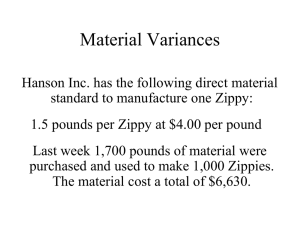

3. Macabees Company budgeted manufacturing materials costs at $12 a unit. Actual materials costs were

$14 a unit. The company had planned to produce 20,000 units but actually produced 23,000 units.

What is the total materials cost variance for Macabees?

$14 - $12 = $2 * 23,000 = $46,000 U a. $46,000 unfavorable b. $82,000 favorable c. $46,000 favorable d. $82,000 unfavorable

4. Starmax Company pays workers producing the product Lotrim an average standard wage of $9 per hour. The standard amount of time required to produce a case of Lotrim is 2 hours. In January,

Starmax produced 18,000 cases of Lotrim at a total actual labor cost of $323,000. During January,

Starmax actually used 34,000 labor hours. Based on this information the labor usage variance is

SQ = 18,000 * 2 = 36,000 hours

36,000 – 34,000 = 2,000 * $9 = $18,000 F a. $18,000 unfavorable. b. $18,000 favorable. c. $34,000 favorable. d. $34,000 unfavorable.

Use the following information to answer the next two questions: Bright Smile, Inc. (BSI) makes a bleach that is used to whiten teeth. BSI expects to use 2 ounces of exeron per bottle of whitener. Exeron is expected to cost $0.20 per ounce. Actual materials cost amounted to $0.23 per ounce. BSI expected to make and sell 1,000,000 bottles of whitener during the accounting period. BSI actually used 2,047,500

ounces to produce 1,050,000 bottles.

5. The materials price variance for exeron is

$0.23 - $0.20 = $0.03 * 2,047,500 = $61,425 U a. $61,425 unfavorable. b. $61,425 favorable. c. $20,000 favorable. d. $20,000 unfavorable.

6. The materials usage variance for exeron is

SQ = 2 * 1,050,000 = 2,100,000

2,100,000 – 2,047,500 = 52,500 * 0.20 = $10,500 a. $3,000 unfavorable. b. $3,000 favorable. c. $10,500 favorable. d. $10,500 unfavorable.

Cole Manufacturing Company expects its variable cost per unit to be $25. Fixed costs are expected to be

$69,000. Cole plans to make and sell 5,000 units of product. The expected sales price is $45 per unit. The company actual made and sold 4,800 units and sold them for $47 per unit.

7.

What is the sales price variance?

$47 - $45 = $2 * 4,800 = $9,600 F

8.

What is the sales volume variance?

5,000 – 4,800 = 200 * $45 = $9,000 U

9.

What is the total sales variance?

$600 F

Use the following information to answer questions 10 - 12.

Max Company has developed the following standards for one of its products:

Direct materials

Direct labor

15 pounds x $16 per pound

4 hours x $24 per hour

Variable overhead 4 hours x $14 per hour

The following activities occurred during the month of October:

Materials used

Units produced

Direct labor

7,200 pounds at a price of $16.25 per pound

500 units

2,300 hours at $23.60 per hour

10.

Max's labor rate variance would be

$24 - $23.60 = $0.40 * 2300 = $920 F

11.

Max’s labor efficiency variance would be

SQ = 4 * 500 = 2,000 hours

2,300 – 2,000 = 300 * $24 = $7,200 U

12.

Max’s total materials variance would be

Static = SP * SQ

$16 * (15 * 500) = $120,000

Actual = AP * AQ

$16.25 * 7200 = $117,000

Variance = $3,000 F