Analisi del bilancio: Analisi dei rapporti

advertisement

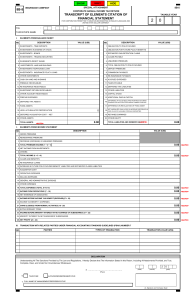

MODUL PERKULIAHAN ANALISA LAPORAN KEUANGAN Analisa Rasio 1.Rasio likuiditas 2.Rasio solvabilitas 3.Rasio aktivitas 4.Ratio profitabilitas Fakultas Program Studi Ekonomi Dan Bisnis Manajemen Tatap Muka 04 Kode MK Disusun Oleh 84031 Hotma Timbul Gultom SE,Ak,M.Si Abstract Kompetensi Petunjuk Penggunaan Template Modul Standar untuk digunakan dalam modul perkuliahan Universitas Mercu Buana Dosen Pengampu dapat menerapkan dan menggunakan template modul standar untuk modul-modul yang akan dipergunakannya Ratio analysis expresses the relationship among selected items of financial statements data. A ratio expresses the mathematical relationship between one quantity and another. The relationship is expressed in terms of either a percentage, a rate, or a simple proportion Ratio analysis, termasuk : Du Pont system – Modul 5 Cross section analysis: industri averages dan intercompany comparisons (lawan dari intracompany comparisons) – Modul 6 Subramanyam dkk mengelompokkan rasio ke dalam 6 (enam) kategori, yaitu : 1. Liquidity ratio. - Current ratio - Acid-test ratio - Collection period - Days to sell inventory 2. Capital Structure and Solvency ratio - Total debt to equity - Long-term debt to equity - Times interest earned 3. Return on Investement - Return on assets - Return on common equity 4. Operating Performance - Gross profit margin - Operating profit margin - Pretax profit margin - Net profit margin 5. ‘13 2 Asset Utilization - Cash turnover - AR turnover - Inventory turnover - Working capital turnover - PPE turnover - Total assets turnover Analisa Laporan Keuangan Hotma Timbul Gultom SE,Ak,M.Si Pusat Bahan Ajar dan eLearning http://www.mercubuana.ac.id 6. Market Measures - PE ratio - Earnings yield - Dividend yield - Dividend payout ratio - Price to book value Penulis lain mengelompokkan rasio kedalam kategori sebagai berikut : 1. Rasio likuiditas : rasio yang mengukur kemampuan perusahaan memenuhi kewajiban jangka pendeknya. a. rasio lancar = b. rasio quick aktiva lancar / hutang lancar = (aktiva lancar – persediaan) / hutang lancar 2. Rasio aktivitas : rasio yang mengukur sejauh mana efektivitas penggunaan asset dengan melihat tingkat aktivitas asset. a. Rata-rata umur piutang (hari) : perputaran piutang = penjualan / piutang rata-rata umur piutang = 365 / perputaran piutang b. perputaran persediaan. perputaran persediaan = harga pokok penjualan / persediaan rata-rata umur persediaan = 365 / perputaran persediaan c. perputaran aktiva tetap = penjualan / aktiva tetap d. perputaran total aktiva = penjualan / total aktiva 3. Rasio solvabilitas : rasio yang mengukur sejauh mana kemampuan perusahaan memenuhi kewajiban jangka panjangnya. a. rasio total hutang ke total asset = total hutang / total asset. b. times interest earned = EBIT / bunga c. fixed charged coverage = (EBIT + biaya sewa) / (bunga + biaya sewa). 4. Rasio profitabilitas : rasio yang melihat kemampuan perusahaan menghasilkan laba (profitabilitas). a. profit margin (%) = laba bersih / penjualan. b. ROA (%) = laba bersih / total asset c. ROE (%) = laba bersih / modal saham 5. Rasio pasar : rasio ini melihat perkembangan nilai perusahaan relatif terhadap nilai buku perusahaan. ‘13 3 a. PER = harga pasar per lembar / laba bersih per lembar b. dividend yield (%) = dividen per lembar / harga pasar per lembar c. dividend payout (%) = dividen per lembar / laba bersih per lembar Analisa Laporan Keuangan Hotma Timbul Gultom SE,Ak,M.Si Pusat Bahan Ajar dan eLearning http://www.mercubuana.ac.id (Mamduh M Hanafi & Abdul Halim, hal 76) 6. Rasio pertumbuhan : rasio ini menggambarkan persentase pertumbuhan pospos perusahaan dari tahun ke tahun a. kenaikan penjualan = (penjualan tahun ini – penjualan tahun lalu) / penjualan tahun lalu b. kenaikan laba bersih = (laba bersih tahun ini – laba bersih tahun lalu) / laba bersih tahun lalu c. EPS = (EPS tahun ini – EPS tahun lalu) / EPS tahun lalu d. kenaikan dividen per share = (dividen per share tahun ini – dividen per share tahun lalu) / dividen per share tahun lalu (Sofyan Syafri Harahap, hal. 309 - 310) - Bandingkan dengan “Summary of Key Financial Statement Analysis and Valuation Measures” pada hal terakhir - Penulis buku yang berbeda mempunyai jenis rasio yang berbeda : lihat lampiran 1 Pelajari SKA (siklus konversi asset) : lihat Exhibit 4-1, hal. 197 Keterbatasan analisa rasio Financial ratio analysis does have some limitations : 1. Comparing an organization that is in a single line of business with an organization that is a competitor but has a multiple lines of business is likely to be a meaningless comparison of unlike organizations 2. Even though organizations might be comparable because they are in similar lines of business, they may use different accounting conventions, making ratio comparisons between the two organizations meaningless 3. Interpreting trends in a single organizaton’s financial ratios may be difficult because of the effect of unknown economic or competitive forces on the organization. 4. It may be difficult to determine the appropriate or acceptable value for a particular ratio, particularly if the industry is in a recession. 5. When there are strong seasonality effects, making comparisons with financial data that are a snapshot of the organization’s financial activities at year end may be meaningless 6. When organizations manipulate or misrepresent their financial information, the financial ratios drawn from these data will be misleading ‘13 4 Analisa Laporan Keuangan Hotma Timbul Gultom SE,Ak,M.Si Pusat Bahan Ajar dan eLearning http://www.mercubuana.ac.id 7. Like all numbers based on historical results, financial ratios look backward. It may be difficult or even meaningless to project past data to predict future performance 8. Because they are backward looking, financial ratios ignore an organization’s current strategic initiatives and may misrepresent future results of current initiatives (Management Accounting – Anthony A. Atkinson, Robert S. Kaplan, Ella Mae Matsumura, S. Mark Young) Benchmarking Penganalisaan laporan keuangan melalui analisa rasio ini dapat dilakukan dengan 4 (empat) macam cara perbandingan, yaitu : 1. membandingkan rasio sekarang dengan rasio dari waktu yang lalu (intracompany comparison), 2. membandingkan rasio perusahaan dengan rasio sejenis dari perusahaan lain yang sejenis untuk waktu yang sama (intercompany comparison), 3. membandingkan rasio perusahaan dengan rasio sejenis dari industry (industry comparison) 4. membandingkan rasio perusahaan terhadap suatu “benchmark” tertentu (predetermined standard) Kendala dalam melakukan pembandingan ini adalah : 1. Sulit memperoleh data perusahaan lain yang sejenis maupun data industri yang dapat digunakan sebagai pembanding 2. Penggunaan data perusahaan lain yang sejenis maupun data industri sebagai pembanding dapat mengakibatkan kekeliruan dalam penafsiran, karena adanya a. Perbedaan lini produk maupun kekhususan produk b. Perbedaan dalam penerapan metoda akuntansi 3. Rasio-rasio periode yang lalu bukan merupakan alat yang baik untuk meramalkan keadaan di masa yang akan datang Contoh soal Berdasarkan data dari neraca dan laporan laba-rugi PT.ABC di bawah ini, dan pemahaman akan berbagai alat analisa laporan keuangan yang telah saudara / i pelajari, buat analisa rasio laporan keuangan PT. ABC tersebut. ‘13 5 Analisa Laporan Keuangan Hotma Timbul Gultom SE,Ak,M.Si Pusat Bahan Ajar dan eLearning http://www.mercubuana.ac.id ‘13 6 Analisa Laporan Keuangan Hotma Timbul Gultom SE,Ak,M.Si Pusat Bahan Ajar dan eLearning http://www.mercubuana.ac.id ‘13 7 Analisa Laporan Keuangan Hotma Timbul Gultom SE,Ak,M.Si Pusat Bahan Ajar dan eLearning http://www.mercubuana.ac.id Lampiran 1a: summary of analytical measures (Financial & Managerial accounting – The Basis of Business Decisions: Williams – Haka – Bettner – Carcello) SUMMARY OF ANALYTICAL MEASURES I. ratios or other measurements measures of short term Iliquidity 1. current ratio method of computation 3. working capital current assets current liabilities quick Assets current liabilities current assets – current liabilities 4. net cash provided by operating activities appears in the statement of cash flows 5. cash flow from operations to current liabilities 6. receivables turnover rate 7. days to collect average accounts receivable 8. inventory turnover rate 9. days to sell the average inventory 10. operating cycle cash flows from operating activities current liabilities 2. quick ratio 11. free cash flow net sales average accounts receivable 365 days receivables turnover rate cost of goods sold average inventory 365 days inventory turnover rate days to sell inventory + days to collect receivables net cash from operating activities – cash used for investing activities and dividends II. measures of long-term credit risk 12. debt ratio 13. trend in net cash provided by operating activities 14. interest coverage ratio ‘13 8 total liabilities total assets appears in comparative statements of cash flows income before interest and taxes annual interest expense Analisa Laporan Keuangan Hotma Timbul Gultom SE,Ak,M.Si Pusat Bahan Ajar dan eLearning http://www.mercubuana.ac.id significance a measure of short-term debt paying ability a measure of short-debt paying ability a measure of short-term debt paying ability indicates the cash generated by operations after allowing for cash payment of expenses and operating liabilities indicates ability to cover currently maturing obligations from recurring operations indicates how quickly receivables are collected indicates in days how quickly receivables are collected indicates in days how quickly inventory sells indicates in days how quickly inventory sells Indicates in days how quickly cash invested in inventory converts back into cash excess of operating cash flow over basic needs percentage of assets financed by creditors; indicates relative size of the equity position indicator of a company’s ability to generate the cash necessary to meet its obligations indicator of a company’s ability to meet its interest payment obligations III. measures of profitability 15. percentage chase that is in net sales and net income 16. gross profit rate 17. operating expense ratio 18. operating Income 19. net Income as a percentage of net sales 20. earnings per share 21. return on assets 22. return on equity 23. return on common stockholder’s equity IV. measures for evaluating the current market price of common stock 24. market value of financial instruments 25. price earnings ratio dollar amount of change financial statement amount in the earlier year gross profit net sales operating expenses net sales gross profit – operating expenses net income Net Sales net Income – preferred dividends average number of common shares outstanding operating Income average total assets net income average total equity net Income – preferred dividends average common stockholder’s equity quoted in financial press or disclosed in financial statement current stock price earnings per share 26. dividend yield annual dividend current stock price 27. book value per share common stockholders’ equity shares of common stock outstanding the rate at which a key measure is increasing ore decreasing ; the “gsowth rate” a measure of the profitability of the company’s products a measure of management’s ability to control expenses the profitability of a company’s basic business activities an indicator of management’s ability to control costs net income applicable to each share of common stock a measure of the productivity of assets, regardless of how the assets are financed the rate of return earned on the stockholders’ equity in the business the rate of return earned on the common stockholders’ equity appropriate when company has both common and preferred stock reflects both investors’ expectations and current market conditions a measure of investors’ expectations about the company’s future prospects dividends expressed as a rate of return on the market price of the stock the recorded value of net assets underlying each share of common stock Lampian 1b : a summary of financial ratios (Intermediate Accounting – Ninth Edition) Kieso & Weygand ratio ‘13 9 Analisa Laporan Keuangan Hotma Timbul Gultom SE,Ak,M.Si formula Pusat Bahan Ajar dan eLearning http://www.mercubuana.ac.id purpose or use I. liquidity 1. current ratio 2. quick or acid test ratio 3. current cash debt coverage ratio II. activity 4. receivables turnover 5. inventory turnover 6. asset turnover III. profitability 7. profit margin on sales 8. rates of return on assets 9. rate of return on common stock 10. earnings per share 11. price earnings ratio IV. coverage 13. debt to total assets 14. times interest earned 15. cash debt coverage ratio 16. book value per share 10 measures shot term debt paying ability measures immediate short term liquidity measures a company’s ability to pay off its current liabilities in a given year from its operations net sales average trade receivables (net) cost of goods sold average inventory net sales average total assets measures liquidity of receivables net income net sales net income average total assets net income minus preferred dividends average common stockholders’ equity net income minus preferred dividends weighted shares outstanding market price of stock earnings per share 12. payout ratio ‘13 current assets current liabilities cash marketable securities, current liabilities net cash provide by operating activities average current liabilities Analisa Laporan Keuangan Hotma Timbul Gultom SE,Ak,M.Si cash dividends net income total debt total assets income before interest expense and taxes interest expense net cash provided by operating activites average total liabilities common stockholders’ equity outstanding shares Pusat Bahan Ajar dan eLearning http://www.mercubuana.ac.id measures liquidity of Inventory measures how efficiently assets are used to generate sales measures net income generated by each dollar of sales measures overall profitability of assets measures profitability of owners’ investment measures nit income earned on each share of common stock measures the ratio of the market price per share to earnings per share measures percentage of earnings distributed in the form of cash dividends measures the percentage of total assets provided by creditors measures ability to meet interest payments as they measures a company’s ability to repay its total liabilities in a given year from its operations measure the amount each share would receive if the company were liquidated at the amounts reported on the balance sheet Lampiran 2 MENGANALISA SKA SKA adalah kependekan dari siklus konversi asset atau assets conversion cycle SKA meliputi proses konversi menyeluruh mulai dari kas atau bahan baku ke barang jadi, ke piutang dan ke kas lagi. Menganalisa SKA dari suatu perusahaan penting karena : 1. perusahaan hanya mampu memenuhi kepentingan stakeholders-nya apabila mampu menyelesaikan SKA-nya dengan baik 2. dengan memahami SKA-nya, kita akan dapat mengetahui potensi kemacetan dalam rangkaian proses konversi itu Lihat Exhibit 4-1, hal. 197 1. Bahan baku dikirim dibeli tunai dibeli secara kredit dari pemasok, menimbulkan hutang dagang pinjam uang untuk membeli bahan baku 2. Nilai tambah (value added) bahan baku memasuki proses produksi dan di konversi menjadi barang jadi nilai ditambah oleh perkerja yang harus dibayar jasanya ada juga nilai tambah dalam bentuk biaya pemeliharaan pabrik, biaya penggunaan utilities, biaya non-kas seperti penyusutan 3. Barang jadi tersedia untuk dijual hampir semua perusahaan memiliki “iron stock” untuk mencegah risiko interupsi bisnis dan untuk memenuhi peningkatan dalam permintaan, dll biaya memiliki “iron stock” terdiri dari biaya gudang dan “carrying cost” lainnya 4. Barang jadi dijual hampir semua perusahaan menjual secara kredit dan karenanya menimbulkan piutang dagang menjual barang jadi menambah biaya, seperti biaya pemasaran dalam bentuk gaji, iklan, distribusi, dan lain-lain 5. Piutang dagang dilunasi : pelunasan dari piutang dagang mengakhiri SKA perusahaan hanya melalui pelunasan piutang dagang ini perusahaan mampu memenuhi kepentingan stakeholders-nya Faktor Waktu dalam SKA 1. SKA dengan timing yang sempurna : contoh : beli bahan baku dengan kredit 30 hari - bahan baku ke barang jadi : 10 hari - jual barang jadi 5 hari - tagih piutang dagang 15 hari Jumlah 30 hari menghasilkan kas tepat waktu pada waktu hutang dagang dan accrued expenses jatuh waktu 2. SKA dengan timing yang tidak sempurna SKA = 60 hari sedangkan hutang dagang 30 hari Ini berarti perusahaan punya hutang yang jatuh tempo sebelum kas dari tagihan masuk perbedaan timing ini harus diusahakan pembiayaannya 3. Perusahan mempunyai SKA yang berbeda-beda ‘13 11 Analisa Laporan Keuangan Hotma Timbul Gultom SE,Ak,M.Si Pusat Bahan Ajar dan eLearning http://www.mercubuana.ac.id ‘13 Untuk perusahaan yang SKA-nya pendek, perhatikan expertise manajemen, fluktuasi harga produk, reliability dari pelanggan dan pemasok, risiko transportasi, kemungkinan rusaknya produk, dll Untuk perusahaan yang SKA-nya panjang, perhatikan kemungkinan buruh mogok, umur pabrik, permintaan terhadap produk, dll Bagaimana menganalisa SKA Pelajari faktor apa saja yang mempengaruhi proses konversi bahan baku, barang dalam proses, barang jadi, dan piutang dagang sehingga membuat perusahaan tidak sanggup menyelesaikan SKA-nya ! 12 Analisa Laporan Keuangan Hotma Timbul Gultom SE,Ak,M.Si Pusat Bahan Ajar dan eLearning http://www.mercubuana.ac.id