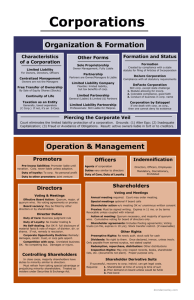

Sole Proprietorship

advertisement