Part 2-I

advertisement

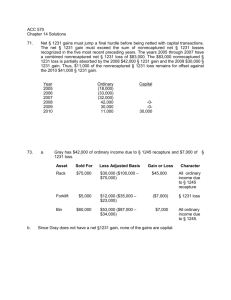

EA Exam Lite Part 2 Businesses - I Previous Exam Questions 1. Betsy is a dairy cow raised on Ronald’s Dairy Farm. On December 26, Ronald sold Betsy for $3,800. He incurred $300 in transportation expenses that were included in the sales price. Ronald estimates that Betsy cost $2,000 for food and other expenses to raise her. He deducted these expenses. What is Ronald’s gain from the sale of Betsy? a. b. c. d. 2. In August 2006, Mr. Greenjeans, a cash basis, calendar year farmer, had his crop destroyed by a drought. On September 1, 2006, he received $30,000 from the federal government under the Disaster Assistance Act of 2006. Mr. Greenjeans would have normally received income from this crop on or about October 1, 2007. How should Mr. Greenjeans treat the $30,000 for federal income tax purposes? a. b. c. d. 3. The $30,000 is nontaxable income. The $30,000 may be included in income in 2007 if the election to do so was made in 2006. The $30,000 must be included in income in 2006. Include $10,000 in income in 2006 and $20,000 in 2007. Farmer Gray is a calendar year cash basis taxpayer. She normally sells 200 head of livestock a year. Because of floods, she sold 250 head of livestock during 2007. Farmer Gray realized $50,000 from the sale. The Department of Agriculture declared the flooded area a disaster area eligible for federal assistance. What is the amount of income that Farmer Gray can elect to postpone until 2008? a. b. c. d. 4. $1,500 $1,800 $3,500 $3,800 $12,500 $50,000 $10,000 $0, since only sales as a result of drought qualify. Ms. Dee owns and operates a dance studio. On December 1, 2006, she received an advance payment of $2,400 from Angie to give her 12 dance lessons. The agreement stated that one lesson would be given in 2006 and 11 lessons in 2007. However, due to Angie’s health, one lesson scheduled for June, 2007, was NOT given until January, 2008. Ms. Dee uses the calendar year and the accrual method of accounting for both tax and financial accounting purposes. Assuming Dee elects to defer the advance payments, when must she include the payment received from Angie in income? a. b. c. d. $2,400 in 2006 $200 in 2006 and $2,200 in 2007 $200 in 2006, $2,000 in 2007 and $200 in 2008 $2,400 in 2008 5 During 2007, Nancy, a calendar year taxpayer, acquired and placed in service the following business assets: January: Delivery trucks…….….. $50,000 March: Warehouse building…… $150,000 June: Computer system………….$ 30,000 September: Automobile………… $30,000 November: Office equipment… $90,000 Which convention(s) can Nancy use to figure depreciation for 2007? a. b. Mid-quarter for all assets except the warehouse building which uses the mid-month. Half-year for all of the assets. c. d. Mid-quarter for all of the assets. Half-year for all assets except the warehouse building which uses mid-month. 6. In 2007, Mary Jane placed in service a machine that cost $539,000. If she placed no other Section 179 property in service during the year, how much is her Section 179 maximum dollar limit? a. b. c. d. $ 7,000 $125,000 $-0$86,000 7. All of the following statements about ADS (alternative depreciation systems) are correct except: a. b. c. d. The election must be made by the due date, INCLUDING extensions, for the tax return of the year in which the property was placed in service. The election to use ADS can be revoked. Excluding nonresidential real and residential rental property, the election of ADS for a recovery class of property applies to all property in that recovery class that is placed in service during the tax year of the election. ADS is figured using straight-line method. 8. On January 1, 2007, Sally Jefferson purchased an auto for $18,000. Her business use was 60% during 2007. She is electing $1,000 section 179 deduction on the auto. What is her total deduction for calendar tax year 2007? a. b. c. d. $3,600 $3,060 $1,836 $6,366 9. With regard to the correct treatment of business bad debts, all of the following statements are correct, except: a. b. c. d. Tom deducted a bad debt in a prior tax year and later recovered part of it. He may have to include the amount recovered in gross income in the year of recovery. Bill can deduct his business bad debt as a short-term capital loss. Sally received property in a partial settlement of a debt. She should reduce the debt by the fair market value of the property received and deduct the remaining amount as a bad debt. Jane can deduct the difference between the amount owed by a bankrupt entity and the amount received from the distribution of its assets as a bad debt. 10. In 2006, the Rox Company had gross income of $185,000, a bad debt deduction of $7,000, and other allowable deductions of $181,000. Rox carried back the 2006 NOL of $3,000 to 2004 and it was used in full to lower Rox’s tax for 2004. In 2007, Rox recovered $5,000 of the bad debt deducted in 2006. What is the amount of the bad debt recovery that Rox should include in income for 2007? a. b. c. d. $-0$1,000 $4,000 $5,000 11. Charlie Croker exchanged real estate held for investment that had an adjusted basis of $8,000 for other real estate that he will hold for investment. The property given up was subject to a $3,000 mortgage. The real estate he received had a fair market value of $10,000. Charlie also received $1,000 in cash from which he paid $500 in exchange expenses. He realized a gain on the exchange. How much of the gain is taxable? a. b. c. d. $5,550 $6,000 $4,000 $3,500 12. Lou and Casey are independent, unrelated taxi drivers who decided to swap cabs. The relevant facts are as follows: Original Owner Lou Original Cost $12,000 Fair market value $ 3,000 Depreciation claimed $10,000 Casey $15,000 $ 5,000 $12,250 Lou had to pay $2,000 cash and his old cab in order to acquire Casey’s cab. What are Lou and Casey’s adjusted basis in their new cabs? a. b. c. d. Lou $4,000 $4,000 $4,750 $4,750 Casey $3,000 $2,750 $3,000 $2,750 13. A used car lot owner sold an adjacent lot on June 9, 2007, for $125,000. He purchased this lot on August 6, 2004, for $65,000, and used it in his dealership. He did not pave this lot or make any improvements to it. He paid $4,600 in closing costs at the sale. How much gain does he have, and what type of gain is it? a. b. c. d. $55,400 Section 1250 gain $55,400 Section 1231 gain $4,600 Section 1245 gain $50,800 Section 1231 gain $55,400 Schedule D gain 14. Mr. X acquired a machine for use in his business, on January 2006 for $30,000. Depreciation was taken on the asset in the following amounts: 2006…………………………$6,000 2007…………..…………… $4,800 Mr. X sold the machine on January 26, 2008, for $32,000. What is the amount and character of X’s gain on the disposition of the asset, assuming this was the only business asset sold during the year? a. b. c. d. $-0- capital gain; $12,800 ordinary gain $2,000 capital gain; $10,800 ordinary gain $10,800 capital gain; $2,800 ordinary gain $12,800 capital gain; $-0- ordinary gain 15. On December 31, 2007, John sold an apartment building for $225,000. He had purchased the building and placed it in service July 31, 1985, for $200,000. The depreciation deducted as of December 31, 2006 was $75,000 of which $25,000 was excess of depreciation adjustments over depreciation using the straight-line method. In 2007, the depreciation deducted was $7,000 of which $2,000 was excess depreciation. What amount may John treat as a Section 1231 gain? a. b. c. $107,000 $ 80,000 $ 27,000 d. $ 25,000 16. Which of the following dispositions of depreciable property would trigger recapture? a. b. c. d. Installment sale. Gift. Transfer at death. Tax-free exchange where no money or unlike property is received. 17. All of the following are subject to self-employment tax except: a. b. c. d. S Corporation shareholder’s share of the corporation’s taxable income. Gain from a casualty or theft loss of inventory. Rental income and related deductions received by a real estate dealer. Income received by a self-employed plumber for repairing a faucet. 18. Sarah owns and operates a retail sporting goods business as a sole proprietor. Her store is located on the ground floor of a 2-story building that she owns. Based on the following information, compute her net self-employment income (for SE tax purposes) for that year. Gross profit from sporting good store…………………………… $100,000 Rental income from upper level (45%) of building……………… $20,000 Building depreciation expense……………………………………. $10,000 Utilities for ground floor (tenant pays own utilities)……………. $4,500 Depreciation on vehicles used in business……………………… . $3,000 Gain on sale of van used 100% in business……………………….. $2,000 Contributions to her Keogh retirement plan…………………… $5,550 Sarah’s Health insurance premiums………………………… . $4,500 Mortgage interest on building…………………………………… $10,000 Other expenses of running her sporting goods business………… $11,500 a. b. c. d. $64,700 $68,200 $70,000 $83,000 19. Cal and Diane, a married couple, had the following income in 2007: Taxable interest and dividend income………………………… $43,500 Rental income (Schedule E)……………………………………. $1,500 Farm income (Schedule F)……………………………………… $75,000 Farm rental income (Form 4835)………………………………. $15,000 Schedule D income (sale of dairy cows)………………………… $5,000 Total gross income ……………….. …………. $140,000 Which of the following statements BEST describes their ESTIMATED tax responsibilities? a. b. c. d. They MUST file and pay estimated taxes in quarterly installments in April, June, September, and January. They can wait until January 15, 2008, to make their first and only estimated tax payment. They MUST file their return by January 31, 2008, and pay all the tax that is due in order to avoid an estimated tax penalty. Their adjusted gross income will be too high to take advantage of ANY special estimated tax filing breaks. 20. During the current year, Scott contributed property having an adjusted basis to him of $10,000, to LMN Partnership for a 45% interest in the partnership. At the time of the contribution, the property had a fair market value of $20,000. What is the amount and character of Scott’s gain on this transaction to be reported on his current-year tax return? a. b. c. d. $-0$4,500 long term capital gain $10,000 ordinary income $10,000 long term capital gain 21. Earl acquired a 20% interest in a partnership by contributing property that had an adjusted basis to him of $8,000 and that was subject to a mortgage of $12,000. Which of the following results is correct? Capital Gain Recognized a. $1,600 b. $-0c. $4,000 d. $1,600 Basis of Partnership Interest $1,600 ($1,600) $8,000 $-0- 22. In return for a 20% partnership interest, Kathy contributed land having a $60,000 fair market value and a $30,000 basis to the partnership. The partnership assumes Kathy’s $15,000 liability arising from her purchase of the land. The partnership’s liabilities arising from its purchases of assets is $4,000 immediately prior to the contribution. What is Kathy’s basis in her partnership’s interest? a. b. c. d. $18,800 $30,000 $15,000 $15,800 23. Bob acquired a 50% interest in a partnership by contributing depreciable property that had an adjusted basis of $15,000 and a fair market value of $45,000. The property was subject to a liability of $32,000, which the partnership assumed for legitimate business purposes. What is the partnership’s basis in the property for depreciation? a. b. c. d. $-0$14,000 $15,000 $16,000 24. With respect to partnerships, which of the following items is NEVER considered a separately stated item and must be included in the net income from the partnership’s nonrental trade or business activities. a. b. c. d. Dividends Charitable contributions Gains or losses from sales or exchanges of capital assets Depreciation expense 25. For the year ended December 31, the partnership of Gil and Bill had book income of $37,000 which included the following: Dividend income………………………………… $1,000 Short-term capital loss………. …………………. ($4,000) Section 1231 gain………………………………… $7,000 Ordinary income (sec. 1245 recapture)………… $1,500 Interest income……………………………………. $750 The partners share profits and losses equally. What amount of partnership income (excluding all partnership items which must be reported separately) should each partner report on his individual income tax return for the year? a. b. c. d. $19,625 $18,500 $16,125 $7,313 26. Under a partnership agreement, Sybil is to receive 40% of the partnership’s income, but not less than $15,000. The partnership’s net income was $30,000 before considering the minimum guarantee amount. What amount can the partnership deduct as a guaranteed payment, and what amount of income is Sybil required to report on her individual tax return? a. b. c. d. Partnership $3,000 $15,000 $3,000 $15,000 Sybil $15,000 $15,000 $27,000 $27,000 27. Under the terms of ABC’s partnership agreement, Eric received, as a guaranteed payment, 12 monthly payments of $1,000 from 2/1/06 to 1/31/07 from ABC partnership. His distributive share of the partnership income is 10%. The ABC partnership has $60,000 of ordinary income after deducting the guaranteed payment. How much must Eric include on his individual tax return for 2007 if Eric is a calendar-year taxpayer and the partnership year ends 1/31/07? a. b. c. d. $1,000 guaranteed payment & $6,000 ordinary income $1,000 guaranteed payment & $500 ordinary income $12,000 guaranteed payment & $500 ordinary income $12,000 guaranteed payment & 6,000 ordinary income 28. The adjusted basis of Paul’s partnership interest is $10,000. He receives a distribution of $4,000 cash and property that has an adjusted basis to the partnership of $8,000. (This was not a distribution in liquidation.) What is the basis of the distributed property in Paul’s hands? a. b. c. d. $8,000 $6,000 14,000 $2,000 29. On April 10, 2005, Reuben contributed land in exchange for a 25% partnership interest in Larson Partners. The fair market value of the land at the time was $60,000 and Reuben’s adjusted basis was $25,000. On November 1, 2007, Larson distributed that land to another partner. The fair market value at that time was $65,000. What is the amount of Reuben’s recognized gain from the transfer of the land by Larson to another partner? a. b. c. d. $5,000 $10,000 $35,000 $40,000 30. Which of the following statements about the liquidation of a partner’s interest is INCORRECT? a. b. c. d. A retiring partner is treated as a partner until his or her interest in the partnership has been completely liquidated. The remaining partner’s distributive shares of partnership income are reduced by payments in exchange for a retiring partner’s interest in partnership property. The retiring partner will recognize a gain on a liquidating distribution to the extent that any money distributed is MORE than the partner’s adjusted basis in the partnership. Payments in liquidation of an interest that are NOT made in exchange for the interest in partnership property are reported as ordinary income by the recipient. 31. A is a partner in partnership PRS and has an adjusted basis in its partnership interest of $6,500. In a complete liquidation of A’s interest. A received the following: Cash Inventory Items Asset X Asset Y PRS’s Basis $-0$1,000 $500 $1,000 Fair Mkt Value $-0$2,000 $4,000 $1,000 What is A’s basis in Assets X & Y? a. b. c. d. Asset X $500 $1,500 $3,500 $4,400 Asset Y $1,000 $3,000 $1,000 $1,100 32. The adjusted basis of Dan’s interest in D & P Enterprise at the end of the year, after allocation of his share of partnership income, was $35,000. This included his $19,000 share of partnership liabilities. The partnership had not unrealized receivables or substantially appreciated inventory items. On December 31, Dan sold his interest in D & P Enterprise to Joanne for $16,000. It was agreed that she would assume Dan’s share of partnership liabilities. What is the amount of Dan’s capital gain (loss)? a. b. c. d. $1,000 $16,000 $-0($19,000) 33. Susan has a 25% interest in the Boggs Partnership. The adjusted basis for her interest at the end of the current year is $40,000. She sells her interest in Boggs Partnership to Brian for $53,000 cash. The basis and fair market value of the partnership’s assets (there are no liabilities) are listed below. There was no agreement between Susan and Brian for any allocation of the sales price. Assets Cash Unrealized receivables Inventory Fixed assets Total assets Basis Fair Market Value $60,000 $60,000 $ -0$32,000 $40,000 $80,000 $60,000 $40,000 $160,000 $212,000 What is the amount and character of Susan’s gain or loss? a. b. c. d. $18,000 ordinary income; $-0- capital gain $-0- ordinary income; $13,000 capital gain $18,000 ordinary income; $5,000 capital loss $6,500 ordinary income; $6,500 capital gain Part 2-I Answers and Explanations to Questions Question Answer 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 c b c b a d b c b d d b b b b a a c b a d a d d c a d b c b d c c Explanation The cost of raising cattle has already been deducted The postponement is allowed if crop income otherwise would occur then ($50,000 / 250 = $200 SP per cow); $200 x 50 excess = $10,000 deferred If all services are not completed by 2007, no further deferral is available More than 40% of personalty (90/200) was placed in service in last qtr The $125,000 maximum is reduced by the $39,000 excess over $500,000 An ADS election may not be revoked Maximum deduction (MACRS & Sec. 179) is $ 3,060 limit x .60 usage Business bad debts are reported as deductions against ordinary income Full amount is includable, since the NOL was used completely in 2004 Gain is limited to boot received; expenses may offset boot first Lou(2,000basis+2,000 boot given);Casey (2,750basis+2,000bt-2,000bt) Assumes property used in trade or business Total depr. taken is ordinary, balance is capital (since only 1231 trans.) Total gain is $107,000 ($225,000 - $118,000); $27,000 excess is ord. inc. All recapture is recognized in the year of sale for an installment sale An S shareholder is and investor and not considered to be self-employed Ignore rents, gain, Keogh, ins. prem.; deduct 55% of depr and mortgage At least 2/3’s of income is from farming, they need only make one pay. Since no boot or services are involved, no gain is reportable by partner Gain = $9,600 liabilities assumed by other partners - $8,000 adj basis Basis = $30,000 adj. basis – ($15,000 x .80) mortg. + ($4,000 x .20) liab. P’ship = $15,000 adj. basis + $1,000 gain reported by Bob (excess liab.) Depreciation expense could never be handled differently by the partners Ord. = [(37,000-1,000+4,000-7,000-750) x .50] (only 1245 is part of ord) Partner is guaranteed $15,000; income share only $12,000; $3,000 GP Use GP and ordinary income share of p’ship year ($12,000 & $6,000) Basis is limited to partnership interest basis less cash received Precontribution gain of $35,000 is recognized ($60,000 - $25,000) Payments for the p’ship interest itself are distributions, not inc. shares After Inv. = $5,500; X gets $500 + $3,500 apprec. + (400/500 x 500 exc) Liabilities assumed are included in amount realized; net gain $0 ¼ of gain on partnership books for rec & inv is ordinary; rest is cap loss