Chapter 12 Examples

advertisement

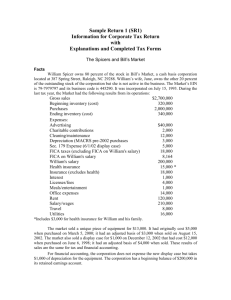

Chapter 12 Examples 1. Assume a corporation is formed with $10,000 cash. It earns $1,000 of net income/taxable income/cash. The shareholder then sells the stock for the FMV of $11,000. Analyze for C Corporation and for S Corporation. 2. S Corporation is a calendar year taxpayer that elected S status in its first year of operations. S’s common stock is owned by A (200 shares with AB = $12,000) and B (100 shares with AB = $6,000). During the current year S has net income for financial statements = $55,000. The S Corporation also made one distribution of $9,000. The corporation’s beginning AAA = 10,000, and the beginning OAA = 1,000. Business Revenue $92,000 Tax-exempt Interest Income 1,000 Gain from sale of equipment – Sec. 1245 depreciation recapture 7,000 Gain from sale of equipment – Sec. 1231 trade/business 12,000 STCG from sale of stock 7,500 Net LTCG from sale of stock 15,000 Rental real estate loss (9,000) Salary expense (44,000) Depreciation expense (8,000) Property tax expense (7,000) Supplies expense (4,000) Interest expense on account with S Corp stock broker (6,000) Bribe of government official (6,000) Recovery of bad debt previously deducted 4,500 Net Income 55,000 a. Assume Sec. 179 election = 5,000 + 11,000 tax depreciation. How will S Corporation, A and B report these results? Also, do the M-1 reconciliation of book income to taxable income. b. What is B’s basis in stock at the end of the current year? c. What is the S Corporation’s AAA balance and OAA balance at the end of the year? 3. DEF, an S Corporation, earns $12,000 ordinary income during the year (actual results are $1,200 per month for January through June 30 and $800 per month for July 1 through December 31) and generates a LTCG of $6,000 on a stock sale that occurs in January. DEF has two 50/50 shareholders, G and H. On July 1 G sells all of G’s stock to M for $30,000. G’s stock basis at the beginning of the year is $25,000. What are the results to G? Assume first no election is made re: allocations. Then, what if an election is made to treat the tax year as ending with respect to G on June 30? 4. After adjusting for income and distributions, L’s AB in S Corporation is $5,000. L has the following flow through losses: capital loss $40,000 and ordinary loss $10,000. What are the tax results? 5. B is a shareholder in RST S Corporation. B’s stock basis before considering a flow through loss on B’s K-1 is $10,000. B has also made a loan to RST in the amount of $5,000. The flow through loss is $13,000. What is the tax result? 6. During the current year an S Corporation made a distribution of $50,000 to its sole shareholder. The shareholder’s stock basis at the beginning of the year = $10,000. The S Corporation has PTI = $9,000 and AEP = $2,500. The AAA account at the beginning of the year = $0. During the year the S Corporation earned $12,000 ordinary income. What are the tax results?