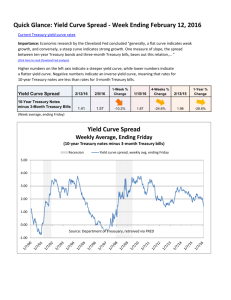

Estimation of the US Treasury Yield Curve at Daily and Intra

advertisement