takes one to - Sequence Inc.

advertisement

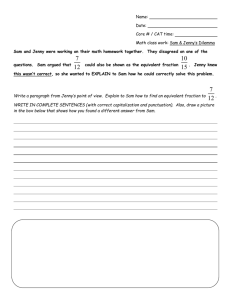

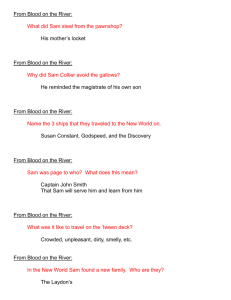

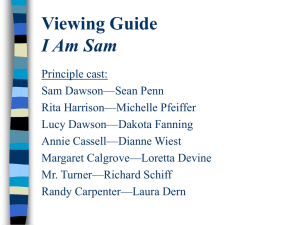

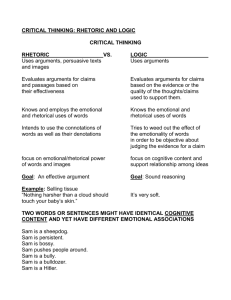

2008 investor’s guide takes one to know one Sam Antar, the felonious former CFO of Crazy Eddie, is now teaching students and prosecutors how to spot fraud in public companies. by peter carbonara and he will not let anyone forget it for a minute. Whenever you find yourself starting to think of him as merely a fast-talking yet charming New York character, he’ll come out with something like: “I had no remorse whatsoever as a criminal. I had no concern about any other human being. I enjoyed being a criminal.” ¶ Antar is a cousin of “Crazy Eddie” Antar, the eponymous founder of the notorious New York City–area consumer electronics chain of the ’70s and ’80s. The business was a forerunner of Best Buy and famous for TV spots featuring a manic, turtleneck-wearing pitchman promising that Crazy Eddie’s “prices are insaaaane!” Sam E. Antar is a convicted felon, Free As a Bird Sam Antar testified against his cousin crazy eddie. now he spends time with his Parrot, Cuddles, in brooklyn. 108 a December 24, 2007 photographs by david yellen December December240, 24, 2007 A 000 takes one to know one Actually, it was the bookkeeping that was insane, and today it provides a cautionary tale that Sam Antar likes to tell, Ancient Mariner–style, to would-be stock pickers. When the company, which went public in 1984, blew up in a financial scandal in 1987, Sam Antar, an accountant, was its CFO. The debacle cost investors roughly $145 million and involved just about every kind of accounting fraud then known to man, including receipt skimming, money laundering, and the counting of bogus inventory. The total dollars involved were puny and the scams simple compared with later baroque swindles like Enron, but for sheer cojones, Crazy Eddie remains unchallenged. That was a long time ago, of course. Antar (known as “Sam E.” to distinguish him from other Sams in the family, especially clan patriarch Sam M.), however, has made a second career out of reliving it. Several times a month he speaks to law-enforcement, accounting, and student groups about Crazy Eddie and what it can tell them about spotting accounting fraud now. In October, for instance, he had two speaking dates in Washington State, a third in South Carolina, a fourth in New York City, and a fifth in Salt Lake City. He travels around the country entirely on his own nickel, he says, and can afford to not because of any pile of money he stashed from the Crazy Eddie era but because his wife, the daughter of a New York real estate developer, is wealthy. While he sneers at words like “redemption,” in more reflective moments Sam E. admits he does it, at least in part, to atone. “I feel guilty about what I did. I want to give back to society,” he says. Antar offers himself for public inspection $145 not as a diabolical accounting genius but as Mr. Bad Example, a living object lesson in million basic criminal behavior. After he’s been introduced at one of his speaking gigs, for instance, he generally thanks the audience for their hospitality—and then scolds them for being chumps. One October morning he told a classroom filled with amused Columbia The college of nefarious knowledge Antar lectures to Professor Arthur Dong’s class at Columbia University’s School of Inter­ national and Public Affairs on Oct. 27. The debacle cost investors and involved nearly every accounting fraud then known to man. 110 A December 24, 2007 University graduate business students, “All too often we give the white-collar criminal a pass. If I were a serial killer, a child molester, a rapist, you wouldn’t applaud me. You’d be throwing eggs—am I right?” And then he’s off to the races, talking about Crazy Eddie and the “artful liars” responsible for the “brutality of white-collar crime.” Sam E., 50, looks exactly like a Mob accountant in a gangster movie, and before an audience he plays the part with brio. A short, balding guy, the product of a tight-knit Syrian Jewish enclave in Brooklyn, Sam E. has bulging eyes. As he talks to the Columbia students, his shirttails are coming out of his pants. He missed a spot shaving this morning. He paces the front of the lecture hall and pauses occasionally to underline a point with his favorite expression: “You understand what I’m saying to you?” At Crazy Eddie he says he had little trouble burying accounting shenanigans where inexperienced or lazy auditors wouldn’t see them. Sam E. and others at Crazy Eddie pumped up the company’s same-store sales with bogus receipts, for instance, and used a variety of devices to count inventory that didn’t exist. Investors who relied on the disclosures blessed by those auditors saw big pops in same-store sales. As a result, Sam E.’s disdain for financial pros runs deep. Most Wall Street analysts are in his estimation wimps: “They don’t ask the right questions.” Accountants: “Most of these people don’t even get any training in fraud.” Corporate audit committees: “They’re less qualified than the inadequately trained auditors.” And the financial press: “You guys are easily intimidated.” As for antifraud laws, Antar says that Sarbanes-Oxley is good as far as it goes, but he doubts that it does much to intimidate dedicated fraudsters. The only safeguards against accounting fraud that work, he says, are stringent disclosure rules for companies and better fraud training for auditors. So with no one looking out for stock pickers, the only investing strategy that makes sense, Sam E. says, is one of sustained and disciplined paranoia. Read SEC takes one to know one then and now Clockwise from left: A New York Times article; A 1981 print ad; and the CNBC reunion of Eddie and Sam in 2007 filings carefully—starting with the footnotes where accounting flimflam may be buried. Listen closely to what executives say publicly and check the comments against their statements and figures in their 10-Qs (the quarterly statements publicly traded companies file with the SEC). Look out for “one-time events” in filings that occur more than once. Those are just some red flags. (For more, see the box below.) the making of a fraud Investor beware 112 A December 24, 2007 About $1.5 million that had been sent to Israel was brought back into the U.S. via drafts on a bank in Panama and pumped back into the company (along with an additional $500,000 in cash) as bogus receipts. The same year as the so-called Panama Pump, Sam E. also created $20 million worth of phony “debit memos” supposedly reflecting rebates on promotional expenses like advertising from manufacturers. The outside accountants didn’t catch either hustle. Most of the auditors monitoring Crazy Eddie’s books were young and inexperienced. Sam E. counted on their lack of suspicion and their unwillingness to do the boring work of checking everything that needed checking. For instance, the auditors checked some of the bogus rebates with the manufacturers and even caught a few of the fakes, but they didn’t check all of them. Sam E. thanked the auditors for catching his “mistakes” and went about his business. Crazy Eddie started to come undone during the mid-1980s as business slumped and the family was riven by a variety of feuds. In 1987, with the stock sliding, a series of shareholder suits were filed alleging that Eddie had withheld bad news from investors while selling much of his stock. The SEC and the U.S. Justice Department started investigations into the company. Various insiders starting telling at least some of what they knew to investigators. In the fall of 1987 a group led by New York businessman Victor Palmieri won a proxy fight for the company and took over from the Antars. Within weeks, though, Palmieri discovered a $65 million inventory shortfall, and he eventually realized he’d been had. Sam E. says that for two years he hung tough, destroying documents and perjuring himself during SEC depositions. In 1990, Eddie fled the coun- From top: Gaslight Ad archives, commack, N.Y.; CNBC Although Sam E. pleaded guilty to three felonies in 1992 and was subsequently kicked out of various accounting industry professional associations, the state of New York got around to revoking his license only this autumn. Sam happily provided documentation of his conviction. “He did a bad thing, and you’d think he’d just Sam E.’s five rules let it go and try to do better in for spotting potential fraud the future. But for some reason it’s important for him to flail in public companies. himself,” says Joseph T. Wells, founder and chairman of the Study SEC filings yourself. External auditors, audit committees, Association of Certified Fraud and Wall Street analysts cannot Examiners, a professional orgaprotect you from most fraud. Ana­ nization. Wells has written exlysts often do not ask the important questions and are too quick to accept tensively about Crazy Eddie and management’s representations. had Sam E. lecture his students at the University of Texas at AusRead the footnotes first. Tiny things can be huge. In the Crazy tin many times. Eddie fraud, the change of a single There were plenty of bad things word (from “purchase discounts done at Crazy Eddie. From its inand trade allowances are recognized when received” to “recognized when ception, members of the Antar earned”) allowed Sam E. to inflate family, which founded and conthe company’s earnings in fiscal year trolled the business, skimmed 1987 by about $20 million. millions of dollars in unreported Watch for inconsistencies. receipts from the company. Some If the CEO tells the press, “We are of that cash went overseas to seprofitable,” make sure the figures in the 10-Q back up the statement. cret bank accounts in Israel and elsewhere. Perhaps the most specAlways crosscheck disclosures. tacular, if not the largest, act of acCompare Management Discussion & Analysis in the current report counting legerdemain happened with MD&A sections in past 10-Qs. in 1986 when the by-then-public Look for any changes in disclosure Crazy Eddie was expanding and language. wanted to show Wall Street how Sound like too much work? good its same-store sales were to If you don't have the time or expertise justify a secondary offering that to do the above, don’t buy individual stocks. Stick with index funds. would benefit company insiders. takes one to know one Crazy Eddie’s new owner discovered a inventory shortfall and realized he had been had. 114 A December 24, 2007 termind the fraud by giving advice to Eddie Antar on accounting aspects of the fraud. I had participated in many aspects of the fraud (though I was not involved in every single aspect of the fraud nor did I have personal knowledge of each and every fraud).” He adds that if his crimes were smaller than Eddie’s—whom he derides as a “coward”—they are still plenty bad: “I take full responsibility for my actions. My sins are unforgivable.” turning over a new leaf As a would-be fraudbuster, Sam E. has yet to notch his first kill. (Although in fairness he doesn’t hold himself out to be a full-time 10-Q detective. “I don’t have 40 people working for me like the SEC,” he says.) He hasn’t brought any companies down or caused any regulators to open any investigations. The one scalp that he has been pursuing lately is online: closeout retailer Overstock.com. Overstock is perhaps most familiar because of the pugnacity of its CEO, Patrick Byrne, and its ongoing libel suit against short-seller Rocker Partners (now Copper River Partners) and research firm Gradient Analytics. (They have denied all of Overstock’s charges and have countersued.) Separately, Byrne has alleged a conspiracy of illegal short-sellers targeting companies like his. (The best introduction to the tangled Byrne-Overstock saga is Bethany McLean’s “Phantom Menace” on fortune.com.) Last year Overstock store: John Pedlin—new york Daily news; Antar: Dan Hulshizer—ap try. (He was caught in Israel in 1992 and extradited to the U.S. in 1993.) With Eddie on the lam, Sam E. claims he was left holding the bag. So he began cooperating, pleading guilty in 1992. He was not motivated by a sudden desire to do right. He didn’t want to do hard time and all that went with it. SEC lawyer Richard Simpson, who was the lead lawyer in the government’s civil case, says Sam E. overcame the government’s distrust of him by telling them lots of things that checked out. “He was the most help of any cooperating witness I’ve seen or any cooperating witness I’ve ever heard of,” Simpson says. In 1993, Eddie and his brother Mitchell $65 million were convicted of racketeering and securities fraud. (Another brother, Allen, was acquitted.) Those convictions were later overturned on appeal, but rather than risk another trial in 1996, Eddie and Mitchell pleaded guilty. Eddie was sentenced to 82 months in prison. Sam E. got off easy because of the plea deal. He paid the SEC $80,000 in disgorgements and fines. He was sentenced to six months of house arrest and 1,200 hours of community service. He served no prison time. Now Eddie is out of jail, and the company is long dead. The emotional wounds of those who went through it all are still very much open, though. Eddie says he doesn’t hate Sam E. but does wish his cousin would let old painful business lie. “It should just be left alone and done with,” he told FORTUNE in an interview this fall. Eddie doesn’t defend himself (“I did what I did”) but says the government let Sam E. skate on his own criminal acts in exchange for his testimony. Sam E., Eddie says, began cooperating with the government two years before Eddie fled the country. (Sam E. denies that.) He also says he finds it absurd that anyone could take a mere flunky like his cousin seriously as any kind of accounting authority. Or as Eddie puts it, “He did what I told him.” Howard Sirota, a New York attorney who was lead counsel for the swindled Crazy Eddie investors, however, defends Sam E. as a capable accountant who befall of the antars came a “relentless investigator” when he decided to coClockwise from top left: a going-out- operate. He also suggests that Eddie and other members of-business sale; a of the family have long tried to discredit Sam E. U.S. Marshals Wanted poster, circa 1990; For his part, Sam E. says he’s made no secret of and eddie being extradited in 1993 any of his misdeeds at Crazy Eddie: “I helped mas- takes one to know one Bench Strength antar enjoys a sunset on the boardwalk not far from his home. lost roughly $100 million (although the company has made much of an Ebidta-positive third quarter in 2007). Its financial performance has made it a target for a number of online gadflies—including Sam E., who has accused the company of a variety of sins. Byrne’s response has been to dismiss Sam E. online as a crank who “makes a hobby out of clogging message boards with deposition-style questions for and non sequiturs about me.” The latest exchange came in November. In October, Sam E. had given his Crazy Eddie presentation at a conference on whitecollar crime at the Utah attorney general’s $80,000 office. He wrote about that on his blog in a post that also contained one of his broadsides against Overstock. The company’s general counsel, former Utah securities regulator Mark Griffin, complained to Utah attorney general Mark Shurtleff, an old friend. Shurtleff wrote a “To Whom It May Concern” letter chastising Sam E. for implying that Shurtleff endorsed his criticisms of Overstock. (Through an Overstock spokesman, Griffin declined to comment.) Shurtleff also took Sam to task for violating an agreement he says Sam had made with the attorney general’s office not to use his recent appearance to promote his campaign against Overstock. Overstock Sam E. got off easy. He paid the SEC in fines and disgorgements and was sentenced to six months’ house arrest. 116 a December 24, 2007 trumpeted the letter in a press release. Sam E. blasted back denying that he had an agreement with Shurtleff prohibiting him from discussing his presentation online. Sam E. also accused the attorney general, who has received campaign contributions from Overstock, of doing the bidding of a wealthy backer. Shurtleff dismisses that as “bullcrap” and adds that Sam E. reminds him of a line he’d read recently: “To a thief everyone looks like a thief.” Which is not the first time Sam E. has been accused of painting with too broad a brush. He’s also been chided by some former Crazy Eddie employees on a message board devoted to reminiscences of the company for painting a totally dark picture of his famous cousin. One former employee wrote, “To me, Kelso [Eddie’s nickname] was a great man, perhaps it was somewhat of a cult, but he was able to take people like myself and draw out of them more success than they might have found by themselves.” The former employee also urged Sam to drop the hair shirt. Sam would have none of it. “What Eddie and I did was nothing but evil. Eddie Antar is not a great man, and neither am I,” he wrote. Any possible lingering doubts about how he wants the world to see him are dispelled by the way he signed that and other posts and e-mails. “Respectfully, Sam E. Antar (former Crazy Eddie CFO and convicted felon).” F feedback fortunemail_letters@fortunemail.com Past as Prologue? For more on Overstock.com, go to fortune.com.