BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

Accounting for Leases

Now & Next

973.822.2220

Accounting for Leases (ASC 840 f/k/aSFAS 13)

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

•

•

•

•

•

•

•

Learning Objectives:

To review recent developments in lease accounting and demonstrate how they have

affected accounting for leases as prescribed under SFAS 13, Accounting for

Leases.

Program Prerequisites: None

Program/Course Level: Overview

Program Content:

Lease accounting has been one of the most controversial accounting topics for

nearly two decades. This program will begin with a quick overview of the current

accounting for leases within ASC 840 (SFAS 13). The focus of the program will be

to address the current exposure draft on Leases, the significant rule changes, the

impact on both the lessee and lessor, impact on preexisting leases and comment

letters associated with this topic.

p

Advanced Preparation: None

Type of Delivery Method: Live & Group Internet Based

CPE Credits: 2

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

2

1

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

3

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

Accounting for Leases

Developments in Lease Accounting

FASB Proposed ASU

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

4

2

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

Accounting for Leases

Developments in Lease Accounting

FASB Proposed ASU

5

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

I. Overview

A lease is a contractual agreement between a lessor, who

conveys the right to use real or personal property (an

asset), and a lessee, who agrees to pay periodic rents over

a specified time.

Rental

Sale

Lessee

Operating Lease

Capital Lease

Lessor

Operating Lease

Sales Type

or

Direct Financing Type

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

6

3

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

II. Operating Leases

A. Definition

An operating lease includes a lessor, who collects

rent, and a lessee, who uses the leased asset and

pays periodic rent for such use. The lessee

merely uses the asset; there is no transfer of

ownership, or of any risk or benefit of ownership.

7

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

B. Accounting for Operating Leases

1. Lessee Accounting

a. Lease Rent Expense

The lessee records rent expense over the lease term,

usually on a straight-line basis unless other methods

are warranted (for example, lease expense can be tied

to sales, to the Consumer Price Index, or to the prime

interest rate).

DR

CR

Rent expense

Cash/rent payable

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

$XXX

$XXX

8

4

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

b.

Lease Bonus (Prepayment)

Lease bonus (prepayment) for future expenses should be classified as an asset

(deferred charge) and amortized using the straight-line method over the life of the

lease.

c.

Leasehold Improvements

A leasehold

l

h ld iimprovementt iis one th

thatt iis permanently

tl affixed

ffi d tto th

the property

t and

d

reverts back to the lessor at the termination of the lease. In general, if the property

is not moveable from the premises by the tenant, it is a leasehold improvement. Air

conditioning ducts would be considered a leasehold improvement, while a painting

hanging on a wall would not.

1) Capitalize Leasehold Improvements

The value of leasehold improvements should be capitalized and added to the property,

plant, and equipment section or the intangible assets section of the balance sheet.

2) Depreciation—Useful Life or Lease Term

Leasehold improvements should be depreciated (amortized) over the lesser of:

a)

Lease life

b)

Asset/improvement life

d.

Rent Kicker

A premium rent payment required for specific events.

e.

Refundable Security Deposit

Is reported as an asset until refunded by the lessor.

1) Period expense

9

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

f.

Free or Reduced Rent Consideration

If consideration (free rental months or reduced rental charge at

beginning) is part of the package, lessee must take total rent expense

to be paid for the entire lease term and divide it evenly over each

period (matching principle).

Rental-Agreement

5 years (60 months) @

$1,000

*First 6 months are free

Net cost for five years

EX

XAMPLE

Total months rented

Monthly rental expense

$60,000

<6,000>

$54,000

÷ 60 mo.

$

900

First 6 months ( Mo. 1 – 6)

DR

CR

Rent expense

$900

Rent payable

$900

Next 54 months (Mo. 7 – 60)

DR

Rent expense

DR

Accrued rent payable

CR

Cash/rent payable

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

$900

100

$1,000

10

5

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

C.

Leasing Issues

1.

2.

Background and evolution

a

a.

Restatements

b.

SEC Staff Letter

Primary issues

a.

Amortization of leasehold improvements

b.

Rent holidays

c.

Lease incentives

d.

Disclosures

11

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

Issue 1: Amortization of Leasehold Improvements

Amortized by lessee over the shorter of:

Their economic lives

Lease term (as defined in ASC 840, f/k/a SFAS 13)

Amortization of LHIs over a term that includes renewals is appropriate only when renewals have

been determined to be "reasonably assured"

A lease that is cancelable……

only upon the occurrence of some remote contingency,

only with the permission of the lessor,

only if the lessee enters into a new lease with the same lessor, or

only if the lessee incurs a penalty in such amount that continuation of the lease appears, at

inception, reasonably assured

... is considered non-cancelable

KEY POINT

Leasehold improvements cause renewal option to be "reasonably assured: when:

1.

LHIs are expected to have significant value at end of initial period such that lessee is

not willing to abandon these assets (i.e. effectively incur a penalty)

2.

Renewal option reasonably assured of exercise

3.

Add the renewal period to the initial term to determine appropriate term for

accounting purposes

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

12

6

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

Issue 2: Rent Holidays

•

Apply ASC 840

840-20-25;

20 25; f/k/a/ FASB Technical Bulletin 85-3,

85 3,

"Accounting for Operating Leases with Scheduled Rent

Increases"

•

Operating leases with rent holidays should be recognized:

1.

On a straight-line basis

2.

Over the lease term

3.

Including the rent holiday period: lease term for accounting purposes

includes all periods lessee has access to and control over leased space

space.

• Straight-line applies unless another systematic or rational

allocation is more representative of the time pattern in which

the leased property is physically employed.

13

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

Issue 3: Lease Incentives

•

Landlord incentives for Leasehold Improvements:

1.

Acquisition of LHI is capitalized asset

2.

Incentive received recorded as a deferred rent by lessee

3.

Amortize incentive as reduction to lease expense over the lease

term

4.

Cash Flow Statement

a.

Acquisition of the leasehold improvement in "investing

activities"

b.

Proceeds of incentive as "operating activities"

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

14

7

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

Issue 4: Disclosures

Amortization Period

For LHIs

Material Lease

Agreements

Disclosures:

Accounting Policies

for Leases

Footnotes, MD&A Critical

Accounting Policies

Basis for

Contingent Rents

Provisions of Material

Leases

original term, renewal

periods, reasonably assured

rent escalations, rent

holidays, contingent rent,

rent concessions, LHI

incentives and other unusual

provisions

15

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

2.

Lessor Accounting

a. Fixed Asset

The cost of the property is included in the

lessor's property, plant and equipment.

1) Depreciation—over the asset's useful life

b. Rental Income

Rental income is reported on either the

straight-line or other systematic method

method.

DR

CR

Cash/rent receivable

Rental income

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

$XXX

$XXX

16

8

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

c.

DR

Security Deposits

Security deposits required by the lease may be either

refundable or nonrefundable:

1)

Nonrefundable—deferred by the lessor

(unearned revenue) and capitalized by the

lessee (prepaid rent expense) until the lessor

considers the deposit earned.

2)

Refundable—treat as a receivable by the lessee

and a liability by the lessor until the deposit is

refunded

f d d tto the

th lessee.

l

Cash

CR

$XXX

Refundable deposit

$XXX

17

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

KEY POINT

• Do not recognize security deposits as revenue in advance of their being earned

(violation of the Rule of Conservatism).

• Remember, revenue is only recognized when the earning process is complete; we

never anticipate revenue.

d.

e.

Temporary Difference

1)

GAAP Rule – report prepaid rental income when

earned

2)

Tax Rule – report prepaid rental income when

received

Lease Bonus

The lease bonus is deferred (unearned income) and

amortized (into income) over the life of the lease.

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

18

9

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

f.

Free or Reduced Rent Consideration

If consideration (free rental months or reduced rental charge at

beginning) is part of package, lessor must take total rental income to

be paid for the entire lease term and divide it evenly over each period

(matching principle/revenue recognition principle).

Rental-Agreement

5 years (60 months) @ $1,000

$60,000

EXAM

MPLE

*First 6 months are free

<6,000>

Net rental income for five years

$54,000

Total months rented

÷ 60 mo.

Monthly rental income

$

900

First 6 months ( Mo

Mo. 1 – 6)

DR

Accrued rent receivable

CR

$900

Accrued rental income

$900

Next 54 months (Mo. 7 – 60)

DR

Cash

$1,000

CR

Rental income

$900

CR

Rent receivable

100

19

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

III.

Capital Lease

A capital lease transfers substantially all of the benefits and

risks inherent in ownership

p of p

property

p y to the lessee.

i.

This is an accounting transaction, which is, in substance, an

installment purchase in the form of a leasing arrangement.

ii.

The lessee accounts for this type of lease as the acquisition of

both an asset (leased asset under capital lease) and a related

liability (obligation under capital lease).

iii.

The lessor accounts for such a lease as a sales-type or a direct

financing lease. A sales-type lease results in a dealer's or

manufacturer's profit or loss to the lessor. A direct financing

lease does not result in a dealer's or manufacturer's profit or loss.

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

20

10

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

A. Lessee Capital Lease Criteria

1. Must meet just one condition to capitalize.

DR

Fi d asset—leased

Fixed

t l

d property

t

CR

$XXX

Liability—obligation under capital lease

$XXX

Ownership transfers at end of lease (upon final payment or required buyout)

Written option for bargain purchase

Ninety (90%) percent of leased property F.V. <= P.V. of lease payments

Seventy-five

y

((75%)) percent

p

of asset economic life is beingg committed in lease term

2. Criteria (N) and (S) cannot be used for a lease that begins

within the last 25% of the original estimated economic life of

the leased property.

21

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

EXAMPLE

Equipment FV is $3,500, lease payments are $1,000 per year, on 12-31 lease term is four years,

assett life

lif iis tten years.

Incremental borrowing rate is 10%

No ownership

No written bargain

FV

P.V. Cost

1

2

3

4

$1,000

$1,000

$1,000

$1,000

$3,500

x 90%

$3,150

$ 910

830

750

680

$3,170

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

22

11

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

B. Lessor: Sales-Type/Direct Financing Type Criteria

1. If a lease, at inception, meets all three of the

following conditions,

conditions it shall be classified by the

lessor as a sales-type or direct financing lease,

whichever is appropriate.

Lessee "owns" the leased property (meets any one of the four lessee's criteria)

Uncertainties do not exist regarding any unreimburseable costs to be incurred by

the lessor.

Collectibility of the lease payments is reasonably predictable.

23

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

IV. Lessee (Capital Lease) Accounting

A.

DR

CR

Calculation of Leased Asset and Liability Amounts

The lessee treats the capital lease as if an asset were being

purchased over time; that is, it is a financing transaction in

which an asset is acquired and a corresponding obligation

(liability) is created.

Fixed asset—leased property

$XXX

Liability—obligation under capital lease

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

$XXX

24

12

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

1.

Recording the Lease

a. Capitalized Amount

Th llessee records

The

d th

the lease

l

as an assett and

d a liability

li bilit

at the lower (lesser) of:

1) Fair value of the asset at the inception of the lease,

or

2) Cost = present value of the minimum lease

payments.

25

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

a)

b)

Includes (all payments that the lessee is obligated to make):

1)

Required Payments

2)

Bargain Purchase Option

When the lease contains a bargain purchase option

option, the lease

obligation includes the present value of the payment required to

exercise the bargain purchase option in addition to the present

value of the minimum lease payments.

3)

Guaranteed Residual Value

The guaranteed residual value is the amount guaranteed by the

lessee to the lessor for the estimated residual value of the asset

at the end of the lease term.

Exclude:

1)

Executory Costs

I

Insurance,

maintenance,

i t

and

d ttaxes can be

b paid

id b

by th

the lessor

l

or

lessee. If the lessor pays them, a portion of each lease

payment representing executory costs is excluded from the

calculation of minimum lease payments. If the lessee pays

these costs directly, they are not included in the minimum lease

payments.

2)

Optional Buyout (not required and not a bargain)

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

26

13

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

KEY POINT

Periodic payment

•Beginning = PV of an annuity due

•Ending = PV of an annuity (in arrears/ordinary)

Bargain

OR

Guaranteed residual

•PV of $1

27

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

b. Interest Rate

The lessee uses the incremental borrowing rate,

d t

determined

i d as th

the llower (l

(lesser)) of:

f

1) Rate implicit in the lease (if known)

2) Rate available in market to lessee (not prime)

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

28

14

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

c. Summary

Capitalized Cost (remember, lower of this cost or market):

O wnership

=

PV of payments and required buyout—(if any)

W ritten

=

PV of payments and bargain buyout

N inety % FV

=

PV of payments (not option buyout)

S eventy five % life

=

PV of payments (not option buyout)

29

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

B.

Term to Use in Computing Depreciation of the Asset

1. Formula for Depreciation

Capitalized lease assets

< Salvage value>

Depreciable Basis

÷ Periods of benefit

Depreciation Expense (per period)

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

30

15

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

2. Period of Benefit (Depreciable Life)

a. Ownership Transfer and Written Bargain

1) Estimated economic life of the asset if the lessee

takes ownership of the leased asset by the end of

the lease or if there is a bargain purchase option as

part of the agreement. The asset is depreciated in

a manner consistent with the lessee's normal

policies.

b. Ninety % FV and Seventy-five % Life

1) The lessee uses the lease term if the lessee does

not take ownership of the asset by the end of the

lease or if there is not a bargain purchase option.

31

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

3. Summary

Depreciation Rules: (Capitalized "lease"

lease asset—salvage

asset salvage value):

Ownership

=

Depreciate over asset life (legal form)

Written

Ninety % FV

Seventy five % life

=

Depreciate over asset life (legal form)

=

Depreciate over lease life (substance over form)

=

Depreciate over lease life (substance over form)

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

32

16

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

E.

Summary of Lessee Capitalization Rules

1. Capitalize

As PP&E on the balance sheet, the leased asset at the lower LESSER of:

a. Cost

PV of future lease payments

Include: Guaranteed Residual Value by Lessee, Bargain Purchase Option (if applicable)

Exclude: "Executory Cost" = Insurance, Taxes, and Repair & Maintenance

1)

Discount Rate: Incremental borrowing rate is the lower (LESSER) of:

a) Rate implicit in the lease (if known)

b) Rate available in market to lessee (not prime)

b. Fair Value

Capitalize

Depr. Life

Ownership

=

PV of payments and required buyout

Asset life

Written

=

PV of payments and bargain buyout

Asset life

Ninety % FV

=

PV of payments (ignore option)

Lease life

Seventy-five % life

=

PV of payments (ignore option)

Lease life

33

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

KEY POINT

If a lease meets more than one of the criteria, then the order of

priority for applying the rules is the exact way they are spelled:

O–W–N–S

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

34

17

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

V. Lessor Accounting

35

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

A. Recording a Sales-Type Lease

g are the terms which are important to

Following

know for sales-type leases:

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

36

18

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

1.

Gross Investment (lease receivable)

The minimum lease payments plus any unguaranteed

g to the benefit of the lessor. This is

residual value accruing

recorded as Lease Payments Receivable on the lessor's

books.

Lease payment

+ Unguaranteed residual value

Gross investment

37

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

2.

Net Investment

This is computed as the sum of the present value of the

payments

y

and the p

present value of any

y

minimum lease p

unguaranteed residual value accruing to the benefit of the

lessor, using the interest rate implicit in the lease.

Lease payments

+ Unguaranteed residual value

Gross investment

x

PV

Net investment

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

38

19

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

3.

Unearned Interest Revenue (Contra-Lease Receivable)

The gross investment less unearned interest revenue equals

net investment. This is amortized over the life of the lease

by the effective interest method and is included in the

balance sheet as a deduction from the gross investment to

report the net investment.

Gross investment

< Net investment >

Unearned interest revenue

39

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

4.

Cost of Goods Sold

The cost of the leased asset plus any initial direct costs,

g fees or commissions to the lessor,, minus the

such as legal

present value of any unguaranteed residual value accruing

to the lessor's benefit. This is charged against income in the

period in which the corresponding sale is recorded.

Cost of Asset

< PV Unguaranteed Residual >

Cost of Goods Sold

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

40

20

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

5.

Sales Revenue

The present value of the minimum lease payments is

p

recorded as sales revenue. This does include the present

value of any guaranteed residual value but does not include

the present value of any unguaranteed residual value.

41

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

EXAMPLE

Recording a SaleSale-Type Lease with Unguaranteed Residual Value (Lessor

(Lessor))

Assume that a lease with a tenten-year term requires rental payments of $5,000 on January 1 of

each year. The lessor's cost for the leased asset is $35,000. The estimated fair value at the

end of the lease (unguaranteed residual value) is $4,000, and the lessor retains ownership at

the end of the lease. The implicit interest rate is 10 percent (P.V. of annuity due is 6.759 and

PV of $1 is .386). Compute the information necessary to record this sales

sales--type lease.

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

42

21

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

EXAMPLE (continued)

1.

Gross investment

= Minimum lease payments + Unguaranteed residual value

= ($5,000 x 10 yrs) + $4,000

= $54,000

43

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

EXAMPLE (continued)

2.

Net investment

= Lease payments x PV of annuity due of $1, 10 periods, 10%

+ Unguaranteed residual value x PV of $1, 10 periods, 10%

= ($5,000 x 6.759) + ($4,000 x .386)

= $35,339

(The present value of the minimum lease payments, but not the unguaranteed residual value, is

recorded as sales, $5,000 x 6.759 = $33,795)

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

44

22

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

EXAMPLE (continued)

3.

Unearned interest revenue = Gross investment – Net investment

= $54,000 – $35,339

= $18,661

45

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

EXAMPLE (continued)

4.

Cost of goods sold

= Lessor’s cost of leased asset + Initial direct costs

– PV of unguaranteed residual value

= $35,000 + 0 – ($4,000 x PV of $1, 10 periods, 10%)

= $35,000 – (4,000 x .386)

= $33,456

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

46

23

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

EXAMPLE (continued)

5.

Present value of lease

payments (sale)

= $5,000 x 6.759 = $33,795

47

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

EXAMPLE (continued)

Journal Entry: To record this sales-type lease

DR

DR

CR

CR

CR

Lease payments receivable

Cost of goods sold

Sales

Equipment

Unearned interest revenue (contra-lease receivable)

$54,000

33,456

$33,795

35,000

18,661

Note: The lessor’s profit on sale is $33,795 – $33,456 = $339, which is recognized at the lease’s

i

inception.

ti

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

48

24

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

B.

Recording a Direct Financing

Since no manufacturer's or dealer's profit is realized in a

g lease,, the fair value of the leased property

p p y

direct financing

equals the cost or carrying value at the inception of the

lease. The information necessary to record this type of

lease is:

49

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

1. Gross Investment (Lease Receivable)

Gross investment equals the minimum lease payments

plus the unguaranteed

p

g

residual value and is recorded

as Lease Payments Receivable.

Lease payments

+ Unguaranteed residual value

Gross investment

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

50

25

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

2. Net Investment

Net investment equals the gross investment plus any

unamortized initial direct costs less the unearned

income. The initial direct costs are amortized over the

lease term by the effective interest method.

Lease receivable

+ Unguaranteed residual

Gross investment

x

PV

Net investment

51

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

3. Unearned Interest Revenue

This is the gross investment less the cost of the leased

property

p

p yp

plus any

y initial direct costs. It is amortized over

the lease term by the effective interest method.

Gross investment

< Net investment >

Unearned interest revenue

Journal Entry: To record a direct financing lease

DR

Lease receivable (gross investment)

$54,000

CR

Unearned interest revenue (contra-lease receivable

$18,661

CR

Asset (at cost or FMV) (Cost + nonrecorded profit)

35,339

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

52

26

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

VI. Sale-Leaseback

53

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

A.

Introduction

In a sale-leaseback transaction, the owner of a property

(seller-lessee) sells the property and simultaneously leases

it back from the purchaser-lessor. Usually there is no visible

interruption in the use of the property. Sale-leaseback

transactions are treated as single financing transactions

where, in general, any profit or loss is deferred and

amortized. In general, two questions are involved in

determining the treatment of any profits:

1. Is the lease a capital or operating lease? And

2. What portion of the rights to the leaseback property are

retained?

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

54

27

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

B. Terminology

1. Selling Price

S lli price

Selling

i iis th

the negotiated

ti t d price

i iin th

the salel

leaseback agreement. It may be less than, equal to, or

greater than the fair value of the property, depending on

the negotiated terms of the sale-leaseback.

2. Profit or Loss on Sale

Profit or loss on the sale is the amount which would

have been recognized by the seller-lessee assuming

there was no leaseback. It is calculated by subtracting

book value from fair value (sale price).

55

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

3. Excess Profit on Sale-Leaseback

a. Operating Lease Excess Profit

The amount of profit on the sale which

exceeds the present value of the minimum

lease payments.

Sale price

< Asset NBV>

T t ti gain

Tentative

i

< PV min. lease payments>

Excess gain

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

56

28

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

b. Capital Lease Excess Profit

The amount of profit on sale that exceeds the

recorded amount of the asset. Note that this

amount will be the same as in an operating lease

unless the leaseback asset is recorded at the

lower fair value.

The recorded amount of the leaseback asset is

the lesser of

i.

The fair value of the leased property, or

ii. The present value of the minimum lease

payments.

57

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

4. Rights to Remaining Use of Property Retained by SellerLessee

The rights to the remaining use of the property are determined by the present

value of rent p

payments

y

p

paid by

y the seller-lessee. The seller-lessee's rights

g

may be categorized as follows:

a.

"Substantially All" Rights Retained (Greater than 90%)

The present value of the rent payments is equal to or greater than 90% of the

fair value of the property. These leases are usually accounted for as capital

leases.

b.

Rights Retained Are Less Than "Substantially All" but Greater than

"Minor" (Between 90% - 10%)

The present value of the rent payments is less than 90% of the fair value, but

greater than 10% of the fair value of property at the lease inception. These

leases are accounted for as either capital or operating leases, depending on

the criteria

criteria.

c.

"Minor" Portion of Rights Retained by Seller-Lessee (Less than 10%)

The present value of the rent payments is 10% or less of the fair value of the

property at lease inception or the lease (back) period is 10% or less of the

asset's remaining life. These leases are usually accounted for as operating

leases.

Note: To determine whether any sales-leaseback transaction should be

accounted for as operating or capital, use the "OWNS" test.

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

58

29

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

Sale-Leaseback: Summary

Gain

Major

90% or More

Middle

90%—10%

Defer All

Defer

(up to PV of leaseback)

(Amortize over leaseback)

Loss (NBV > FMV)

(real economic losses)

Other Losses

(artificial loss)

Recognize

Immediately

Minor

10% or Less

(Life or Sales Price)

No Deferral

(Amortize over leaseback)

Recognize

Immediately

Recognize

Immediately

Defer All

Defer All

(Amortize over leaseback)

(Amortize over leaseback)

Recognize

Immediately

59

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

EXAMPLE

Leaseback—Less Than "Substantially All" but More Than "Minor"

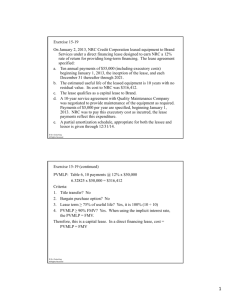

On January 1, Year 1, Carlson Company sold an airplane with an estimated useful life of ten years.

Carlson simultaneously leased back the airplane for three years. The lease is classified as an

operating lease. Applicable data follow:

Sale price, fair value

Book value of airplane

Monthly rental

Present value of lease rentals

$500,000

100,000

5,100

153,000

Calculate the amount of Carlson’s profit recognized on January 1, Year 1, and rent expense on

December 31, Year 1.

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

60

30

Accounting for Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

EXAMPLE (continued)

The present value of lease rentals exceeds 10% of the fair value ($50,000) but is less than 90%

of the fair market value ($450,000).

($450 000) Therefore

Therefore, the amount of profit recognized is the amount in excess

of the present value of the minimum lease payments. The calculation follows:

Sale price

Less book value

Total profit

Less present value of lease payments

(deferred amount)

Profit recognized at lease inception 1/1/Yr 1

(excess profit on sale leaseback)

$500,000

(100,000)

400,000

(153,000)

$247,000

Carlson’s rent expense for the year is calculated as follows:

Annual rent payments ($5,100 x 12 months)

Less one year recognition of deferred profit

($153,000 ÷ 3 years)

Rent expense 12/31/Yr 1

$ 61,200

(51,000)

$ 10,200

61

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

Accounting for Leases

Developments in Lease Accounting

FASB Proposed ASU

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

62

31

SEC Staff Report to Congress

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

I. July 2005 – SEC Staff Issued Report to Congress

A. Required under §401 (c) of Sarbanes-Oxley Act

B. The extent of Off-Balance Sheet Arrangements

C. Whether current financial statements

transparently reflect the economics of offbalance sheet arrangements

D. Among many topics, Lease Accounting is

discussed

63

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Improving Financial Transparency

Objectives-Oriented Standards

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

II. SEC recommends: Accounting standards that are

principle-based or "objectives-oriented":

Clearly state the accounting objective

Minimize the use of exceptions in a standard

Avoid use of percentage tests ("bright lines") to evade intent

Based on an approved and consistently applied conceptual

framework

Provide sufficient detail and structure to operationalize and

consistently apply

III. Rules-based standards:

"further a need and demand for voluminously detailed

implementation guidance creating complexity and uncertainty in

the standard."

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

64

32

SEC Standard Setting

Recommendations—Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

IV. Reconsider Accounting for Leases

A. Repeatedly identified as an area to be reexamined by the

FASB.

FASB

B. Current "all or nothing" approach

not designed to reflect the wide variety of lease structures.

C. Transparency and consistency in reporting is not achieved.

D. A project on lease accounting would be consistent with several

of the key initiatives identified in achieving transparency in

reporting

reporting.

65

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

SEC Standard Setting

Recommendations—Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

• Reconsider Accounting for Leases (continued)

E. Currently uses "bright-lines"

1. Increases potential for similar arrangements to be portrayed

differently

F. “Bright-line” tests facilitate structuring leases by form over

substance

1. Seek desired accounting treatment vs. principle-based

approach

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

66

33

SEC Standard Setting

Recommendations—Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

V. The lease project is complex and controversial

VI Leases have many different terms including:

VI.

contingent rents

optional extensions

penalty clauses

purchase options

67

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

Accounting for Leases

Developments in Lease Accounting

FASB Proposed ASU

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

68

34

Proposed FASB ASU on Leases

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

Accounting for Leases

Developments in Lease

Accounting

FASB Proposed ASU

General Provisions of Lease

Accounting

Lessee Accounting

Lessor Accounting

Other Lease Accounting Topics

Effects on Financial Reporting

Transition and Effective Date

69

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Leases

General Provisions

I.

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

Corporate Behavior – Why Enter into a Lease?

A. Avoid large initial cash outlays

B. Features and options offered by lessor

C. Financial flexibility

D. Off-balance sheet financing

E. Tax Advantages of capital lease – deductions for:

1. Depreciation

2. Interest Expense

3. Synthetic Leases

p company

p y may

y lack credit to borrow from bank

F. Start-up

G. Restaurants and Retailers:

1. No need for lease vs. buy decision (shopping malls)

2. Embedded in business model

3. Prime Location

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

70

35

Leases – 2010 Exposure Draft

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

II.

Leases – 2010 Exposure Draft

A.

On August 17, 2010, the ISAB and the FASB issued an exposure

draft on Leases that p

proposes

p

that a new standard on lease

accounting for lessees and that lessors would replace IAS 17 Leases,

IFRC 4 Determining whether an arrangement contains a Lease, SIC15 Operating Leases – Incentives, and SIC-27 Evaluating the

Substance of Transactions Involving the Legal Form of a Lease.

Source: Aug. 2010 Exposure Draft

71

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Leases

General Provision

III.

CONTINUING PROFESSIONAL EDUCATION

Definition

A.

IV.

BECKER GEARTY

Lease – a contract in which the right to use a specified asset is conveyed, for a period of time,

in exchange for consideration.

Scope

A.

The proposed standard will apply to all leases including subleases of right-to-use assets. Some

arrangements that are specifically stated to not be within the scope of the exposure draft are:

1.

Leases of intangible assets

2.

Leases to explore for or use minerals, oil, natural gas, and other nonregenerative

resources;

3.

Leases of biological assets; and

4.

Leases that meet the definition of onerous contracts prior to the date of the

commencement of the lease.

5.

Contracts that represent the purchase or sale of the underlying asset would be excluded

from the scope. A contract constitutes a purchase or a sale if, at the end of the contract,

the contract transfers both of the following:

a.

Control of the underlying asset.

b.

All but a trivial amount of the risk and benefits associated with the underlying asset.

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

72

36

Leases

General Provision

IV.

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

Scope

B.

C.

Includes:

1.

Combined services and lease contracts (bifurcate lease)

2

2.

Short term leases

3.

Sale-leasebacks

4.

Subleases

5.

Leveraged leases (tentatively added at the July 13, 2011 meeting)

Excludes immaterial items.

1.

If material in the aggregate, consider a policy similar to PP&E capitalization policy.

72

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Leases – 2010 Exposure Draft

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

•

.

KEY POINT

DEFINITION OF A LEASE AS UPDATED BY THE BOARDS ON APRIL 12

12, 2011

1. An entity would determine whether a contract contains a lease by assessing whether:

a. The fulfillment of the contract depends on the use of a specified asset; and

b. The contract conveys the right to control the use of a specified asset for a period of time.

2. A contract would convey that right to control the use if the customer has the ability to direct the use,

and receive the benefit from use, of a specified asset throughout the lease term. Guidance on

separating the use of a specified asset from other services should be aligned with the boards’ tentative

decisions in March 2011 relating to the separation of lease and non-lease components.

3. A “specified asset” refers to an asset that is explicitly or implicitly identifiable.

4. A physically distinct portion of a larger asset of which a customer has exclusive use is a specified

asset. A capacity portion of a larger asset that is not physically distinct (for example, a capacity portion

of a pipeline) is not a specified asset.

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

74lese

37

Leases – 2010 Exposure Draft

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

•

.

KEY POINT

T i pending

Topics

di B

Board

dd

decision

i i on whether

h th they

th will

ill be

b included

i l d d iin scope:

1. Leases of internal-use software in accordance with Subtopic 350-40,

Intangibles–Goodwill and Other Internal-Use Software, of the FASB Accounting

Standards Codification®.

2. Leases of inventory.

74

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Leases

General Provision

V.

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

Types of Leases

A. At the Feb 17th meeting the boards tentatively decided to identify a

principle for identifying two types of leases for both lessees and

lessors with different profit and loss effects

lessors,

effects, as follows:

1. A finance lease with a profit or loss recognition pattern

consistent with the proposals in the exposure draft .

2. An other-than-finance lease with a profit or loss recognition

pattern consistent with an operating lease under existing

IFRSs/U.S. GAAP.

B. The boards tentatively decided to establish indicators to distinguish

a finance lease from an other-than-finance lease

C. The boards asked the staff to use these tentative decisions to

perform targeted outreach to determine if stakeholders’ concerns

about the profit and loss recognition pattern proposed in the

exposure draft would be addressed.

D. To date no subsequent decisions on this topic have been noted.

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

72

38

Leases

General Provision

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

KEY POINT

Ownership transfers at end of lease (upon final payment or required buyout)

Written option for bargain purchase

Ninety (90%) percent of leased property F.V. <= P.V. of lease payments

Seventy-five (75%) percent of asset economic life is being committed in lease term

Operating Leases

73

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Leases – 2010 Exposure Draft

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

•

Note: A contract would normally meet both of these criteria when it transfers

title of the underlying asset automatically at the end of the contract or

includes a bargain purchase option in which it is reasonably certain, at the

inception of the lease, that the lessee will exercise the option. But, all facts

and circumstances should be considered, not just how the transaction is

described in the contract.

KEY POINT

• The determination about whether a contract is a purchase or sale is made at

the time of inception and is not subsequently reassessed.

• Transfer

T

f off the

th title

titl off th

the assett alone

l

is

i insufficient

i

ffi i t for

f an entity

tit to

t decide

d id

that the transaction should be treated as a purchase or sale. For purchase

or sale treatment, all but a trivial amount of the risks and benefits must also

be transferred to the lessee.

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

74

39

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

Accounting for Leases

Developments in Lease

Accounting

General Provisions of Lease

Accounting

FASB Proposed ASU

Lessee Accounting

Lessor Accounting

Other Lease Accounting Topics

Effects on Financial Reporting

Transition and Effective Date

75

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Lessee Accounting - General

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

General

•

•

•

A lessee

lessee’s

s rights and obligations

under all leases, existing and

new, would be recognized on

the balance sheet.

Removes the concept of capital

leases and operating lease

classifications.

Straight-line rent expense will be

replaced with amortization of the

right-of-use asset and interest

expense on the lease obligation

L

Lessee

R

Recognizes

i

on

Balance Sheet

“Right--of

“Right

of-use” Asset

Amortization

Expense

Liability to

make Lease

Payments

Interest Expense

Income Statement

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

76

40

Lessee Accounting – Initial Measurement

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

I.

Initial Measurement

A.

B.

C.

D.

Initially recognize asset and liability at present value of lease

payments

y

to be made.

The right-of-use asset is measured at the amount of the lease

obligations plus any initial direct costs incurred.

1. Initial direct costs: Incremental costs directly attributable to

negotiating and arranging the lease that would not have been

incurred had the lease transaction not been made (commissions,

legal fees) .

Present value uses the rate charged by lessor if available or lessee’s

incremental borrowing rate.

It also includes:

1. Options (renewal and termination) in lease term

2. Contingent rentals, residual value guarantees and termination

payments

77

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Lessee Accounting – Initial Measurement

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

E.

Measurement Date

1. The initial measurement of the lease asset and liability as well

as the date to determine the discount rate is to be the

commencement date of the lease rather than the inception date.

a) Inception of the lease is the earlier of the date of the lease

agreement and the date of commitment by the parties to

the principal provisions of the lease.

b) Commencement of the lease term is the date from which

the lessee is entitled to exercise its right to use the leased

asset.

2 The lease standard will also include guidance regarding:

2.

a) The treatment of costs incurred between the inception

and commencement dates.

b) Lease payments made prior to the commencement date.

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

77

41

Lessee Accounting – Lease Term

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

II.

Lease Term

A.

B.

C.

The lease term is now the same for lessee and lessor. It is defined as

“the non-cancellable period for which the lessee has contracted with

the lessor to lease the underlying asset,

asset together with any options to

extend or terminate the lease when there is a significant economic

incentive for an entity to exercise an option to extend the lease, or for

an entity not to exercise an option to terminate the lease Lessees

would be required to estimate the ultimate expected lease term and

periodically reassess such estimate.”

The boards are to publish indicators of what defines a clear economic

incentive.

p

“only

y when there is a

The lease term will be reassessed byy both parties

significant change in relevant factors such that the lessee would then

either have, or no longer have, a significant economic incentive to

exercise any options to extend or terminate the lease.”

78

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Lessee Accounting – Lease Payments

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

III. Lease Payments

A. Concept of “minimum lease payments” is gone.

B “L

B.

“Lease payments”

t ” will

ill include

i l d contractual

t t l payments

t plus

l estimated

ti t d

contingent rentals.

1.

Percentage rent.

2.

Payments which depend on an index or rate – updated at the

July 20 meeting.

a.

Initial measurement at date of commencement of lease.

b

b.

Reassess at the rate in effect at the end of each reporting

period.

c.

Reflect any adjustment in the income statement if it applies

to the current period or to the value of the right-to-use

asset if they relate to a future period.

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

85

42

Lessee Accounting – Lease Payments

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

IV. Lease Payments

3.

Termination penalties – should be consistent with the

accounting for options to extend or terminate a lease

lease.

4.

Guaranteed residual values – except for amount guaranteed

by unrelated third parties.

85

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Lessee Accounting – Lease Payments

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

C. Contingent Rentals and Residual Value Guarantees

1.

The exposure draft provides that contingent rentals and

es dua value

a ue gua

guarantees

a tees must

ust be est

estimated

ated a

and

d accou

accounted

ted

residual

for using an expected outcome approach, based on a

probability-weighted average for a reasonable number of

potential outcomes. Contingent rentals based on interest rate

changes would be estimated using spot rates.

a.

Amounts payable under purchase options would be

excluded from the present value of lease payments

calculation

calculation.

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

86

43

Lessee Accounting – Lease Payments

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

b.

When determining the present value of lease payments,

the lessee must include contingent rents, residual value

guarantees, and expected payments under termination

penalties.

KEY POINT

This represents a major change from the current lease accounting guidance under

GAAP and IAS that call for the exclusion of contingent rents from the minimum lease

payment calculation regardless of their probability of occurrence.

2.

Initial Measurement: The underlying asset would be initially

measured at the amount of the liability and adjusted for any

prepaid lease rentals and any recoverable initial direct costs

that the lessee incurs.

87

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Lessee Accounting – Lease Payments

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

3.

Timing of Recognition: The asset and liability would be

measured at the inception of the lease, but neither would be

recognized until the date that the lessor makes the underlying

asset available to the lessee for use.

KEY POINT

Under the exposure draft, contingent rents are required to be

estimated and included in the minimum lease payment calculation that

is recorded at the commencement of the lease. The current guidance

under GAAP calls for the exclusion of contingent rents from the

minimum calculation regardless of their probability of occurrence.

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

88

44

Lessee Accounting – Subsequent

Measurement

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

V. Subsequent Measurement

A.

B.

Reassess the carrying amount of the lease payment obligation if there

is a significant change

Accounting for Subsequent Measurement

1. Changes in lease terms: Adjust the right-of-use asset and the

obligation to make rental payments

2. Changes to assumptions (contingent rents, GRV and termination

penalties): Reflected in earnings if change arises from current or

prior reporting periods

3. Changes related to future reporting periods: Adjust the right-ofg

to make rental p

payments

y

use asset and the obligation

KEY POINT

No changes required for the incremental borrowing rate. The discount rate is locked

in at initial measurement

89

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Lessee Accounting – Financial Reporting

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

VI.

Presentation

A.

Balance Sheet

1.

Right of use assets presented with PP&E but separate from nonnon

lease assets.

a.

2.

Lease obligation presented separate from other liabilities.

a.

B.

C.

Amortization term of LHIs to coincide with lease term.

Could affect leverage covenants.

Income Statement

1.

Straight-line expense replaced with amortization and interest

expense.

2.

Foreign exchange differences related to the liability to make lease

payments.

Statement of Cash Flows

1.

Cash payments shown as financing activity.

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

90

45

Lessee Accounting – Financial Reporting

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

D. Updated Requirements – Tentative Decisions as of July 21, 2011

1.

Statement of Financial Position - Lessees may separately

present

p

ese t or

o disclose

d sc ose tthe

e values

a ues related

e ated to right

g to

of use assets

and liabilities.

a.

If they do not separately present they must disclose in

what account the values are included.

b.

The right of use assets should be presented as if they are

owned assets.

90

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Lessee Accounting – Financial Reporting

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

2.

Statement of Cash Flows:

a.

Cash paid for leases payments is classified in financing

act t es

activities.

b.

Classify or disclose the cash paid relating to interest using

U.S. GAAP or IFRS.

c.

Classify cash paid for variable lease payments not

included in the measurement of the liability to make

lease payments as operating activities. (FASB: 4 to 3;

IASB: 13 IASB to 2).

d. Cash paid for short-term leases not included in the

lease liability value are treated as operating activities.

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

90

46

Lessee Accounting – Financial Reporting

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Lessee Accounting – Financial Reporting

91

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

92

47

Lessee Accounting – Financial Reporting

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

VII. Disclosure

A.

As of the July 21st meeting the boards tentatively decided on the

g disclosure requirements:

q

following

1.

A reconciliation of the opening and closing balance of right-of-use

assets, disaggregated by class of underlying asset.

2.

A reconciliation of the opening and closing balance of the liability

to make lease payments – disaggregation is not required as it was

in the ED.

3.

Maturity analysis of the undiscounted cash flows that are included

in the liability to make lease payments

payments. The maturity analysis

should show, at a minimum, the undiscounted cash flows to be

paid in each of the first five years after the reporting date and a

total of the amounts for the years thereafter. The analysis should

reconcile to the liability to make lease payments.

90

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Lessee Accounting – Financial Reporting

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

4.

Information about the principal terms of any lease that has not yet

commenced if the lease creates significant rights and obligations

for the lessee.

5.

Information required in paragraphs 73(a)(ii)-73(a)(iii) of the

exposure draft (additional guidance pending on this item.)

6.

All expenses relating to leases recognized in the reporting period,

in a tabular format, disaggregated into (a) amortization expense,

(b) interest expense, (c) expense relating to variable lease

payments not included in the liability to make lease payments, and

(d) expense for those leases for which the short-term practical

expedient is elected, to be followed by the principal and interest

paid on the liability to make lease payments.

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

90

48

Lessee Accounting – Financial Reporting

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

7. Qualitative information to indicate if circumstances or expectations

about short-term lease arrangements are present that would result in a

material change to the expense in the next reporting period as

compared with the current reporting period

B.

Tentatively the boards agreed these items do not require disclosure:

1.

The discount rate and range of discount rates used to calculate the

liabilities to make lease payments.

2.

The fair value of the liability to make lease payments.

3.

The existence and principal terms of any options to purchase the

underlying asset,

asset or initial direct costs incurred on a lease

lease.

4.

Information about arrangements that are no longer determined to

contain a lease.

90

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Lessee Accounting – Financial Reporting

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

C. Future Commitments – The 2 Boards Differ on This Point.

1 FASB: lessee should disclose the future contractual

1.

commitments associated with services and other non-lease

components that are separated from a lease contract.

2. IASB: lessee is not required to disclose the future

contractual commitments associated with services and

other non-lease components that are separated from a

lease contract.

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

90

49

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

Accounting for Leases

General Provisions of Lease

Accounting

Developments in Lease

Accounting

Lessee Accounting

Lessor Accounting

FASB Proposed ASU

Other Lease Accounting Topics

Effects on Financial Reporting

Transition and Effective Date

94

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Lessor Accounting – General

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

I.

Dual Model

A. Performance Obligation Approach

1. Lease receivable and liability

y to permit

p

lessee’s use of asset

2. Interest income and lease income as obligation is satisfied

B. De-recognition Approach

1. Used only if lessor does not retain significant risks and rewards

of ownership of leased asset

2. Up-front gain for de-recognition of leased asset

KEY POINT

Ownership transfers at end of lease (upon final payment or required buyout)

Written option for bargain purchase

Ninety (90%) percent of leased property F.V. <= P.V. of lease payments

Seventy-five (75%) percent of asset economic life is being committed in lease term

Operating Leases

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

95

50

Lessor Accounting – General

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

II.

Estimates for Both

A. Lease term, contingent payments, other assumptions similar to

essee accou

accounting.

t g

lessee

B. Predict lessee’s behavior as to whether or not lessee is likely to

exercise the options built into the lease

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Lessor Accounting – General

96

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

97

51

Lessor Accounting – General

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

III.

Performance Obligation Approach

KEY POINT

Ownership

p transfers at end of lease ((upon

p final p

payment

y

or required

q

buyout)

y )

Written option for bargain purchase

Ninety (90%) percent of leased property F.V. <= P.V. of lease payments

Seventy-five (75%) percent of asset economic life is being committed in lease term

Operating Leases

A. When risks and benefits of underlying asset are retained, lessor

considers:

1.

Significance of contingent rentals during the expected lease

term based on performance or use of the underlying asset,

2.

Options to extend or terminate the lease, or

3.

Material non-distinct services provided in the lease contract.

98

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Lessor Accounting – General

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

B. The underlying leased asset remains on the lessor’s balance

sheet.

C. The

C

e lessor

esso recognizes:

ecog es

1.

A lease receivable (right to receive rental payments from the

lessee).

2.

A corresponding performance obligation / lease obligation.

D. As the performance obligation is satisfied, revenue is recognized.

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

99

52

Lessor Accounting – General

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

E.

Subsequent measurement: Performance obligation approach

Subsequent measurement of the lessor’s receivable would be at

amortized cost using the effective interest method, resulting in interest

income.

income

1. The exposure draft proposes that, from the time that the lease is

commenced, the lessor would measure its lease asset at

amortized cost using the effective interest method and recognize

any impairments in accordance with IAS 39 Financial Instruments:

Recognition and Measurements.

a) The right to receive lease payments is amortized over the

life of the lease, and the lessor recognizes interest income

using the interest method.

b) To amortize the performance obligation, the lessor must

use a rational and systematic approach based on pattern of

use. If none exists, straight-line amortization should be

used.

100

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Lessor Accounting – General

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

F.

Reassessment: Performance Obligation Approach

1.

The exposure draft requires the lessor to reassess the amount of

p

lease p

payments,

y

, the lease term,, contingent

g

rentals,,

expected

termination options, and residual value guarantees each reporting

period if the facts or circumstances indicate that a significant

change in the right to receive rental payments has occurred.

2.

Accounting for Changes

a)

Changes to lease term: Adjust the lease liability and the right

to receive lease payments.

b)

For contingent cash flows:

1)

Recognize in revenue, if the performance obligation has

been already satisfied

2)

Recognize as an adjustment to performance obligation if

obligation has not yet been satisfied

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

101

53

Lessor Accounting – General

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

G. Presentation: Performance Obligation Approach

Performance Obligation – Lessor Financial Statement Presentation

Balance Sheet

Underlying Asset

xx

Right to Receive Lease Payments

Lease Liability

xx

(xx)

Net Lease Asset / (Liability)

xx

Income Statement

Lease Income

xx

Depreciation Expense

(xx)

Interest Income

xx

Source: August 2010, IASB Exposure Draft Snap Shot: Leases

102

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Lessor Accounting – General

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

IV.

Derecognition Approach:

V.

KEY POINT

Ownership

p transfers at end of lease ((upon

p final p

payment

y

or required

q

buyout)

y )

Written option for bargain purchase

Ninety (90%) percent of leased property F.V. <= P.V. of lease payments

Seventy-five (75%) percent of asset economic life is being committed in lease term

Operating Leases

A.

Assumes that the lessor has performed by delivering the leased asset

and providing an unconditional right to use it over the lease term.

B.

The lessor recognizes:

1.

A receivable (right to receive rental payments from the lessee) and

2.

Records revenue

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

103

54

Lessor Accounting – General

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

C.

D.

A portion of the carrying value of the leased asset is viewed as having

transferred to the lessee, is derecognized and recorded as cost of sales

The amount derecognized:

1

1.

Based on the relationship between the fair value of the receivable from the

lessee and the fair value of the underlying asset

2.

Determined at inception of the lease

E.

The lessor would not remeasure the residual asset retained, except for

impairment.

F.

The value of the residual asset would not be accreted over time

KEY POINT

Note that, although the exposure draft would require the lessor to recognize income and

expense at the time the lease is commenced, the amount of profit recognized initially may

differ from that recognized under a sales-type lease under the current GAAP rules. This is

because the guidance in the exposure draft differs from the current lease accounting

guidance with regards to contingent rentals, residual value guarantees, and other

elements of lease contracts.

104

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

Lessor Accounting – General

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

G. Subsequent Measurement: Derecognition Approach

1.

The exposure draft proposes that, from the onset of the lease, the

g the

lessor would measure the leased asset at amortized cost using

effective interest method and recognize any impairment in

accordance with the guidance set forth in IAS 39.

2.

The lessor would reassess its lease liability similar to how the

lessee would reassess its liability except that the lessor would:

a)

Allocate any change in the carrying amount of the leased

asset that is attributable to a reassessment of the lease

profit and loss;; and

term between the residual asset and p

b)

Recognize other changes in the carrying amount of the

leased asset in profit or loss.

© 2011 DeVry/Becker Educational Development Corp. All rights reserved.

105

55

Lessor Accounting – General

BECKER GEARTY

CONTINUING PROFESSIONAL EDUCATION

3.