PDF Handout - Accounting Educator

advertisement

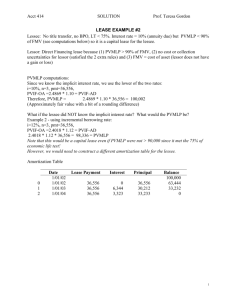

Exercise 15-19 On January 2, 2013, NRC Credit Corporation leased equipment to Brand Services under a direct financing lease designed to earn NRC a 12% rate of return for providing long-term financing. The lease agreement specified: payments y of $55,000 , (including ( g executory y costs)) a. Ten annual p beginning January 1, 2013, the inception of the lease, and each December 31 thereafter through 2021. b. The estimated useful life of the leased equipment is 10 years with no residual value. Its cost to NRC was $316,412. c. The lease qualifies as a capital lease to Brand. d. A 10-year service agreement with Quality Maintenance Company g to provide p maintenance of the equipment q p as required. q was negotiated Payments of $5,000 per year are specified, beginning January 1, 2013. NRC was to pay this executory cost as incurred, the lease payments reflect this expenditure. e. A partial amortization schedule, appropriate for both the lessee and lessor is given through 12/31/14. © Dr. Chula King All Rights Received Exercise 15-19 (continued) PVMLP: Table 6, 10 payments @ 12% x $50,000 6.32825 x $50,000 = $316,412 Criteria: 1. Title transfer? No 2. Bargain purchase option? No 3. Lease term ≥ 75% of useful life? Yes, it is 100% (10 ÷ 10) 4. PVMLP ≥ 90% FMV? Yes. When using the implicit interest rate, the PVMLP = FMV. Therefore, this is a capital lease. In a direct financing lease, cost = PVMLP = FMV © Dr. Chula King All Rights Received 1 Exercise 15-19 (continued) Part 1: Prepare the appropriate entries for both the lessee and lessor to record the lease at its inception. Lessee: Leased asset 316,412 Lease payable 316 412 316,412 Lease payable 50,000 Prepaid maintenance 5,000 Cash 55,000 Lessor: Lease receivable Equipment Cash Maintenance payable Lease receivable 316,412 316,412 55,000 5,000 50,000 © Dr. Chula King All Rights Received Exercise 15-19 (continued) Part 2: Prepare the appropriate entries for both the lessee and lessor to record second payment and depreciation (straight-line) on December 31, 2013 Lessee: Leased payable 18,031 Interests expense 31 969 31,969 Maintenance expense 5,000 Cash 55,000 Depreciation expense 31,641 Accumulated depreciation 31,641 (316,412 ÷ 10) Lessor: Cash 55,000 Interest revenue 31,969 Lease receivable 18,031 Maintenance payable 5,000 © Dr. Chula King All Rights Received 2