Demand, Supply, and Market Equilibrium

advertisement

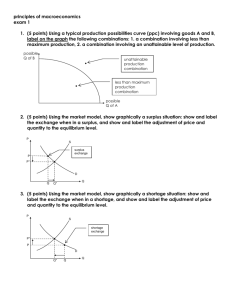

Demand, Supply, and Market Equilibrium Chapter Outline 1. The Circular Flow Diagram 2. Demand a. Definitions b. Law of Demand c. Changes in Quantity Demand vs. Changes in Demand d. Determinants of Demand 3. Supply a. Definitions b. Law of Supply c. Changes in Quantity Supply vs. Changes in Supply d. Determinants of Supply 4. Market Equilibrium a. Excess Demand / Supply $ b. Changes in Equilibrium $ INCOMES COSTS RESOURCE MARKET Circular Flow Diagram On Right. RESOURCES INPUTS Demand Quantity Demanded – the amount of a good that a consumer is HOUSEBUSINESS HOLDS willing and able to purchase at the current market price. Demand – the amount of a good GOODS & GOODS & SERVICES SERVICES that a consumer is willing and able to purchase at all market PRODUCT prices, holding all else MARKET constant. $ $ Demand Schedule – a table CONSUMPTION REVENUE showing how much a consumer is willing and able to purchase at different market prices. Demand Curve – a graph showing how much a consumer is willing and able to purchase at different market prices. Law of Demand – All else equal, as price falls the quantity demanded rises and vice versa. Determinants of Demand 1. Income 2. Price of Related Goods a. Substitute Goods b. Complementary Goods 3. Tastes and Preferences 4. Expectations Chapter 3 Page 1 of 1 Case / Fair Normal Good – the higher your income the more you consume Examples: Sports Tickets, Cars, and Luxury Goods ↑Income consume more at each P ↑D Inferior Good – as income rises you consume less Examples: Ramen Noodles, Potatoes ↑Income consume other products ↓D Substitute Goods – two goods in which a consumer will consume one good or the other Examples: Pepsi or Coke, Rent Movie or Go to Theater, SUV or Mini Van ↑Price of Pepsi drink less Pepsi purchase more Coke ↑D Complementary Goods – two goods consumed together Examples: Pizza and Pop, DVD Player and Movie, Cookies and Milk ↑Price of pizza consume less pizza consume less pizza and pop ↓D Tastes / Preference New tastes for the product Consume more ↑D Expectations ↑Price tomorrow buy today instead of tomorrow ↑D Supply Quantity Supplied – the amount of a good that a firm is willing and able to offer for sale at the current market price. Supply – the amount of a good that a firm is willing and able to offer for sale at all market prices, holding all else constant. Supply Schedule – a table showing how much a firm is willing and able to offer for sale at different market prices. Supply Curve – a graph showing how much a firm is willing and able to offer for sale at different market prices. Chapter 3 Page 2 of 2 Case / Fair Law of Supply – All else equal, as price falls the quantity supplies falls and vice versa. Determinants of Supply 1. Cost of Production a. Prices of required inputs b. Technologies used in production 2. Price of Related Products Prices of required inputs ↑Price of labor hire less people produce less at current P ↓S Technologies used in production New technology produce output for less higher profit on output produce more at current P ↑S Price of Related Products - book only mentions this. Market Equilibrium Shortage (Excess Demand) – a shortage occurs when the quantity demanded is greater than the quantity supplied at a particular price. Surplus (Excess Supply) – a shortage occurs when the quantity demanded is less than the quantity supplied at a particular price. Market Equilibrium – occurs when there is no incentive for prices to change (a steady state). This occurs when there is no surplus or shortage (when QS = QD). Example: Suppose that we are analyzing the market for chocolate. What will happen to the market price and sales of chocolate if consumer’s income increases? Example: Suppose that the actor’s guild lost a lawsuit filed by the movie studios. After the lawsuit the wages fall in the industry. What will happen to the market equilibrium for movie theater tickets? Example: Suppose that Cox Communications increases the price of cable service. 1. What will happen to the price and sales of Direct TV systems? 2. What will happen the equilibrium price and quantity of televisions sold? Chapter 3 Page 3 of 3 Case / Fair