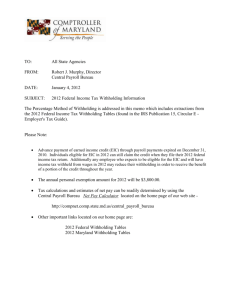

MARYLAND EMpLoYER WithhoLDiNg guiDE

advertisement