india

advertisement

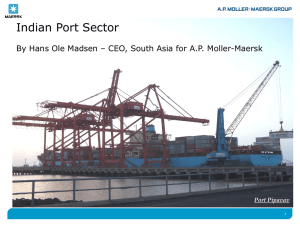

NAMASTE From the Land of Great Wealth and Opportunity INDIA Global Opportunities – India Maritime Sector Presented by : Captain. Somesh Batra Co-Chairman SEAHORSE GROUP Introduction Capt. Somesh Batra ACADEMIC & PROFESSIONAL QUALIFICATIONS 1963 - Pre-sea training on Training Ship ‘Dufferin’ - was awarded ‘Extra First Class’ (Distinction - the highest award). 1970 - Master’s Certificate of Proficiency and Competence from Ministry of Transport, Government of India 1976-77 - Post Graduate Studies in Shipping Management from Plymouth Polytechnic, United Kingdom 1977 - “Management of Offshore Operations” from the above mentioned institution. One of the few professionals in India being qualified in this field. Introduction Capt. Somesh Batra DIRECTORSHIPS Currently Director/Chairman of the following companies: Bay Container Terminals Pvt. Ltd Marine Container Services (India) Pvt. Ltd. Marine Container Services (South) P. Ltd Seahorse Ship Agencies Pvt. Ltd. Seahorse Distribution & Freight Services Pvt. Ltd Sanko Kisen Seahorse (India) Pvt. Ltd Seahorse Buss Infrastructure Pvt. Ltd. Tristar Container Services (Asia) Pvt. Ltd. Yang Ming Line (India) Pvt. Ltd. Member on the Council of Management of the World Trade Centre, Mumbai since 1992. Vice Chairman of the Board. Introduction Seahorse Group Container Leasing NVOCC & Multimodal Transportation Ship Agency Container Repairs & Storage Depot Management Core Operating Areas Port Representation Total Freight Solutions & Distribution Systems Port Captaincy & Cargo Supervision Ship Manning & Management Chartering & COAs, Offshore Introduction Seahorse Group n Ludhiana New Delhi n w n Mundra n n Ahmedabad Kandla Pipavav n Kolkata nn INDIA Vadodara w Nagpur w w Mumbai n Nhava Sheva n n Vizag Hyderabad Associate Offices w Depots n nw Bangalore Mangalore n Seahorse Offices w n wn Chennai n Coimbatore Cochin n Tuticorin w More than 2000 employees & 30 Offices Introduction Seahorse Group – Joint Ventures Yang Ming Line (India) Pvt. Ltd. Marine Container Services & Yang Ming Line, Taipei Shipping & Transport Tristar Container Services (Asia) Pvt. Ltd. Marine Container Services & Triton Container Intl, U.S.A. Domestic container leasing Seahorse Buss Infrastructure Pvt. Ltd. Marine Container Services & Buss Capital, Singapore) For long term financing of Infrastructure Projects. Sanko Kisen Seahorse (India) Pvt. Ltd. Seahorse Ship Agencies & Sanko Kisen, Tokyo For handling chartering of Sanko’s tonnages INDIA India At a Glance Official Name: Republic of India Area: 3.3 MN Square Kilometres North to South - 3,214 KM East to West - 2,993 KM Coastline - 7,517 KM Administrative Divisions: 28 States and 7 Union Territories Head of Government: Prime Minister Capital: New Delhi Population: 1.24 BN GDP: US$ 3.26 TN Major Cities: Delhi, Mumbai, Kolkata, Chennai, Bengaluru, Hyderabad Currency: Indian Rupee (INR) *Source: National Portals of India India At a Glance India At a Glance - Road Network – 2nd Largest in the World *Source: map of world India At a Glance - Railway Network – 4th Largest in the World *Source: map of world India At a Glance - Air Network – One of the Largest Networks in the World *Source: map of world ECONOMY India GDP Growth 9 8 8.4 8.4 7.6* 7 6 6.9 6.7 5 4 3 2 1 0 Y08-09 Y09-10 Y10-11 Y11-12 Y12-13 Mr. Pranab Kumar Mukherjee Finance Minister *Projected - Source: Prime Minister office – Y – APR-MAR India Economic Scenario - GDP growth trends – India Vs World Region 2010 2011* 2012* 2013* World 4.0 2.8 2.6 3.2 Developed Economies 2.7 1.3 1.3 1.9 Developing Economies 7.5 6.0 5.6 5.9 China 10.4 9.3 8.7 8.5 India 9.0 7.6 7.7 7.9 Source : World Economic Situation and Prospects 2012 The United Nations Department of Economic and Social Affairs India Economic Scenario - % GDP Contribution Percentage share in GDP - Agriculture Percentage Share in GDP - Industry Industry 30% Agriculture 17% Services 53% Percentage Share in GDP - Services India Pre – Liberalization – Prior 1991 Industry Licensing and Quotas Dominance of Public Sector Restriction on Private Investment Controlled Economy India Post - Liberalization Stage - Strategies Developed Government’s role -Licensor to Regulator Barriers Dismantled - Procedures Simplified Open Economy FDI welcomed in all sectors E-Governance Free Trade Agreements Globalization of Indian Industries Service sector to the forefront India India’s – Trade Total EXIM trade over US$790BN Ambitious Target – Achieving a 5% share in world trade by the year 2020 April – March 2010-11 2011-12 % Increase Export $ BN 251 303 21 % Import $ BN 370 488 32 % Mr. Anand Sharma Union Cabinet Minister in charge of Commerce and Industry and Textiles * Department of Commerce – Govt. of India` India India- Canada Bilateral Trade 2008-2011(Jan-Dec) - US$ BN Details 2008 2009 2010 2011 Exports to Canada 2.0 1.8 2.1 2.6 Imports from Canada 2.3 1.9 2.0 2.6 Total 4.3 3.6 4.1 5.2 “Bilateral Trade - equivalent to 2 1/2 days of US-Canada trade… India stands out in the world, as an emerging market with a strong democratic base, fully functional in English – the worldwide accepted business language, as a country where the rule of law pervades and as a country that survived the economic recession.” John Manley, President & CEO, Canadian Council of Chief Executives Source: Statistics Canada India Direct investment between India and Canada 2008-2010 – Canadian$ MN Details 2008 2009 2010 2011 Canadian direct investment in India 785 601 500 492 Indian direct investment in Canada 2,667 2,972 6,600 6,554 Total 3,452 3.573 7,100 7,046 “Common democratic traditions and underlying people-to-people links, bind IndoCanadian ties. Broad based bilateral economic partnership with strong collaborations in agriculture, education, infrastructure, manufacturing, tourism and knowledge industries like clean technologies, biotech, pharmaceuticals and R&D.” Hari Bhartia, President-designate, CII Source: Government of Canada India Indian companies investments in Canada Indian Co’s Canadian Co’s / Industry Year Essar Steel Ltd - Acquired Algoma Steel 2007 TATA Communication (VSNL) Acquired Teleglobe 2007 Hindalco Ltd (Aditya Birla Group) – Acquired Novelis Inc 2007 Jubilant Organosys – Acquired Draxis Health 2008 Tata Steel Global Mineral Holdings – JV New Millennium Capital (NML) and LabMag – For developing a direct shipment ore (DSO) project 2009 Mahindra Satyam – Opened Smart Grid Research and Innovation Centre (RIC) University of Waterloo Campus in Ontario 2011 Maharashtra State Government MOU Government of Quebec- Health & Social Services 2012 Other Major Investors Tata, Satyam Computer Services, Wipro, Infosys and Aditya Birla Group, State Bank of India, ICICI Bank India Canadian companies investments in India Canadian Co’s India Co’s / Industry Year Bombardier – Plant to build Metro rail coaches State of Gujarat 2008 CAE Inc. – Construction of new Flight helicopter simulation centre Hindustan Aeronautics Limited / Bangaluru 2009 SNC-Lavalin PAE Inc – Contract to build Mumbai’s newest metro lines Mumbai Metro Rail cooperation 2009 Other Major Investors BCE, RIM, McCain Foods, CGI, Sun Life, MDS Nordion, Scotiabank, R. V. Anderson Associates Ltd., M. A. Jans & Associates (MAJ), Tele-Direct International & Deloitte & Touche LLP Canada. India BRICS countries are BIG on Merger & Acquisitions % Businesses planning M&A over the next 3 Years * GRANT THORNTON IBR 2012 India Potential Foreign Trade (FTA’s) Canada **CEPA: Likely to conclude by 2013 (Current $ 5 BN) EU FTA: End 2012 – Operational 2013 (Current Trade $ 75 BN) China: Trade to double - $100 BN by 2014 (Current $ 60 BN) ASEAN: Bilateral trade $70 BN by 2014 (Current $ 50 BN) Korea: Trade to double $24 BN by 2015 (Current $12 BN) Indonesia: Trade to double $20 BN (Current $10.5BN ) Japan - CEPA 2011:Trade to double $ 25 BN by 2014 Malaysia CECA 2011:Trade to reach $15 BN by 2015 (Current $ 9 BN) India- 2nd most preferred destination for foreign investors “Doing Business in India‘-Ernst & Young” http://www.international.gc.ca INFRASTRUCTURE India Infrastructure Infrastructure sector will require $ 1.7 TN investment in the next 10-years. “Goldman Sachs Report” Needs to spend $ 1.2 TN by 2030 to meet the projected demand of its cities “McKinsey Global Institute Report” India 12th Plan – To Focus on All Inclusive Growth 50% - Private sector participation (11th Plan 36%) - Decade ago - 5% 12th Five year Investment plan Total – $1025 BN ($ 514 BN 11th Plan) 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 132 155 178 202 230 260 India Building India, Step by step !!! 10th – 12th Year Plan Agriculture : 12th-2012-17 9 12th year plan aimed at a 4% growth. (11th plan 3%, 10th plan 2%) Manufacturing : 8.2 11th-2007-12 9 Prime Focus on Public Private Partnership (PPP) to facilitate infrastructure investment. 7.8 10th-2002-07 8 7 7.2 7.4 7.6 7.8 8 The Brick and Mortar of the Economy – will grow at 11-12 % 8.2 ACHIEVEMENT 8.4 8.6 8.8 9 TARGET India Infrastructure in India FDI up to 100% under the Automatic Route: Exploration of oil and natural gas fields, infrastructure related to actual trading and marketing of petroleum products, petroleum product & natural gas/LNG pipelines, Petroleum refining in the private sector. Setting up New and in Established Industrial Parks Investment Opportunities: Global private equity (PE) funds to target Indian infrastructure companies in the coming years for high return on investments making India the most preferred choice among Emerging Markets. Sub-sectors to chose from: Power, Telecom, Roads and Ports. Report by Research Agency “Preqin” Source: Consolidated FDI Policy, Department of Industrial Policy & Promotion (DIPP) India Growth of Infrastructure 1998 – 2011 - impressive physical growth Sector Roads Length (MN KM) National highways (000 KM) 1998 2011 % increase 3.3 35 4.2 71 28 101 2.5 8.3 226 62,800 350 65,000 950 4 175 16 50 213 Ports Traffic handled (MN TEUs) Rail Route (KM) Goods transported (MN tonnes) Airports Passengers handled (MN) India Golden Quadrilateral Golden Quadrilateral highway 5829 KM – 4 Lane North–South & East–West Corridor highway 5831 KM – 4 Lane Port connectivity – All major ports 330 KM – 4 Lane Inter-capital 1342 KM – 4 Lane Bypass and other national highways. 945 KM – 4 Lane 14,277 KM of highways connect major manufacturing centers, commercial cities of India *Source: map of world India Western Corridor - Dadri (Delhi) to JNPT– Nhava Sheva Project Investment $ 100 BN 1483-km long Passes through Six States Traffic will rise 2017 3.8mn TEU 2022 5.3mn TEU Project Phasing : Phase – I Commissioning Rewari – Vadodara 31st Dec 2016 Full Commissioning J.N. Port - Dadri 31st March 2017 India Eastern Corridor – Sonnagar (Bihar) to Ludhiana (Punjab) Project Investment $ 100 BN Total length of 1,279km. Passes thru 6 states Traffic will rise 2017 75.6 MN tonnes 2022 91.0 MN tonnes Project Phasing : Commissioning of Eastern Corridor 31st December 2016 India Roads Development - Transition 1997 Policy framework Approved India BOT Initiative for private investment in Road sector 2005 NHDP Programmes/Projects awarded only on BOT basis. NHDP - Largest Private Sector Interest “Classical Infrastructure Projects.” 2012 India has about 4.2MN KM of Road Network “Department of Industrial Policy and Promotion (DIPP) statistics” India Roads Development - Investment Opportunities 2012–13 India’s Construction Sector to grow @ 35%. 12th Five Year Plan US$ 100 BN on Roads and Highways The Private Sector is Expected to Contribute 44% Phase IV connectivity of 20,000 km of 2 Lane and 4 Lane Roads to be built during the 12th five year plan, connectivity to the economic hinterlands. “Department of Industrial Policy and Promotion (DIPP) statistics” India Roads Development - Investment Opportunities 100% FDI is allowed under the Automatic Route: Support services to Land Transport like Operation of Highway Bridges, Toll Roads, and Vehicular Tunnels Services incidental to Land Transport like Cargo Handling Construction and Maintenance of Roads, Bridges Construction and Maintenance of Roads and Highways on Build-onTransfer (BOT) basis, including collection of Toll “Source: Consolidated FDI Policy, Department of Industrial Policy & Promotion (DIPP) India Railways in India: Vision 2020 The 4th largest Rail Network after US, Russia and China. 4th largest commercial or utility employer - over 1.4 MN employees 114,500 KM & 7,500 stations. FDI inflows worth US$ 233 MN - April 2000 to November 2011 Aims at Adding 25,000 Route km to the Railway Network Will follow Public Private Partnership (PPP) Model in Projects Special Task Force to Clear Investment Proposals within 100 Days http://m.oifc.in/Sectors/Infrastructure/Railways and “Source: Consolidated FDI Policy, Department of Industrial Policy & Promotion (DIPP) India Railways - Investment Opportunities Large investment under PPP route – Logistic Parks/ Hub Efficient Use of Assets - Modernization and upgradation of equipmentboth fixed infrastructure & rolling-stock Doubling and Port Connectivity Dedicated Freight Corridors Asset Renewal/Modernization of Freight Terminals Wagon investment scheme FOIS : Freight Operations (Real time) information system Introduction of Private Container trains http://m.oifc.in/Sectors/Infrastructure/Railways & *Source: CII India Special Economic Zones (SEZ)- Engines of Economic Growth A major hub for Manufacturing & Exports Srinagar Internationally competitive Environment Shimla Dehra Dun Noida Delhi Jaipur Lucknow Jodhpur Guwahati Kanpur Gandhidham Tax exemption benefits Indore Ahmedabad Kolkata Bhuvaneswar Mumbai Pune 91- Special Economic Zones 8 - Export Processing Zones Hyderabad Nhavasheva Vishakhapatnam 27 % of India’s Exports 143 Operational SEZ Manipal Bangalore Chennai Kochi 587 Formal Approvals Coimbatore Partial List Nanguneri *Source: map of world India Major Inland Container Depot’s (ICDS) Ludhiana Delhi Rewari Jodhpur Faridabad Moradabad Guhawati Jaipur Gateway Port Mundra Ahmedabad NhavaSheva Ludhiana, Delhi, Dadri, Faridabad, Loni, Moradabad, Rewari, Jaipur, Ahmedabad, Dashrath, Pune, Pithampur, Hyderabad Mundra/Pipavav Ludhiana, Delhi, Dadri, Faridabad, Loni, Ahmedabad, Kandla Ahmedabad, Tuticorin Coimbatore Chennai Hyderabad, Bangalore Vizag Delhi Kolkatta/ Haldia Guwahati Kandla Dashrath Pipavav Haldia Pithampur Kolkata Hyderabad Pune Mumbai Vizag Nhava Sheva ICD Connectivity Bangalore Coimbatore Chennai Kochi ICD SEA PORT Tuticorin *Source: map of world India Major Freight corridors Delhi Amristsar Birgunj - Nepal Guhawati Ahmedabad Indore Mundra Haldia Nagpur Kolkata Pipavav Hazira Mumbai Vishakhapatnam Nhava Sheva Hyderabad Kakinada Guntur Bangalore Chennai Cochin Tuticorin Trunk route Secondary route *Source: map of world India Logistics - Adaptation India Logistics - Adaptation India Logistics - New vehicle designs on the Indian roads today India Logistics - New vehicle designs on the Indian roads today MARITIME DEVELOPMENT India Sea Ports India’s trade stands at 9.7 MN TEUs per annum in 2011. Between 2000 and 2010, India grew at CAGR of 13% annually Increased port capacity imperative for the country's trade growth Ludhiana Delhi Rewari Jodhpur Mundra Faridabad Moradabad Guhawati Jaipur 13 Major Ports - 64 % Cargo Ahmedabad Kandla Haldia Paradip Pipavav Kulpi Dashrath Pithampur Mumbai Nhava Sheva Dhamra Kolkata Vizag Mormugoa Kochi 38 % Liquid bulk Hyderabad Pune New Mangaluru 187 State ports 33 % Dry Bulk 15 % Containerized Cargo Bangalore Coimbatore Ennore Katupally Chennai Tuticorin ICD SEA PORT 5 Major Bulks – Iron ore, Coal, Grain, Bauxite, Alumina & Phosphate. India Throughput Jan-Dec 2011 – (9.7 MN Teus) Sea Ports - Ludhiana Delhi Rewari Jodhpur Mundra Faridabad Moradabad Guhawati Jaipur Ahmedabad Kandla Haldia Paradip Pipavav Kulpi Dashrath Pithampur Mumbai Nhava Sheva Dhamra Kolkata Hyderabad Pune Vizag Port 2011 Nhava Sheva 4.3 ** Chennai 1.6 Mundra 1.4 Kolkata / Haldia 0.5 Tuticorin 0.5 Pipavav 0.6 Kochi 0.3 Kandla 0.2 Mumbai 0.1 Vizag 0.2 Total 9.7 Mormugoa New Mangaluru Kochi Bangalore Coimbatore Ennore **Nhava Sheva throughput Katupally Chennai Tuticorin ICD SEA PORT 2016 2020 11 MN Teus (Proj) 23 MN Teus (Proj) (Latest 10 year Plan Indian Ministry of Shipping) India Maritime Sector India’s merchant shipping fleet- ranked 16th among the maritime countries 95 % by volume and 70% by value of International trade is carried through Maritime transport. 14,500 KM of inland waterways- 5 declared as National Waterways Develop coastal movement, inland water ways to supplement rail-road India Maritime Agenda 2010-20 The Government aims to create a port capacity of around 3200 MN Tons to handle the expected traffic of about 2500 MN Tons by 2020 Mr. GK Vasan, Union Minister MoS India Maritime Agenda 2020 - Port Traffic / Tonnage Projected Total Cargo Traffic Growth 3500 3126 3000 2591 2500 2495 2019 MMTPA 2000 Traffic Capacity 1500 1088 1000 884 570 660 500 0 2005-06 2010-11 2016-17 2019-20 India Projected container handling capacity-2020 Upper West Coast Total 33 MNTEUs Upper East Coast 6.0 Kandla, Mundra, Pipavav, Hazira 3.0 Central West Coast 12.3 Mumbai, JNPT, Dighi & Jaigardh 1.2 Paradip, Haldia, Kolkata, Dhamra, Kulpi Central East Coast Vizag, Gangavaram, and Krishnapatnam Lower West Coast Lower East Coast New Mangalore, Kochi, Mormugao, Vizhinjam Chennai, Ennore, Tuticorin India Port Developments Container handling Projects Envisaged up to 2020 Upper West coast Adani Hazira Port at Jamnagar. South Port-Adani Port( Mundra) – Ro-R0 & Container Terminnal - mid2012. Mundra Kandla Central West Coast-Mumbai Haldia Pipavav Paradip Hazria Offshore Terminal - Dec-2012. 4th Container Terminal at JNPT – Awarded to PSA Intl & ABG Ports 4.8 MN Teus Corporatisation of JNPT (Venice Port Authority agreement signed), New developments in Rewas and Dighi ports 5th Terminal 10MN Teus designed by Scott Wilson Kolkata Mumbai Rewas Nhava Sheva Vishakhapatnam Dighi Mormugao Krishnapatnam Mangalore Kochi Chennai Tuticorin Vizhinjam 2015 -Private sector to handle 50% of the nation's cargo. India Port Developments Container handling Projects Envisaged up to 2020 Central East coast 270 meter long riverine multipurpose jetty at Salukhkhali, Haldia Dock under process Container handling facilities at Gangavaram & Krishnapatnam. Mundra Kandla Haldia Pipavav Kolkata Paradip Hazria 2nd Container Terminal at Tuticorin, Mumbai Rewas Nhava Sheva Vishakhapatnam Dighi International Bunkering terminal at Vypeen, Cochin Port Container Terminal at Kattupalli (near Chennai) BY May/2012 Lower West coastMormugao Container Terminal at Vizhinjam. Kulpi and Dhamra Lower East coast Krishnapatnam Mangalore Kochi Vizhinjam Chennai Tuticorin Container terminal at Ennore (near Chennai) progressing. Container handling facility at Karaikal 2015 -Private sector to handle 50% of the nation's cargo. India Developments - Break Bulk terminals Central East coast Break bulk - port development to meet – Coal Import / Iron Ore Export. Dhamra port - URS Scott Wilson project Management consultant. Mundra Kandla Haldia Pipavav Kolkata Paradip Hazria Mumbai Rewas Nhava Sheva Vishakhapatnam Dighi Mormugao Krishnapatnam Mangalore Kochi Paradip - Channel deepening/construction of deep draft iron ore and coal berths – capacity expansion 251m tonnes. Chennai Krishnapatnam port, a private greenfield deepsea port – 18 metres draft Ambitious plans to become a “South Asian” focus for dry bulk, heavy lift and project cargo. Tuticorin Vizhinjam 2015 -Private sector to handle 50% of the nation's cargo. India Ports Development - Transition 1995 1st Privatisation Effort – BOT Concession for NSICT signed in 1997 Subsequent PPPs – Terminals at Tuticorin, Chennai, Visakhapatanam, and JNPT 3rd Berth Success Stories- State Level Projects: Gujarat-Mundra, Pipavav Andhra Pradesh-Gangavaram Odhisa-Dhamra Tamil Naidu -Kariakal Most state developments as “Greenfield” development India Ports Developments – Break Bulk India Ports Developments – Break Bulk India Ports Developments – Dry bulk seaborne trade growth 2012 f Billion tonnes 2010 2,400 2,300 2,200 2,100 2,000 1,900 1,800 1,700 1,600 1,500 1,400 1,300 1,200 1,100 1,000 900 800 700 600 500 400 300 200 100 0 Capesize Iron Ore Phosphate Rock Salt Sulphur Ex-capesize Steam Coal Aluminium Raws Rice Aluminium Products Capesize Coking Coal Cement Coke Paper/Pulp Grains Non-Ferrous Ores Pig Iron DRI Steel Forest Products Petroleum Coke Ex-capesize Fertilisers Sugar Ferrous Scrap India Ports – Cargo Outlook POL (Petroleum, Oil, Lubricants) Increased focus on LNG Increase - Consumption of Crude Oil and products Demand & Supply gap – increased imports Coal Steel consumption is to grow at about 16% pa Electricity demand to increase 7-10 % pa India Ports – Cargo Outlook Iron ore Government policy - Iron ore exports to be canalized Restrictions on mining Fertilizers (Agriculture sector) Consumption exceeded domestic production in Nitrogenous (N), phosphatic (P) fertilizers Entire potassic (K) fertilizers met through import http://steel.nic.in/policy.htm India India Infrastructure - Maritime Agenda New Maritime Agenda 2010-20 (Maritime Development Program) $ 110 BN to Develop Ports and Shipbuilding by 2020 Port Sector $ 66 BN Private investment Shipping sector $ 44 BN thru PPP Capacity expansion 3.2 BN MT (Traffic of about 2,500 BN MT). Develop Coastal Movement, Inland Water Ways to Supplement RailRoad To increase India's share in global ship building to 5%(Present 1%) Source: Consolidated FDI Policy, Department of Industrial Policy & Promotion (DIPP) India Target 2020 Develop 2 New Major Ports Develop 2 New Hub ports: One each on the West Coast & East Coast Upgrade 4 of the existing 13 ports – (Major Maritime Hubs) West Coast - Nhava Sheva & Kochi East Coast - Chennai & Visakhapatnam All Major Ports 14 metres and Hub Ports 17 metres Draft Adequate storage areas in Major Ports Major Ports to set up Ship Repair and Maintenance Hubs India Port Sector - Target 2020 100% FDI is allowed under the Automatic Route: To Supplement Domestic Capital, Technology and Skills, for Accelerated Economic Growth. 2000-2012 (FDI) into Ports at US$ 1,635 MN Leasing of existing Ports / Assets Leasing of Equipment for Port Handling and Leasing of Floating Crafts Captive Facilities for Port based Industries http://m.oifc.in/Sectors/Infrastructure/ports Source: Consolidated FDI Policy, Department of Industrial Policy & Promotion (DIPP) India Port Sector - Target 2020 Construction / creation and maintenance of Assets Container terminals Bulk / Break bulk Multi-purpose and specialized cargo berths Warehousing, container freight stations Storage facilities and tank farms, cranage / handling equipment, Setting up of captive power plants, dry docking and ship repair facilities Coastal movement Source: Consolidated FDI Policy, Department of Industrial Policy & Promotion (DIPP) India Inland waterways 14,500 KM of navigable inland waterways Total 5 National inland Waterways 3 developed & operational - 2716 KM Allahabad-Haldia -1620 KM in Uttar Pradesh, Bihar, Jharkhand and West Bengal Sadiya-Dhubri -891 KM in Assam Kollam-Kottapuram -205 KM in Kerala 1027 KM states of Andhra Pradesh, Tamil Nadu & the Union Territory of Puducherry 588 KM states of West Bengal & Orissa STRENGTHS India Politics in India Democracy … is our Biggest Asset … Yet sometimes it moves like : ‘ A Drunken Sailor … One step Forward and Two Step Sideways ! India Strengths Availability of Democratic System of Resources Governance 1. Availability of Raw material 1. 2. Well-developed technical and tertiary education infrastructure Active judiciary-respect of patents 2. Progressive reforms 3. English is language of business 3. 4. High availability of skilled workforce Low cost labour INDIA ADVANTAGE Large Domestic Strong Economic Market Environment 1. Strong middle-class 1. Consistently growing GDP & FDI 2. Growing consumerism and young population 2. Stable Interest rates 3. Maturing capital markets India Growing younger Population distribution (In MN) : 2016 140 120 120 100 100 80 80 60 60 40 40 20 20 0 0 0-4 5-9 10-14 15-19 20-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75-79 80+ 140 0-4 5-9 10-14 15-19 20-24 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64 65-69 70-74 75-79 80+ Population distribution (In MN) : 1996 77% of India’s population is less than 40 years old. The average age of its population is 25 years. Source: IMA Research, Census of India, Ministry of Home Affairs India Working Harder - A growing working population India China Japan UK % of working age adults to total population 75 70 65 60 55 50 45 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050 By 2020: India’s working age population ratio will be the highest in the world. A huge opportunity… Source: UN population division; working age defined as 15-64 years OPPORTUNITIES India Globalization of world economy bolsters the increasing importance of international trade and the roles of ports and MNC’s. Technological advances in networking, telecommunication, & information Economic liberalization Capital market formation Globalization The importance of international trade Globalization Globalization Globalization Globalization The importance of port economics The role of multinational corporations India The increasing importance of Air/ Sea ports and MNCs Economic Liberalization Internationalization Networking & Informationalization *Source: Jennifer Fang-Yu Huang / Taiwan India India Auto Industry - Global Small Car & Outsourcing Hub! COMMERCIAL VEHICLES India India Auto Industry - Global Sourcing Giants! India India – HI-Tech Industry India Multinational Companies * Partial List India MNC’s – A part of Rural India India MNC’s – A part of Rural India India MNC’s – A part of Rural India India Consumerism in India - A brave new world Indian mangoes have hit US shelves( Walmart) Harley Davidson motor cycles cruising India’s roads India Consumerism in India – Grape Expectations $ 1 BN Industry 25- 30 % Growth in Consumption Estimated consumption to reach 14.7 MN litres by 2012 end Indian Wine Industry Forecast to 2012 India 900+ MN Mobile subscribers – Still Growing Estimated 10 MN potential new mobile phone buyers every month India Dabbawala’s - Management Skills 116 years old Business 5000 strong Semi-Literate work force 1,75,000 boxes delivered daily in a 3 hour period Achievements: - Six Sigma - ISO India 12th Plan – To Focus on All Inclusive Growth 50% - Private sector participation (11th Plan 36%) - Decade ago - 5% 12th Five year Investment plan Total – $1025 BN ($ 514 BN 11th Plan) 2011-12 2012-13 2013-14 2014-15 2015-16 2016-17 132 155 178 202 230 260 India Doing Business in India India Doing Business in India The question for CEO’s the world over was not “ Should my company go to India?” But rather “Can my company afford not to be in India?” … On the economic front, it is clearly opportunity INDIA Mr. Kamal Nath Former Minister of Commerce & Industry Government of India India Challenges India Challenges Infrastructure bottlenecks – Logistics Local customs and habits / Religious beliefs Analysis of skilled Manpower Pent up Demand Capital vs Labor Prerequisites for Success Preparation and Planning Prerequisites for Success Preparation and Planning Feasibility / Research prior Launch Work with specialists / Outsource Choose the right Markets/Partners Bureaucracy / Policy matters Family Business (Ties) Cricket vs. Baseball Hollywood vs. Bollywood Prerequisites for Success Preparation and Planning Joint Ventures & Acquisitions ? Board of Directors Tax / Statutory Obligations - Manage but do not fall for Avoidance Technology Effective communication Patience (Long-term view) Some Tips Do’s Be Global as well as Indian to succeed Special Pricing for Indian market Research, Assessment - Understand the Market Study Logistics … and supply chain, delivery system HR Policies to meet local environment Some Tips Don'ts Try to do too much too early Take short term positions in the market Interfere with local Management Practices Politicize the organization Take Consumer for Granted - Threat or Opportunity THANK YOU Captain. Somesh Batra someshbatra@seahorsegroup.co.in someshbatra@yml.in