Capital Budgeting -Topics Short-run decisions Vs. Capital budgeting

advertisement

Course Name: Advanced Management Accounting

MA2

Module: 4

Module Title: Capital Budgeting

Lectures and handouts by:

Paul Jeyakumar, M.Sc., CGA

1

Capital Budgeting -Topics

Urgency method

Qualitative method

Payback method

Accounting rate of return method

Net present value method

Internal rate of return method

Performance evaluation

Assignment review

2

Short-run decisions Vs. Capital

budgeting decisions –

Major difference

Capital budgeting decisions have

significant financial effects beyond the

current year.

The long-term nature of the investments

adds new factors to our considerations.

3

1

Short-run decisions Vs. Capital

budgeting decisions –

Similarities

In both situations, we should have a good

understanding of the:

decision criteria

available alternatives

relevant qualitative and quantitative factors

decision model

4

3 phases in capital budgeting

1. Identifying potential investments

2. Selecting the investments

3. Follow-up monitoring or post-auditing the

investments

5

Long-term orientation – Factors to

consider

The first factor:

Time value of money is a factor for

consideration.

6

2

Long-term orientation – Factors to

consider (contd.)

The first factor:

Time value of money is a factor for

consideration.

The second factor:

All capital outlays involve risk and

uncertainty.

7

Course theme 1

In the identification and selection phases,

we emphasize the planning use of

accounting information.

In the post-auditing phase, we emphasize

the control use of accounting information.

8

Course theme 2

NPV and IRR models use cash basis of

accounting.

ARR model uses accrual basis of

accounting.

9

3

Course themes 3 & 4

In capital budgeting we have a long-term

orientation.

The advanced approaches to capital

budgeting consider true economic costs.

10

Models

Discounted cash flow model (NPV & IRR)

Payback model

Accounting rate of return model

11

Survey of 133 companies

Discounted cash flow methods were used in

more than 75% of the firms.

IRR was used more frequently than NPV.

ARR had an usage rate of about 20%.

More than 50% used the payback method

either alone or along with other techniques.

12

4

Qualitative factors

In the evaluation criteria, we should also

include qualitative factors.

13

Equivalent cash flow approach

The time value of money is ignored.

4 methods:

Urgency method

Qualitative method

Accounting rate of return method

Payback method

14

Multiple choice question

All the following methods can be used to

make capital budgeting decisions. Which

method does not belong to the category of

equivalent cash flow methods?

1) The accounting rate of return method

2) The internal rate of return method

3) The payback method

4) The qualitative method

Answer 2

15

5

Urgency method

Uses the emergency persuasion technique

Projects are selected because of the

persuasion skills of certain individuals

16

Qualitative method

The qualitative method is used when

organizations make decisions for reasons

other than dollar returns.

17

Payback method

Payback period:

It is the time taken to recoup, in the form of

cash inflows from operations, the initial

dollars of outlay.

Selection criterion:

If the payback period is within the required

time limit, accept the investment.

18

6

Payback – Weaknesses &

Strengths

Weaknesses:

Does not measure profitability

A project with a shorter payback time

may not be the preferable one

Ignores the time value of money

Strengths:

Provides a rough estimate of risk

Involves simpler computations

19

Payback – Even cash flows No income tax implications

Payback period = (net investment)/(annual

net cash flow)

Data:

Net investment is $20,000 and the annual net

cash inflow generated from the investment

is $4,800

Payback period =$20,000/$4,800= 4.167 years

20

Payback – Even cash flows - Income

tax implications - Handout question 1

Cash flow = change in earnings after tax +

change in non-cash expenses

Amortization = $18,000/4= $4,500/year

Earnings before tax & amortn $5,000

Less: Amortization exp

(4,500)

Earnings before tax

500

Less: Tax (40%)

( 200)

Earnings after tax

300

21

7

Payback – Even cash flows

Income tax implications (contd.)

Cash flow = change in earnings after tax + change in

non-cash expenses

Earnings before tax & amortization

Less: Amortization exp

Earnings before tax

Less: Tax (40%)

Earnings after tax

Earnings after tax

Plus: Non-cash amortization

Cash flow

$5,000

(4,500)

500

( 200)

300

$ 300

4,500

$ 4,800

22

Payback – Even cash flows

Income tax implications (contd.)

Cash flow = change in earnings after tax + change in

non-cash expenses

Earnings before tax & amortization

$5,000

Less: Amortization exp

(4,500)

Earnings before tax

500

Less: Tax (40%)

( 200)

Earnings after tax

300

Plus: Non-cash amortization

4,500

Cash flow

$4,800

Payback period =$18,000/$4,800 = 3.75 years

23

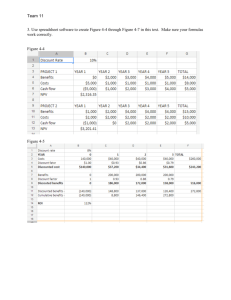

Payback – Uneven cash flows No income tax implications

Data: Investment: $90,000 Useful life: 4 years

Cash flows for the 4 years:

1: $50,000 2: $30,000 3: $15,000 4: $10,000

Year Cash flow Expenditure – Cum cash flow

0

$(90,000)

1

$50,000

(40,000)

2

30,000

(10,000)

3

15,000

5,000

4

10,000

15,000

Payback period = 2 + 10,000/15,000 =2.67 years

24

8

Payback – Uneven cash flows

No tax implications- Handout question 2

Year Cash flow Expenditure – Cum cash flow

0

$(330,000)

1

$100,000

(230,000)

2

150,000

(80,000)

3

210,000

130,000

Payback = 2 + 80,000/210,000 = 2.38 years

25

Payback – Uneven cash flows

Tax implications- Question 3a

Yr 1

Revenues

300.00

Op exp

(100.00)

Amortizn

(165.00)

Inc bef tax

35.00

Tax (35%)

(12.25)

Net inc

22.75

Add: Amtz

165.00

WC increase (50.00)

WC release

Salvage

__

Cash flow

137.75

Yr 2

Yr 3

26

Payback – Uneven cash flows

Tax implications- Question 3a

Yr 1

Revenues

300.00

Op exp

(100.00)

Amortizn

(165.00)

Inc bef tax

35.00

Tax (35%)

(12.25)

Net inc

22.75

Add: Amtz

165.00

WC increase (50.00)

WC release

Salvage

__

Cash flow

137.75

Yr 2

400.00

(100.00)

(165.00)

135.00

(47.25)

87.75

165.00

Yr 3

252.75

27

9

Payback – Uneven cash flows

Tax implications- Question 3a

Yr 1

Revenues

300.00

Op exp

(100.00)

Amortizn

(165.00)

Inc bef tax

35.00

Tax (35%)

(12.25)

Net inc

22.75

Add: Amtz

165.00

WC increase (50.00)

WC release

Salvage

__

Cash flow

137.75

Yr 2

400.00

(100.00)

(165.00)

135.00

(47.25)

87.75

165.00

Yr 3

500.00

(100.00)

(165.00)

235.00

(82.25)

152.75

165.00

252.75

317.75

28

Payback – Uneven cash flows

Tax implications- Question 3a

Yr 1

Revenues

300.00

Op exp

(100.00)

Amortizn

(165.00)

Inc bef tax

35.00

Tax (35%)

(12.25)

Net inc

22.75

Add: Amtz

165.00

WC increase (50.00)

WC release

Salvage

__

Cash flow

137.75

Yr 2

400.00

(100.00)

(165.00)

135.00

(47.25)

87.75

165.00

252.75

Yr 3

Yr 4

500.00

600.00

(100.00) (100.00)

(165.00) (165.00)

235.00

335.00

(82.25) (117.25)

152.75

217.75

165.00

165.00

317.75

50.00

140.00

572.75

29

Payback – Uneven cash flows

Tax implications- Question 3b

Capital cost allowance computation

Year

0

1

2

CCA

$800 x 0.30 x 0.5 = $120

$680 x 0.3 = $204

UCC

$800

$680

$476

30

10

Payback – Uneven cash flows

Tax implications- Question 3b

Revenues

Op exp

CCA

Taxable income

Tax (35%)

Earnings after-tax

Add: CCA

WC increase

Cash flow

Year 1

$ 300.00

(100.00)

(120.00)

80.00

(28.00)

52.00

120.00

(50.00)

Year 2

$400.00

(100.00)

(204.00)

96.00

(33.60)

62.40

204.00

$122.00

$266.40

31

Payback – Uneven cash flows

Tax implications- Question 3b

Year 1 Year 2

After-tax operating cash flow:

($300 - $100) x (1 – 0.35)

$130.00

($400 - $100) x (1 – 0.35)

$195.00

Add: CCA tax shield

$120 x 0.35

42.00

$204 x 0.35

71.40

Increase in working capital

(50.00)

Cash flow

$122.00 $266.40

32

Question 4- Initial Investment

Cost of new equipment

Installation costs

Sale of old equipment

Total initial investment

$9,600,000

147,000

( 23,000)

$9,724,000

33

11

Question 4 – Cash flows – Years 1 - 7

Income before income taxes and amortization

[52,500 units × ($349.95 – $320.00)] +

[50,000 units × ($325.00 – $320.00)]

$ 1,822,375

Amortization expense

($9,600,000 + $147,000 – $37,850) / 10

(970,915)

Income before taxes

851,460

Less: Income taxes (40%)

(340,584)

Net income

510,876

Plus: Non cash expenses

970,915

Annual net cash flow, years 1 to 7

$ 1,481,791

34

Question 4 – Payback in 7 years

Initial investment

Cash flows Years 1 to 7:

$1,481,791 x 7

$9,724,000

$10,372,537

Accept the proposal.

35

Accounting rate of return

If ARR is greater than the minimum target

rate, the investment proposal is accepted.

Method 1:

ARR = (Average increase in annual net

income) / (Net original investment outlay)

36

12

Accounting rate of return (contd.)

Method 2:

ARR = (Average increase in annual net

income) / (Average investment)

where

Average investment = (original investment +

salvage) / 2

37

ARR – Strength/weakness

Strength:

It is a profitability measure.

Weakness:

It ignores the time value of money.

38

ARR – Handout question 5

Initial investment

Useful life

Incremental revenues/year

Incremental before-tax

expenses per year

Minimum target ARR

Average investment method

$16,000

3 years

$20,000

$12,000

15%

39

13

ARR – Handout question 5 (contd.)

Yr

1 ($20,000–$16,000) × (1–0.5) =

2 ($20,000–$16,000) × (1–0.5) =

3 ($20,000–$16,000) × (1–0.5) =

Total

Net profit

$2,000

$2,000

$2,000

$6,000

Average increase in Accounting income =

$6,000/3 = $2,000

Average investment = $(30,000+0)/2 = $15,000

ARR = $2,000/ $15,000 = 13.33%

40

Net Present Value (NPV)

NPV calculations are based on cash flows.

The present value is computed using the

cost of capital, which is the minimum

acceptable rate of return.

41

Present value – Simple example

What amount should be invested now to

accumulate $5,000 in 3 years if the expected

interest rate is 8% compounded semiannually?

PV = $5,000 × (1.04)–6

PV = $3,952

OR, PV = $5,000 × 0.7903 = $3,952

42

14

NPV – Important points

Cost of capital is used as the assumed

interest rate.

Cost of capital is the minimum acceptable

rate of return.

For CCA, the half-year rule is applied.

43

NPV – Important points (contd.)

If you sell an asset, the basis on which you

calculate the tax savings goes down.

If there is only one item in the pool, the new

basis = 0.

If there is more than one item in the pool, the

new basis = old basis – salvage.

44

NPV – Important points (contd.)

Present value of tax shield

= {[(cdt)/(d+i)] x [(1+0.5i)/(1+i)]} – {[(sdt)/(d+i)

x [1/(1+i)^n]}

where

c = cost of the asset (will be discussed)

d = CCA rate t = tax rate i = cost of capital

s = salvage value

n = number of periods

45

15

NPV – Initial investment – Handout

question 6 – part a

The market price of the old asset reduces

the investment cost to $92,000 ($100,000 $8,000).

Installation costs qualify as capital

expenditures. So the investment cost is

$92,000 + $12,000 = $104,000.

The value for ‘c’ is $104,000.

46

NPV – Initial investment – Handout

question 6 – part b

The training costs are not capitalized.

Training expenses are tax deductible.

Recorded as $7,000 x (1 – 0.4) = $4,200.

47

NPV – Initial investment – Handout

question 6 – part b

• Cash balance has no tax implication

• Shown as an outflow of $10,000 at the time

of investment

At the end of 5 years, $10,000 would be

considered as a cash inflow. So PV

computation is necessary.

48

16

NPV – Initial investment – Handout

question 6 – part c

The $5,000 salvage value is considered as

cash inflow at the end of 5 years.

We compute the present value of this cash

flow using cost of capital.

We also compute the present value of the

tax shield lost.

49

Comparison of alternatives

2 NPV approaches

Total project approach:

Compares alternatives by computing their

NPVs. The alternative with the largest NPV

of cash flows is preferred.

The differential approach:

Compares by computing the differences in

cash flows and then converting these

differences to their present values.

50

NPV – Handout question 7 – part a

After-tax cash inflows = $180,000(1 – 0.4) =

$108,000

We use 15 years and a discount rate of 12%.

The factor for this ordinary annuity is 6.8109

Present value of cash inflows:

= $108,000 x 6.8109

= $735,577

51

17

NPV – Handout question 7 – part b

The training costs are not capital

expenditures. So they are not included in

the value of ‘c’.

There is no salvage value.

Present value of CCA tax saving:

[(800,000x0.40x0.10)/(0.10+0.12)] x

{[(1+0.5(0.12)]/(1+0.12)}

= $137,662

52

NPV – Handout question 8

Initial investment

$(9,724,000)

53

NPV – Handout question 8

Initial investment

PV of cash inflows: Years 1 – 7:

PV of cash inflows: Years 8 – 10

$(9,724,000)

4,549,085

564,251

54

18

NPV – Handout question 8

Initial investment

$(9,724,000)

PV of cash inflows: Years 1 – 7:

4,549,085

PV of cash inflows: Years 8 – 10

564,251

PV of tax shield:

2,077,674

Present value of lost tax shield:

(2,139)

PV of salv value: $37,850 × (1.15)-10

9,357

Net present value of the project $(2,525,772)

55

NPV – Handout question 9

Investment

Cost of the new sewing machine $2,500,000

Less: Market value of old machine (260,000)

Investment as ‘c’ value

$2,240,000

Training costs $85,000 × (1 – 0.4)

51,000

Net investment

$2,291,000

Now review the handout solution for the rest.

56

Internal Rate of Return - IRR

IRR is the interest rate that makes the net

present value of the investment equals to

zero.

If the IRR is equal to or greater than the

minimum desired rate, accept the project.

We may have to use trial and error method

to determine the IRR. Review course notes

for an illustration.

57

19

IRR – Multiple choice question

What is internal rate of return?

1) The accounting rate of return

2) The cost of capital

3) An equivalent cash flow method to

make a capital budgeting decision

4) The discount rate at which the net present

value of the cash flows equals zero

Answer: 4

58

IRR – Handout question 10

NPV (if cost of capital rate is 15%) =

–$5,000 + ($3,000 × 1.15–1 ) + ($2,000 × 1.15–2 ) +

($2,000 × 1.15–3 ) = $436

NPV (if cost of capital rate is 20%) =

–$5,000 + ($3,000 × 1.20–1 ) + ($2,000 × 1.20–2 ) +

($2,000 × 1.20–3 ) = $46

The IRR is approximately 20%.

59

IRR – Handout question 11

Net cash flows = $800 + (500,000 donuts ×

$0.05/donut) = $25,800

If i = 8%, NPV = –$90,000 + ($25,800 × 3.3121)

+ ($6,000 × 0.7350) = –$138

The IRR should be below 8%. The only

possible answer is 7.9%.

60

20

IRR & NPV Assumptions

We assume certainty. We assume that the

predicted cash flows are certain to occur at

the times specified.

We also assume perfect markets. We

assume that we can borrow or lend money

at the same interest rate. This is our

minimum desired rate of return for the NPV

method, and the internal rate of return for

the IRR method.

61

Performance Evaluation Conflict

Discounted cash flow models use cash

flows over a long-term.

Managers are often evaluated on the basis

of accrual income usually over a short

period.

62

Performance Evaluation Conflict

(contd.)

Use the same model for the decision and for

measuring performance.

63

21

Performance Evaluation Conflict

(contd.)

Use the same model for the decision and for

measuring performance.

Perform a post audit.

64

Performance Evaluation Conflict

(contd.)

Use the same model for the decision and for

measuring performance.

Perform a post audit.

Use multiple criteria (such as the balanced

scorecard) to evaluate the performance of

managers.

65

Ethics

Consider professional ethics, business

ethics in general, and personal ethics.

Consider ethics in the areas of

confidentiality, integrity, competence and

objectivity.

66

22

Assignment Question 1 – Part A

(i) NPV = $9,704

(ii) Payback period = 3.13 years

67

Assignment Question 1 – Part A

(iii)

At 19%, total present value = $90,600

At 20%, total present value = $88,536

Discount rate

At 19%

True Value

At 20%

Difference

Total Present Value

$90,600

$90,600

$90,000

$88,536

__

$ 2,064

$ 600

IRR = 19% + (600/2,064) x 1% = 19.29%

68

Assignment Question 1 – Part B

(i) Net present value = $11,944

(ii)

Net present value = $239

(iii) Payback period = 3.24 years

69

23

Assignment Question 1 – Part B

(iv)

Discuss the effect of the payback period

requirement on the long-term perspective

of the business.

70

Assignment Question 2

Multiple choice question!

No check figures are provided.

71

Assignment Question 3 – Part a

Cost to buy:

$40 per unit x 40,000 units = $1,600,000

Cost to make:

$17.60 x 40,000 = $704,000

Annual savings = $896,000

Net present value = $352,316

72

24

Assignment Question 3 – Part b

List qualitative factors.

73

Assignment Question 4

Investment = $220,000

Before-tax operating profit/per year= $40,000

Tax rate = 18%

CCA = 12%

Useful life = 10 years

Cost of capital = 14%

Net present value = $(27,048)

74

Assignment Question 5 – Part a

Investment = $336,000

Trade-in = $10,000

Increase in working capital at the time of

investment = $50,000 x 0.5 = $25,000

Cost savings/year = $100,000

Release of working capital: Year 5 = $25,000

Salvage on equipment = $50,000

NPV = -$485

75

25

Assignment Question 5 – Part b

Provide comments and suggestions, and

describe the concerns of the senior

management.

76

26