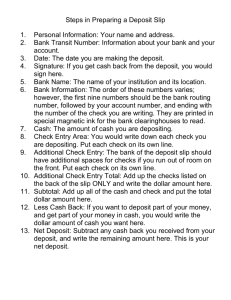

Rules and Regulations For Deposit Accounts

advertisement