AP MACRO - Unit 1 Notes

advertisement

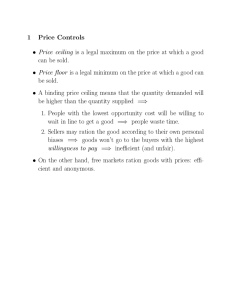

AP Macroeconomics – UNIT 1 Basic Economic Concepts What is economics? • A social science that studies how resources are used (often concerned with how they are used to their full potential). Macroeconomics • involves economic problems encountered by the nation as a whole. Macroeconomic Concepts: • Do we spend too many of our resources on national defense and not enough on education? • • • If households are required to pay fewer taxes, will national savings be affected? Will prices rise or fall because of a tax cut? Will increasing the money supply increase production levels in the economy? Microeconomics • concerned with economic problems faced by individual units within the overall economy. (particular families, individuals and firms) Microeconomic Concepts: • • • Does a particular family save enough to provide for its future needs? How will a tax break affect XYZ Corporation’s output? If the Smith’s win the lottery, how will their spending patterns change? Resources • Resources are anything that can be used to produce a good or a service. • LAND (natural) • LABOR (human attributes) • CAPITAL (productive equipment or machinery) Scarcity • Unlimited Wants > Limited Resources Opportunity Costs • • What must be sacrificed to obtain something. The amount of one good that must be sacrificed to obtain an alternative good. Opp. Cost of Good X = Change in Good Y production Change in Good X production Production Possibilities Frontier • • PPFs; also known as PPCs The combination of two goods that can be produced if the economy uses all of its resources fully & efficiently. Economic Systems & Circular Flow The Three Basic Economic Questions 1. What to Produce? • Deals with opportunity costs; what will be sacrificed in order to make more of something else 2. How to Produce? • By what means is production going to take place? Mechanized labor or human labor? 3. For Whom to Produce? • Allocation. How are the products to be distributed? Society’s Economic Goals • • • • • • • • Economic Growth Full Employment Economic Efficiency Price-level Stability Economic Freedom Equitable Distribution of Income Economic Security Balance of Trade Principal Types of Economic Systems • • • • Traditional Economies Command Economies - Centrally Directed Economies Market Economies Mixed Economies Traditional Economies • The basic questions of what, how and for whom to produce are resolved primarily by custom or tradition. • Things are done the way they have always been done. • Prominent in non-industrial (less developed) countries. • Examples include some areas of Africa. Command Economies • • • • Government owns most or all of the resources. Central planning is responsible for decision making. Type of government is usually socialism or communism. North Korea and Cuba are the last remaining examples of largely centrally planned economies. Market Economies • Economic system in which the basic questions of what, how, and for whom to produce are resolved primarily by buyers and sellers interacting in markets. • In other words, supply and demand answer the three basic economic questions. • Everyone acts in their own self interests. • Individuals and business seek to maximize its satisfaction or profit through its own decision regarding consumption or production. • United States is an example. Mixed Economies • An economic system in which the basic questions of what, how, and for whom to produce are resolved by a mixture of market forces with governmental direction and/or custom and tradition. • China tends to be more of a command economy, but has some private ownership. • United States tends to be more of a market economy, but the government has some restrictions. Markets • Any institution or mechanism that brings together buyers (demanders), and sellers (suppliers) of a particular good or service. Product & Factor Markets • Product Market – A market in which finished goods and services are exchanged. – Buyers are individuals and households. – Households consist of individuals or a family. • Factor Market – A market in which resources and semi-finished products are exchanged. – The buyers are businesses. Circular Flow Model • The flow of resources from households to firms and of products from firms to households. These flows are accompanied by reverse flows of money from firms to households and from households to firms. Supply & Demand Markets • A market is an institution or mechanism that brings together buyers (“demanders”) and sellers (“suppliers”) of particular goods, services, or resources. Markets Exist in Many Forms • Stores • Internet • Telephone • Door to Door Salesmen • Stock Exchanges • Labor Markets Any situation that links potential buyers with potential sellers. Price • Price can act as both an: • ENCOURAGEMENT • DISCOURAGEMENT • • • Price can be an obstacle. The higher the obstacle, the less of the product that will be bought. “Sales” at stores is evidence of this. Forces That Determine Price • Demand • The buyer’s side of the market • Supply • The seller’s side of the market DEMAND • The quantities of a particular good or service consumers are willing and able to buy at different possible prices at a particular time. • Generally, the higher the price the less consumers will buy of an item, AND the lower the price, the more consumers will buy. Demand Schedule Law of Demand • All else being equal, as price falls, the quantity demanded rises, and as price rises, the quantity demanded falls. • Consumers will generally buy less of an item at higher prices than they do at lower prices. • This is a inverse relationship Why is it an inverse relationship? • Common Sense Consumers will generally buy less of an item at higher prices than they do at lower prices. • Diminishing Marginal Utility • Each buyer of a product will derive less satisfaction (or benefit) from each successive unit of the product consumed. • The Income Effect • Low prices increases the purchasing power of a buyer’s money income, and vice versa. A higher price will force consumers to substitute items for that product. • Determinants of Demand 1.Expectations (Tastes & Preferences) 2.Income 3.Substitutes and Compliments 4.Population (Number of Buyers) These are often referred to as price shifters. Expectations • • • Also known as tastes & preferences. Change in styles, tastes, and habits. Diminishing Marginal Utility Example: CDs have greatly decreased the demand for cassette tapes. Income • • • Desire must be backed up by the ability to pay. Increases in income allows people to purchase more of some commodities. Commodities (steaks, sunscreen, stereos, etc.) whose demand varies directly with income are called normal goods. Substitutes & Compliments • A substitute good is one that can be used in place of another good. Ex. Nikes & Reboks, Sweaters & Jackets, Toyotas & Hondas, Coke & Pepsi • A complimentary good is one used together with another good. Ex. Ham & Eggs, Tuition & Textbooks, Movies & Popcorn, Cameras & Film, TVs & VCRs, CDs & CD Players Population (Number of Buyers) • • An increase in the number of consumers in a market increases demand. A decrease in the number of consumers in a market decreases demand. Changes in Quantity Demanded • A change in demand must not be confused with a change in quantity demanded. • • Change in Demand is a shift of demand curve. Change in Quantity Demanded is a movement from one point to another point on the demand curve. Supply • The amount or quantity of goods and services that producers are willing and able to provide at various prices. • • • • Producers want to sell more at higher prices than at lower prices. The influence of market prices on the amount supplied is the price effect. There are opportunity costs whenever goods and services are produced. The cost of each additional item or service is the marginal cost. Supply Schedule Law of Supply • The higher the price, the more producers will supply; and at the lower price they will supply less. • Producers must receive a price for their goods and services that will cover their costs and provide a profit in order to stay in business. Determinants of Supply 1.Technology 2.Price of Inputs 3.Taxes & Subsidies 4.Price of Related Goods 5.Population: Number of Sellers Determinants of Supply are Line Shifters. Technology • Advances in technology make it easier to make more. The marginal cost of making more of something is reduced. • • Marginal Cost = the added cost of producing one more unit of output. As a rule, as COSTS decrease, SUPPLY increases. Price of Inputs • Land, labor, and capital Materials from nature. Wages. Man-made materials. • • As COSTS increase, SUPPLY decreases. As COSTS decrease, SUPPLY increases. Taxes & Subsidies • A tax (or tariff) is an extra cost added to the cost of a good or service. • A subsidy is when someone (usually the government) pays someone to produce something; they provide an incentive to produce more. • The government approach is if they want more of something, they subsidize, and if they want less they impose a tax. Price of Related Goods • • An opportunity cost; a choice is made in what to produce. An example: What should the farmer grow? Corn or Beans? Which ever he can make the most money on. Population: Number of Sellers • • More sellers equals greater supply. Fewer sellers equals less supply. What are the barriers of entry? How easy is entry into the market? Changes in Quantity Supplied • • Change in Supply means a change in the schedule and a shift in the curve. Change in quantity supplied is a movement from one point to another on a fixed supply curve. Market-Clearing Price • The price that balances the amount buyers want to buy with the amount sellers want to sell. • Also known as Market Equilibrium. • Point where buyers and sellers meet. Shortage • How much more of a product buyers want to buy than sellers want to sell at a given price. • You need to be able to recognize a graph that depicts this. • How much more of a product sellers want to sell than buyers want to buy at a given price. • You need to be able to recognize a graph that depicts this. Surplus