Kohl – Megatrends

advertisement

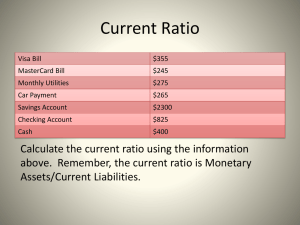

GLOBAL E CONOMICS & T RENDS: P OSITIONING FOR S UCCESS Dr. David M. Kohl Professor Emeritus, Agricultural and Applied Economics Virginia Tech, Blacksburg, VA (540) 961-2094 (Alicia Morris) | (540) 719-0752 (Angela Meadows) | sullylab@vt.edu Macro Clinic Video Blog: http://agstar.com/edge/ January 12, 2015 Road Warrior of Agriculture: www.cornandsoybeandigest.com Ag Globe Trotter: www.northwestfcs.com Dave’s GPS & Dashboard Indicators: www.farmermac.com Super Cycle I (4 Years) WWI global need for production mechanical industrial revolution farm & city movement 2 Super Cycle II (4 Years) post WWII- restructure infrastructure war technology applied to farming and manufacturing- Cold War peak of industrial, mechanical resolution acceleration of farm & city movement increasing standard of living 3 Super Cycle III (3 Years) inflation commodity cycle unrest in commodity producing regions Russian wheat deal growing world population increasing standard of living 4 Super Cycle IV (10 Years) ethanol & biofuels low interest rates emerging nations need for commodities growing world population increasing standard of living 5 2016 – 2020 Economic Reset 1 BRICS & KIMT’s – 53% world economic growth growth moderating 8-5-3 Rule China does matter to fly over states 2007 to 2012 aberration in commodity prices one half of emerging nations in recession 6 World Economic Outlook: Real GDP Growth 2000-2015 emerging market and developing economies world advanced economies Source: IMF World Economic Outlook (October 2015) http://www.imf.org/external/datamapper/index.php 7 2016 – 2020 Economic Reset 2 ethanol & biofuels oil black gold “recession effect” deflation in commodities regulatory issues in developed countries political dysfunction technology, automation demographics 8 2016 – 2020 Economic Reset 3 40% of commodity prices & asset values U.S. Central Bank reducing stimulus European Central Bank increasing stimulus 60 billion plus 21 months Japan’s stimulus China’s Central Bank stimulus stock market appreciation beneficial to fly over states/Canada/Australia, etc. 9 2016 – 2020 Economic Reset 4 weather wild card political military sanctions quality & standards risk consumers & public “Black Swans” 10 Grain Industry- Reset easy money 2007-2012 has been made top notch managers adjust high overhead/fixed cost structure classic tail effect prices go down costs lag cycle duration 11 Grain Producers: “Houston, We Have a Problem” Super Cycle Observation Constant 2014 Dollars Median Net Income 2007-2012 $169,968 2002-2006 $66,574 Super Cycle 2.42 x’s greater 2013-2014 $32,944 2000-2001 $40,123 • Lost 40% working capital in two years • Greater 60% Debt to Asset Ratios under 10% working capital • Operators under age of 30 - 24 to 15% working capital • Most leveraged farms- negative working capital • Debt coverage ratio is 45% 12 Livestock Industry strategic resource shift grain industry economic Vortex 50 to 65 year olds will not return 1953/73/78 cycle duration curve ball effect 13 Horticulture, Vegetable, & Retail/Entrepreneurial growth of the economy housing starts lower unemployment growth of local, natural, and organic population dynamics 14 Global Economics: Europe France economy sluggish Germany- export driven Europe China connection Greece central bank stimulus extended Ukraine 15 Global Economics: China China PMI <50 exports down >10% lowered rates five times stock market up 105%, down 30 to 40% devalued currency natural resource issues shadow banking 16 Global Economics: Other Russia oil Mr. Putin Brazil recession Infrastructure Argentina tax political dysfunction Brazil & China connection 17 Global Economics: Japan/Asia debt issues demographic wedge South Korea sluggish India quite strong 18 U.S. Economy Watch LEI declining PMI slowing manufacturing, building inventory housing 1.2 million business cycle expansion later innings 19 Federal Reserve’s Interest Rate Barometer Indicator Possible Change Definite Change Current Status Unemployment 7.0% 6.5% 5.0% GDP Growth 2.0% 2.5% 1.5% Core Inflation 2.0% 2.5% 1.9% Headline Inflation 4.0% 5.0% 0.0% Watch List: • Dr. Yellen • Rail traffic • Overland trucking • FOMC voting • Shoe shiners • Baltic Sea index • FOMC minutes • Copper prices 20 Nine Innings of an Evolution of a Cycle Reset 1. profits start to decline but asset appreciation continues 2. new lenders enter the market place 3. strong equity growth mentality creates complacency 4. machinery & equipment values first to decline 5. aggressive growth businesses & fraudulent activities occur 6. margin negative cash flow & operating lines of credit become an issue 7. marginal assets discounted 8. non-traditional & new lenders retreat 9. quality assets adjust in value depending upon length of adjustment 21 Ten Mega Trends Impacting Agriculture 22 Global Economy geopolitical trade risk volatility in revenues and cost agriculture’s movement to emerging nations opportunity failure premium on planning, execution, and monitoring “Think globally but act locally.” 23 Technology convergence of technology bio tech engineering information/big data high levels of talent innovation vs. technology systems “High tech, high touch.” 24 Consumers local, natural, & organic GMO/non-GMO ethnic groups global consumers consumer trends 2025 “Consumers will drive the business model.” 25 Potpourri Trends 2050 - 70% of the world’s population will be urban 85% of Americans are 2 generations away from farm/ranch animal welfare environmental black swans “Expect the unexpected.” 26 Rural Communities The characteristics of thriving communities are: healthcare & preventive health internet access Infrastructure education lifestyle amenities such as shopping & recreation “Rural communities will define your business/people strategy.” 27 Education/Lifelong Learning internships experienced education knowledge centers, blended education vocational schools emotional intelligence – 4-H, FFA, rural leadership groups First job Baby Boomers = age 12; Millennials = age 22 “750 universities and colleges will file bankruptcy by 2025??” 28 New Wave of Players under 42 years of age age wave is world wide women minorities lifelong learners new entrants “Hire for attitude, train for aptitude.” 29 Natural Resource/Environment water quality & quantity quality land is premium extreme in weather around the globe moisture temperature other energy infrastructure 30 Transition & Evolution 60% of U.S. farm ground will change hands by 2030 independent vs. interdependent lending: banks, Farm Credit, FSA agribusiness family and business dynamics “Heart vs. head concept.” 31 Global Economic / Government Policy China 2030 debt issues worldwide tax laws new leadership other “You can only imagine!” 32 Strategic 2025 1 CEO/ leaders will be “visionary/champions” vs. “gate keepers” “big enough to serve but small enough to care” alignment & collaboration- agribusiness, education & lenders technology strategy- value added, big data refinement of processes- collaboration, training, & execution human resources- talent alignment, culture, recruit, & retain 33 Strategic 2025 2 knowledge, intellectual research, information Global, domestic, industry, region, & local capital, liquidity, profitability, & efficiency public policy, public regulatory voice education- internal & external- “life long learners” natural resources- demographic, drive your model transition- evolution of customers, association, footprint- corporate vs. family 34 20/20 Foresight building perceptual acuity cultivate perspectives listening for risk & opportunity change what’s new inside & outside the industry watch, read, & repeat examples of success 35 P OSITIONING YOUR B USINESS FOR S UCCESS IN THE R ESET Dr. David M. Kohl Professor Emeritus, Agricultural and Applied Economics Virginia Tech, Blacksburg, VA (540) 961-2094 (Alicia Morris) | (540) 719-0752 (Angela Meadows) | sullylab@vt.edu Macro Clinic Video Blog: http://agstar.com/edge/ January 12, 2015 Road Warrior of Agriculture: www.cornandsoybeandigest.com Ag Globe Trotter: www.northwestfcs.com Dave’s GPS & Dashboard Indicators: www.farmermac.com Business Equation for Success P=O+C+L+M² P=people, profits, & plans O=overhead cost control C=costs- know thy cost L=liquidity-cash is king M²=marketing & management = margin 2 Positioning for the Reset family living cost- business & personal machinery & equipment investment crop cost $100 to $150 per acre “15% to 30%” reduction of human assets “uncle example” earns & turns – “margin/capital turnover” 3 The Five “P” Evaluation of Successful Business Planners(1) Rate the following statements regarding business planners. 1-Strongly Disagree, 2- Disagree, 3-Neither Agree or Disagree, 4-Agree, 5- Strongly Agree Evaluation Points: Rating Paradigm: Conversations center around profitability instead of production, operations Receptive to new technology & ideas High priority on education & training for new ideas View people inside & outside of business as important resources _____ _____ _____ _____ People: Employees & suppliers trust & respect them Employees & management are given opportunity to grow Employees & suppliers enjoy working with this business Low employee & management turnover Planner: Utilize a business mission statement & core values Use tactical plans to achieve written business goals Use record systems (financial, production) to monitor & evaluate performance Could leave their business for a week/month & things would run smoothly _____ _____ _____ _____ _____ _____ _____ _____ 4 The Five “P” Evaluation of Successful Business Planners(2) Rate the following statements regarding business planners. 1-Strongly Disagree, 2- Disagree, 3-Neither Agree or Disagree, 4-Agree, 5- Strongly Agree Evaluation Points: Rating Problem Solver: Identify problems in the business before they are obvious Seldom have the same problem reoccur in their business Solicit input from ag & non-ag sources when looking for solutions Take responsibility for their decisions _____ _____ _____ _____ Proactive: Can make a decision & accept consequences Productive & gets things done Complete tasks - multitaskers Complete tasks on schedule _____ _____ _____ _____ Scoring: 90-100 High Potential for Success 80-90 Above Average Potential for Success 70-80 Needs Management Assistance for Success <70 Probably will be around until the money runs out Total Score Source: Adapted & Revised from Southeastern Agricultural Lenders School _____ 5 Financial Dashboard Key Ratio Green Yellow Red Coverage Ratio >200% 125% to 200% <125% Working Capital/Revenue >33% 10% to 33% <10% Equity Percent >70% 40% to 70% <40% Term Debt/EBITDA <350% 350% to 600% >600% ROA- Return on Assets >6% 2% to 6% <1% 6 Screening Guide for Negative Margins 1 Historically has the producer/entity: Yes No Been profitable above interest rates and rate of inflation? Shown growth of balance sheet which is earned vs. appreciated net worth? Has built and protected working capital in positive cycle? Been able to cut living expenses if needed? Been able to sell unproductive assets? Followed and executed a marketing risk management program? Have the ability to cut 10 to 30% of costs? Producer Version 7 Screening Guide for Negative Margins 2 Historically has the producer/entity: Yes No Been able to shed unprofitable land, machinery, livestock, & human assets if necessary? Had a burn rate for working capital 2.5 years or more? Had a term debt/EBITDA ratio <5 to 1? Scoring Key: >8 Yes boxes checked= strong case for sustainability 5-8 Yes boxes checked= modest case for sustainability <5 Yes boxes checked= very questionable for sustainability Producer Version 8 Financial Characteristics that Thrive During Tough Times Characteristic: Yes No Working capital revenue above 33% Burn rate working capital to net income loss over 2.5 years Burn rate of working capital to annual debt service payments 3.0 years or greater Moderation in family living costs Debt coverage ratio above 125% 9 Liquidity, Liquidity, & Liquidity current ratio limitations lender speak/producer speak 25% of revenue to expenses top level producers- 40% bottom level producers- 10% Burn Rate: Working Capital Green 3.0 Years Yellow 1.0-3.0 Years Red 1.0 Year Payments 5.0 Years 2.5-5.0 Years <2.5 Years 10 The Burn Rate – Working Capital Revenue $2,000,000 Expenses 2,200,000 Loss $200,000 Current Assets $1,000,000 Current Liabilities 500,000 Net Working Capital $500,000 Net Working Capital $500,000= 2.5 Years Projected Loss $200,000 Green >3.0 Years Yellow 1.0-3.0 Years Red <1.0 Year 11 The Burn Rate – Debt Service Payments Revenue $2,000,000 Current Assets $1,000,000 Expenses 1,800,000 Current Liabilities 500,000 Profit $200,000 Net Working Capital $500,000 Debt Service Payments = $100,000 Net Working Capital $500,000= 5.0 Years Debt Service Payments $100,000 Green >5.0 Years Yellow 2.5-5.0 Years Red <2.5 Years 12 True Working Capital Analysis Assets Liabilities Scenario A (Base Hits- Sweat the Small Stuff) Months 0-4 mo. Current Asset Amount Cash $100,000 A/R $75,000 Inventory $350,000 Subtotal $525,000 5-8 mo. A/R $75,000 Inventory $350,000 Crops Growing $200,000 Subtotal $625,000 9-12 mo. Prepaid Expenses $500,000 Subtotal $500,000 Total Current Assets $1,650,000 Months 0-4 mo. 5-8 mo. Current Liability A/P Operating Line Payment Subtotal Payment Amount $100,000 $560,000 $50,000 $710,000 $50,000 Subtotal $50,000 9-12 mo. Payment $100,000 Subtotal $100,000 Total Current Liabilities $860,000 13 True Working Capital Analysis Calculations- Scenario A 1. Current Ratio= Current Assets Current Liabilities 2. Working Capital to Revenue WC=$1,650,000-$860,000 (Revenue= $2,000,000) $1,650,000 = $860,000 1.92 $790,000 = $2,000,000 39.5% 3. Burn Rate on Working Capital= (assuming $200,000 projected losses) $790,000 = 3.95 Years $200,000 4. Burn Rate on Debt Service Payments= (assuming $200,000 annual debt payment) $790,000 = 3.95 Years $200,000 5. Debt to Asset Ratio= = 60% 6. Return on Assets (ROA)- 3 Year Trend= = 8% 14 Key Financial Metrics Degree of Financial Leverage: Risk Mitigation Compensating Factors: Debt to Asset Ratio Term Debt/EBITDA Working Capital to Revenue or Expenses Coverage Ratio ROA / Cost <20% 6 to 1 >25% 125% 4% 21-50% 4 to 1 >25% 140% 6% 51-75% 2.5 to 1 >33% 150% 8% >75% <2.5 to 1 >40% 175% >10% 15 Problems You Want Your Business to Have (1) You pay income taxes. You can leave your business for a month & the business runs smoothly. Your lender seeks you for business. People want to work for your business. Your business has idle cash and liquid financial assets. You can fire your customers/suppliers. You leave money on the table in some deals. 16 Problems You Want Your Business to Have (2) You surround yourself with people smarter than you. You spend time networking and seeking education. You could send your son/daughter/assistant away for two years. You appear to be dissatisfied, not happy with status quo. You occasionally fail. 17 Ten Best Management Practices of Young Producers modesty in family living invest in productive assets personal/business independent vs. interdependent lifelong learners strong group of peers good set of mentors profit plan 60-30-10 get better before getting bigger balance between head/heart (numbers vs. passion) strong relationship with lender 18 Ten Compelling Reasons to Be Optimistic in Agriculture 1 50/70/70 Rule 1995-2013- Top 20% livestock/crop producers had 10% returns one size does not fit all young people, women, and minorities are the “new energy” innovation and technology bio, engineering & information 19 Ten Compelling Reasons to Be Optimistic in Agriculture 2 talent wars in agriculture and rural America 1 in 6 jobs in U.S. are directly or indirectly connected to agriculture retail, entrepreneurial segments emerging nations, BRICS & KIMT, think globally but act locally raising a family- value systems/living expenses 20