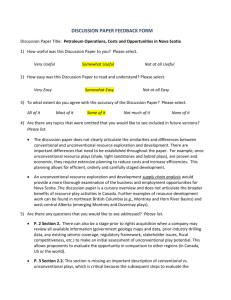

The Economic and Employment Contributions of Unconventional Gas Development in State Economies Prepared for: AMERICA'S NATURAL GAS ALLIANCE Submitted by: IHS Inc. 1150 Connecticut Avenue NW, Suite 401 Washington, DC 20036 June 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES About IHS (ihs.com) IHS Inc. (NYSE: IHS) is a leading source of information and insight in critical areas that shape today's business landscape, including energy and power; design and supply chain; defense, risk and security; environmental, health and safety, and sustainability; country and industry forecasting; and commodities, pricing and cost. IHS has been in business since 1959 and became a publicly traded company on the New York Stock Exchange in 2005. Headquartered in Englewood, Colorado, USA, IHS employs more than 5,100 people in more than 30 countries around the world. About IHS Global Insight IHS Global Insightis one of the leading economic analysis and forecasting firms in the world. With over 600 economists, statisticians, and industry specialists in 25 offices worldwide, IHS Global Insight has an established track record for providing rigorous, objective forecast analysis and data to governments and businesses around the world. Among our areas of expertise are the economic impact, tax implications, and job-creation dynamics within multiple sectors core to national, state and local economies. It helps governments and companies at all levels interpret the impact of proposed investments, policies, programs, and projects. IHS Global Insight was formed by the merger of DRI and WEFA. Still active in an advisory capacity to the firm is the original founder of WEFA, Lawrence R. Klein, the 1980 winner of the Nobel Prize in Economics. For more information, contact: Richard F. Fullenbaum Vice President, Public Sector, IHS Richard.Fullenbaum@ihs.com John W. Larson Vice President, Public Sector, IHS John.Larson@ihs.com For press information, contact: Jim Dorsey Senior Manager Media Relations, IHS Jim.Dorsey@ihs.com IHS 1150 Connecticut Avenue NW, Suite 401 Washington, DC 20036 © 2012 IHS. All information contained herein is obtained by IHS Inc. from sources believed by it to be accurate and reliable. All forecasts and predictions contained herein are believed by IHS, Inc. to be as accurate as the data and methodologies will allow. However, because of the possibilities of human and mechanical error, as well as other factors such as unforeseen and unforeseeable changes in political and economic circumstances beyond IHS's control, the information herein is provided "as is" without warranty of any kind and IHS Inc., AND ALL THIRD PARTY PROVIDERS MAKE NO REPRESENTATIONS OR WARRANTIES EXPRESS OR IMPLIED TO ANY SUBSCRIBER OR ANY OTHER PERSON OR ENTITY AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY OF THE INFORMATION OR FORECASTS CONTAINED HEREIN. ii JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Project Team Authors Mohsen Bonakdarpour, Director, Economic Analysis and Planning, IHS Consulting John W. Larson, Vice President, Public Sector, IHS Consulting Contributors Tabitha M. Bailey, Project Manager and Senior Associate, Public Sector, IHS Consulting Richard F. Fullenbaum, Special Advisor and Vice President, Public Sector, IHS Consulting Acknowledgments We would like to acknowledge IHS Cambridge Energy Research Associates (IHS CERA) on which we have relied for oil and gas expertise and analysis. For the data on oil and gas production, holdings, and reserves, we have used IHS CERA's extensive oil and gas databases. In particular, we want to thank Dr. Mary Barcella, Director and North American Natural Gas and team leader, IHS CERA; Samuel Andrus, Director, North American Natural Gas, IHS CERA; and James Osten, Director, North American Natural Gas, IHS CERA. We also would also like to thank the additional subject matter experts, technical experts, industry experts and analysts who have contributed to this study: Parker Andrews, John Anton, Rick Chamberlain, Laura Hand, Miguel Goncalves, Samantha Gross, Yanni He, Dewey Johnson, Rafael McDonald, Joe Michael, Michael Montgomery, Walter Moody, John Mothersole, Shane Norton, Sunaina Ocalan, Rajeevee Panditharatna, Frantz Price, Surya Rajan, Curtis Smith, Tom Runiewicz, Mark Wegenka, and Steve Zinger. IHS offers an independent assessment of the importance unconventional gas to the overall US economy. This research was supported by the America's Natural Gas Alliance (ANGA). IHS is exclusively responsible for all of the analysis and content contained herein. The analyses and metrics developed during the course of this research are intended to contribute to the national dialogue on the role of unconventional gas in terms of production, employment, economic growth, and energy security. IHS iii THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Executive Summary: The Economic and Employment Contributions of Unconventional Gas Development in State Economies In our 2009 study, "The Contributions of the Natural Gas Industry to the US National and State Economies," IHS examined the US economic and employment contributions of the natural gas industry's conventional and unconventional drilling and production activities. Our subsequent study released in December 2011, "The Economic and Employment Contributions of Shale Gas in the United States," furthered this research by focusing on the economic benefits to the nation of the natural gas industry's unconventional shale activity. This study, "The Economic and Employment Contributions of Unconventional Gas Development in State Economies" examines the natural gas industry's unconventional gas activities—gas production from shale formations, tight sands and coal bed methane (CBM)—at the state level. The report assesses the economic benefits of this growth, including the employment contributions for each of the US lower 48 states and the District of Columbia through 2035. These projections are based on the assumption that there are no significant changes to the current levels of environmental regulations at the federal or state level throughout the forecast horizon. Unconventional gas activity is having a dramatic impact on employment and economic growth across the US lower 48 states and the District of Columbia, in terms of jobs and its contribution to gross state product (GSP) and, by extension, US gross domestic product (GDP). This reflects the significant capital intensity required to develop unconventional gas resources, the ability to source inputs from a coast-to-coast network of suppliers and professional services around the United States, and the high quality of the jobs created by this activity. Unconventional gas is expected to lead future growth in US natural gas productive capacity. By 2015, the share of US natural gas produced from unconventional sources will increase to 67% and, by 2035, will reach 79%. Increased unconventional gas activity will contribute to capital investment, job opportunities, economic growth, government revenue, and lower prices across the country including: • Nearly $3.2 trillion in investments in the development of unconventional gas are expected to fuel the increase in production between 2010 and 2035. • In 2010, unconventional gas activity supported 1 million jobs; this will grow to nearly 1.5 million jobs in 2015 and to over 2.4 million in 2035. • By 2015, unconventional gas activities will contribute nearly $50 billion in federal, state and local government tax and federal royalty revenue; between 2010 and 2035, continued development of unconventional gas will generate a cumulative total of nearly $1.5 trillion in federal, state, and local tax and royalty revenue. This study, which focuses on 58 unconventional gas plays across the lower 48 US states, assesses their economic impact on each individual state. Three types of gas plays are analyzed in this report: natural gas extracted from shale formations, tight sands, and CBM. These are referred to collectively throughout this report as "unconventional gas."1 The following are highlights of this study's findings regarding the economic contributions to individual states, in terms of jobs, GSP, and tax revenue paid to federal, state and local governments as a result of unconventional gas activity: • Over the projection horizon, there are 20 "producing" states for unconventional gas—comprised of 13 states that have both existing and new well completion and production activities and seven additional states that have production activity associated with existing unconventional gas wells. Together, unconventional gas activity in these producing states contributed more than 826,000 jobs in 2010 and that number will grow to nearly 1.2 million jobs by 2015. 1 The major distinction between conventional and unconventional natural gas has to do with the permeability (or lack thereof) of the source rock in which they are contained. In a conventional natural gas reservoir, natural gas has migrated upward from its source rock through other permeable rocks until it has become trapped by an impermeable layer of rock. Unconventional natural gas is contained in source rock of low permeability, and hence is unable to move at all out of the source rock. Given the increasingly dominant share of this type of natural gas production, the term 'unconventional' may no longer be appropriate, though it remains in common use. IHS v THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES • According to US Bureau of Labor Statistics data, the majority of top-producing states have shown lower unemployment than the overall national average. In 2010, the Top 5 producing states' unemployment rates were 6.98.9%, compared with the national average of 9.6%. • Between 2010 and 2015, the Top 10 producing states—as ranked by employment generated by their unconventional gas activity—will experience a compound annual employment growth rate of nearly 8%. Pennsylvania and Colorado are expected to lead in employment contribution growth, experiencing compound annual growth rates of roughly 14% and 10% respectively. Total US employment is expected to grow at an average rate of 1.6% during the same time period. • By 2015, the 20 producing states will contribute just over $41 billion in federal, state and local government tax and federal royalty revenue. By 2035, these receipts will be nearly $72 billion. • Non-producing states—defined as the 28 states and the District of Columbia that do not include current or projected unconventional gas resource development—still benefit from their roles as suppliers in the unconventional gas expansion in the future. Together, in 2010, they contribute 18% of the total US employment generated by unconventional gas activity and 17% of the resulting tax revenue. By 2035, employment and government revenues in these states grow more than two-fold. The dramatic impact on employment and the economy from unconventional gas activity reflects its significant capital intensity requirements, the ability to source inputs from domestic sources, the coast-to-coast structure of the supply chain, and the high quality of the jobs created.2 These economic contributions will be largely driven by activity in the 20 producing states with both new well completion and production or existing production. However, the 28 non-producing states that do not include projected unconventional gas development will still contribute nearly one in every five jobs to the overall economy. 2 For more information, please see "The Economic and Employment Contributions of Shale Gas in the United States:" http://www.ihs.com/info/ecc/a/shale-gas-jobs-report.aspx. vi JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES TABLE OF CONTENTS Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .1 Jobs: Nearly 1.5 Million US Jobs by 2015—268,000 in Non-Producing States Alone . . . . . . . . . . . . . .3 Government Revenue: Nearly $50 Billion Nationwide by 2015—$8 Billion in Non-Producing States . . .5 Value Added: Nearly $197 Billion in US GDP by 2015—$22 Billion from Non-Producing States . . . . . .6 Structure of the Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8 1. Background . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .9 2. Methodology and Approach . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10 Energy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10 Economic Contribution Assessment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .12 Data Requirements and Assumptions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .12 Capital Expenditures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .12 Modeling the State Economic Contribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15 3. Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .16 4. Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .19 Appendix A. Economic Contributions by State and Year . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .A-1 Employment Contribution: Alphabetical by State . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .A-2 Employment Contribution by State: Ranked by Total Contribution . . . . . . . . . . . . . . . . . . . . . . . . . . .A-8 Value Added Contribution: Alphabetical by State . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .A-14 Value Added Contribution by State: Ranked by Total Contribution . . . . . . . . . . . . . . . . . . . . . . . . . .A-20 Labor Income Contribution: Alphabetical by State . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .A-26 Government Revenue and Private Lease Payments by State . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .A-32 Appendix B. Economic Contributions by State, Industry, and Year . . . . . . . . . . . . . . . . . . . . . . . . . . . . .B-1 Employment Contribution by State and Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .B-2 Value Added Contribution by State and Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .B-100 Labor Income Contribution by State and Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .B-198 Appendix C. Economic Contributions Excluding Cross-State Contributions by State and Year . . . . . . . .C-1 Employment Contribution Excluding Cross-State Contributions: Alphabetical by State . . . . . . . . . . .C-2 Value Added Contribution Excluding Cross-State Contributions: Alphabetical by State . . . . . . . . . . .C-8 Labor Income Contribution Excluding Cross-State Contributions: Alphabetical by State . . . . . . . . .C-14 Appendix D. The Economic and Employment Contributions of Non-Shale Unconventional Gas in the United States . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-1 IHS vii THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Overview In our 2009 study “The Contributions of the Natural Gas Industry to the US National and State Economies,” IHS examined the U.S economic and employment contributions of the entire natural gas industry, which includes both conventional and unconventional activities. Our subsequent study, “The Economic and Employment Contributions of Shale Gas in the United States,” furthered this research by focusing on the natural gas industry’s unconventional shale activity for the nation. As a companion to that report, this study examines the natural gas industry’s unconventional activities—namely gas production from shale, tight sands and CBM—at a state level to assess the economic and employment contributions in each of the lower 48 states and the District of Columbia through 2035. The projections presented within this report are based on the assumption that there are no significant changes to the current levels of environmental regulations at the federal or state level throughout the forecast horizon. To understand the economic and employment contributions at the state level, we begin with a national perspective of the total unconventional gas activity. The economic contributions associated with all unconventional gas activities are significant. Rapid development of these unconventional resources is projected to fundamentally alter US sources of natural gas production for decades to come. In fact, in 2010 alone, unconventional gas activity already represented 53% of total US gas production and is projected to rise to 79% by 2035. Fueling this increase in the proportion of natural gas production from unconventional activity is a projected $3.2 trillion in cumulative capital investments through 2035. These massive capital outlays, along with the promise of stable low natural gas prices, will have profound national economic consequences including: • By 2015, the employment contributed by unconventional gas activity is projected to reach nearly 1.5 million US jobs on a path to more than 2.4 million jobs by 2035. • By 2015, the annual contribution of unconventional gas activity to GDP is projected to reach nearly $197 billion and, by 2035, is expected to more than double to nearly $332 billion. • By 2015, government revenue provided by unconventional gas activity is projected to reach nearly $50 billion and will continue to rise to nearly $86 billion by 2035. Over the entire 25-year projected horizon of this study, this activity is expected to generate nearly $1.5 trillion in total government revenue. In addition to its direct economic contributions, U S E m p l o y m e n t C o n t r i b u tion, 2015 unconventional gas activity has fostered low and Unconventional Gas (Number of workers) stable gas prices that have additional positive macroeconomic impacts. A simulation of IHS Global Insight’s Macroeconomic Model of the 1,195,346 US Economy shows that current low and stable gas prices in the near term will contribute to a 10% reduction in electricity costs, a rise in the level of GDP that peaks at a 1.1% increase by 2013, and an 809,000 rise in employment by 2015. In the long run (beyond 15 years), the equilibrating tendency of the economy will lessen 268,104 the relative beneficial impacts of low gas prices, but they will continue to bring noteworthy benefits to the industrial sectors. For example, improvements in the competitiveness of domestic Non-Producing States Producing States manufacturers, due to lower natural gas and Source: IHS Global Insight electricity costs, will result in an initial 2.9% increase in industrial production by 2017 and 4.7% higher production by 2035 compared to the level of activity that would occur under a higher price scenario without unconventional gas. IHS 1 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES The remainder of this study examines how these national economic and employment contributions—from 58 US unconventional gas plays—are distributed across the lower 48 US States and the District of Columbia. It finds that traditional oil and gas states like Texas and Louisiana will lead the way in terms of the economic benefits they will receive from unconventional gas activity. However, by 2015, many of these economic benefits—including employment (268,000), value added to GDP ($22 billion), and tax revenue ($8 billion)—will be realized in states that do not have any unconventional gas production activity (“non-producing” states), but instead will benefit from the purchases of supplies and services from businesses across the United States. This report provides a detailed analysis of how these economic contributions will be distributed among the various states. The ability of each state to share in the benefits of increasing production of unconventional gas will be determined by a number of critical factors, including its natural resource endowment, the regulatory environment, its underlying industrial base, its capital and labor composition, and the diversity of its overall economy. U S V a l u e A d d e d C o n t r i b u t i o n t o GDP, 2015 Unconventional Gas ($M) 174,037 22,479 Non-Producing States Producing States Source: IHS Global Insight C o n t r i b u t i o n t o U S G o v e r n m e n t R evenue, 2015 Unconventional Gas ($M) 41,090 This study was performed on a state-by-state basis and results are presented in their entirety 8,246 in appendices A, B and C. However, to summarize the findings across the lower 48 states and the District of Columbia, the results are presented in two distinct groups. First are the 20 Non-Producing States Producing States “producing” states where natural gas producSource: IHS Global Insight tion is located. Of these producing states, 13 states have both existing and new well drilling and production activities, and another seven states have existing unconventional gas wells in production, but no anticipated new well drilling and development planned during the 25-year forecast horizon of this study. Second are the 28 non-producing states and the District of Columbia. The commonality across these states is that none of them currently has unconventional gas wells, nor are they projected to engage in unconventional gas drilling and production activities during the forecast horizon of the study. It is important to note that this does not mean these states lack the potential for resource development. Rather, with the currently available information, we assume there will be no unconventional gas production occurring within these states during the forecast horizon. However, these non-producing states are expected to greatly benefit from unconventional gas development in the future through a complex network of supply chains, trade flows among the various producing states, and the income effects of earnings spent by workers benefitting directly or indirectly from natural gas production within these states. 2 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES In the following sections, the economic gains that will be generated by increased unconventional gas production in the United States will be presented in terms of their contributions to employment, GDP, and federal, state and local government revenue. For each of these categories of economic contributions, the report will break out and compare gains between the producing and non-producing states. State-by-state details supporting these aggregate data can be found in Appendices A, B, and C. Jobs: Nearly 1.5 Million US Jobs by 2015—268,000 in Non-Producing States Alone The majority of US economic activity generated by unconventional gas production will take place in the 20 states with natural gas resources. In these producing states, unconventional gas activity was responsible for creating more than 826,000 jobs in 2010. We project these states will add nearly 400,000 additional jobs between 2010 and 2015, growing to nearly 1.2 million. In both 2010 and 2015, the Top 10 producing states account for approximately 84% of the employment gains that will be generated by all of the producing states, with Texas and Louisiana leading the way in terms of the absolute numbers of jobs created. Between 2010 and 2015, the overall annual growth rate in employment for unconventional gas activity will be approximately 7.7%. Pennsylvania and Colorado will lead in terms of compound annual employment growth, experiencing roughly 14% and 10% growth, respectively. Employment Contribution of Unconventional Gas* in Producing States vs. Non-P Producing States Top 10 Unconventional Gas* Producing States: Employment Contribution** (Number of workers) (Number of workers) Producing States** Non-Producing States US Total 2010 826,355 182,303 2015 1,195,346 268,104 2035 2,007,90 430,975 1,008,658 1,463,450 2,438,877 NOTES: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. **Producing states are the 20 states that have either new well completions and production or production from existing wells. They include Alabama, Arkansas, Colorado, Illinois, Kansas, Kentucky, Louisiana, Michigan, Mississippi, Montana, New Mexico, New York, Ohio, Oklahoma, Pennsylvania, Texas, Utah, Virginia, West Virginia, and Wyoming; the rest of the states are non-producing states. Source: IHS Global Insight Texas Louisiana Colorado Pennsylvania Arkansas Wyoming Ohio Utah Oklahoma Michigan Top 10 Total Producing Total US Total 2010 288,222 81,022 77,466 56,884 36,698 34,787 31,462 30,561 28,315 28,063 693,481 2015 385,318 124,782 126,525 111,024 53,919 45,763 41,366 36,593 41,763 37,926 1,004,979 2035 682,740 200,555 127,843 270,058 79,723 78,792 81,349 50,839 69,261 63,380 1,704,541 826,355 1,008,658 1,195,346 1,463,450 2,007,902 2,438,877 NOTES: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. **The rank for all years are based on the 2010 ranking. Source: IHS Global Insight Unconventional Gas Contributes to Lower Unemployment Rate in Producing States Based on US Bureau of Labor Statistic data, the US unemployment rate registered 9.6% in 2010. All of the topproducing states, with the exception of Michigan and Ohio, have shown lower unemployment than the national average. The Top 10 producing states' unemployment rates ranged from 0.7-2.7 percentage points lower than the national average. IHS 3 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES One of the most important findings from this study is the fact that the economic contributions from unconventional gas activity are not limited to states endowed with the resources. For example, California does not directly produce unconventional gas, yet the economic activity associated with unconventional gas production supported nearly 23,000 jobs in California in 2010; the state’s unconventional gas activity-related employment is expected to increase to more than 33,000 jobs by 2015 and will more than double to nearly 49,500 by 2035. Top 10 Unconventional Gas* Non-P Producing States: Employment Contribution** (Number of workers) 2010 22,773 15,758 13,294 12,031 11,377 10,819 9,608 9,271 8,519 7,008 120,459 2015 33,265 27,402 18,800 17,427 16,570 15,206 14,285 14,499 12,323 10,263 180,042 2035 49,494 30,903 29,262 30,105 28,271 26,837 24,871 22,638 21,487 16,634 280,503 182,303 1,008,658 268,104 1,463,450 430,975 2,438,877 California Florida Georgia Missouri North Carolina Indiana Wisconsin Minnesota Tennessee Maryland Top 10 Total Non-Producing Total US Total NOTES: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. **The rank for all years are based on the 2010 ranking. Source: IHS Global Insight Unconventional Gas Fuels States' Economic Recoveries As the nation's economic recovery continues, state labor markets are expected to exhibit different growth patterns that will be determined by their industrial initiatives. During the next few years, IHS Global Insight's outlook for state economies shows that four out of the five states with the strongest employment growth will either be unconventional gas producers or will appear on top of the list of non-producing states. The five states are North Dakota, Utah, Colorado, Florida, and Texas—all of them are expected to have annual employment growth that exceeds 2% through 2015. While IHS Global Insight expects economic conditions to improve over the next few years, with average US unemployment falling to 6.8% by 2015, top producing states' unemployment rates will outperform the national average. Employment Composition Varies in Producing and Non-Producing States The employment contributions and the types of jobs created by the natural gas industry's unconventional gas activity vary between the producing and non-producing states. The main reasons for these differences are the scope of direct industrial activity, the location of capital goods that are purchased, the supply chain, and the income ramifications throughout the economy. In the producing states, a greater proportion of the total jobs generated are found in direct production or key support industries of unconventional gas activity. In Arkansas, for example, 30% of all of employment associated with unconventional gas is found in the mining sector, followed by other key industries such as construction, trade, and manufacturing. Alternatively, in non-producing states, more employment is generated in supplier networks that support the unconventional gas activity. In California, 47% and 30% of employment, respectively, is in the service sector and in manufacturing. 4 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Government Revenue: Nearly $50 Billion Nationwide by 2015—$8 Billion in Non-Producing States Our study estimates nearly $34 billion in annual tax receipts in 2010 by federal, state and local governments. Total annual receipts will approach $50 billion by 2015 and exceed $85 billion by 2035—more than doubling 2010 levels. On a cumulative basis between 2010 and 2015, unconventional activity is projected to contribute nearly $208 billion in total tax revenue; over the 25-year forecast horizon, IHS projects nearly $1.5 trillion in total revenue3. Contribution to US Government Revenue of Unconventional Gas* in Producing States vs. Non-P Producing States ($M) Producing States*** Non-Producing States 2010 28,034 5,758 2015 41,090 8,246 2035 2010-2035** 71,806 1,255,034 13,317 243,701 US Total 33,793 49,335 85,123 1,498,734 NOTES: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. **2010-2035 represents the total for all years including those years not reported. ***Producing states are the 20 states that have either new well completions and production or production from existing wells. They include Alabama, Arkansas, Colorado, Illinois, Kansas, Kentucky, Louisiana, Michigan, Mississippi, Montana, New Mexico, New York, Ohio, Oklahoma, Pennsylvania, Texas, Utah, Virginia, West Virginia, and Wyoming; the rest of the states are non-producing states. Source: IHS Global Insight The majority of the government revenue generated by unconventional gas production will occur in the 20 producing states. The revenue derives not only from personal, corporate, federal, state, and local taxes but also from severance, ad valorem, and royalty payments, which are particular to unconventional gas activity. Combined, the unconventional gas activity in these producing states is projected to contribute $41 billion in all types of government tax and related revenue by 2015 and nearly $72 billion to annual receipts by 2035. Unconventional Gas Activity Makes Large Contributions to State Budgets In 2010, the education budget for the state of Texas was $81 billion and healthcare spending registered $40 billion. Unconventional gas activity generated state and local revenues of $5 billion—representing 6 percent of the education and 13 percent of the healthcare budget. Colorado allocated $12 billion to education in 2010—in comparison, the unconventional gas industry generated $1.6 billion state and local revenue, which equals 13 percent of its education budget. The Top 10 producing states provide a substantial share of total payments to governments at the federal, state and local level. Unconventional gas activity in these 10 states will generate over $24 billion in total taxes in 2010—72% of all tax revenue generated by unconventional gas activity in all of the producing states. The producing states’ share will continue to increase. By 2015, unconventional gas activity in the Top 10 states will pay about $36 billion—or nearly 73% of total tax receipts from all unconventional activity. By 2035, they will pay nearly $63 billion in taxes—or 74% of total government revenues. While traditional energy-producing states like Texas and Louisiana will lead the way in generating government revenue from their unconventional gas activities, the nonproducing states will contribute a total of nearly $6 billion in 2010 and are projected to pay over $8 billion by 2015. Top 10 Unconventional Gas* Producing States: Contribution to US Government Revenue** ($M) Texas Colorado Wyoming Louisiana Pennsylvania Arkansas New Mexico Oklahoma New York Michigan Top 10 Total 2010 10,891 3,197 2,247 2,074 1,476 1,193 1,091 875 721 693 24,458 2015 14,757 4,434 3,362 3,897 3,505 1,792 1,045 1,310 1,038 884 36,025 2035 26,412 4,526 6,243 7,702 8,889 2,775 914 2,257 1,599 1,403 62,720 Producing Total US Total 28,034 33,793 41,090 49,335 71,806 85,123 NOTES: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. **The rank for all years are based on the 2010 ranking. Source: IHS Global Insight 3 Tax projections were based upon current tax structures and did not consider how changes to the current tax structure might impact these projected receipts. IHS 5 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES By 2035, receipts from all of the non-producing states will surpass $13 billion. The Top 10 non-producing states—like the producing states—also comprise a significant share of the total government revenue from all of the non-producing states. In fact, at over $4 billion, these 10 states will contribute 74% of all government revenue from non-producing states in 2010. By 2015, that share will increase to more than $6 billion, or about 75% of the total, due to the rapid expansion of support activities supplied to producing states. Top 10 Unconventional Gas* Non-P Producing States: Contribution to US Government Revenue** ($M) California Florida Missouri New Jersey Georgia Massachusetts North Carolina Minnesota Indiana Wisconsin Top 10 Total Non-Producing Total US Total 2010 1,516 536 426 353 271 263 252 224 212 211 4,263 2015 2,237 886 594 475 364 391 300 350 275 315 6,188 2035 3,440 1,201 1,007 834 578 611 519 539 473 546 9,748 5,758 33,793 8,246 49,335 13,317 85,123 NOTES: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. **The rank for all years are based on the 2010 ranking. Source: IHS Global Insight Unconventional Natural Gas Important To Pennsylvania State Budget Pennsylvania's 2010 state budget included $11 billion for public transportation and $9 billion for public safety and criminal justice. A combination of corporations, businesses and individuals supporting unconventional natural gas activity paid a combined total of $641 million in taxes to Pennsylvania state and local governments that year, accounting for 6 percent of the state's transportation budget and 7 percent of spending on public safety and criminal justice. Value Added: Nearly $197 Billion in US GDP by 2015—$22 Billion from Non-Producing States The commonly used measure of GDP, which is simply the sum of the value added across all products and services produced in the United States, is generally considered the broadest measure of the health of the US economy. Value added to US GDP is defined as the sum of labor incomes, corporate profits, indirect business taxes paid, and depreciation. Annual value added to GDP from unconventional gas activities was more than $133 billion in 2010 and, by 2015, is projected to approach $200 billion. The majority of the value added to GDP—nearly 90%—over the 25-year forecast horizon is generated by unconventional gas production activities that take place in the 20 producing states. In 2010, the Top 10 producing states accounted for 78% of the US total value added to GDP by unconventional 6 US Value Added Contribution of Unconventional Gas* in Producing States vs. Non-P Producing States ($M) Producing States** Non-Producing States 2010 118,077 15,328 2015 174,037 22,479 2035 295,897 35,831 US Total 133,405 196,516 331,728 NOTES: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. **Producing states are the 20 states that have either new well completions and production or production from existing wells. They include Alabama, Arkansas, Colorado, Illinois, Kansas, Kentucky, Louisiana, Michigan, Mississippi, Montana, New Mexico, New York, Ohio, Oklahoma, Pennsylvania, Texas, Utah, Virginia, West Virginia, and Wyoming; the rest of the states are non-producing states. Source: IHS Global Insight JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES An Economic Growth Engine in Producing States IHS Global Insight's outlook for Texas and Utah shows that economic growth in these states will outperform all other states. From 2010 to 2015, each state's economy is expected to grow more than 3.5% annually. In Texas and Utah, the average employee in the unconventional gas and related industries will contribute $167,000 and $94,000 in "value-added" to their respective state's economies in 2010 through 2015; this outpaces the state's average employee contributions of $111,000 and $90,000, respectively. gas activity. By 2015, we project these Top 10 states will add another $50 billion to GDP, valued at 78% of the unconventional gas activity’s total contribution to GDP. Pennsylvania and Louisiana will lead the way with annual growth in their contributions to GDP of 18.7% and 12.6%, respectively. By 2035, unconventional gas activity will add almost $332 billion to US GDP—with the Top 10 producing states accounting for 78% of the relative contributions. Overall, the non-producing states account for about 11%, on average, of the total value to US GDP throughout the forecast horizon. While the share of labor income from the non-producing states is in line with their employment share, they do not make as large of a relative contribution to GDP as the producing states. This is attributable to the fact that producing states are heavily influenced by the Oil and Gas sector which has high value added (mostly dedicated to non-labor income). Top 10 Unconventional Gas* Producing States: Value Added Contribution** ($M) Texas Colorado Louisiana Pennsylvania Wyoming Arkansas Oklahoma New Mexico Utah Ohio Top 10 Total 2010 47,995 12,258 11,020 7,121 6,760 4,910 4,008 3,356 3,126 3,045 103,600 2015 64,768 18,162 20,005 16,806 8,815 7,264 6,033 3,160 3,866 3,942 152,821 2035 111,089 17,485 37,759 42,438 14,735 10,540 9,905 2,589 5,343 7,921 259,805 Producing Total US Total 118,077 133,405 174,037 196,516 295,897 331,728 NOTES: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. **The rank for all years are based on the 2010 ranking. Source: IHS Global Insight Top 10 Unconventional Gas* Non-P Producing States: Value Added Contribution** ($M) California Florida Georgia Missouri Indiana North Carolina Minnesota Wisconsin Tennessee New Jersey Top 10 Total Non-Producing Total US Total 2010 2,192 1,163 1,147 1,057 957 909 796 783 683 640 10,326 2015 3,197 2,034 1,622 1,529 1,326 1,318 1,272 1,167 986 841 15,291 2035 4,617 2,266 2,398 2,616 2,331 2,185 1,937 2,044 1,727 1,406 23,527 15,328 133,405 22,479 196,516 35,831 331,728 NOTES: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. **The rank for all years are based on the 2010 ranking. Source: IHS Global Insight IHS 7 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Structure of the Report This report is a companion to the previous national level report, “The Economic and Employment Contributions of Shale Gas in the United States,” published by IHS in December 2011. The remainder of this report is divided into the following four sections: • Section 1 provides a background and reports our findings. • Section 2 explains the methodology and approach that was used to develop the estimates economic activity generated by each state’s unconventional gas activity. It is divided into two main parts—Energy and Economic Contribution Assessment—each of which describes the inputs required to develop our final estimates. • Section 3 provides a snapshot of the results by state for 2010, 2015 and 2035 for the following four main concepts: employment, government revenue, value added to GDP, and labor income contributions. • Section 4 wraps up the report with important conclusions from its findings. Additionally, we provide several appendices to both present more detailed results from our report and to facilitate the readers’ understanding of the methodologies, research, and data relied upon for the analyses. The appendices to the report are as follows: 8 • Appendix A: Economic Contributions by State and Year provides six detailed tables by state for each of the five-year increments presented. The concepts covered are employment contribution (both alphabetically and ranked by total value for that year), value-added contribution (both alphabetically and ranked by total value for that year), labor income contribution (alphabetical only), and government revenue. • Appendix B: Economic Contributions by State, Industry and Year breaks down the three main concepts—employment, value added to GDP, and labor income contribution—even further by industry such that the final tables are by state and industry for each of the five-year increments. • Appendix C: Economic Contributions Excluding Cross-State Contributions by State and Year provides three detailed tables by state for each of the five-year increments; however, these tables differ in that the resulting numbers do not include any cross-state contributions (this approach contrasts with Appendix A, which does include these cross-state contributions). The concepts covered are employment, value-added and labor income contribution, each of which is displayed alphabetically. • Appendix D: Find the report, “The Economic and Employment Contributions of Non-Shale Unconventional Gas in the United States,” which presents the results from our analysis of total and non-shale unconventional gas activity at the national level. It includes its own appendices (A through C) detailing the underlying methodology and detailed data related to the assumed future production profile and capital expenditure outlook for nonshale unconventional gas; the detailed results of the economic contribution assessment for non-shale unconventional gas; and the data and modeling approach underlying the economic contribution analysis for non-shale unconventional gas. JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES 1. Background The development of unconventional gas resources in the United States is credited with fundamentally changing the outlook for domestic natural gas supply and price, with significant contributions to employment and the economy. These have been documented in our report, “The Economic and Employment Contributions of Shale Gas in the United States.” This study provides an analysis of the distribution of these national results at the state level. The analysis takes into account the broad distribution of unconventional gas development across a wide range of states. The results reflect careful analysis of each state’s production potential through 2035, based on IHS CERA’s analyses of each natural gas play and calculates the investment of capital, labor, and other inputs required to produce the gas at each play. The economic effects of these investments are then calculated using IHS Global Insight’s proprietary economic impact assessment and macroeconomic models, generating employment, value added to GDP, labor income, and tax revenue resulting from the growth in the coming years of unconventional gas development. IHS 9 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES 2. Methodology and Approach Energy IHS CERA’s outlook for unconventional gas in the US lower 48 states includes production from 58 unconventional gas plays nationwide: 21 shale plays, 23 tight sands gas plays, and 14 CBM plays. 10 Unconventional Gas Plays Play Type Geographic Extent of Play* Barnett Shale Texas Eagle Ford Shale Texas Fayetteville Shale Arkansas Haynesville (Arkla Basin) Shale Louisiana ETB Haynesville Shale Texas Marcellus Shale Pennsylvania, West Virginia, New York, Kentucky, Virginia Woodford Shale Oklahoma Barnett-Woodford Shale Texas Utica Shale Ohio, Pennsylvania, New York Floyd Shale Mississippi , Alabama Bossier Shale Texas Antrim Shale Michigan Niobrara Shale Colorado Baxter Shale Wyoming Pierre Shale Colorado, New Mexico Mancos Shale Colorado, New Mexico, Utah Mesa Verde Shale Colorado, New Mexico, Utah Upper Devonian Shale Kentucky, New York, Ohio, Pennsylvania, Virginia, West Virginia Ordovician Shale Kentucky, New York, Ohio, Pennsylvania, Virginia, West Virginia Devonian Shale Kentucky, New York, Ohio, Pennsylvania, West Virginia Jurassic-Lower Cretaceous Shale Texas Big Sandy Tight Sands Kentucky, Virginia, West Virginia Trenton-Black River Tight Sands Kentucky, New York, Ohio, Pennsylvania, Virginia, West Virginia Cotton Valley Tight Sands Louisiana Vernon/Terryville Tight Sands Louisiana East Cotton Valley Tight Sands Texas West Cotton Valley Tight Sands Texas Deep Bossier Tight Sands Texas Wilcox (Lobo) Tight Sands Texas Granite Wash Tight Sands Texas, Oklahoma Sahara Tight Sands Oklahoma Colony Wash Tight Sands Arkansas Hartshorne Tight Sands Oklahoma Haley Deep Tight Sands Texas Wattenberg-Niobrara-Codell Tight Sands Colorado Piceance Emerging Tight Sands Colorado Lower Cretaceous-Mesozoic Tight Sands Colorado Natural Buttes Tight Sands Utah Buttes Deep Tight Sands Utah Lance Tight Sands Wyoming Appalachian, avg Coal Bed Methane (CBM) Pennsylvania, Virginia, West Virginia JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Unconventional Gas Plays Play Type Geographic Extent of Play* Black Warrior - Pottsville CBM Alabama Arkoma - Hartshorne CBM Oklahoma Chatauqua CBM Oklahoma Cherokee CBM Kansas East Green River CBM Wyoming LV Raton CBM Colorado, New Mexico Piceance CBM Colorado Big George CBM Wyoming, Montana Wyodak CBM Wyoming, Montana Canyon CBM Wyoming, Montana Anderson CBM Wyoming, Montana Uinta CBM Utah San Juan CBM New Mexico, Colorado *The list of gas plays provides the state location or locations of the full extent of the underground gas play. However, states containing part of a play do not necessarily have production from that play. For example, the Marcellus play extends into Virginia and Kentucky, but no extractions of Marcellus gas take place in those states at present or in the outlook for this study. This study also assumes that no Marcellus production is forthcoming from New York. A table on capital expenditures found in the next section on Economic Contribution Assessment provides a more important guide for how the impacts of US unconventional gas development flow to different states. The cost of drilling and constructing a well and putting it into operation is a critical component of the economic viability of developing any unconventional gas play, and costs to the industry vary. An unconventional gas well in a shale or tight sands target may cost anywhere between $3.5 million and $12 million, while a well targeting CBM may cost between $500,000 and $1.5 million. The cost of the well depends on several factors such as the vertical depth of the well bore, its lateral length, reservoir pressure, rock characteristics, and the number of fracture stages, as well as commercial factors such as ease of access to materials and services, such as supplies of water, proppant, drilling and completion services. Capital expenditures are undertaken for land, drilling, completion, facilities, gathering, processing, and compression. The development of a major play also requires the addition of pipeline capacity to get the gas to market. IHS CERA has estimated the costs associated with the production outlook for unconventional gas, which are based on IHS databases and proprietary models detailed in our prior report, “The Economic and Employment Contributions of Shale Gas in the United States.” In this report, the production profiles were developed based on detailed analyses of each unconventional gas play. The production possibilities were constrained to be consistent with IHS CERA’s outlook for natural gas demand, price, and infrastructure, as reported in its “North American Natural Gas Market Briefing” in September 2011. Well counts were estimated for each play consistent with the play-level production outlook, and capital expenditures associated with the well counts were estimated. IHS CERA initially allocated the capital expenditures to individual states according to the geographic locations of each play. For plays that cross state boundaries, the capital expenditures were prorated to provide allocations among the states involved. The initial set of capital expenditures were further distributed to states where purchases are actually undertaken. This methodology is described in the next section. Infrastructure capital expenditures include expenditures for gathering lines and processing plants, as well as the pipeline expansions required to connect new supply areas to consumers. Gathering and processing expenditures were allocated to the states in the same way that well expenditures were allocated. Pipeline expansion costs and allocations were based on the expansion requirements indicated by the Gas Pipeline Competition Model™, which was used for the market analysis in the study. IHS 11 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Economic Contribution Assessment Data Requirements and Assumptions In this economic contribution assessment, IHS Global Insight, with support from IHS CERA, compiled state-level data of unconventional gas activity in the 20 US states (13 of which have current and future development) that contain plays that extract natural gas from shale, tight sands, and CBM. Both the value of production and capital expenditures were input, by state, into the model to conduct the economic analysis. The following activities were determined to be major direct contributors: • Natural gas drilling • Natural gas extraction • Support activities and services required for oil and natural gas drilling and extraction • Construction of facilities, related materials and machinery for hydraulic fracturing and completions, and construction of natural gas pipeline The primary analytical tool for this multi-state study is the same IMPLAN Input-Output model used, with the IHS US Macroeconomic Model, in the overall US analysis. However, the architecture of the existing IMPLAN model could not efficiently handle the computational complexity of a multi-state analysis in which each state is, within IMPLAN, effectively an independent geographic region. To adjust for this limitation, IHS Global Insight ran multiple, alternative versions of the IMPLAN multi-regional model and integrated the output with in-house proprietary database to assess the indirect and induced economic contribution by industry and state. This fine-tuned methodology ensures that inputs that are not locally produced—or do not have a competitive advantage locally—are sourced from other states creating economic “leakage” from one state to another. In the broader context, economic “leakage” is explained as inter-regional activity in which the production requirements of a commodity (or a service) use inputs produced in other states thus causing the economic impact to “leak” to other states and introducing a regional ripple effect. The model framework used here was set up as a system of linked state economies. As a result, the sourcing of inputs for the development of unconventional gas activity will impact those states that do not have an unconventional gas play within their borders. For example, the development of unconventional gas wells in Arkansas relies on bank, insurance and securities services in New York and professional services primarily located in Texas. Capturing these connections highlights the indirect economic contribution even in states that lack unconventional gas plays. The leakages also impact US GDP and employment multipliers, making them more accurate for states that do have unconventional gas plays. The IMPLAN model also produces “own-state” multipliers—that is, the indirect and induced impact that flow from direct activity as a result of that state’s unconventional gas development but exclude any impact from the supplier states providing services or products. Appendix C provides the results of this analysis, when cross-state ramifications are excluded. In a given year, the volume of natural gas produced in each state is impacted by both the wells drilled during the course of the year and by wells drilled in previous years that remained in operation. The monetary value of gas production volumes was calculated using the Henry Hub price. These values served as inputs to the oil and gas extraction industry in the corresponding states in the IMPLAN model. Capital Expenditures While the value of gas production is attributed only to states with unconventional gas plays, the allocation of capital expenditures among the 48 producing and non-producing states is more involved. Capital expenditures act as direct impacts at both the state and industry levels. The complexity lies in the fact that a portion of that spending 12 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES may be allocated to states that do not have unconventional gas plays. This spending will trigger indirect and induced impacts in these states as they provide goods and services. To ensure that these effects are included in the economic analysis, IHS Global Insight used industry input, IHS Global Insight’s in-house expertise and proprietary databases, and extensive additional research to arrive at the best possible methodology for allocating capital expenditures among different states. The first step, as in the national study, was to map the capital expenditure breakdown for the categories specified by the IMPLAN model. Capital expenditure and support services for natural gas drilling correspond to industry sectors within the IMPLAN model. However, the breakdowns for drilling, completion, facilities, gathering, processing, pipeline construction, and liquid natural gas exports were mapped to many other categories of the model. The research, expertise and input from industry sources were integrated with an interstate trade-flow database to determine the sources of various products and services by state. For example, it is evident that unconventional gas extraction requires special sand for hydraulic fracturing that is produced primarily in Wisconsin, Minnesota, Ohio, and Arkansas. Since not all states with unconventional gas plays produce these unusual sands, they must import them from other states and are assumed to do so in the model. IHS’s trade-flow database was one of many sources used to determine the origin and destination of the various materials and equipment on a state level basis. This process was undertaken for all the products in the 13 states with current and future drilling in unconventional gas plays. The final set of capital expenditures, by various products and services, and, if applicable the value of production, was input into 44 IMPLAN state models to assess the contribution on each individual state’s economy. The following table presents the distribution of capital expenditures, by state, for all unconventional gas. IHS 13 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Annual Capital Expenditures: Unconventional Gas* ($Th) Alabama Arizona Arkansas California Colorado Connecticut Delaware Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina Ohio Oklahoma Oregon Pennsylvania South Carolina South Dakota Tennessee Texas Utah Virginia Washington West Virginia Wisconsin Wyoming 2010 88,198 92 1,674,752 1,792,229 4,326,768 2,199 87,721 474,246 273,702 2,929 789,017 183,532 78,210 168,896 302,190 5,261,222 2,084 40,153 1,100,916 80,105 11,572 1,396,689 326 41,164 261,370 11,524 227,351 507,570 111,869 13,220 1,749,294 2,034,698 147,021 3,137,275 9,243 3,106 50,525 20,985,288 2,189,541 238,551 18 1,181,468 45,641 1,488,366 2015 298,134 110 2,476,340 2,766,315 10,110,603 3,067 112,401 1,289,315 374,289 7,544 1,089,138 226,242 180,845 355,504 310,017 6,772,454 2,808 54,355 1,749,145 215,268 450,321 2,276,124 1,562 112,785 21,791 15,960 230,677 657,168 122,330 0 2,176,777 3,635,595 100,742 4,493,278 2,469 8,949 27,384 31,831,564 2,885,964 261,814 52 1,643,809 85,488 3,525,542 2020 211,635 25,457 3,085,442 3,301,097 11,969,358 5,260 188,339 732,600 243,848 8,978 1,630,895 374,257 229,437 429,051 433,158 6,298,067 4,769 92,443 2,643,963 252,339 246,439 3,265,169 3,952 133,865 90,592 27,318 371,154 803,839 204,222 36,564 3,551,881 4,852,863 111,455 7,655,977 21,222 10,666 55,263 46,217,167 3,381,468 416,916 131 2,696,010 121,625 4,178,904 2025 123,635 67,596 3,624,901 3,611,178 11,463,671 5,484 195,549 311,469 83,628 12,169 1,769,409 390,165 278,192 482,980 479,157 7,076,555 4,989 96,653 2,843,977 250,066 160,795 3,814,038 4,167 172,504 33,285 28,499 375,067 1,073,100 207,597 0 3,687,076 5,646,081 96,564 7,949,314 8,340 14,653 43,331 53,187,694 4,033,959 446,013 138 2,854,824 140,719 5,552,087 2030 258,901 175 4,372,585 4,218,463 12,026,623 7,652 269,226 1,389,372 388,887 15,959 2,310,066 533,868 358,615 571,271 599,869 7,954,937 6,931 134,356 3,675,159 270,750 165,182 4,818,032 4,360 221,395 41,055 39,728 500,846 1,193,464 281,826 0 4,974,479 7,074,172 92,235 11,025,053 12,151 19,439 52,480 67,419,993 4,730,273 601,777 144 3,904,395 187,488 7,222,197 2035 97,145 200 5,270,629 4,860,867 13,361,154 11,980 415,616 357,554 55,700 19,849 3,222,471 817,060 464,589 673,717 793,877 9,164,785 10,788 209,295 5,009,391 307,869 148,872 5,972,064 4,789 274,189 51,288 62,128 751,713 1,392,301 427,600 0 7,416,145 8,725,802 96,491 17,034,074 6,837 24,460 50,297 82,530,724 5,223,302 898,362 158 5,944,282 259,761 8,968,134 US Total 52,571,853 82,962,040 110,615,055 122,701,270 153,945,828 191,388,309 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight 14 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Modeling the State Economic Contribution The multi-regional capability of the IMPLAN model estimated the economic contributions of unconventional gas production and capital spending at the state level. The methodology assessed not only the contribution to states with unconventional gas production but also non-producing states affected directly (via capital expenditures) or indirectly (via cross-state trade flows) by the producing states’ activity. The IMPLAN model calculated the contribution to states with unconventional gas production and/or allocated direct capital spending. However, indirect and induced impacts were determined using various analytical tools: the IMPLAN model, IHS Global Insight’s trade-flow databases for product groupings, and IHS Business Market Insight for services categories. The process was repeated for each state with unconventional gas production and for those states affected by direct capital spending (a subset of non-producing states). Finally, all of the state-by-industry direct, indirect and induced contributions to employment, value added to GDP, labor income, and government revenue were calibrated with the national results. Starting with the IMPLAN Multi Regional Analysis (MRA) capability, each of the state models were simulated using production and/or capital expenditures depending on whether the state is a producing state or not. The MRA results were obtained for each state with direct production and/or capital expenditures as well as for all states that experience cross border impacts (leakages). The cross border contributions on the other states include both supply chain (indirect) and income (induced) effects. To ensure these impacts were traced to the best possible source location, IHS used its point-to-point commodity trade database (Transearch) and establishment location database (Business Market Insight) to determine the distribution of cross border contributions by state and industry. Finally, all of the state-by-state level results were calibrated with the national results to report a consistent and cohesive set of contributions by state and industry. State-L Level Enhanced Economic Contribution Methodology Schematic States with Unconventional Gas Plays States with Distributed Capital Expenditures IMPLAN St t MRA Models State M d l Contribution b on States With Unconventional Gas Plays or Distributed Capital Expenditures Cross Border Contributions on All Other States Commodity Trade d Database b (TRANSEARCH) Indirect and Induced Impacts Impacts by Industry and Type (All States) National Impact IHS Business Market Insight Calibration IHS 15 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES 3. Results The analysis of unconventional gas development and its contribution to the US regional economies was conducted using a top-down/bottom-up approach. The contribution was assessed separately for direct, indirect, and induced contributions defined as follow: • Direct contributions of unconventional gas are those activities required to explore, produce, transport, and deliver natural gas to consumers or to provide critical supplies or onsite services that support unconventional gas activity. • Indirect contributions are defined as activities in outside industries that supply equipment, material and services for the development of unconventional gas and its tier suppliers. • Induced contributions are the economic effects caused by workers spending their wages and salaries on consumer goods and household items. This IHS Global Insight study was performed on a state-by-state basis. However, to summarize the findings across the lower 48 states and the District of Columbia, the results are presented in two distinct groups. First are the 20 so-called “producing” states. Of these, 13 states have both existing and new well drilling and production activities, and another seven states have economic activity from their existing unconventional gas wells, but no new well drilling and development is anticipated over the course of our forecast horizon. Second are the “non-producing” states, of which there are 28 in the lower 48 states; our analysis also includes the District of Columbia. These states benefit from unconventional gas development through supply chains, trade flows with the various producing and non-producing states, and the income effects of earnings spent within these states. Direct activity in the producing states includes new well drilling and completion, unconventional gas production, and spending on various capital equipment and commodities for unconventional gas activity. Many of these states have built strong support industries, and they participate in the unconventional gas supply chain. The direct contribution from direct and indirect activity Employment Contribution of Unconventional Gas* in Producing States vs. associated with unconventional Non-P Producing States**: 2015 gas production is further ampli(Number of workers) fied on income and will fuel conProducing States Non-Producing States All States sumer expenditures—the Direct 309,070 24,709 333,779 induced impact. Indirect 374,296 105,191 479,487 650,184 While most of the capital spendTotal 1,195,346 268,104 1,463,450 ing is undertaken in the producing states, non-producing states NOTES: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. states are the 20 states that have either new well completions and production or production will benefit directly from pur- **Producing from existing wells. They include Alabama, Arkansas, Colorado, Illinois, Kansas, Kentucky, Louisiana, Michichases of goods and services gan, Mississippi, Montana, New Mexico, New York, Ohio, Oklahoma, Pennsylvania, Texas, Utah, Virginia, that constitute the capital West Virginia, and Wyoming; the rest of the states are non-producing states. Source: IHS Global Insight spending that supports unconventional gas activity. Some of the capital goods industries in the non-producing states will have competitive advantages over the producing states, which will cause spending to leak out to those states. In addition, non-producing states actively participate in the supply chain and will contribute to the indirect impact and expenditure induced impact. Induced 511,980 138,204 The tables on the following pages show the state-by-state results for employment, value added to GDP and government revenue for all 48 states and the District of Columbia in the primary forecast years: 2010, 2015, and 2035. More detailed tables are provided in the appendices. 16 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Employment Contribution of Unconventional Gas* Summary US State-L Level Government Revenue Contribution of Unconventional Gas* Summary (Number of workers) ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming 2010 8,675 6,918 36,698 22,773 77,466 5,017 1,681 905 15,758 13,294 1,841 25,773 10,819 5,183 5,353 10,870 81,022 1,666 7,008 4,968 28,063 9,271 3,259 12,031 1,591 3,199 2,153 647 6,865 20,417 26,887 11,377 1,141 31,462 28,315 6,756 56,884 1,368 5,607 1,176 8,519 288,222 30,561 848 13,162 3,904 16,888 9,608 34,787 2015 12,673 10,364 53,919 33,265 126,525 7,015 2,362 1,348 27,402 18,800 2,766 36,387 15,206 8,095 7,594 14,252 124,782 2,390 10,263 7,220 37,926 14,499 9,428 17,427 2,236 5,142 1,743 938 9,271 19,617 39,047 16,570 1,867 41,366 41,763 8,516 111,024 1,968 8,227 1,770 12,323 385,318 36,593 1,261 17,753 5,797 31,380 14,285 45,763 2035 15,866 19,737 79,723 49,494 127,843 10,380 4,770 2,294 30,903 29,262 4,818 61,657 26,837 14,526 12,470 21,825 200,555 3,774 16,634 11,356 63,380 22,638 8,768 30,105 3,582 9,216 3,278 1,576 15,064 18,462 58,377 28,271 3,645 81,349 69,261 14,107 270,058 2,904 14,368 2,959 21,487 682,740 50,839 1,922 30,732 9,777 71,620 24,871 78,792 US Total 1,008,658 1,463,450 2,438,877 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming 2010 240 136 1,193 1,516 3,197 116 39 15 536 271 31 630 212 97 120 291 2,074 26 152 263 693 224 67 426 44 61 139 46 353 1,091 721 252 22 688 875 143 1,476 23 114 18 140 10,891 662 14 321 161 514 211 2,247 2015 263 203 1,792 2,237 4,434 163 54 23 886 364 48 865 275 153 155 356 3,897 38 226 391 884 350 153 594 58 99 94 68 475 1,045 1,038 300 41 885 1,310 192 3,505 33 136 27 196 14,757 818 22 401 242 1,111 315 3,362 2035 295 385 2,775 3,440 4,526 237 110 40 1,201 578 87 1,467 473 278 251 473 7,702 60 357 611 1,403 539 172 1,007 85 185 173 118 834 914 1,599 519 85 1,719 2,257 319 8,889 48 240 46 348 26,412 1,190 33 685 421 2,749 546 6,243 US Total 33,793 49,335 85,123 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight 17 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Value Added Contribution of Unconventional Gas* Summary US State-L Level Labor Income Contribution of Unconventional Gas* Summary ($M) ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming US Total 2010 952 529 4,910 2,192 12,258 422 163 72 1,163 1,147 142 2,560 957 420 512 1,234 11,020 124 555 423 2,966 796 264 1,057 162 265 180 52 640 3,356 2,316 909 105 3,045 4,008 548 7,121 107 444 88 683 47,995 3,126 68 1,273 298 2,239 783 6,760 2015 1,183 791 7,264 3,197 18,162 587 226 108 2,034 1,622 214 3,555 1,326 665 702 1,572 20,005 177 814 613 3,794 1,272 675 1,529 214 429 128 75 841 3,160 3,325 1,318 190 3,942 6,033 689 16,806 153 655 132 986 64,768 3,866 101 1,634 441 4,563 1,167 8,815 2035 1,405 1,509 10,540 4,617 17,485 865 482 186 2,266 2,398 375 6,178 2,331 1,189 1,135 2,174 37,759 282 1,281 981 6,096 1,937 685 2,616 318 791 237 128 1,406 2,589 5,000 2,185 390 7,921 9,905 1,093 42,438 225 1,155 220 1,727 111,089 5,343 152 2,789 761 10,313 2,044 14,735 Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming 2010 583 430 2,314 1,553 5,958 344 116 61 912 860 113 1,828 716 321 347 708 5,492 100 460 343 1,851 616 206 724 104 207 133 41 497 1,461 1,871 731 79 2,031 1,993 406 3,975 87 353 70 537 22,840 1,710 54 889 243 1,091 611 2,753 2015 801 643 3,407 2,295 9,258 479 164 91 1,564 1,226 169 2,562 999 499 491 930 9,238 143 674 498 2,483 963 497 1,049 146 329 101 59 662 1,407 2,710 1,061 138 2,684 2,961 524 8,351 125 521 104 782 30,769 2,098 81 1,191 360 2,088 906 3,669 2035 1,069 1,241 5,020 3,397 9,236 702 334 158 1,860 1,943 295 4,374 1,734 892 819 1,396 16,361 227 1,064 791 4,135 1,500 534 1,794 230 606 189 99 1,097 1,277 4,075 1,775 282 5,225 4,885 856 20,349 184 921 173 1,371 53,427 2,952 122 2,086 617 4,697 1,590 6,196 133,405 196,516 331,728 US Total 71,727 104,951 176,154 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight 18 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES 4. Conclusion Unconventional gas activity is expected to make a significant contribution to all of the economies of the lower 48 states over the next 25 years. Traditional oil and gas producing states like Texas and Louisiana will continue to lead the way in terms of their absolute contributions to the US economy. But many new and emerging energy states will drive much of the growth in the coming years, and the economic activity generated by this increase in unconventional gas activity will also reach well beyond the traditional unconventional producing states. IHS 19 The Economic and Employment Contributions of Unconventional Gas Development in State Economies Appendix A. Economic Contributions by State and Year Prepared for: AMERICA'S NATURAL GAS ALLIANCE Submitted by: IHS Inc. 1150 Connecticut Avenue NW, Suite 401 Washington, DC 20036 June 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES About IHS (ihs.com) IHS Inc. (NYSE: IHS) is a leading source of information and insight in critical areas that shape today's business landscape, including energy and power; design and supply chain; defense, risk and security; environmental, health and safety, and sustainability; country and industry forecasting; and commodities, pricing and cost. IHS has been in business since 1959 and became a publicly traded company on the New York Stock Exchange in 2005. Headquartered in Englewood, Colorado, USA, IHS employs more than 5,100 people in more than 30 countries around the world. About IHS Global Insight IHS Global Insightis one of the leading economic analysis and forecasting firms in the world. With over 600 economists, statisticians, and industry specialists in 25 offices worldwide, IHS Global Insight has an established track record for providing rigorous, objective forecast analysis and data to governments and businesses around the world. Among our areas of expertise are the economic impact, tax implications, and job-creation dynamics within multiple sectors core to national, state and local economies. It helps governments and companies at all levels interpret the impact of proposed investments, policies, programs, and projects. IHS Global Insight was formed by the merger of DRI and WEFA. Still active in an advisory capacity to the firm is the original founder of WEFA, Lawrence R. Klein, the 1980 winner of the Nobel Prize in Economics. For more information, contact: Richard F. Fullenbaum Vice President, Public Sector, IHS Richard.Fullenbaum@ihs.com John W. Larson Vice President, Public Sector, IHS John.Larson@ihs.com For press information, contact: Jim Dorsey Senior Manager Media Relations, IHS Jim.Dorsey@ihs.com IHS 1150 Connecticut Avenue NW, Suite 401 Washington, DC 20036 © 2012 IHS. All information contained herein is obtained by IHS Inc. from sources believed by it to be accurate and reliable. All forecasts and predictions contained herein are believed by IHS, Inc. to be as accurate as the data and methodologies will allow. However, because of the possibilities of human and mechanical error, as well as other factors such as unforeseen and unforeseeable changes in political and economic circumstances beyond IHS's control, the information herein is provided "as is" without warranty of any kind and IHS Inc., AND ALL THIRD PARTY PROVIDERS MAKE NO REPRESENTATIONS OR WARRANTIES EXPRESS OR IMPLIED TO ANY SUBSCRIBER OR ANY OTHER PERSON OR ENTITY AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY OF THE INFORMATION OR FORECASTS CONTAINED HEREIN. ii JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Appendix A. Economic Contributions by State and Year Appendix A presents six different types of detailed tables by state in five-year increments over the forecast horizon (2010, 2015, 2020, 2025, 2030 and 2035). Results for the following four concepts are presented: 1) Employment Contribution 2) Value Added Contribution 3) Labor Income Contribution 4) Government Revenue and Private Lease Payments. Employment and value added contribution results are presented twice: 1) Alphabetical by State 2) Ranked by Total Contribution (where total contribution is the sum of direct, indirect, and induced concepts) Labor income and government revenue results are presented alphabetically by state only. The three contribution concepts (employment, value added, and labor income) are split out into direct, indirect and induced contributions with a separate table for each of our forecast years. A summary description of the tables is as follows: 1 - Employment Contribution: Alphabetical by State. These tables present the direct, indirect, induced, and total employment contributions for 2010, 2015, 2020, 2025, 2030, and 2035 alphabetically by state. 2- Employment Contribution by State: Ranked by Total Contribution. These tables present the direct, indirect, induced, and total employment contributions for 2010, 2015, 2020, 2025, 2030, and 2035 ranked by the total contribution for each of the years. 3 - Value Added Contribution: Alphabetical by State. These tables present the direct, indirect, induced, and total value added contributions for 2010, 2015, 2020, 2025, 2030, and 2035 alphabetically by state. 4 - Value Added Contribution by State: Ranked by Total Contribution. These tables present the direct, indirect, induced, and total value added contributions for 2010, 2015, 2020, 2025, 2030, and 2035 ranked by the total contribution for each of the years. 5 - Labor Income Contribution: Alphabetical by State. These tables present the direct, indirect, induced, and total value added contributions for 2010, 2015, 2020, 2025, 2030, and 2035 alphabetically by state. 6- Government Revenue and Private Lease Payments by State. These tables present detailed government revenue information for 2010, 2015, 2020, 2025, 2030, and 2035 alphabetically by state. IHS A-1 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Employment Contribution: Alphabetical by State US State-L Level Employment Contribution of Unconventional Gas*: 2010 (Number of workers) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming US Total Direct 1,195 0 13,640 4,718 22,535 0 187 0 3,204 952 0 2,814 516 315 658 2,145 29,896 0 0 136 6,968 352 92 4,133 90 104 505 0 592 6,797 408 102 0 4,979 8,636 670 13,594 0 61 0 142 73,744 10,404 0 923 0 6,871 137 14,753 Indirect 3,417 2,919 9,922 8,071 21,759 2,166 615 366 5,032 5,269 765 10,016 5,037 2,012 1,992 3,855 21,997 637 2,945 2,046 8,647 3,837 1,338 3,070 600 1,323 741 286 2,669 5,462 10,696 4,825 489 12,643 8,672 2,690 18,342 570 2,545 452 3,660 88,561 8,993 330 5,498 1,597 4,522 4,457 8,647 Induced 4,063 3,999 13,136 9,984 33,172 2,851 879 539 7,522 7,073 1,076 12,943 5,266 2,856 2,703 4,870 29,130 1,029 4,063 2,787 12,448 5,082 1,829 4,828 902 1,773 906 361 3,604 8,159 15,783 6,451 652 13,840 11,007 3,396 24,948 798 3,001 725 4,717 125,918 11,165 518 6,740 2,307 5,495 5,013 11,386 Total 8,675 6,918 36,698 22,773 77,466 5,017 1,681 905 15,758 13,294 1,841 25,773 10,819 5,183 5,353 10,870 81,022 1,666 7,008 4,968 28,063 9,271 3,259 12,031 1,591 3,199 2,153 647 6,865 20,417 26,887 11,377 1,141 31,462 28,315 6,756 56,884 1,368 5,607 1,176 8,519 288,222 30,561 848 13,162 3,904 16,888 9,608 34,787 237,968 326,999 443,691 1,008,658 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-2 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Employment Contribution of Unconventional Gas*: 2015 (Number of workers) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming US Total Direct 2,042 0 19,767 6,970 40,115 0 236 0 6,838 1,106 0 3,724 586 650 824 2,336 40,341 0 0 193 9,107 860 2,703 6,005 85 276 10 0 465 6,017 386 0 0 5,776 12,217 185 26,007 0 3 0 62 93,838 11,232 0 777 0 12,857 263 18,917 Indirect 4,960 4,341 14,930 11,736 35,280 2,999 869 550 8,328 7,601 1,150 14,380 7,100 3,082 2,910 5,321 35,273 913 4,359 3,002 12,248 5,811 2,953 4,477 866 2,127 789 410 3,742 5,607 15,684 7,078 861 17,085 13,278 3,704 34,594 820 3,813 677 5,404 121,994 11,532 491 7,612 2,360 8,115 6,599 9,673 Induced 5,670 6,023 19,222 14,560 51,130 4,016 1,258 798 12,236 10,093 1,616 18,282 7,521 4,362 3,861 6,596 49,168 1,477 5,905 4,025 16,571 7,827 3,772 6,945 1,285 2,739 944 529 5,064 7,993 22,977 9,493 1,006 18,504 16,267 4,627 50,423 1,148 4,411 1,093 6,856 169,486 13,829 770 9,364 3,438 10,408 7,424 17,173 Total 12,673 10,364 53,919 33,265 126,525 7,015 2,362 1,348 27,402 18,800 2,766 36,387 15,206 8,095 7,594 14,252 124,782 2,390 10,263 7,220 37,926 14,499 9,428 17,427 2,236 5,142 1,743 938 9,271 19,617 39,047 16,570 1,867 41,366 41,763 8,516 111,024 1,968 8,227 1,770 12,323 385,318 36,593 1,261 17,753 5,797 31,380 14,285 45,763 333,779 479,487 650,184 1,463,450 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-3 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Employment Contribution of Unconventional Gas*: 2020 (Number of workers) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 1,232 0 22,868 7,582 43,714 0 402 0 3,274 734 0 5,295 898 782 880 2,517 40,665 0 0 355 11,554 917 1,300 7,702 82 332 93 0 676 4,928 584 188 0 8,875 14,598 216 41,258 0 93 0 147 125,882 12,472 0 838 0 18,520 321 20,698 Indirect 5,519 5,518 17,673 14,066 38,518 3,586 1,182 692 8,916 9,198 1,427 17,648 8,859 3,815 3,509 6,455 41,093 1,111 5,355 3,667 15,120 7,087 2,857 5,583 1,045 2,695 1,031 511 4,540 5,224 18,639 8,877 1,118 22,668 15,939 4,670 50,276 977 4,794 828 6,761 158,308 13,281 597 9,448 2,919 11,335 8,252 10,630 Induced 6,137 7,572 22,430 17,352 54,818 4,727 1,658 997 13,232 11,984 2,009 22,778 9,307 5,326 4,645 7,732 58,797 1,767 7,211 4,842 19,979 9,388 3,815 8,596 1,551 3,407 1,250 661 6,156 7,130 27,377 11,847 1,269 24,203 19,389 5,743 73,321 1,364 5,487 1,341 8,504 215,755 15,803 933 11,501 4,205 14,368 9,146 18,675 Total 12,888 13,090 62,971 39,000 137,050 8,312 3,242 1,689 25,422 21,915 3,437 45,721 19,065 9,923 9,034 16,705 140,556 2,878 12,566 8,865 46,653 17,393 7,972 21,881 2,677 6,433 2,375 1,171 11,371 17,282 46,600 20,912 2,387 55,747 49,925 10,629 164,856 2,341 10,373 2,169 15,412 499,946 41,556 1,530 21,787 7,123 44,223 17,719 50,002 US Total 403,473 593,817 797,483 1,794,773 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-4 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Employment Contribution of Unconventional Gas*: 2025 (Number of workers) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 628 0 23,720 7,247 37,733 0 363 0 1,084 220 0 4,918 820 798 874 2,345 44,245 0 0 324 10,680 778 765 7,843 74 364 12 0 602 4,794 512 0 0 8,048 15,245 163 41,140 0 22 0 91 127,899 13,054 0 772 0 18,748 333 23,700 Indirect 5,440 5,745 18,350 13,892 33,601 3,518 1,147 695 8,611 9,263 1,459 17,257 8,915 3,993 3,587 6,448 46,135 1,112 5,241 3,562 14,995 7,003 2,663 5,649 1,050 2,804 1,015 503 4,448 5,052 18,108 8,829 1,190 22,019 16,289 4,620 50,463 944 4,871 829 6,887 161,495 13,810 579 9,506 2,984 11,498 8,413 12,010 Induced 5,950 7,917 23,414 17,412 48,298 4,633 1,653 1,015 12,858 11,981 2,076 22,568 9,451 5,511 4,740 7,711 67,437 1,768 7,279 4,771 19,278 9,404 3,672 8,676 1,575 3,511 1,256 662 6,142 6,720 27,049 12,018 1,340 23,471 20,097 5,821 75,445 1,351 5,573 1,372 8,678 222,082 16,613 932 11,685 4,265 14,828 9,411 21,129 Total 12,018 13,662 65,484 38,551 119,632 8,151 3,163 1,710 22,552 21,463 3,536 44,743 19,186 10,302 9,201 16,505 157,818 2,881 12,519 8,657 44,953 17,184 7,099 22,168 2,699 6,679 2,284 1,165 11,192 16,565 45,669 20,847 2,531 53,538 51,631 10,604 167,048 2,295 10,466 2,201 15,656 511,476 43,477 1,510 21,963 7,249 45,074 18,156 56,840 US Total 400,958 598,495 812,501 1,811,954 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-5 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Employment Contribution of Unconventional Gas*: 2030 (Number of workers) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 1,047 0 24,272 7,461 35,346 0 438 0 4,926 835 0 5,634 986 891 902 2,365 44,571 0 0 396 11,907 731 681 8,702 65 405 13 0 709 4,207 611 0 0 9,588 16,580 136 47,761 0 31 0 98 140,803 13,412 0 815 0 21,154 382 26,183 Indirect 6,198 6,395 18,958 14,699 31,695 3,715 1,270 738 10,515 10,425 1,579 18,303 9,744 4,442 3,950 6,992 47,988 1,189 5,523 3,724 16,346 7,487 2,803 6,182 1,118 3,095 1,121 536 4,686 4,949 18,803 9,487 1,331 24,532 17,607 4,881 56,790 976 5,357 893 7,549 175,989 14,453 600 10,389 3,236 12,883 9,171 13,152 Induced 6,546 8,852 24,089 18,490 45,636 4,797 1,824 1,087 15,390 13,499 2,255 24,293 10,204 5,997 5,100 8,166 70,266 1,873 7,787 5,014 20,728 9,995 3,901 9,406 1,680 3,799 1,403 713 6,525 6,503 28,208 13,055 1,482 25,813 21,666 6,246 84,671 1,416 6,066 1,478 9,412 240,624 17,447 980 12,750 4,556 16,492 10,150 22,994 Total 13,791 15,246 67,319 40,650 112,677 8,512 3,532 1,825 30,831 24,759 3,833 48,229 20,934 11,330 9,952 17,523 162,825 3,063 13,310 9,134 48,982 18,213 7,386 24,290 2,862 7,299 2,537 1,249 11,920 15,659 47,622 22,542 2,812 59,933 55,853 11,264 189,222 2,391 11,453 2,372 17,059 557,416 45,312 1,581 23,953 7,793 50,529 19,703 62,329 US Total 435,045 644,443 871,324 1,950,812 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-6 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Employment Contribution of Unconventional Gas*: 2035 (Number of workers) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 401 0 28,524 8,617 39,723 0 673 0 990 113 0 7,879 1,503 1,150 1,035 2,879 53,428 0 0 615 15,951 822 614 10,746 69 498 17 0 1,063 4,822 927 0 0 14,378 20,537 142 70,734 0 6 0 89 170,896 14,640 0 1,069 0 30,390 506 32,953 Indirect 7,608 8,273 22,526 18,016 36,084 4,568 1,694 920 12,091 12,728 1,975 22,797 12,371 5,723 5,024 8,794 59,587 1,461 6,854 4,569 20,855 9,341 3,368 7,699 1,402 3,939 1,438 675 5,828 5,894 22,875 11,798 1,729 32,668 21,851 6,071 79,807 1,173 6,742 1,107 9,522 216,434 16,392 724 13,368 4,088 18,110 11,585 16,664 Induced 7,858 11,465 28,673 22,861 52,036 5,813 2,403 1,374 17,822 16,422 2,842 30,981 12,963 7,654 6,411 10,152 87,540 2,312 9,780 6,172 26,574 12,474 4,786 11,659 2,110 4,780 1,823 901 8,173 7,747 34,575 16,473 1,916 34,303 26,874 7,894 119,518 1,731 7,621 1,852 11,876 295,411 19,807 1,198 16,296 5,689 23,121 12,779 29,176 Total 15,866 19,737 79,723 49,494 127,843 10,380 4,770 2,294 30,903 29,262 4,818 61,657 26,837 14,526 12,470 21,825 200,555 3,774 16,634 11,356 63,380 22,638 8,768 30,105 3,582 9,216 3,278 1,576 15,064 18,462 58,377 28,271 3,645 81,349 69,261 14,107 270,058 2,904 14,368 2,959 21,487 682,740 50,839 1,922 30,732 9,777 71,620 24,871 78,792 US Total 539,398 806,810 1,092,669 2,438,877 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-7 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Employment Contribution by State: Ranked by Total Contribution US State-L Level Employment Contribution of Unconventional Gas*: 2010 (Number of workers ranked by total employment contribution) Texas Louisiana Colorado Pennsylvania Arkansas Wyoming Ohio Utah Oklahoma Michigan New York Illinois California New Mexico West Virginia Florida Georgia Virginia Missouri North Carolina Kentucky Indiana Wisconsin Minnesota Alabama Tennessee Maryland Arizona New Jersey Oregon South Carolina Kansas Iowa Connecticut Massachusetts Washington Mississippi Nebraska Nevada Idaho Delaware Maine Montana Rhode Island South Dakota North Dakota District of Columbia Vermont New Hampshire US Total Direct 73,744 29,896 22,535 13,594 13,640 14,753 4,979 10,404 8,636 6,968 408 2,814 4,718 6,797 6,871 3,204 952 923 4,133 102 2,145 516 137 352 1,195 142 0 0 592 670 61 658 315 0 136 0 92 104 505 0 187 0 90 0 0 0 0 0 0 Indirect 88,561 21,997 21,759 18,342 9,922 8,647 12,643 8,993 8,672 8,647 10,696 10,016 8,071 5,462 4,522 5,032 5,269 5,498 3,070 4,825 3,855 5,037 4,457 3,837 3,417 3,660 2,945 2,919 2,669 2,690 2,545 1,992 2,012 2,166 2,046 1,597 1,338 1,323 741 765 615 637 600 570 452 489 366 330 286 Induced 125,918 29,130 33,172 24,948 13,136 11,386 13,840 11,165 11,007 12,448 15,783 12,943 9,984 8,159 5,495 7,522 7,073 6,740 4,828 6,451 4,870 5,266 5,013 5,082 4,063 4,717 4,063 3,999 3,604 3,396 3,001 2,703 2,856 2,851 2,787 2,307 1,829 1,773 906 1,076 879 1,029 902 798 725 652 539 518 361 Total 288,222 81,022 77,466 56,884 36,698 34,787 31,462 30,561 28,315 28,063 26,887 25,773 22,773 20,417 16,888 15,758 13,294 13,162 12,031 11,377 10,870 10,819 9,608 9,271 8,675 8,519 7,008 6,918 6,865 6,756 5,607 5,353 5,183 5,017 4,968 3,904 3,259 3,199 2,153 1,841 1,681 1,666 1,591 1,368 1,176 1,141 905 848 647 237,968 326,999 443,691 1,008,658 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-8 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Employment Contribution of Unconventional Gas*: 2015 (Number of workers ranked by total employment contribution) Texas Colorado Louisiana Pennsylvania Arkansas Oklahoma Ohio New York Michigan Wyoming Utah Illinois California West Virginia Florida New Mexico Georgia Virginia Missouri North Carolina Indiana Minnesota Wisconsin Kentucky Alabama Tennessee Arizona Maryland Mississippi New Jersey Oregon South Carolina Iowa Kansas Massachusetts Connecticut Washington Nebraska Idaho Maine Delaware Montana Rhode Island North Dakota South Dakota Nevada District of Columbia Vermont New Hampshire US Total Direct 93,838 40,115 40,341 26,007 19,767 12,217 5,776 386 9,107 18,917 11,232 3,724 6,970 12,857 6,838 6,017 1,106 777 6,005 0 586 860 263 2,336 2,042 62 0 0 2,703 465 185 3 650 824 193 0 0 276 0 0 236 85 0 0 0 10 0 0 0 Indirect 121,994 35,280 35,273 34,594 14,930 13,278 17,085 15,684 12,248 9,673 11,532 14,380 11,736 8,115 8,328 5,607 7,601 7,612 4,477 7,078 7,100 5,811 6,599 5,321 4,960 5,404 4,341 4,359 2,953 3,742 3,704 3,813 3,082 2,910 3,002 2,999 2,360 2,127 1,150 913 869 866 820 861 677 789 550 491 410 Induced 169,486 51,130 49,168 50,423 19,222 16,267 18,504 22,977 16,571 17,173 13,829 18,282 14,560 10,408 12,236 7,993 10,093 9,364 6,945 9,493 7,521 7,827 7,424 6,596 5,670 6,856 6,023 5,905 3,772 5,064 4,627 4,411 4,362 3,861 4,025 4,016 3,438 2,739 1,616 1,477 1,258 1,285 1,148 1,006 1,093 944 798 770 529 Total 385,318 126,525 124,782 111,024 53,919 41,763 41,366 39,047 37,926 45,763 36,593 36,387 33,265 31,380 27,402 19,617 18,800 17,753 17,427 16,570 15,206 14,499 14,285 14,252 12,673 12,323 10,364 10,263 9,428 9,271 8,516 8,227 8,095 7,594 7,220 7,015 5,797 5,142 2,766 2,390 2,362 2,236 1,968 1,867 1,770 1,743 1,348 1,261 938 333,779 479,487 650,184 1,463,450 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-9 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Employment Contribution of Unconventional Gas*: 2020 (Number of workers ranked by total employment contribution) Texas Pennsylvania Louisiana Colorado Arkansas Ohio Oklahoma New York Michigan Illinois West Virginia Utah Wyoming California Florida Georgia Missouri Virginia North Carolina Indiana Wisconsin Minnesota New Mexico Kentucky Tennessee Arizona Alabama Maryland New Jersey Oregon South Carolina Iowa Kansas Massachusetts Connecticut Mississippi Washington Nebraska Idaho Delaware Maine Montana North Dakota Nevada Rhode Island South Dakota District of Columbia Vermont New Hampshire Direct 125,882 41,258 40,665 43,714 22,868 8,875 14,598 584 11,554 5,295 18,520 12,472 20,698 7,582 3,274 734 7,702 838 188 898 321 917 4,928 2,517 147 0 1,232 0 676 216 93 782 880 355 0 1,300 0 332 0 402 0 82 0 93 0 0 0 0 0 Indirect 158,308 50,276 41,093 38,518 17,673 22,668 15,939 18,639 15,120 17,648 11,335 13,281 10,630 14,066 8,916 9,198 5,583 9,448 8,877 8,859 8,252 7,087 5,224 6,455 6,761 5,518 5,519 5,355 4,540 4,670 4,794 3,815 3,509 3,667 3,586 2,857 2,919 2,695 1,427 1,182 1,111 1,045 1,118 1,031 977 828 692 597 511 Induced 215,755 73,321 58,797 54,818 22,430 24,203 19,389 27,377 19,979 22,778 14,368 15,803 18,675 17,352 13,232 11,984 8,596 11,501 11,847 9,307 9,146 9,388 7,130 7,732 8,504 7,572 6,137 7,211 6,156 5,743 5,487 5,326 4,645 4,842 4,727 3,815 4,205 3,407 2,009 1,658 1,767 1,551 1,269 1,250 1,364 1,341 997 933 661 Total 499,946 164,856 140,556 137,050 62,971 55,747 49,925 46,600 46,653 45,721 44,223 41,556 50,002 39,000 25,422 21,915 21,881 21,787 20,912 19,065 17,719 17,393 17,282 16,705 15,412 13,090 12,888 12,566 11,371 10,629 10,373 9,923 9,034 8,865 8,312 7,972 7,123 6,433 3,437 3,242 2,878 2,677 2,387 2,375 2,341 2,169 1,689 1,530 1,171 US Total 403,473 593,817 797,483 1,794,773 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-10 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Employment Contribution of Unconventional Gas*: 2025 (Number of workers ranked by total employment contribution) Texas Pennsylvania Louisiana Colorado Arkansas Ohio Oklahoma Wyoming New York West Virginia Michigan Illinois Utah California Florida Missouri Virginia Georgia North Carolina Indiana Wisconsin Minnesota New Mexico Kentucky Tennessee Arizona Maryland Alabama New Jersey Oregon South Carolina Iowa Kansas Massachusetts Connecticut Washington Mississippi Nebraska Idaho Delaware Maine Montana North Dakota Rhode Island Nevada South Dakota District of Columbia Vermont New Hampshire Direct 127,899 41,140 44,245 37,733 23,720 8,048 15,245 23,700 512 18,748 10,680 4,918 13,054 7,247 1,084 7,843 772 220 0 820 333 778 4,794 2,345 91 0 0 628 602 163 22 798 874 324 0 0 765 364 0 363 0 74 0 0 12 0 0 0 0 Indirect 161,495 50,463 46,135 33,601 18,350 22,019 16,289 12,010 18,108 11,498 14,995 17,257 13,810 13,892 8,611 5,649 9,506 9,263 8,829 8,915 8,413 7,003 5,052 6,448 6,887 5,745 5,241 5,440 4,448 4,620 4,871 3,993 3,587 3,562 3,518 2,984 2,663 2,804 1,459 1,147 1,112 1,050 1,190 944 1,015 829 695 579 503 Induced 222,082 75,445 67,437 48,298 23,414 23,471 20,097 21,129 27,049 14,828 19,278 22,568 16,613 17,412 12,858 8,676 11,685 11,981 12,018 9,451 9,411 9,404 6,720 7,711 8,678 7,917 7,279 5,950 6,142 5,821 5,573 5,511 4,740 4,771 4,633 4,265 3,672 3,511 2,076 1,653 1,768 1,575 1,340 1,351 1,256 1,372 1,015 932 662 Total 511,476 167,048 157,818 119,632 65,484 53,538 51,631 56,840 45,669 45,074 44,953 44,743 43,477 38,551 22,552 22,168 21,963 21,463 20,847 19,186 18,156 17,184 16,565 16,505 15,656 13,662 12,519 12,018 11,192 10,604 10,466 10,302 9,201 8,657 8,151 7,249 7,099 6,679 3,536 3,163 2,881 2,699 2,531 2,295 2,284 2,201 1,710 1,510 1,165 US Total 400,958 598,495 812,501 1,811,954 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-11 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Employment Contribution of Unconventional Gas*: 2030 (Number of workers ranked by total employment contribution) Texas Pennsylvania Louisiana Colorado Arkansas Ohio Oklahoma West Virginia Wyoming Michigan Illinois New York Utah California Florida Georgia Missouri Virginia North Carolina Indiana Wisconsin Minnesota Kentucky Tennessee New Mexico Arizona Alabama Maryland New Jersey South Carolina Iowa Oregon Kansas Massachusetts Connecticut Washington Mississippi Nebraska Idaho Delaware Maine Montana North Dakota Nevada Rhode Island South Dakota District of Columbia Vermont New Hampshire Direct 140,803 47,761 44,571 35,346 24,272 9,588 16,580 21,154 26,183 11,907 5,634 611 13,412 7,461 4,926 835 8,702 815 0 986 382 731 2,365 98 4,207 0 1,047 0 709 31 891 136 902 396 0 0 681 405 0 438 0 65 0 13 0 0 0 0 0 Indirect 175,989 56,790 47,988 31,695 18,958 24,532 17,607 12,883 13,152 16,346 18,303 18,803 14,453 14,699 10,515 10,425 6,182 10,389 9,487 9,744 9,171 7,487 6,992 7,549 4,949 6,395 6,198 5,523 4,686 5,357 4,442 4,881 3,950 3,724 3,715 3,236 2,803 3,095 1,579 1,270 1,189 1,118 1,331 1,121 976 893 738 600 536 Induced 240,624 84,671 70,266 45,636 24,089 25,813 21,666 16,492 22,994 20,728 24,293 28,208 17,447 18,490 15,390 13,499 9,406 12,750 13,055 10,204 10,150 9,995 8,166 9,412 6,503 8,852 6,546 7,787 6,525 6,066 5,997 6,246 5,100 5,014 4,797 4,556 3,901 3,799 2,255 1,824 1,873 1,680 1,482 1,403 1,416 1,478 1,087 980 713 Total 557,416 189,222 162,825 112,677 67,319 59,933 55,853 50,529 62,329 48,982 48,229 47,622 45,312 40,650 30,831 24,759 24,290 23,953 22,542 20,934 19,703 18,213 17,523 17,059 15,659 15,246 13,791 13,310 11,920 11,453 11,330 11,264 9,952 9,134 8,512 7,793 7,386 7,299 3,833 3,532 3,063 2,862 2,812 2,537 2,391 2,372 1,825 1,581 1,249 US Total 435,045 644,443 871,324 1,950,812 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-12 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Employment Contribution of Unconventional Gas*: 2035 (Number of workers ranked by total employment contribution) Texas Pennsylvania Louisiana Colorado Ohio Arkansas West Virginia Oklahoma Wyoming Michigan Illinois New York Utah California Florida Virginia Missouri Georgia North Carolina Indiana Wisconsin Minnesota Kentucky Tennessee Arizona New Mexico Maryland Alabama New Jersey Iowa South Carolina Oregon Kansas Massachusetts Connecticut Washington Nebraska Mississippi Idaho Delaware Maine North Dakota Montana Nevada South Dakota Rhode Island District of Columbia Vermont New Hampshire Direct 170,896 70,734 53,428 39,723 14,378 28,524 30,390 20,537 32,953 15,951 7,879 927 14,640 8,617 990 1,069 10,746 113 0 1,503 506 822 2,879 89 0 4,822 0 401 1,063 1,150 6 142 1,035 615 0 0 498 614 0 673 0 0 69 17 0 0 0 0 0 Indirect 216,434 79,807 59,587 36,084 32,668 22,526 18,110 21,851 16,664 20,855 22,797 22,875 16,392 18,016 12,091 13,368 7,699 12,728 11,798 12,371 11,585 9,341 8,794 9,522 8,273 5,894 6,854 7,608 5,828 5,723 6,742 6,071 5,024 4,569 4,568 4,088 3,939 3,368 1,975 1,694 1,461 1,729 1,402 1,438 1,107 1,173 920 724 675 Induced 295,411 119,518 87,540 52,036 34,303 28,673 23,121 26,874 29,176 26,574 30,981 34,575 19,807 22,861 17,822 16,296 11,659 16,422 16,473 12,963 12,779 12,474 10,152 11,876 11,465 7,747 9,780 7,858 8,173 7,654 7,621 7,894 6,411 6,172 5,813 5,689 4,780 4,786 2,842 2,403 2,312 1,916 2,110 1,823 1,852 1,731 1,374 1,198 901 Total 682,740 270,058 200,555 127,843 81,349 79,723 71,620 69,261 78,792 63,380 61,657 58,377 50,839 49,494 30,903 30,732 30,105 29,262 28,271 26,837 24,871 22,638 21,825 21,487 19,737 18,462 16,634 15,866 15,064 14,526 14,368 14,107 12,470 11,356 10,380 9,777 9,216 8,768 4,818 4,770 3,774 3,645 3,582 3,278 2,959 2,904 2,294 1,922 1,576 US Total 539,398 806,810 1,092,669 2,438,877 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-13 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Value Added Contribution: Alphabetical by State US State-L Level Value Added Contribution of Unconventional Gas*: 2010 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 276 0 2,745 505 5,587 0 25 0 180 109 0 395 54 36 99 451 5,664 0 0 13 859 45 4 314 35 8 41 0 81 2,091 61 5 0 539 1,924 50 2,444 0 3 0 12 19,621 1,256 0 179 0 1,261 17 5,014 Indirect 341 246 1,005 815 2,913 197 63 32 413 472 66 1,000 478 171 200 376 2,497 52 255 190 949 355 122 316 60 120 65 25 253 529 994 414 55 1,302 1,053 242 2,162 49 216 37 310 13,636 855 29 556 134 487 386 807 Induced 335 283 1,161 871 3,758 224 74 40 570 566 77 1,165 424 213 213 407 2,859 72 300 220 1,159 396 138 427 67 137 74 27 306 736 1,260 490 50 1,204 1,031 256 2,515 57 224 51 361 14,739 1,015 39 538 164 491 380 940 Total 952 529 4,910 2,192 12,258 422 163 72 1,163 1,147 142 2,560 957 420 512 1,234 11,020 124 555 423 2,966 796 264 1,057 162 265 180 52 640 3,356 2,316 909 105 3,045 4,008 548 7,121 107 444 88 683 47,995 3,126 68 1,273 298 2,239 783 6,760 US Total 52,004 38,301 43,101 133,405 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-14 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Value Added Contribution of Unconventional Gas*: 2015 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 243 0 4,068 751 7,777 0 32 0 387 136 0 523 62 75 105 519 11,039 0 0 18 977 112 119 461 32 21 2 0 73 1,898 50 0 0 620 2,922 23 7,063 0 1 0 5 26,463 1,527 0 165 0 2,751 34 5,953 Indirect 477 364 1,508 1,181 4,613 275 90 48 695 681 100 1,413 667 266 295 513 4,151 74 379 279 1,302 541 258 458 89 197 65 36 349 556 1,458 605 110 1,743 1,595 331 4,471 72 324 56 458 18,662 1,096 43 746 198 880 573 1,099 Induced 463 426 1,688 1,265 5,772 313 105 60 953 804 114 1,619 597 325 302 540 4,815 103 434 316 1,514 619 298 609 94 212 61 39 418 706 1,816 712 81 1,579 1,517 334 5,272 82 330 76 523 19,643 1,243 58 723 243 932 560 1,763 Total 1,183 791 7,264 3,197 18,162 587 226 108 2,034 1,622 214 3,555 1,326 665 702 1,572 20,005 177 814 613 3,794 1,272 675 1,529 214 429 128 75 841 3,160 3,325 1,318 190 3,942 6,033 689 16,806 153 655 132 986 64,768 3,866 101 1,634 441 4,563 1,167 8,815 US Total 77,007 56,441 63,069 196,516 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-15 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Value Added Contribution of Unconventional Gas*: 2020 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 142 0 4,624 823 7,949 0 54 0 185 77 0 727 94 89 110 503 14,111 0 0 32 1,116 119 57 587 28 25 9 0 106 1,456 60 9 0 936 3,422 27 10,777 0 5 0 13 32,840 1,714 0 170 0 3,832 40 6,394 Indirect 525 459 1,781 1,397 4,967 326 126 61 720 805 124 1,741 826 328 349 613 4,897 90 464 343 1,593 653 254 568 106 252 85 45 426 525 1,744 752 143 2,338 1,894 417 6,585 85 405 68 573 23,722 1,254 52 924 246 1,216 713 1,200 Induced 488 539 1,959 1,488 6,135 366 141 75 965 941 142 2,035 735 394 360 625 5,741 123 527 383 1,818 736 293 753 112 263 83 49 508 617 2,162 885 102 2,091 1,800 412 7,774 97 411 93 648 24,945 1,411 70 883 298 1,285 689 1,910 Total 1,155 998 8,364 3,708 19,051 693 321 135 1,871 1,823 266 4,502 1,656 811 819 1,741 24,749 213 992 758 4,527 1,507 604 1,908 246 540 177 94 1,040 2,599 3,967 1,645 245 5,366 7,116 856 25,136 182 822 161 1,233 81,507 4,379 123 1,977 544 6,333 1,442 9,503 US Total 93,261 69,779 77,363 240,403 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-16 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Value Added Contribution of Unconventional Gas*: 2025 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 79 0 4,850 785 6,932 0 49 0 65 23 0 677 86 91 107 457 16,678 0 0 29 996 101 33 594 26 27 2 0 94 1,263 51 0 0 846 3,606 21 11,507 0 2 0 8 34,194 1,821 0 154 0 4,011 42 7,211 Indirect 517 476 1,853 1,380 4,365 321 122 62 688 808 127 1,698 827 343 357 609 5,559 90 451 334 1,568 644 239 576 107 266 83 44 419 510 1,709 744 156 2,263 1,944 408 6,730 83 413 69 586 24,380 1,309 50 929 253 1,243 730 1,348 Induced 470 567 2,045 1,483 5,367 359 139 76 910 935 147 2,003 747 407 369 622 6,599 124 526 377 1,742 734 280 759 114 272 81 49 505 579 2,135 890 109 2,019 1,866 413 8,015 96 420 95 664 25,648 1,482 70 893 304 1,326 710 2,162 Total 1,066 1,043 8,749 3,648 16,664 679 310 138 1,662 1,766 275 4,378 1,660 841 834 1,689 28,837 214 977 740 4,306 1,480 551 1,929 246 565 167 93 1,019 2,352 3,895 1,634 265 5,127 7,416 842 26,252 179 835 163 1,258 84,223 4,613 121 1,976 557 6,580 1,482 10,722 US Total 97,518 70,793 78,706 247,017 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-17 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Value Added Contribution of Unconventional Gas*: 2030 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming US Total Direct 84 0 4,900 804 6,360 0 59 0 277 97 0 772 104 101 111 441 17,429 0 0 36 1,079 95 30 657 22 30 2 0 111 1,146 57 0 0 1,002 3,872 17 12,973 0 3 0 8 36,540 1,885 0 161 0 4,434 48 7,758 Indirect 587 529 1,913 1,451 4,103 338 137 66 853 918 138 1,812 902 381 392 659 5,792 96 471 350 1,717 686 250 629 113 297 92 47 445 505 1,782 793 174 2,530 2,092 426 7,582 85 454 74 642 26,353 1,368 52 1,017 275 1,387 796 1,465 Induced 523 635 2,102 1,567 5,033 371 154 82 1,140 1,069 160 2,172 809 444 400 659 6,878 132 558 397 1,883 780 295 825 121 295 91 53 539 556 2,229 962 122 2,241 2,014 439 9,047 100 460 102 721 27,767 1,553 73 974 327 1,476 768 2,354 Total 1,193 1,164 8,914 3,822 15,496 709 349 148 2,270 2,084 298 4,757 1,814 926 904 1,759 30,100 228 1,030 783 4,679 1,561 575 2,111 257 622 185 100 1,095 2,206 4,069 1,754 296 5,774 7,978 883 29,603 186 917 176 1,372 90,660 4,807 125 2,152 602 7,297 1,613 11,578 103,505 76,021 84,456 263,982 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-18 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Value Added Contribution of Unconventional Gas*: 2035 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming US Total Direct 58 0 5,769 928 7,123 0 90 0 61 14 0 1,087 158 131 130 525 21,981 0 0 56 1,441 107 26 814 24 37 3 0 167 1,323 85 0 0 1,500 4,809 18 18,808 0 2 0 7 44,731 2,038 0 213 0 6,299 64 9,894 Indirect 722 684 2,276 1,769 4,664 415 186 82 953 1,105 173 2,289 1,142 491 498 831 7,208 119 583 433 2,222 856 299 782 143 382 117 60 559 606 2,182 978 230 3,405 2,598 525 10,741 103 573 92 810 32,359 1,552 62 1,326 350 1,941 1,011 1,855 Induced 624 826 2,495 1,920 5,698 450 205 104 1,252 1,280 202 2,802 1,031 567 506 818 8,569 163 699 492 2,433 974 359 1,020 151 372 117 68 680 660 2,732 1,206 160 3,017 2,498 550 12,889 123 581 128 909 33,998 1,753 89 1,250 411 2,072 970 2,986 Total 1,405 1,509 10,540 4,617 17,485 865 482 186 2,266 2,398 375 6,178 2,331 1,189 1,135 2,174 37,759 282 1,281 981 6,096 1,937 685 2,616 318 791 237 128 1,406 2,589 5,000 2,185 390 7,921 9,905 1,093 42,438 225 1,155 220 1,727 111,089 5,343 152 2,789 761 10,313 2,044 14,735 130,520 95,346 105,862 331,728 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-19 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Value Added Contribution by State: Ranked by Total Contribution US State-L Level Value Added Contribution of Unconventional Gas*: 2010 ($M ranked by total value added contribution) Texas Colorado Louisiana Pennsylvania Wyoming Arkansas Oklahoma New Mexico Utah Ohio Michigan Illinois New York West Virginia California Virginia Kentucky Florida Georgia Missouri Indiana Alabama North Carolina Minnesota Wisconsin Tennessee New Jersey Maryland Oregon Arizona Kansas South Carolina Massachusetts Connecticut Iowa Washington Nebraska Mississippi Nevada Delaware Montana Idaho Maine Rhode Island North Dakota South Dakota District of Columbia Vermont New Hampshire Direct 19,621 5,587 5,664 2,444 5,014 2,745 1,924 2,091 1,256 539 859 395 61 1,261 505 179 451 180 109 314 54 276 5 45 17 12 81 0 50 0 99 3 13 0 36 0 8 4 41 25 35 0 0 0 0 0 0 0 0 Indirect 13,636 2,913 2,497 2,162 807 1,005 1,053 529 855 1,302 949 1,000 994 487 815 556 376 413 472 316 478 341 414 355 386 310 253 255 242 246 200 216 190 197 171 134 120 122 65 63 60 66 52 49 55 37 32 29 25 Induced 14,739 3,758 2,859 2,515 940 1,161 1,031 736 1,015 1,204 1,159 1,165 1,260 491 871 538 407 570 566 427 424 335 490 396 380 361 306 300 256 283 213 224 220 224 213 164 137 138 74 74 67 77 72 57 50 51 40 39 27 Total 47,995 12,258 11,020 7,121 6,760 4,910 4,008 3,356 3,126 3,045 2,966 2,560 2,316 2,239 2,192 1,273 1,234 1,163 1,147 1,057 957 952 909 796 783 683 640 555 548 529 512 444 423 422 420 298 265 264 180 163 162 142 124 107 105 88 72 68 52 US Total 52,004 38,301 43,101 133,405 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-20 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Value Added Contribution of Unconventional Gas*: 2015 ($M ranked by total value added contribution) Texas Louisiana Colorado Pennsylvania Wyoming Arkansas Oklahoma West Virginia Ohio Utah Michigan Illinois New York California New Mexico Florida Virginia Georgia Kentucky Missouri Indiana North Carolina Minnesota Alabama Wisconsin Tennessee New Jersey Maryland Arizona Kansas Oregon Mississippi Iowa South Carolina Massachusetts Connecticut Washington Nebraska Delaware Montana Idaho North Dakota Maine Rhode Island South Dakota Nevada District of Columbia Vermont New Hampshire Direct 26,463 11,039 7,777 7,063 5,953 4,068 2,922 2,751 620 1,527 977 523 50 751 1,898 387 165 136 519 461 62 0 112 243 34 5 73 0 0 105 23 119 75 1 18 0 0 21 32 32 0 0 0 0 0 2 0 0 0 Indirect 18,662 4,151 4,613 4,471 1,099 1,508 1,595 880 1,743 1,096 1,302 1,413 1,458 1,181 556 695 746 681 513 458 667 605 541 477 573 458 349 379 364 295 331 258 266 324 279 275 198 197 90 89 100 110 74 72 56 65 48 43 36 Induced 19,643 4,815 5,772 5,272 1,763 1,688 1,517 932 1,579 1,243 1,514 1,619 1,816 1,265 706 953 723 804 540 609 597 712 619 463 560 523 418 434 426 302 334 298 325 330 316 313 243 212 105 94 114 81 103 82 76 61 60 58 39 Total 64,768 20,005 18,162 16,806 8,815 7,264 6,033 4,563 3,942 3,866 3,794 3,555 3,325 3,197 3,160 2,034 1,634 1,622 1,572 1,529 1,326 1,318 1,272 1,183 1,167 986 841 814 791 702 689 675 665 655 613 587 441 429 226 214 214 190 177 153 132 128 108 101 75 US Total 77,007 56,441 63,069 196,516 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-21 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Value Added Contribution of Unconventional Gas*: 2020 ($M ranked by total value added contribution) Texas Pennsylvania Louisiana Colorado Wyoming Arkansas Oklahoma West Virginia Ohio Michigan Illinois Utah New York California New Mexico Virginia Missouri Florida Georgia Kentucky Indiana North Carolina Minnesota Wisconsin Tennessee Alabama New Jersey Arizona Maryland Oregon South Carolina Kansas Iowa Massachusetts Connecticut Mississippi Washington Nebraska Delaware Idaho Montana North Dakota Maine Rhode Island Nevada South Dakota District of Columbia Vermont New Hampshire Direct 32,840 10,777 14,111 7,949 6,394 4,624 3,422 3,832 936 1,116 727 1,714 60 823 1,456 170 587 185 77 503 94 9 119 40 13 142 106 0 0 27 5 110 89 32 0 57 0 25 54 0 28 0 0 0 9 0 0 0 0 Indirect 23,722 6,585 4,897 4,967 1,200 1,781 1,894 1,216 2,338 1,593 1,741 1,254 1,744 1,397 525 924 568 720 805 613 826 752 653 713 573 525 426 459 464 417 405 349 328 343 326 254 246 252 126 124 106 143 90 85 85 68 61 52 45 Induced 24,945 7,774 5,741 6,135 1,910 1,959 1,800 1,285 2,091 1,818 2,035 1,411 2,162 1,488 617 883 753 965 941 625 735 885 736 689 648 488 508 539 527 412 411 360 394 383 366 293 298 263 141 142 112 102 123 97 83 93 75 70 49 Total 81,507 25,136 24,749 19,051 9,503 8,364 7,116 6,333 5,366 4,527 4,502 4,379 3,967 3,708 2,599 1,977 1,908 1,871 1,823 1,741 1,656 1,645 1,507 1,442 1,233 1,155 1,040 998 992 856 822 819 811 758 693 604 544 540 321 266 246 245 213 182 177 161 135 123 94 US Total 93,261 69,779 77,363 240,403 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-22 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Value Added Contribution of Unconventional Gas*: 2025 ($M ranked by total value added contribution) Texas Louisiana Pennsylvania Colorado Wyoming Arkansas Oklahoma West Virginia Ohio Utah Illinois Michigan New York California New Mexico Virginia Missouri Georgia Kentucky Florida Indiana North Carolina Wisconsin Minnesota Tennessee Alabama Arizona New Jersey Maryland Oregon Iowa South Carolina Kansas Massachusetts Connecticut Nebraska Washington Mississippi Delaware Idaho North Dakota Montana Maine Rhode Island Nevada South Dakota District of Columbia Vermont New Hampshire Direct 34,194 16,678 11,507 6,932 7,211 4,850 3,606 4,011 846 1,821 677 996 51 785 1,263 154 594 23 457 65 86 0 42 101 8 79 0 94 0 21 91 2 107 29 0 27 0 33 49 0 0 26 0 0 2 0 0 0 0 Indirect 24,380 5,559 6,730 4,365 1,348 1,853 1,944 1,243 2,263 1,309 1,698 1,568 1,709 1,380 510 929 576 808 609 688 827 744 730 644 586 517 476 419 451 408 343 413 357 334 321 266 253 239 122 127 156 107 90 83 83 69 62 50 44 Induced 25,648 6,599 8,015 5,367 2,162 2,045 1,866 1,326 2,019 1,482 2,003 1,742 2,135 1,483 579 893 759 935 622 910 747 890 710 734 664 470 567 505 526 413 407 420 369 377 359 272 304 280 139 147 109 114 124 96 81 95 76 70 49 Total 84,223 28,837 26,252 16,664 10,722 8,749 7,416 6,580 5,127 4,613 4,378 4,306 3,895 3,648 2,352 1,976 1,929 1,766 1,689 1,662 1,660 1,634 1,482 1,480 1,258 1,066 1,043 1,019 977 842 841 835 834 740 679 565 557 551 310 275 265 246 214 179 167 163 138 121 93 US Total 97,518 70,793 78,706 247,017 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-23 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Value Added Contribution of Unconventional Gas*: 2030 ($M ranked by total value added contribution) Texas Louisiana Pennsylvania Colorado Wyoming Arkansas Oklahoma West Virginia Ohio Utah Illinois Michigan New York California Florida New Mexico Virginia Missouri Georgia Indiana Kentucky North Carolina Wisconsin Minnesota Tennessee Alabama Arizona New Jersey Maryland Iowa South Carolina Kansas Oregon Massachusetts Connecticut Nebraska Washington Mississippi Delaware Idaho North Dakota Montana Maine Rhode Island Nevada South Dakota District of Columbia Vermont New Hampshire US Total Direct 36,540 17,429 12,973 6,360 7,758 4,900 3,872 4,434 1,002 1,885 772 1,079 57 804 277 1,146 161 657 97 104 441 0 48 95 8 84 0 111 0 101 3 111 17 36 0 30 0 30 59 0 0 22 0 0 2 0 0 0 0 Indirect 26,353 5,792 7,582 4,103 1,465 1,913 2,092 1,387 2,530 1,368 1,812 1,717 1,782 1,451 853 505 1,017 629 918 902 659 793 796 686 642 587 529 445 471 381 454 392 426 350 338 297 275 250 137 138 174 113 96 85 92 74 66 52 47 Induced 27,767 6,878 9,047 5,033 2,354 2,102 2,014 1,476 2,241 1,553 2,172 1,883 2,229 1,567 1,140 556 974 825 1,069 809 659 962 768 780 721 523 635 539 558 444 460 400 439 397 371 295 327 295 154 160 122 121 132 100 91 102 82 73 53 Total 90,660 30,100 29,603 15,496 11,578 8,914 7,978 7,297 5,774 4,807 4,757 4,679 4,069 3,822 2,270 2,206 2,152 2,111 2,084 1,814 1,759 1,754 1,613 1,561 1,372 1,193 1,164 1,095 1,030 926 917 904 883 783 709 622 602 575 349 298 296 257 228 186 185 176 148 125 100 103,505 76,021 84,456 263,982 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-24 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Value Added Contribution of Unconventional Gas*: 2035 ($M ranked by total value added contribution) Texas Pennsylvania Louisiana Colorado Wyoming Arkansas West Virginia Oklahoma Ohio Illinois Michigan Utah New York California Virginia Missouri New Mexico Georgia Indiana Florida North Carolina Kentucky Wisconsin Minnesota Tennessee Arizona New Jersey Alabama Maryland Iowa South Carolina Kansas Oregon Massachusetts Connecticut Nebraska Washington Mississippi Delaware North Dakota Idaho Montana Maine Nevada Rhode Island South Dakota District of Columbia Vermont New Hampshire US Total Direct 44,731 18,808 21,981 7,123 9,894 5,769 6,299 4,809 1,500 1,087 1,441 2,038 85 928 213 814 1,323 14 158 61 0 525 64 107 7 0 167 58 0 131 2 130 18 56 0 37 0 26 90 0 0 24 0 3 0 0 0 0 0 Indirect 32,359 10,741 7,208 4,664 1,855 2,276 1,941 2,598 3,405 2,289 2,222 1,552 2,182 1,769 1,326 782 606 1,105 1,142 953 978 831 1,011 856 810 684 559 722 583 491 573 498 525 433 415 382 350 299 186 230 173 143 119 117 103 92 82 62 60 Induced 33,998 12,889 8,569 5,698 2,986 2,495 2,072 2,498 3,017 2,802 2,433 1,753 2,732 1,920 1,250 1,020 660 1,280 1,031 1,252 1,206 818 970 974 909 826 680 624 699 567 581 506 550 492 450 372 411 359 205 160 202 151 163 117 123 128 104 89 68 Total 111,089 42,438 37,759 17,485 14,735 10,540 10,313 9,905 7,921 6,178 6,096 5,343 5,000 4,617 2,789 2,616 2,589 2,398 2,331 2,266 2,185 2,174 2,044 1,937 1,727 1,509 1,406 1,405 1,281 1,189 1,155 1,135 1,093 981 865 791 761 685 482 390 375 318 282 237 225 220 186 152 128 130,520 95,346 105,862 331,728 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-25 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Labor Income Contribution: Alphabetical by State US State-L Level Labor Income Contribution of Unconventional Gas*: 2010 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 117 0 1,171 349 2,561 0 16 0 171 63 0 291 34 27 52 186 2,740 0 0 12 541 34 4 258 13 5 38 0 62 785 39 4 0 372 903 39 1,210 0 3 0 7 9,377 689 0 81 0 556 12 1,931 Indirect 237 197 561 584 1,575 160 46 27 318 366 52 729 362 133 142 257 1,371 42 211 153 612 277 95 209 43 95 47 20 198 314 806 335 41 873 563 179 1,326 40 172 30 246 6,538 501 23 405 110 281 303 428 Induced 229 233 582 620 1,822 184 55 34 424 431 61 808 320 161 153 265 1,381 58 249 178 698 305 107 257 49 107 49 21 237 362 1,026 391 39 786 527 188 1,439 47 178 40 284 6,925 520 31 403 133 254 296 394 Total 583 430 2,314 1,553 5,958 344 116 61 912 860 113 1,828 716 321 347 708 5,492 100 460 343 1,851 616 206 724 104 207 133 41 497 1,461 1,871 731 79 2,031 1,993 406 3,975 87 353 70 537 22,840 1,710 54 889 243 1,091 611 2,753 US Total 24,755 22,633 24,339 71,727 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-26 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Labor Income Contribution of Unconventional Gas*: 2015 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 135 0 1,725 547 3,943 0 21 0 366 76 0 387 39 56 64 214 4,723 0 0 17 684 83 113 379 12 13 1 0 54 709 35 0 0 434 1,338 16 2,981 0 0 0 3 12,486 799 0 73 0 1,126 25 2,351 Indirect 343 292 838 847 2,524 222 65 40 519 532 78 1,039 506 203 207 355 2,210 60 313 225 864 415 184 304 64 152 50 28 278 335 1,186 490 77 1,189 850 251 2,526 58 257 44 364 8,993 648 35 560 163 497 447 580 Induced 322 351 845 900 2,790 257 78 51 679 619 91 1,136 454 241 219 361 2,304 83 360 255 935 465 201 367 70 164 50 31 330 363 1,490 571 62 1,061 774 257 2,844 67 263 60 414 9,291 651 46 558 197 466 434 738 Total 801 643 3,407 2,295 9,258 479 164 91 1,564 1,226 169 2,562 999 499 491 930 9,238 143 674 498 2,483 963 497 1,049 146 329 101 59 662 1,407 2,710 1,061 138 2,684 2,961 524 8,351 125 521 104 782 30,769 2,098 81 1,191 360 2,088 906 3,669 US Total 36,028 33,309 35,615 104,951 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-27 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Labor Income Contribution of Unconventional Gas*: 2020 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 80 0 1,979 601 4,140 0 36 0 176 46 0 539 60 66 67 216 5,672 0 0 31 839 88 53 482 11 16 7 0 78 556 47 8 0 660 1,585 20 4,590 0 4 0 8 15,840 889 0 80 0 1,585 29 2,534 Indirect 393 372 995 1,014 2,758 265 89 51 570 645 97 1,274 626 251 250 430 2,594 73 385 276 1,066 504 192 377 77 195 65 35 339 324 1,423 610 101 1,563 1,015 317 3,654 69 323 54 456 11,562 752 42 699 202 684 559 637 Induced 361 445 986 1,069 2,994 301 102 64 748 743 112 1,407 556 293 265 427 2,749 99 438 307 1,123 557 215 451 85 203 66 38 400 334 1,772 708 78 1,367 922 318 4,093 79 327 73 513 11,790 750 56 686 242 635 534 804 Total 834 816 3,960 2,685 9,893 566 226 115 1,494 1,434 210 3,220 1,243 610 582 1,073 11,015 172 823 614 3,028 1,149 460 1,310 173 415 138 73 817 1,215 3,242 1,326 179 3,590 3,522 654 12,336 148 654 127 977 39,192 2,391 99 1,465 444 2,904 1,122 3,974 US Total 43,717 41,307 43,687 128,711 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-28 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Labor Income Contribution of Unconventional Gas*: 2025 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 42 0 2,066 578 3,597 0 32 0 62 14 0 502 55 67 67 199 6,581 0 0 28 767 75 31 488 10 18 1 0 69 500 40 0 0 596 1,659 15 4,791 0 1 0 5 16,331 939 0 73 0 1,634 31 2,872 Indirect 394 387 1,032 1,005 2,426 259 87 52 559 656 100 1,247 629 263 257 431 2,911 73 374 269 1,064 500 184 381 78 205 65 35 335 315 1,393 605 109 1,526 1,037 314 3,679 67 329 54 467 11,822 782 41 707 207 698 572 715 Induced 359 469 1,027 1,071 2,648 294 102 65 736 753 117 1,397 567 303 273 429 3,140 100 437 302 1,093 560 211 455 87 210 66 38 400 318 1,754 717 83 1,338 954 322 4,204 79 335 75 526 12,132 788 56 698 246 655 551 907 Total 795 855 4,124 2,655 8,671 554 221 117 1,357 1,422 216 3,146 1,250 633 596 1,059 12,632 173 811 599 2,924 1,136 426 1,323 174 433 132 73 804 1,134 3,187 1,323 192 3,460 3,649 651 12,674 146 665 129 998 40,285 2,509 97 1,478 454 2,986 1,154 4,494 US Total 44,834 41,695 44,445 130,974 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-29 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Labor Income Contribution of Unconventional Gas*: 2030 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 57 0 2,102 598 3,333 0 39 0 262 55 0 573 66 75 69 196 6,820 0 0 35 849 70 28 540 8 20 1 0 82 451 47 0 0 708 1,791 12 5,453 0 2 0 5 17,610 968 0 78 0 1,823 35 3,114 Indirect 447 430 1,068 1,063 2,300 273 96 55 670 735 108 1,326 684 292 283 469 3,032 78 392 282 1,166 535 194 416 83 229 71 37 355 315 1,453 647 122 1,694 1,118 331 4,130 69 362 58 512 12,840 822 42 776 225 777 625 778 Induced 396 526 1,059 1,136 2,511 304 112 70 872 844 127 1,502 611 329 297 458 3,274 106 464 318 1,176 599 225 492 93 227 74 41 425 313 1,829 776 93 1,466 1,028 344 4,706 83 367 80 571 13,144 832 59 762 264 726 596 988 Total 900 956 4,229 2,797 8,143 577 247 126 1,804 1,633 235 3,400 1,361 696 649 1,122 13,126 184 855 634 3,190 1,204 446 1,448 184 476 146 78 861 1,079 3,328 1,424 215 3,867 3,937 688 14,289 152 731 139 1,089 43,594 2,623 101 1,616 490 3,326 1,256 4,880 US Total 47,974 44,865 47,692 140,531 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-30 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Labor Income Contribution of Unconventional Gas*: 2035 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 29 0 2,485 693 3,739 0 60 0 58 8 0 807 100 97 80 237 8,519 0 0 54 1,136 80 25 668 9 25 1 0 123 522 71 0 0 1,059 2,219 13 7,966 0 1 0 5 21,507 1,050 0 105 0 2,609 47 3,958 Indirect 556 557 1,273 1,303 2,628 335 127 69 781 900 135 1,657 861 376 362 590 3,767 96 484 347 1,495 669 233 518 105 295 91 47 443 379 1,772 800 160 2,240 1,389 410 5,777 83 457 72 646 15,788 944 51 1,004 286 1,080 792 986 Induced 484 684 1,262 1,401 2,868 367 146 89 1,021 1,035 160 1,909 773 420 377 570 4,075 131 580 391 1,504 751 276 609 117 286 96 52 531 376 2,233 975 122 1,927 1,276 433 6,606 101 463 100 720 16,133 958 72 977 332 1,008 751 1,252 Total 1,069 1,241 5,020 3,397 9,236 702 334 158 1,860 1,943 295 4,374 1,734 892 819 1,396 16,361 227 1,064 791 4,135 1,500 534 1,794 230 606 189 99 1,097 1,277 4,075 1,775 282 5,225 4,885 856 20,349 184 921 173 1,371 53,427 2,952 122 2,086 617 4,697 1,590 6,196 US Total 60,162 56,212 59,780 176,154 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-31 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Government Revenue and Private Lease Payments by State Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Alabama ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 106,963 80,367 26,596 132,733 14,860 77,599 35,020 5,253 0 239,696 2015 130,609 102,678 27,931 132,137 17,374 87,180 23,986 3,598 0 262,746 2020 146,576 116,530 30,046 127,494 20,656 90,141 14,519 2,178 0 274,070 2025 122,027 96,872 25,155 102,580 16,305 75,246 9,591 1,439 0 224,607 2030 140,167 112,259 27,908 114,867 18,713 87,779 7,283 1,092 0 255,034 2035 162,781 129,210 33,571 132,590 21,782 101,166 8,384 1,258 0 295,370 2010-2035 3,371,258 2,665,636 705,621 3,048,698 456,845 2,148,640 385,402 57,810 0 6,419,955 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Arizona ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 84,003 69,543 14,460 51,683 12,544 39,138 0 0 0 135,685 2015 126,201 104,731 21,470 76,580 18,680 57,900 0 0 0 202,781 2020 161,891 131,407 30,483 139,668 23,844 115,824 0 0 0 301,558 2025 173,836 141,811 32,026 148,362 26,129 122,233 0 0 0 322,198 2030 185,989 155,264 30,725 110,795 28,246 82,549 0 0 0 296,785 2035 241,599 201,750 39,849 143,395 36,477 106,917 0 0 0 384,994 2010-2035 4,053,592 3,344,299 709,293 2,864,717 607,051 2,257,666 0 0 0 6,918,309 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-32 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Arkansas ($Th) 2010 Federal Taxes 462,301 Personal Taxes 327,776 Corporate Taxes 134,526 State and Local Taxes 715,078 Personal Taxes 72,954 Corporate Taxes 442,061 Severance Taxes 153,894 Ad Valorem Taxes 46,168 Federal Royalty Payments 15,213 Total Govt Revenue 1,192,592 Lease Payments to Private Landowners 15,425 2015 682,288 482,957 199,331 1,085,876 106,640 657,459 247,521 74,256 24,044 1,792,208 2020 787,205 560,094 227,111 1,250,403 123,138 744,563 294,386 88,316 28,488 2,066,097 2025 830,505 590,157 240,348 1,394,575 131,901 790,555 363,168 108,951 34,955 2,260,036 2030 850,157 605,876 244,282 1,475,379 136,182 804,748 411,114 123,334 39,487 2,365,024 2035 1,008,556 719,860 288,696 1,721,033 160,685 950,997 468,732 140,620 44,918 2,774,506 2010-2035 19,427,923 13,814,508 5,613,414 32,121,442 3,073,402 18,469,273 8,137,513 2,441,254 785,200 52,334,565 14,241 17,182 20,278 23,884 27,074 484,172 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: California ($Th) 2010 Federal Taxes 832,152 Personal Taxes 696,726 Corporate Taxes 135,426 State and Local Taxes 684,244 Personal Taxes 221,412 Corporate Taxes 462,832 Severance Taxes 0 Ad Valorem Taxes 0 Federal Royalty Payments 0 Total Govt Revenue 1,516,396 Lease Payments to Private Landowners 0 2015 1,222,812 1,023,707 199,105 1,013,838 322,713 691,125 0 0 0 2,236,651 2020 1,437,927 1,203,909 234,018 1,187,999 377,641 810,358 0 0 0 2,625,926 2025 1,441,360 1,205,019 236,341 1,208,210 383,766 824,444 0 0 0 2,649,571 2030 1,518,915 1,269,511 249,404 1,280,517 407,016 873,501 0 0 0 2,799,432 2035 1,863,453 1,554,999 308,454 1,576,497 495,378 1,081,119 0 0 0 3,439,950 2010-2035 34,844,086 29,140,044 5,704,042 29,104,679 9,247,657 19,857,023 0 0 0 63,948,766 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-33 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Colorado ($Th) 2010 Federal Taxes 1,386,141 Personal Taxes 1,035,700 Corporate Taxes 350,442 State and Local Taxes 1,579,908 Personal Taxes 230,443 Corporate Taxes 902,728 Severance Taxes 248,187 Ad Valorem Taxes 198,550 Federal Royalty Payments 231,273 Total Govt Revenue 3,197,323 Lease Payments to Private Landowners 30,577 2015 2,114,452 1,636,244 478,208 2,066,264 356,553 1,213,958 275,419 220,335 253,208 4,433,925 2020 2,230,811 1,740,246 490,565 2,084,772 377,363 1,232,441 263,871 211,097 242,252 4,557,835 2025 1,973,929 1,535,870 438,059 1,971,476 338,475 1,110,727 290,152 232,122 265,108 4,210,513 2030 1,848,011 1,439,170 408,842 1,925,593 319,230 1,042,570 313,218 250,574 285,247 4,058,852 2035 2,098,686 1,633,723 464,962 2,131,337 360,109 1,187,464 324,313 259,450 295,940 4,525,963 2010-2035 49,548,086 38,431,207 11,116,879 49,518,640 8,434,483 28,223,964 7,144,552 5,715,641 6,547,114 105,613,840 80,308 94,206 79,875 76,709 79,593 1,930,914 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Connecticut ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 80,441 70,161 10,280 35,292 15,622 19,670 0 0 0 115,734 2015 113,058 98,498 14,560 49,465 21,712 27,752 0 0 0 162,523 2020 132,467 115,695 16,772 57,165 25,443 31,722 0 0 0 189,632 2025 130,817 114,253 16,564 56,935 25,512 31,423 0 0 0 187,752 2030 136,020 119,089 16,932 58,928 26,775 32,153 0 0 0 194,948 2035 165,889 145,386 20,502 71,380 32,484 38,896 0 0 0 237,269 2010-2035 3,177,633 2,776,543 401,090 1,379,147 617,478 761,670 0 0 0 4,556,781 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-34 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Delaware ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 22,147 18,401 3,747 16,815 4,380 12,436 0 0 0 38,963 2015 31,006 25,948 5,058 23,326 6,137 17,189 0 0 0 54,331 2020 42,573 35,761 6,812 31,834 8,457 23,376 0 0 0 74,407 2025 41,635 35,071 6,564 31,057 8,424 22,633 0 0 0 72,692 2030 46,369 39,087 7,282 34,636 9,455 25,181 0 0 0 81,005 2035 62,977 53,054 9,923 47,093 12,757 34,336 0 0 0 110,069 2010-2035 1,020,725 857,967 162,758 764,031 205,208 558,824 0 0 0 1,784,756 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: District of Columbia ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 11,493 10,847 646 3,685 1,860 1,825 0 0 0 15,178 2015 17,370 16,377 993 5,606 2,808 2,799 0 0 0 22,977 2020 21,887 20,655 1,232 7,002 3,537 3,465 0 0 0 28,889 2025 22,288 21,017 1,271 7,180 3,605 3,574 0 0 0 29,468 2030 23,878 22,519 1,358 7,681 3,860 3,821 0 0 0 31,559 2035 30,047 28,331 1,716 9,682 4,858 4,824 0 0 0 39,728 2010-2035 530,962 500,785 30,177 170,764 85,848 84,916 0 0 0 701,726 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-35 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Florida ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 321,178 279,055 42,123 215,188 13,845 201,342 0 0 0 536,365 2015 535,885 468,084 67,801 350,570 20,633 329,936 0 0 0 886,455 2020 551,106 476,103 75,003 376,773 23,325 353,448 0 0 0 927,879 2025 507,671 437,328 70,343 353,285 18,717 334,568 0 0 0 860,956 2030 641,715 556,464 85,251 434,872 24,540 410,332 0 0 0 1,076,587 2035 705,608 606,752 98,856 495,319 25,978 469,340 0 0 0 1,200,927 2010-2035 13,748,850 11,904,410 1,844,440 9,353,767 535,635 8,818,132 0 0 0 23,102,617 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Georgia ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 164,265 132,696 31,569 106,311 33,416 72,895 0 0 0 270,576 2015 222,406 179,141 43,265 142,021 44,421 97,601 0 0 0 364,428 2020 272,557 219,005 53,552 181,175 54,708 126,468 0 0 0 453,732 2025 255,042 204,112 50,930 172,285 51,697 120,589 0 0 0 427,328 2030 294,916 236,954 57,962 190,346 60,058 130,287 0 0 0 485,262 2035 348,617 279,784 68,833 229,130 70,506 158,625 0 0 0 577,747 2010-2035 6,506,813 5,227,263 1,279,550 4,267,743 1,314,221 2,953,522 0 0 0 10,774,556 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-36 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Idaho ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 19,469 16,294 3,175 11,860 3,769 8,091 0 0 0 31,329 2015 29,584 24,713 4,870 18,021 5,659 12,362 0 0 0 47,605 2020 36,749 30,591 6,158 22,501 6,988 15,513 0 0 0 59,250 2025 38,466 31,893 6,573 24,006 7,398 16,608 0 0 0 62,472 2030 41,831 34,575 7,256 26,427 8,075 18,352 0 0 0 68,258 2035 52,903 43,558 9,345 33,720 10,110 23,611 0 0 0 86,623 2010-2035 914,082 758,489 155,592 568,730 175,298 393,432 0 0 0 1,482,812 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Illinois ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 379,894 324,743 55,151 249,709 60,373 189,305 0 31 30 629,632 2015 521,383 445,680 75,703 344,003 81,191 262,812 0 1 1 865,388 2020 668,911 572,687 96,225 433,530 105,131 328,400 0 0 0 1,102,442 2025 640,333 549,461 90,873 414,403 101,341 313,063 0 0 0 1,054,736 2030 690,779 593,771 97,008 444,548 110,241 334,307 0 0 0 1,135,327 2035 892,006 767,184 124,821 574,833 141,636 433,197 0 0 0 1,466,838 2010-2035 15,786,786 13,537,813 2,248,973 10,243,776 2,494,534 7,749,159 0 83 80 26,030,642 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-37 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Indiana ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 128,219 107,103 21,117 84,074 22,325 61,749 0 0 0 212,294 2015 165,739 138,500 27,239 109,665 28,014 81,651 0 0 0 275,405 2020 221,475 185,240 36,235 142,773 38,136 104,637 0 0 0 364,248 2025 206,855 173,702 33,154 131,738 35,557 96,181 0 0 0 338,594 2030 224,532 188,817 35,715 142,250 38,904 103,346 0 0 0 366,782 2035 287,185 241,158 46,026 186,102 49,444 136,658 0 0 0 473,287 2010-2035 5,131,521 4,301,949 829,571 3,307,575 882,481 2,425,094 0 0 0 8,439,095 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Iowa ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 54,558 44,410 10,149 42,495 9,982 32,513 0 0 0 97,054 2015 86,140 70,118 16,022 67,006 15,571 51,434 0 0 0 153,146 2020 104,873 85,196 19,677 81,632 18,866 62,766 0 0 0 186,506 2025 109,854 89,275 20,579 86,075 20,054 66,022 0 0 0 195,930 2030 120,756 98,114 22,641 94,947 22,184 72,762 0 0 0 215,702 2035 155,480 126,097 29,383 122,609 28,342 94,267 0 0 0 278,089 2010-2035 2,633,214 2,139,785 493,428 2,061,061 479,188 1,581,874 0 0 0 4,694,275 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-38 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Kansas ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 64,324 50,753 13,571 55,654 11,696 38,062 3,065 2,831 71 120,048 2015 91,042 73,379 17,662 64,399 16,210 47,599 307 283 7 155,448 2020 106,597 86,332 20,265 72,875 18,974 53,849 27 25 1 179,472 2025 109,648 89,077 20,570 74,802 19,869 54,928 3 2 0 184,450 2030 118,864 96,813 22,050 80,698 21,746 58,951 1 0 0 199,562 2035 150,003 122,315 27,687 101,176 27,319 73,856 1 1 0 251,179 2010-2035 2,666,565 2,160,682 505,883 1,855,950 481,535 1,356,430 9,349 8,636 216 4,522,730 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Kentucky ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 130,244 94,404 35,840 157,598 26,551 105,390 20,992 4,665 3,315 291,156 2015 155,557 112,190 43,367 196,317 31,709 131,177 27,353 6,078 4,296 356,170 2020 190,668 141,993 48,675 213,700 39,130 143,054 25,786 5,730 4,044 408,411 2025 170,532 126,830 43,702 193,369 35,621 129,062 23,470 5,216 3,694 367,595 2030 178,348 133,771 44,577 199,676 37,594 131,315 25,172 5,594 3,946 381,969 2035 221,268 166,360 54,907 247,240 46,284 165,365 29,119 6,471 4,544 473,052 2010-2035 4,354,304 3,225,828 1,128,476 5,027,402 902,356 3,349,935 634,183 140,929 99,545 9,481,251 4,333 2,874 3,468 4,093 4,820 5,464 100,767 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-39 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Louisiana ($Th) 2010 Federal Taxes 1,052,791 Personal Taxes 784,452 Corporate Taxes 268,338 State and Local Taxes 1,020,976 Personal Taxes 140,109 Corporate Taxes 804,853 Severance Taxes 28,541 Ad Valorem Taxes 47,474 Federal Royalty Payments 0 Total Govt Revenue 2,073,767 Lease Payments to Private Landowners 39,076 2015 1,857,187 1,323,847 533,340 2,039,799 236,215 1,613,738 63,754 126,091 0 3,896,986 2020 2,249,761 1,561,864 687,897 2,618,671 279,411 2,062,794 89,953 186,515 0 $4,868,433 2025 2,627,846 1,808,928 818,918 3,175,771 329,280 2,469,303 111,298 265,889 0 5,803,617 2030 2,743,095 1,881,100 861,995 3,392,989 345,002 2,600,643 122,246 325,097 0 6,136,084 2035 3,437,170 2,346,907 1,090,263 4,265,159 428,066 3,285,162 135,937 415,995 0 7,702,330 2010-2035 58,614,351 40,707,093 17,907,258 69,351,485 7,369,974 53,957,431 2,347,450 5,676,631 0 127,965,836 45,855 57,967 68,439 81,099 105,496 1,628,231 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Maine ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 19,285 17,841 1,444 7,139 3,059 4,080 0 0 0 26,424 2015 27,680 25,590 2,090 10,275 4,388 5,887 0 0 0 37,955 2020 33,336 30,843 2,493 12,295 5,281 7,014 0 0 0 45,632 2025 33,412 30,898 2,514 12,370 5,301 7,069 0 0 0 45,781 2030 35,666 32,984 2,682 13,199 5,654 7,545 0 0 0 48,866 2035 44,011 40,688 3,323 16,320 6,977 9,343 0 0 0 60,331 2010-2035 808,713 747,899 60,814 299,342 128,210 171,132 0 0 0 1,108,055 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-40 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Maryland ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 91,191 77,480 13,711 61,298 25,770 35,527 0 0 0 152,489 2015 135,376 114,757 20,619 91,010 37,787 53,222 0 0 0 226,386 2020 164,249 139,552 24,696 109,101 45,844 63,257 0 0 0 273,350 2025 163,116 138,326 24,790 109,828 46,140 63,688 0 0 0 272,944 2030 171,481 145,440 26,040 115,812 48,845 66,967 0 0 0 287,293 2035 213,435 180,927 32,508 143,902 60,386 83,517 0 0 0 357,337 2010-2035 3,932,673 3,336,394 596,279 2,641,752 1,108,473 1,533,279 0 0 0 6,574,425 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Massachusetts ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 146,851 124,517 22,335 115,756 32,775 82,980 0 0 0 262,607 2015 216,489 182,386 34,102 174,528 47,527 127,001 0 0 0 391,017 2020 263,407 222,233 41,174 210,948 57,772 153,175 0 0 0 474,355 2025 260,256 219,255 41,001 210,866 57,875 152,990 0 0 0 471,122 2030 273,278 230,707 42,570 220,321 61,316 159,005 0 0 0 493,598 2035 339,412 286,918 52,494 271,652 75,781 195,871 0 0 0 611,065 2010-2035 6,282,806 5,301,499 981,307 5,051,833 1,393,845 3,657,988 0 0 0 11,334,639 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-41 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Michigan ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 361,495 297,935 63,560 329,377 70,225 223,399 27,502 8,251 1,775 692,647 2015 484,124 405,778 78,346 398,353 93,288 276,796 21,746 6,524 1,393 883,871 2020 585,590 495,807 89,783 448,739 112,595 317,197 14,574 4,372 933 1,035,262 2025 570,246 484,196 86,050 431,228 111,281 305,844 10,849 3,255 692 1,002,166 2030 620,494 528,341 92,153 462,232 121,931 328,707 8,918 2,675 567 1,083,293 2035 806,084 686,605 119,479 596,644 157,371 425,972 10,231 3,069 648 1,403,376 2010-2035 14,221,219 12,031,956 2,189,262 11,017,812 2,764,467 7,766,148 374,767 112,430 23,984 25,263,015 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Minnesota ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 124,734 102,603 22,131 98,883 28,220 70,663 0 0 0 223,617 2015 196,771 162,424 34,347 153,471 44,227 109,244 0 0 0 350,242 2020 233,008 192,483 40,524 180,190 52,287 127,903 0 0 0 413,198 2025 231,463 191,208 40,255 180,173 52,740 127,433 0 0 0 411,636 2030 244,250 202,079 42,171 189,753 56,121 133,633 0 0 0 434,003 2035 303,979 251,611 52,367 235,223 69,442 165,781 0 0 0 539,201 2010-2035 5,599,240 4,626,513 972,727 4,353,199 1,271,028 3,082,171 0 0 0 9,952,439 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-42 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Mississippi ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 32,384 25,935 6,449 35,043 5,165 29,878 0 0 0 67,427 2015 80,389 67,488 12,900 72,872 13,305 59,567 0 0 0 153,261 2020 72,582 59,514 13,068 71,584 11,705 59,879 0 0 0 144,165 2025 67,240 54,615 12,626 68,933 10,906 58,026 0 0 0 136,173 2030 70,209 56,922 13,286 72,569 11,445 61,124 0 0 0 142,778 2035 84,006 67,883 16,123 87,663 13,564 74,099 0 0 0 171,669 2010-2035 1,743,071 1,427,238 315,832 1,736,552 283,627 1,452,926 0 0 0 3,479,623 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Missouri ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 257,958 215,624 42,334 167,947 45,007 122,940 0 0 0 425,905 2015 359,549 300,709 58,840 234,043 61,582 172,461 0 0 0 593,592 2020 461,931 386,650 75,281 295,992 79,717 216,274 0 0 0 757,923 2025 452,645 379,639 73,006 289,458 78,718 210,741 0 0 0 742,103 2030 493,271 413,996 79,275 315,102 86,418 228,683 0 0 0 808,373 2035 612,087 513,130 98,957 395,111 106,485 288,626 0 0 0 1,007,198 2010-2035 11,012,092 9,226,856 1,785,236 7,080,616 1,910,908 5,169,708 0 0 0 18,092,709 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-43 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Montana ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 19,456 14,053 5,403 22,742 3,707 13,767 4,536 732 1,742 43,940 2015 27,195 19,787 7,408 28,919 5,149 18,765 4,310 695 1,645 57,760 2020 31,891 23,464 8,427 31,641 6,047 21,068 3,897 629 1,485 65,017 2025 32,331 23,900 8,431 32,203 6,254 21,141 4,140 668 1,571 66,105 2030 34,036 25,269 8,767 33,487 6,655 21,998 4,163 671 1,574 69,097 2035 42,596 31,643 10,952 40,884 8,279 27,447 4,442 716 1,673 85,153 2010-2035 782,396 576,346 206,050 790,316 150,489 517,893 104,999 16,935 39,919 1,612,631 8 24 62 64 68 74 1,302 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Nebraska ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 34,580 28,157 6,423 26,295 5,404 20,890 0 0 0 60,875 2015 55,676 45,260 10,416 43,486 8,601 34,884 0 0 0 99,161 2020 70,000 56,972 13,028 54,882 10,802 44,080 0 0 0 124,882 2025 73,926 60,306 13,620 58,637 11,611 47,026 0 0 0 132,563 2030 81,225 66,475 14,749 64,334 12,888 51,447 0 0 0 145,559 2035 103,663 84,994 18,669 81,723 16,376 65,348 0 0 0 185,386 2010-2035 1,749,736 1,427,939 321,797 1,376,741 273,964 1,102,778 0 0 0 3,126,478 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-44 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Nevada ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 82,974 69,982 12,992 56,246 4,924 51,323 0 0 0 139,221 2015 64,443 52,140 12,303 29,323 3,644 25,679 0 0 0 93,766 2020 88,824 71,291 17,533 61,810 4,957 56,854 0 0 0 150,634 2025 84,066 68,223 15,843 37,742 4,830 32,912 0 0 0 121,808 2030 92,896 75,452 17,444 41,653 5,379 36,275 0 0 0 134,550 2035 119,430 97,101 22,329 53,265 6,879 46,386 0 0 0 172,694 2010-2035 2,157,155 1,753,240 403,915 1,126,420 123,555 1,002,864 0 0 0 3,283,575 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: New Hampshire ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 26,999 23,022 3,977 19,148 1,518 17,631 0 0 0 46,148 2015 39,475 33,559 5,916 28,314 2,190 26,124 0 0 0 67,789 2020 50,078 42,629 7,449 35,415 2,776 32,639 0 0 0 85,493 2025 49,950 42,461 7,490 35,724 2,807 32,917 0 0 0 85,674 2030 53,798 45,745 8,053 38,473 3,045 35,428 0 0 0 92,272 2035 69,070 58,785 10,285 49,093 3,889 45,204 0 0 0 118,163 2010-2035 1,206,680 1,026,487 180,194 860,234 67,609 792,625 0 0 0 2,066,914 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-45 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: New Jersey ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 210,501 179,321 31,179 142,431 35,561 106,870 0 0 0 352,932 2015 279,500 235,390 44,110 195,501 45,219 150,282 0 0 0 475,001 2020 359,117 300,322 58,796 252,632 58,438 194,194 0 0 0 611,750 2025 344,742 284,887 59,855 255,087 55,364 199,723 0 0 0 599,829 2030 368,102 302,450 65,652 277,652 59,139 218,512 0 0 0 645,754 2035 469,161 382,690 86,471 364,674 74,416 290,258 0 0 0 833,835 2010-2035 8,456,463 7,020,272 1,436,191 6,172,123 1,365,743 4,806,380 0 0 0 14,628,586 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: New Mexico ($Th) 2010 Federal Taxes 306,482 Personal Taxes 214,571 Corporate Taxes 91,910 State and Local Taxes 632,190 Personal Taxes 44,673 Corporate Taxes 332,225 Severance Taxes 214,727 Ad Valorem Taxes 40,566 Federal Royalty Payments 152,245 Total Govt Revenue 1,090,917 Lease Payments to Private Landowners 921 2015 293,283 206,500 86,783 604,564 42,544 312,658 209,739 39,623 147,382 1,045,229 2020 247,819 177,450 70,369 482,034 36,403 251,568 163,227 30,836 114,605 844,458 2025 230,834 167,712 63,122 453,146 34,852 226,712 161,140 30,442 112,485 796,464 2030 219,109 159,406 59,704 446,795 33,348 214,508 167,328 31,611 116,457 782,361 2035 259,394 188,737 70,657 521,239 39,239 253,583 192,122 36,295 133,252 913,885 2010-2035 6,369,916 4,563,609 1,806,307 12,816,267 945,514 6,491,745 4,524,292 854,715 3,168,384 22,354,566 1,100 1,264 1,492 1,757 1,991 35,343 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-46 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: New York ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 377,030 321,607 55,423 344,139 119,250 224,169 0 720 185 721,354 2015 543,298 464,789 78,509 494,806 169,903 324,479 0 424 82 1,038,185 2020 669,605 574,057 95,548 598,912 205,282 393,363 0 268 38 1,268,555 2025 649,544 557,483 92,061 588,849 203,135 385,522 0 192 20 1,238,412 2030 678,123 582,191 95,932 617,323 213,054 404,111 0 158 13 1,295,459 2035 834,018 715,127 118,890 764,866 259,941 504,737 0 188 15 1,598,899 2010-2035 15,730,469 13,484,435 2,246,034 14,271,959 4,904,842 9,359,643 0 7,475 1,258 30,003,686 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: North Carolina ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 131,483 105,465 26,018 120,058 27,758 92,300 0 0 0 251,541 2015 193,002 159,863 33,139 106,925 40,913 66,012 0 0 0 299,926 2020 238,469 192,399 46,070 211,571 50,014 161,557 0 0 0 450,040 2025 241,936 198,499 43,437 171,833 52,093 119,740 0 0 0 413,769 2030 265,848 217,729 48,119 196,139 57,598 138,541 0 0 0 461,987 2035 334,336 278,588 55,748 184,395 72,287 112,107 0 0 0 518,731 2010-2035 5,860,818 4,802,581 1,058,236 4,193,472 1,253,204 2,940,268 0 0 0 10,054,290 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-47 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: North Dakota ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 15,676 14,124 1,552 6,806 2,422 4,384 0 0 0 22,482 2015 28,082 24,924 3,159 13,171 4,273 8,897 0 0 0 41,253 2020 36,272 32,196 4,076 16,979 5,513 11,466 0 0 0 53,251 2025 39,022 34,569 4,452 18,451 5,931 12,520 0 0 0 57,473 2030 43,701 38,727 4,974 20,631 6,639 13,992 0 0 0 64,332 2035 57,394 50,769 6,625 27,333 8,706 18,627 0 0 0 84,727 2010-2035 918,061 814,313 103,748 431,505 139,597 291,908 0 0 0 1,349,566 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Ohio ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 370,263 307,420 62,843 317,082 91,344 224,457 632 649 176 687,521 2015 475,107 394,464 80,643 409,300 116,411 292,027 425 437 94 884,501 2020 649,654 540,120 109,534 548,670 158,358 389,790 257 264 45 1,198,369 2025 612,998 510,220 102,777 522,544 152,385 369,792 181 186 24 1,135,566 2030 683,808 569,746 114,062 581,573 171,298 409,980 146 150 16 1,265,397 2035 929,331 774,209 155,122 790,096 231,333 558,425 167 172 19 1,719,446 2010-2035 15,356,818 12,776,823 2,579,994 13,078,383 3,798,954 9,265,154 7,042 7,234 1,386 28,436,587 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-48 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Oklahoma ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 414,348 295,681 118,667 447,110 61,471 259,335 104,015 22,289 13,742 875,199 2015 621,801 443,054 178,746 666,949 90,862 382,226 159,651 34,211 21,340 1,310,090 2020 730,719 523,454 207,265 770,889 106,981 437,836 186,177 39,895 24,932 1,526,540 2025 765,869 547,718 218,151 862,468 113,781 461,800 236,260 50,627 31,508 1,659,844 2030 824,078 590,672 233,405 958,907 123,511 493,227 281,787 60,383 37,502 1,820,487 2035 1,025,377 734,381 290,995 1,185,825 152,600 613,705 345,487 74,033 45,849 2,257,050 2010-2035 18,311,639 13,099,645 5,211,994 20,378,400 2,710,849 11,058,039 5,443,128 1,166,385 725,384 39,415,423 7,592 25,639 33,244 39,931 52,102 65,577 937,509 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Oregon ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 77,798 63,488 14,310 64,768 20,948 43,819 0 0 0 142,565 2015 102,988 83,204 19,784 89,102 26,595 62,507 0 0 0 192,090 2020 127,831 103,344 24,488 110,425 32,961 77,464 0 0 0 238,256 2025 128,349 103,582 24,767 112,028 33,547 78,481 0 0 0 240,376 2030 135,598 109,227 26,371 119,183 35,619 83,564 0 0 0 254,781 2035 169,332 135,981 33,350 149,620 44,068 105,552 0 0 0 318,952 2010-2035 3,091,657 2,495,458 596,199 2,689,652 806,150 1,883,502 0 0 0 5,781,309 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-49 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Pennsylvania ($Th) 2010 Federal Taxes 819,692 Personal Taxes 653,764 Corporate Taxes 165,928 State and Local Taxes 641,630 Personal Taxes 142,330 Corporate Taxes 499,300 Severance Taxes 0 Ad Valorem Taxes 0 Federal Royalty Payments 14,460 Total Govt Revenue 1,475,782 Lease Payments to Private Landowners 37,852 2015 1,788,973 1,349,558 439,414 1,642,573 299,334 1,343,239 0 0 73,356 3,504,902 2020 2,664,295 2,010,479 653,816 2,419,581 444,253 1,975,328 0 0 116,855 5,200,732 2025 2,760,482 2,062,636 697,846 2,587,699 464,989 2,122,710 0 0 154,278 5,502,459 2030 3,115,655 2,332,385 783,270 2,909,403 528,309 2,381,094 0 0 196,276 6,221,333 2035 4,460,429 3,340,073 1,120,356 4,149,587 750,423 3,399,164 0 0 279,174 8,889,189 2010-2035 64,847,323 48,759,880 16,087,444 59,774,322 10,916,307 48,858,015 0 0 3,437,911 128,059,557 53,558 92,891 95,328 134,733 210,003 2,502,188 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Rhode Island ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 16,695 15,513 1,182 6,000 2,660 3,340 0 0 0 22,695 2015 24,085 22,346 1,740 8,731 3,831 4,900 0 0 0 32,817 2020 28,640 26,598 2,043 10,301 4,554 5,746 0 0 0 38,941 2025 28,064 26,056 2,008 10,117 4,470 5,647 0 0 0 38,181 2030 29,232 27,156 2,076 10,495 4,655 5,840 0 0 0 39,728 2035 35,451 32,932 2,519 12,729 5,647 7,082 0 0 0 48,179 2010-2035 680,476 631,893 48,584 245,041 108,323 136,718 0 0 0 925,518 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-50 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: South Carolina ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 61,207 49,380 11,827 52,665 11,003 41,662 0 0 0 113,872 2015 89,914 74,849 15,064 46,014 16,218 29,796 0 0 0 135,927 2020 113,586 91,890 21,697 94,702 20,218 74,484 0 0 0 208,289 2025 115,260 94,803 20,457 76,263 21,058 55,205 0 0 0 191,523 2030 126,649 103,987 22,662 87,156 23,283 63,873 0 0 0 213,805 2035 159,308 133,054 26,255 80,907 29,221 51,686 0 0 0 240,216 2010-2035 2,778,331 2,283,732 494,599 1,854,607 504,445 1,350,162 0 0 0 4,632,939 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: South Dakota ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 11,851 9,690 2,161 6,230 722 5,508 0 0 0 18,081 2015 17,861 14,584 3,277 9,395 1,075 8,319 0 0 0 27,256 2020 21,549 17,611 3,938 11,216 1,296 9,920 0 0 0 32,765 2025 22,058 17,991 4,067 11,619 1,344 10,275 0 0 0 33,676 2030 23,751 19,342 4,408 12,604 1,455 11,149 0 0 0 36,355 2035 29,685 24,110 5,575 15,888 1,802 14,086 0 0 0 45,573 2010-2035 529,937 432,142 97,794 279,456 32,159 247,297 0 0 0 809,393 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-51 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Tennessee ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 92,813 77,657 15,156 47,648 4,077 43,571 0 0 0 140,461 2015 123,174 102,325 20,849 73,258 2,996 70,263 0 0 0 196,432 2020 169,484 141,670 27,814 88,643 7,347 81,295 0 0 0 258,127 2025 158,042 131,835 26,207 88,629 3,974 84,655 0 0 0 246,671 2030 171,905 143,684 28,221 94,357 4,334 90,023 0 0 0 266,262 2035 217,467 180,964 36,503 130,310 5,432 124,878 0 0 0 347,776 2010-2035 3,888,723 3,244,123 644,600 2,169,331 117,030 2,052,301 0 0 0 6,058,054 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Texas ($Th) 2010 Federal Taxes 5,404,857 Personal Taxes 4,030,771 Corporate Taxes 1,374,086 State and Local Taxes 5,444,695 Personal Taxes 313,110 Corporate Taxes 3,478,954 Severance Taxes 1,304,708 Ad Valorem Taxes 347,922 Federal Royalty Payments 41,701 Total Govt Revenue 10,891,252 Lease Payments to Private Landowners 111,548 2015 7,338,322 5,469,925 1,868,397 7,358,503 420,495 4,673,678 1,787,630 476,701 60,285 14,757,110 2020 9,240,879 6,947,423 2,293,456 8,923,748 532,353 5,670,580 2,148,011 572,803 77,139 18,241,767 2025 9,608,788 7,205,344 2,403,445 9,935,765 560,817 5,958,069 2,697,536 719,343 100,201 19,644,754 2030 10,366,027 7,796,562 2,569,465 11,028,021 610,848 6,369,334 3,195,663 852,177 121,993 21,516,041 2035 12,729,949 9,567,990 3,161,959 13,529,109 744,998 7,830,240 3,910,950 1,042,920 152,541 26,411,599 2010-2035 228,107,095 171,093,173 57,013,923 233,664,694 13,267,833 141,631,292 62,183,344 16,582,225 2,283,696 464,055,485 201,214 312,016 358,963 468,995 570,309 8,410,580 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-52 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Utah ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 349,074 278,915 70,159 286,454 64,304 194,220 21,485 6,446 25,976 661,504 2015 435,877 346,745 89,132 351,669 78,838 239,963 25,283 7,585 30,306 817,852 2020 492,928 391,919 101,009 397,087 88,875 268,894 30,245 9,073 36,263 926,278 2025 521,979 414,521 107,458 436,815 95,574 287,622 41,245 12,374 49,156 1,007,950 2030 544,800 432,420 112,379 468,796 100,465 301,675 51,274 15,382 60,950 1,074,546 2035 611,599 486,645 124,955 515,723 112,279 334,743 52,848 15,854 62,625 1,189,948 2010-2035 12,379,605 9,841,928 2,537,677 10,277,277 2,260,221 6,813,174 926,063 277,819 1,104,876 23,761,759 23,893 33,101 39,026 46,416 54,974 59,487 1,076,035 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Vermont ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 10,479 9,669 809 3,945 1,658 2,287 0 0 0 14,423 2015 15,732 14,503 1,229 5,948 2,487 3,461 0 0 0 21,680 2020 19,144 17,671 1,474 7,171 3,026 4,145 0 0 0 26,316 2025 18,795 17,353 1,443 7,034 2,977 4,057 0 0 0 25,829 2030 19,593 18,102 1,491 7,298 3,103 4,194 0 0 0 26,891 2035 23,733 21,930 1,802 8,828 3,760 5,067 0 0 0 32,560 2010-2035 451,852 417,142 34,710 169,184 71,509 97,675 0 0 0 621,036 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-53 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Virginia ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 179,773 145,220 34,553 140,970 37,193 95,797 5,320 2,660 493 321,236 2015 226,426 183,934 42,492 174,137 46,568 119,719 5,234 2,617 633 401,196 2020 293,992 241,664 52,328 211,537 60,305 144,454 4,518 2,259 594 506,123 2025 281,485 232,484 49,001 200,916 58,666 135,506 4,496 2,248 607 483,008 2030 307,547 255,085 52,462 216,806 64,468 145,216 4,749 2,374 645 524,999 2035 400,192 332,185 68,006 283,723 83,091 192,407 5,483 2,742 742 684,657 2010-2035 6,997,165 5,759,353 1,237,812 5,078,712 1,450,739 3,444,983 121,994 60,997 15,488 12,091,365 1,083 719 867 1,023 1,205 1,366 25,192 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Washington ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 97,610 83,606 14,004 63,617 3,501 60,117 0 0 0 161,227 2015 145,996 125,024 20,973 96,265 5,184 91,081 0 0 0 242,261 2020 179,029 153,365 25,665 118,526 6,339 112,187 0 0 0 297,555 2025 184,874 158,330 26,545 123,049 6,642 116,407 0 0 0 307,923 2030 199,488 170,846 28,643 132,932 7,228 125,704 0 0 0 332,420 2035 252,333 215,985 36,348 168,441 9,070 159,371 0 0 0 420,775 2010-2035 4,421,799 3,786,796 635,003 2,934,002 158,389 2,775,613 0 0 0 7,355,802 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-54 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: West Virginia ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 227,900 165,192 62,708 280,197 30,400 174,497 57,923 17,377 5,750 513,847 2015 434,997 302,676 132,321 658,548 55,785 380,798 170,742 51,222 17,095 1,110,639 2020 621,405 436,789 184,616 922,013 81,130 521,237 245,881 73,764 24,627 1,568,044 2025 631,110 438,417 192,692 1,040,158 82,124 549,154 314,523 94,357 31,388 1,702,656 2030 702,947 490,291 212,656 1,207,815 92,220 604,527 393,129 117,939 39,126 1,949,888 2035 996,505 696,791 299,714 1,697,928 130,097 852,167 550,511 165,153 54,574 2,749,007 2010-2035 15,013,300 10,495,820 4,517,480 24,087,982 1,957,543 12,845,244 7,142,458 2,142,737 711,988 39,813,269 18,034 21,445 35,298 36,892 50,936 76,831 960,022 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Wisconsin ($Th) Federal Taxes Personal Taxes Corporate Taxes State and Local Taxes Personal Taxes Corporate Taxes Severance Taxes Ad Valorem Taxes Federal Royalty Payments Total Govt Revenue Lease Payments to Private Landowners 2010 112,061 93,306 18,755 99,032 23,734 75,298 0 0 0 211,092 2015 167,446 139,265 28,180 147,345 35,205 112,140 0 0 0 314,791 2020 205,797 171,484 34,313 178,940 43,184 135,757 0 0 0 384,737 2025 213,082 177,745 35,337 185,509 45,503 140,006 0 0 0 398,591 2030 231,227 193,278 37,948 200,368 49,804 150,564 0 0 0 431,595 2035 293,337 245,497 47,841 252,701 62,797 189,904 0 0 0 546,038 2010-2035 5,101,251 4,255,871 845,380 4,440,145 1,084,807 3,355,338 0 0 0 9,541,395 0 0 0 0 0 0 0 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS A-55 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Contribution of Unconventional Gas* to Government Revenue and Private Lease Payments: Wyoming ($Th) 2010 Federal Taxes 723,916 Personal Taxes 524,060 Corporate Taxes 199,856 State and Local Taxes 1,170,784 Personal Taxes 31,098 Corporate Taxes 432,619 Severance Taxes 347,738 Ad Valorem Taxes 359,329 Federal Royalty Payments 352,785 Total Govt Revenue 2,247,486 Lease Payments to Private Landowners 15,515 2015 1,096,250 804,405 291,845 1,746,181 47,418 616,245 532,386 550,132 519,809 3,362,240 2020 1,182,853 869,349 313,503 1,910,967 51,145 654,330 592,865 612,627 572,414 3,666,233 2025 1,350,392 995,113 355,279 2,366,746 59,461 742,218 769,705 795,362 735,929 4,453,067 2030 1,465,865 1,083,147 382,718 2,776,038 65,199 797,764 940,857 972,218 895,030 5,136,932 2035 1,865,673 1,376,649 489,024 3,331,886 82,334 1,019,413 1,096,790 1,133,349 1,045,147 6,242,707 2010-2035 31,950,772 23,511,845 8,438,927 55,256,332 1,399,692 17,682,868 17,790,380 18,383,392 17,110,736 104,317,840 44,669 53,617 72,613 97,412 121,730 1,684,667 Note: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight A-56 JUNE 2012 The Economic and Employment Contributions of Unconventional Gas Development in State Economies Appendix B. Economic Contributions by State, Industry, and Year Prepared for: AMERICA'S NATURAL GAS ALLIANCE Submitted by: IHS Inc. 1150 Connecticut Avenue NW, Suite 401 Washington, DC 20036 June 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES About IHS (ihs.com) IHS Inc. (NYSE: IHS) is a leading source of information and insight in critical areas that shape today's business landscape, including energy and power; design and supply chain; defense, risk and security; environmental, health and safety, and sustainability; country and industry forecasting; and commodities, pricing and cost. IHS has been in business since 1959 and became a publicly traded company on the New York Stock Exchange in 2005. Headquartered in Englewood, Colorado, USA, IHS employs more than 5,100 people in more than 30 countries around the world. About IHS Global Insight IHS Global Insightis one of the leading economic analysis and forecasting firms in the world. With over 600 economists, statisticians, and industry specialists in 25 offices worldwide, IHS Global Insight has an established track record for providing rigorous, objective forecast analysis and data to governments and businesses around the world. Among our areas of expertise are the economic impact, tax implications, and job-creation dynamics within multiple sectors core to national, state and local economies. It helps governments and companies at all levels interpret the impact of proposed investments, policies, programs, and projects. IHS Global Insight was formed by the merger of DRI and WEFA. Still active in an advisory capacity to the firm is the original founder of WEFA, Lawrence R. Klein, the 1980 winner of the Nobel Prize in Economics. For more information, contact: Richard F. Fullenbaum Vice President, Public Sector, IHS Richard.Fullenbaum@ihs.com John W. Larson Vice President, Public Sector, IHS John.Larson@ihs.com For press information, contact: Jim Dorsey Senior Manager Media Relations, IHS Jim.Dorsey@ihs.com IHS 1150 Connecticut Avenue NW, Suite 401 Washington, DC 20036 © 2012 IHS. All information contained herein is obtained by IHS Inc. from sources believed by it to be accurate and reliable. All forecasts and predictions contained herein are believed by IHS, Inc. to be as accurate as the data and methodologies will allow. However, because of the possibilities of human and mechanical error, as well as other factors such as unforeseen and unforeseeable changes in political and economic circumstances beyond IHS's control, the information herein is provided "as is" without warranty of any kind and IHS Inc., AND ALL THIRD PARTY PROVIDERS MAKE NO REPRESENTATIONS OR WARRANTIES EXPRESS OR IMPLIED TO ANY SUBSCRIBER OR ANY OTHER PERSON OR ENTITY AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY OF THE INFORMATION OR FORECASTS CONTAINED HEREIN. ii JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Appendix B. Economic Contributions by State, Industry, and Year Appendix B presents the same contribution results as in Appendix A - employment, value added and labor income - disaggregated by major industry grouping for each of the five year increments (2010, 2015, 2020, 2025, 2030, and 2035). A summary description of the tables is as follows: 1. Employment Contribution by State and Industry. These tables present estimates of employment contributions on a direct, indirect, induced, and total basis for each state by industry for each five-year increment. 2. Value Added Contribution by State and Industry. These tables present estimates of value added contributions on a direct, indirect, induced, and total basis for each state by industry for each five-year increment. 3. Labor Income Contribution by State and Industry. These tables present estimates of labor income contributions on a direct, indirect, induced, and total basis for each state by industry for each five-year increment. IHS B-1 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Employment Contribution by State and Industry Alabama Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-2 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 580 602 13 0 0 0 0 1,195 Indirect 64 89 253 1,058 269 221 1,402 61 3,417 Induced 173 13 41 479 236 775 2,274 73 4,063 Total 237 683 896 1,549 505 996 3,676 134 8,675 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 371 1,657 14 0 0 0 0 2,042 Indirect 89 124 251 1,556 404 357 2,093 86 4,960 Induced 245 19 53 696 336 1,080 3,140 101 5,670 Total 334 514 1,962 2,265 740 1,436 5,233 188 12,673 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 211 1,005 16 0 0 0 0 1,232 Indirect 107 169 235 1,924 437 354 2,193 100 5,519 Induced 289 27 54 841 362 1,110 3,341 112 6,137 Total 395 408 1,294 2,782 799 1,465 5,534 212 12,888 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Alabama Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 118 493 17 0 0 0 0 628 Indirect 102 175 219 2,045 414 319 2,069 97 5,440 Induced 280 29 51 888 351 1,044 3,199 108 5,950 Total 382 322 763 2,951 765 1,362 5,268 205 12,018 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 78 952 17 0 0 0 0 1,047 Indirect 107 197 219 2,392 453 373 2,351 106 6,198 Induced 285 32 56 996 378 1,138 3,542 118 6,546 Total 392 307 1,227 3,405 831 1,511 5,894 224 13,791 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 88 290 23 0 0 0 0 401 Indirect 128 251 270 3,138 546 406 2,739 130 7,608 Induced 338 41 66 1,292 462 1,321 4,195 142 7,858 Total 466 380 625 4,453 1,008 1,727 6,934 272 15,866 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-3 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Arizona Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-4 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 35 152 165 458 242 198 1,615 54 2,919 Induced 117 14 44 209 233 695 2,626 61 3,999 Total 151 166 209 667 474 894 4,242 115 6,918 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 52 203 268 643 394 303 2,399 80 4,341 Induced 175 18 69 294 375 1,054 3,949 89 6,023 Total 227 221 337 938 769 1,356 6,348 168 10,364 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 65 235 343 779 520 389 3,083 105 5,518 Induced 210 21 90 349 490 1,305 4,992 115 7,572 Total 275 256 433 1,128 1,010 1,695 8,074 219 13,090 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Arizona Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 59 222 398 732 559 405 3,259 112 5,745 Induced 201 21 99 343 535 1,348 5,246 124 7,917 Total 261 243 497 1,075 1,094 1,753 8,504 236 13,662 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 69 238 428 767 637 454 3,674 128 6,395 Induced 223 22 106 360 607 1,510 5,882 141 8,852 Total 291 260 535 1,127 1,243 1,964 9,556 269 15,246 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 82 297 543 941 857 575 4,810 168 8,273 Induced 272 28 133 448 818 1,941 7,642 184 11,465 Total 354 325 676 1,389 1,675 2,516 12,452 352 19,737 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-5 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Arkansas Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-6 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 10,567 1,076 933 847 0 217 0 13,640 Indirect 74 195 1,738 888 1,059 884 4,946 138 9,922 Induced 237 11 136 514 745 2,890 8,407 197 13,136 Total 310 10,773 2,950 2,335 2,651 3,774 13,570 335 36,698 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 15,435 1,509 1,837 740 0 247 0 19,767 Indirect 107 275 2,648 1,299 1,569 1,400 7,427 206 14,930 Induced 354 15 201 739 1,089 4,228 12,308 289 19,222 Total 461 15,724 4,357 3,875 3,398 5,628 19,982 495 53,919 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 18,006 1,587 2,207 824 0 244 0 22,868 Indirect 127 318 2,991 1,601 1,903 1,687 8,795 251 17,673 Induced 423 18 234 886 1,270 4,923 14,338 338 22,430 Total 550 18,342 4,813 4,694 3,997 6,609 23,376 589 62,971 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Arkansas Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 18,726 1,714 2,191 841 0 248 0 23,720 Indirect 125 329 3,172 1,627 1,944 1,749 9,145 259 18,350 Induced 428 18 245 924 1,302 5,150 14,993 354 23,414 Total 553 19,073 5,131 4,741 4,086 6,899 24,387 613 65,484 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 19,083 1,732 2,340 864 0 252 0 24,272 Indirect 132 338 3,191 1,739 2,028 1,820 9,437 272 18,958 Induced 446 19 253 975 1,331 5,288 15,411 366 24,089 Total 578 19,440 5,176 5,054 4,223 7,108 25,100 639 67,319 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 22,471 1,977 2,807 983 0 286 0 28,524 Indirect 161 407 3,757 2,091 2,438 2,155 11,188 330 22,526 Induced 546 23 302 1,195 1,585 6,278 18,307 437 28,673 Total 706 22,901 6,037 6,094 5,006 8,433 29,780 766 79,723 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-7 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES California Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-8 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 468 0 4,250 0 0 0 0 4,718 Indirect 160 96 299 1,569 700 693 4,419 135 8,071 Induced 451 15 111 817 539 1,590 6,313 149 9,984 Total 610 580 410 6,636 1,239 2,283 10,732 284 22,773 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 760 547 5,663 0 0 0 0 6,970 Indirect 225 137 456 2,169 1,034 1,014 6,502 199 11,736 Induced 643 22 173 1,179 797 2,314 9,215 217 14,560 Total 868 920 1,176 9,011 1,831 3,328 15,716 416 33,265 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 810 0 6,773 0 0 0 0 7,582 Indirect 276 162 556 2,568 1,257 1,222 7,781 245 14,066 Induced 778 28 220 1,404 968 2,755 10,937 262 17,352 Total 1,054 999 776 10,744 2,225 3,977 18,718 507 39,000 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES California Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 768 0 6,479 0 0 0 0 7,247 Indirect 272 163 587 2,364 1,255 1,205 7,801 245 13,892 Induced 793 28 226 1,367 988 2,763 10,982 265 17,412 Total 1,065 959 813 10,210 2,243 3,968 18,783 510 38,551 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 757 0 6,704 0 0 0 0 7,461 Indirect 291 172 631 2,421 1,347 1,281 8,293 263 14,699 Induced 845 29 248 1,420 1,063 2,925 11,676 284 18,490 Total 1,137 958 879 10,545 2,410 4,205 19,969 547 40,650 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 831 0 7,786 0 0 0 0 8,617 Indirect 358 213 782 2,894 1,658 1,547 10,238 325 18,016 Induced 1,054 36 306 1,744 1,321 3,607 14,443 351 22,861 Total 1,412 1,081 1,088 12,424 2,979 5,153 24,681 676 49,494 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-9 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Colorado Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-10 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 8,490 3,597 8,747 1,163 0 539 0 22,535 Indirect 59 487 2,575 1,033 1,892 2,073 13,248 392 21,759 Induced 313 46 329 706 1,637 7,280 22,324 537 33,172 Total 372 9,023 6,501 10,486 4,692 9,353 36,111 929 77,466 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 12,168 7,214 16,674 2,894 0 1,165 0 40,115 Indirect 98 713 2,927 1,775 3,393 3,610 22,129 636 35,280 Induced 487 71 504 1,081 2,547 11,227 34,389 825 51,130 Total 584 12,952 10,645 19,529 8,834 14,836 57,683 1,461 126,525 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 13,067 7,341 19,053 3,136 0 1,117 0 43,714 Indirect 116 864 2,836 2,029 3,762 3,970 24,242 699 38,518 Induced 560 88 543 1,196 2,754 11,965 36,824 889 54,818 Total 676 14,019 10,720 22,278 9,652 15,935 62,183 1,588 137,050 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Colorado Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 10,767 5,693 18,157 2,298 0 818 0 37,733 Indirect 108 897 2,615 1,775 3,287 3,422 20,883 615 33,601 Induced 536 90 474 1,082 2,448 10,453 32,428 786 48,298 Total 644 11,754 8,781 21,013 8,034 13,875 54,129 1,401 119,632 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 9,474 4,691 18,578 1,926 0 678 0 35,346 Indirect 112 978 2,447 1,706 3,119 3,210 19,537 585 31,695 Induced 550 98 445 1,043 2,326 9,802 30,628 744 45,636 Total 661 10,550 7,583 21,327 7,371 13,012 50,844 1,328 112,677 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 10,274 4,901 21,839 2,006 0 702 0 39,723 Indirect 140 1,236 2,797 1,958 3,552 3,603 22,130 668 36,084 Induced 681 123 505 1,212 2,667 11,099 34,903 846 52,036 Total 822 11,633 8,203 25,009 8,225 14,702 57,735 1,514 127,843 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-11 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Connecticut Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-12 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 9 6 78 666 177 130 1,071 29 2,166 Induced 33 1 25 220 176 440 1,923 33 2,851 Total 42 7 103 886 352 570 2,994 63 5,017 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 13 9 124 864 246 191 1,508 45 2,999 Induced 48 1 34 311 237 627 2,709 50 4,016 Total 60 11 157 1,175 483 818 4,217 95 7,015 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 16 12 151 1,057 293 231 1,771 55 3,586 Induced 58 2 40 387 275 737 3,169 59 4,727 Total 74 13 191 1,445 567 968 4,940 114 8,312 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Connecticut Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 15 11 157 1,059 281 228 1,712 54 3,518 Induced 57 2 38 405 266 723 3,084 58 4,633 Total 72 13 195 1,465 547 951 4,796 112 8,151 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 16 11 163 1,176 291 244 1,756 56 3,715 Induced 59 2 39 447 272 750 3,168 61 4,797 Total 76 13 202 1,623 563 994 4,924 117 8,512 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 20 13 203 1,511 352 299 2,102 68 4,568 Induced 73 2 47 575 327 906 3,808 74 5,813 Total 93 15 250 2,086 678 1,205 5,910 142 10,380 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-13 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Delaware Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-14 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 187 0 0 0 0 187 Indirect 3 0 34 81 55 53 376 12 615 Induced 13 0 10 57 39 149 599 12 879 Total 16 0 44 325 94 202 975 24 1,681 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 236 0 0 0 0 236 Indirect 4 0 50 116 77 72 532 17 869 Induced 18 0 15 83 54 205 866 17 1,258 Total 22 0 65 434 131 277 1,398 35 2,362 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 402 0 0 0 0 402 Indirect 6 0 65 148 109 110 720 24 1,182 Induced 23 0 19 101 71 279 1,144 23 1,658 Total 29 0 84 650 180 389 1,864 47 3,242 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Delaware Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 363 0 0 0 0 363 Indirect 5 0 67 134 107 106 704 23 1,147 Induced 23 0 19 100 71 280 1,138 22 1,653 Total 29 0 87 596 178 386 1,842 45 3,163 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 438 0 0 0 0 438 Indirect 6 0 75 139 123 126 776 26 1,270 Induced 25 0 21 106 79 316 1,252 24 1,824 Total 31 0 96 683 202 442 2,028 50 3,532 Induced 33 0 28 132 107 430 1,642 32 2,403 Total 40 1 128 977 279 613 2,667 66 4,770 2035 Direct Indirect Agriculture 0 7 Mining 0 0 Construction 0 100 Manufacturing 673 171 Transportation and Utilities 0 172 Retail And WholesaleTrade 0 183 Services 0 1,025 Government 0 35 Total 673 1,694 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-15 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES District of Columbia Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-16 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 5 2 6 5 340 8 366 Induced 0 0 3 2 6 22 495 13 539 Total 0 0 7 4 12 27 835 21 905 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 7 2 9 8 510 14 550 Induced 0 0 4 3 8 31 733 20 798 Total 0 0 10 5 17 39 1,242 34 1,348 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 9 3 12 10 641 18 692 Induced 0 0 5 3 10 39 914 25 997 Total 0 0 14 6 21 49 1,555 43 1,689 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES District of Columbia Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 10 2 12 10 641 18 695 Induced 0 0 6 3 10 40 928 27 1,015 Total 0 0 16 5 22 51 1,570 45 1,710 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 11 2 13 11 681 19 738 Induced 0 0 7 3 11 44 994 27 1,087 Total 0 0 18 5 25 56 1,674 46 1,825 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 14 3 18 15 845 25 920 Induced 0 0 10 3 15 57 1,252 36 1,374 Total 0 0 25 6 32 72 2,098 61 2,294 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-17 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Florida Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-18 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 3,032 172 0 0 0 0 3,204 Indirect 77 35 265 542 425 431 3,180 77 5,032 Induced 214 3 82 300 394 1,319 5,118 91 7,522 Total 291 38 3,380 1,014 819 1,750 8,298 168 15,758 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 6,598 241 0 0 0 0 6,838 Indirect 114 53 412 873 710 740 5,307 119 8,328 Induced 322 5 132 457 646 2,192 8,340 140 12,236 Total 435 59 7,142 1,572 1,356 2,932 13,647 259 27,402 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 2,950 324 0 0 0 0 3,274 Indirect 127 52 498 923 762 721 5,690 143 8,916 Induced 372 5 147 505 700 2,318 9,025 160 13,232 Total 499 57 3,596 1,751 1,462 3,039 14,716 302 25,422 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Florida Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 752 331 0 0 0 0 1,084 Indirect 120 43 534 813 718 651 5,590 143 8,611 Induced 373 4 143 476 678 2,206 8,818 159 12,858 Total 492 48 1,429 1,621 1,396 2,857 14,408 301 22,552 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 4,558 368 0 0 0 0 4,926 Indirect 134 50 591 951 861 865 6,901 162 10,515 Induced 418 5 169 520 803 2,680 10,610 184 15,390 Total 553 56 5,318 1,839 1,664 3,545 17,512 346 30,831 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 536 454 0 0 0 0 990 Indirect 155 52 762 1,018 959 906 8,041 198 12,091 Induced 510 5 200 597 911 3,014 12,366 218 17,822 Total 664 58 1,499 2,069 1,870 3,920 20,407 417 30,903 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-19 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Georgia Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-20 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 111 841 0 0 0 0 952 Indirect 74 56 219 1,025 590 447 2,767 91 5,269 Induced 193 5 63 730 543 1,237 4,194 108 7,073 Total 266 61 393 2,596 1,133 1,684 6,961 199 13,294 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 1,106 0 0 0 0 1,106 Indirect 95 68 291 1,458 882 634 4,039 134 7,601 Induced 261 7 89 1,070 809 1,759 5,945 154 10,093 Total 356 75 379 3,633 1,692 2,393 9,984 289 18,800 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 174 560 0 0 0 0 734 Indirect 115 82 349 1,786 1,056 761 4,884 166 9,198 Induced 309 9 113 1,323 982 2,061 7,002 185 11,984 Total 424 91 636 3,669 2,037 2,822 11,886 351 21,915 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Georgia Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 53 166 0 0 0 0 220 Indirect 112 82 365 1,819 1,035 754 4,929 166 9,263 Induced 310 9 118 1,380 992 2,019 6,967 185 11,981 Total 423 91 537 3,366 2,027 2,773 11,896 350 21,463 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 76 759 0 0 0 0 835 Indirect 125 88 391 2,027 1,172 887 5,553 182 10,425 Induced 344 9 137 1,507 1,103 2,301 7,894 204 13,499 Total 470 97 603 4,292 2,275 3,188 13,447 386 24,759 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 113 0 0 0 0 113 Indirect 155 107 487 2,490 1,434 1,060 6,772 224 12,728 Induced 430 12 172 1,876 1,376 2,746 9,564 247 16,422 Total 585 118 659 4,478 2,809 3,806 16,336 471 29,262 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-21 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Idaho Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-22 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 43 29 43 157 78 52 347 16 765 Induced 128 2 11 103 72 179 564 18 1,076 Total 171 31 55 259 150 231 911 33 1,841 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 63 47 49 241 115 79 532 24 1,150 Induced 187 3 13 155 105 268 860 26 1,616 Total 250 50 62 395 220 347 1,392 50 2,766 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 84 72 51 288 138 101 662 31 1,427 Induced 230 5 13 189 126 341 1,073 33 2,009 Total 314 77 64 477 264 442 1,735 64 3,437 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Idaho Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 86 81 50 285 137 104 686 31 1,459 Induced 231 6 12 200 127 355 1,111 34 2,076 Total 317 87 62 484 264 459 1,797 65 3,536 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 93 92 49 296 147 113 753 34 1,579 Induced 243 7 12 216 135 385 1,219 37 2,255 Total 336 99 62 512 282 498 1,973 71 3,833 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 116 123 59 347 185 151 952 43 1,975 Induced 297 9 15 268 171 486 1,549 46 2,842 Total 413 132 73 615 356 637 2,501 90 4,818 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-23 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Illinois Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-24 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 2,295 0 519 0 0 0 0 2,814 Indirect 73 181 307 2,839 1,013 695 4,777 131 10,016 Induced 265 17 118 1,162 898 2,177 8,148 159 12,943 Total 338 2,493 425 4,519 1,911 2,872 12,925 290 25,773 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 3,163 0 562 0 0 0 0 3,724 Indirect 109 246 476 4,136 1,487 980 6,760 186 14,380 Induced 389 22 186 1,699 1,312 3,072 11,384 220 18,282 Total 498 3,432 662 6,397 2,798 4,052 18,144 405 36,387 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4,515 0 780 0 0 0 0 5,295 Indirect 132 314 565 4,930 1,881 1,200 8,394 232 17,648 Induced 455 27 240 2,062 1,638 3,834 14,250 272 22,778 Total 587 4,856 805 7,772 3,519 5,034 22,643 504 45,721 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Illinois Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4,156 0 762 0 0 0 0 4,918 Indirect 126 293 576 4,650 1,866 1,166 8,353 227 17,257 Induced 442 25 240 2,051 1,652 3,765 14,125 268 22,568 Total 568 4,475 816 7,463 3,518 4,931 22,478 494 44,743 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4,799 0 835 0 0 0 0 5,634 Indirect 131 316 598 4,833 2,037 1,244 8,899 244 18,303 Induced 453 26 262 2,171 1,793 4,079 15,221 288 24,293 Total 584 5,141 860 7,839 3,830 5,323 24,119 533 48,229 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 6,787 0 1,092 0 0 0 0 7,879 Indirect 152 414 740 5,854 2,593 1,544 11,191 309 22,797 Induced 534 32 336 2,702 2,276 5,241 19,494 366 30,981 Total 686 7,233 1,076 9,648 4,870 6,785 30,685 674 61,657 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-25 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Indiana Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-26 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 516 0 0 0 0 516 Indirect 52 59 169 2,321 501 282 1,593 60 5,037 Induced 200 9 55 880 408 827 2,819 68 5,266 Total 251 69 223 3,717 909 1,109 4,412 128 10,819 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 586 0 0 0 0 586 Indirect 77 80 266 3,237 698 389 2,265 87 7,100 Induced 296 13 85 1,286 568 1,162 4,015 96 7,521 Total 373 93 351 5,110 1,266 1,551 6,280 183 15,206 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 898 0 0 0 0 898 Indirect 95 95 316 3,986 862 499 2,898 108 8,859 Induced 349 15 104 1,578 686 1,447 5,011 116 9,307 Total 444 110 419 6,463 1,548 1,947 7,909 224 19,065 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Indiana Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 820 0 0 0 0 820 Indirect 92 93 322 4,036 831 489 2,946 107 8,915 Induced 341 15 101 1,662 679 1,448 5,089 116 9,451 Total 433 107 423 6,518 1,510 1,937 8,034 223 19,186 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 986 0 0 0 0 986 Indirect 96 97 334 4,452 884 539 3,226 115 9,744 Induced 346 15 106 1,825 715 1,566 5,505 125 10,204 Total 442 112 440 7,264 1,599 2,106 8,731 239 20,934 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 1,503 0 0 0 0 1,503 Indirect 117 120 424 5,563 1,110 710 4,184 144 12,371 Induced 415 18 134 2,315 889 2,003 7,034 155 12,963 Total 532 138 558 9,381 1,998 2,714 11,218 299 26,837 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-27 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Iowa Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-28 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 285 0 30 0 0 0 0 315 Indirect 81 21 93 669 234 142 736 36 2,012 Induced 295 2 27 369 194 472 1,457 40 2,856 Total 376 309 120 1,068 428 614 2,193 77 5,183 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 555 0 96 0 0 0 0 650 Indirect 133 28 152 966 379 225 1,142 56 3,082 Induced 485 3 44 548 297 724 2,201 61 4,362 Total 618 586 196 1,609 676 949 3,343 117 8,095 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 656 0 126 0 0 0 0 782 Indirect 169 33 187 1,185 475 272 1,425 69 3,815 Induced 595 4 55 661 368 880 2,690 74 5,326 Total 764 692 241 1,972 843 1,152 4,115 144 9,923 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Iowa Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 647 0 151 0 0 0 0 798 Indirect 171 26 208 1,248 495 270 1,504 70 3,993 Induced 619 3 58 689 390 894 2,784 75 5,511 Total 790 676 266 2,088 884 1,164 4,289 145 10,302 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 715 0 177 0 0 0 0 891 Indirect 190 24 225 1,410 570 291 1,657 75 4,442 Induced 677 2 63 755 448 960 3,012 80 5,997 Total 867 741 288 2,342 1,017 1,251 4,669 155 11,330 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 928 0 222 0 0 0 0 1,150 Indirect 248 27 294 1,824 735 366 2,135 93 5,723 Induced 885 3 82 969 579 1,213 3,824 99 7,654 Total 1,133 958 377 3,015 1,314 1,579 5,960 192 14,526 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-29 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Kansas Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-30 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 165 0 493 0 0 0 0 658 Indirect 41 79 109 413 244 154 900 52 1,992 Induced 184 12 26 248 182 473 1,531 47 2,703 Total 224 256 135 1,155 425 627 2,431 99 5,353 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 15 0 808 0 0 0 0 824 Indirect 64 108 128 607 381 228 1,309 84 2,910 Induced 284 16 37 374 268 660 2,154 67 3,861 Total 348 140 165 1,790 649 888 3,463 151 7,594 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1 0 879 0 0 0 0 880 Indirect 84 123 141 753 459 274 1,577 99 3,509 Induced 352 19 43 456 328 795 2,573 80 4,645 Total 435 143 183 2,088 787 1,069 4,150 178 9,034 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Kansas Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 874 0 0 0 0 874 Indirect 84 120 143 817 461 274 1,592 97 3,587 Induced 358 18 42 485 336 813 2,607 80 4,740 Total 442 137 185 2,176 796 1,087 4,199 178 9,201 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 902 0 0 0 0 902 Indirect 92 123 148 971 494 291 1,727 104 3,950 Induced 387 18 44 544 361 862 2,800 85 5,100 Total 479 141 193 2,416 855 1,153 4,526 189 9,952 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 1,035 0 0 0 0 1,035 Indirect 120 151 182 1,292 617 355 2,181 127 5,024 Induced 497 22 54 710 455 1,056 3,512 105 6,411 Total 617 173 236 3,037 1,072 1,411 5,693 231 12,470 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-31 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Kentucky Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-32 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,310 285 281 215 0 54 0 2,145 Indirect 59 311 281 931 385 273 1,550 64 3,855 Induced 279 42 43 476 333 892 2,727 78 4,870 Total 338 1,663 609 1,688 933 1,165 4,331 142 10,870 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,577 287 291 135 0 45 0 2,336 Indirect 83 429 363 1,405 528 359 2,066 89 5,321 Induced 399 57 57 721 461 1,167 3,629 104 6,596 Total 481 2,064 707 2,417 1,124 1,526 5,739 193 14,252 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,517 302 504 150 0 44 0 2,517 Indirect 111 463 370 1,795 689 442 2,474 111 6,455 Induced 506 61 66 891 576 1,329 4,180 123 7,732 Total 618 2,041 739 3,189 1,416 1,770 6,698 234 16,705 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Kentucky Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,385 326 436 153 0 45 0 2,345 Indirect 114 416 359 1,892 718 426 2,413 111 6,448 Induced 524 57 66 938 612 1,292 4,099 124 7,711 Total 638 1,858 751 3,266 1,483 1,717 6,557 235 16,505 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,313 330 518 158 0 46 0 2,365 Indirect 125 419 361 2,165 806 457 2,537 121 6,992 Induced 570 58 70 1,034 679 1,342 4,282 132 8,166 Total 695 1,791 761 3,717 1,642 1,799 6,865 254 17,523 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,491 376 781 179 0 52 0 2,879 Indirect 159 492 443 2,786 1,027 582 3,149 156 8,794 Induced 726 69 88 1,312 853 1,650 5,287 167 10,152 Total 885 2,052 907 4,879 2,060 2,232 8,487 323 21,825 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-33 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Louisiana Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-34 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 9,312 14,525 3,329 1,870 0 859 0 29,896 Indirect 117 652 2,239 1,725 1,896 2,357 12,816 195 21,997 Induced 341 60 302 611 1,430 6,708 19,333 343 29,130 Total 458 10,024 17,067 5,665 5,196 9,065 33,008 539 81,022 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 17,356 14,794 5,421 2,079 0 690 0 40,341 Indirect 153 1,120 5,168 2,508 2,817 3,605 19,591 310 35,273 Induced 551 89 508 1,010 2,397 11,391 32,656 567 49,168 Total 704 18,565 20,470 8,939 7,293 14,996 52,937 878 124,782 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 23,952 9,539 4,035 2,427 0 712 0 40,665 Indirect 161 1,424 6,993 2,588 3,144 3,873 22,541 370 41,093 Induced 651 108 608 1,213 2,866 13,646 39,027 679 58,797 Total 812 25,484 17,140 7,835 8,438 17,519 62,279 1,049 140,556 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Louisiana Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 28,118 9,367 3,557 2,477 0 726 0 44,245 Indirect 165 1,611 8,464 2,641 3,404 4,261 25,182 406 46,135 Induced 720 115 697 1,349 3,268 15,697 44,818 774 67,437 Total 885 29,845 18,529 7,547 9,149 19,958 70,726 1,180 157,818 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 29,542 7,892 3,834 2,561 0 743 0 44,571 Indirect 168 1,700 8,923 2,783 3,516 4,391 26,082 424 47,988 Induced 748 122 728 1,427 3,397 16,340 46,697 806 70,266 Total 917 31,364 17,544 8,043 9,474 20,731 73,521 1,230 162,825 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 37,440 8,124 3,555 3,345 0 964 0 53,428 Indirect 205 2,142 11,349 3,363 4,314 5,333 32,356 524 59,587 Induced 931 154 908 1,795 4,235 20,359 58,159 999 87,540 Total 1,136 39,736 20,382 8,713 11,895 25,691 91,479 1,523 200,555 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-35 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Maine Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-36 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 32 1 36 156 60 46 293 13 637 Induced 61 0 11 100 55 196 590 15 1,029 Total 94 1 47 256 114 242 882 28 1,666 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 45 2 52 218 83 67 426 19 913 Induced 82 0 15 147 74 283 855 22 1,477 Total 127 3 67 365 157 349 1,281 41 2,390 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 55 4 64 274 97 80 514 23 1,111 Induced 97 0 17 184 84 335 1,024 26 1,767 Total 151 4 81 458 181 416 1,537 49 2,878 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Maine Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 53 5 68 277 92 78 516 23 1,112 Induced 93 1 17 189 81 332 1,030 25 1,768 Total 145 6 86 466 173 411 1,546 48 2,881 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 56 7 73 302 95 82 549 24 1,189 Induced 96 1 18 205 83 351 1,094 27 1,873 Total 152 8 92 507 178 433 1,643 51 3,063 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 69 11 93 370 113 100 676 29 1,461 Induced 120 1 23 256 99 431 1,352 32 2,312 Total 189 12 116 625 212 530 2,028 62 3,774 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-37 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Maryland Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-38 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 17 22 226 390 272 178 1,781 61 2,945 Induced 61 2 75 219 269 647 2,718 72 4,063 Total 78 23 301 609 541 824 4,499 132 7,008 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 26 30 334 573 392 256 2,654 94 4,359 Induced 94 3 108 322 375 929 3,968 108 5,905 Total 119 33 441 894 767 1,185 6,622 202 10,263 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 33 44 415 698 484 310 3,253 118 5,355 Induced 118 4 133 388 453 1,129 4,855 132 7,211 Total 151 48 548 1,085 937 1,439 8,108 250 12,566 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Maryland Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 34 47 451 643 481 308 3,157 120 5,241 Induced 122 4 135 382 451 1,159 4,889 136 7,279 Total 156 51 586 1,025 932 1,467 8,047 256 12,519 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 37 53 489 648 528 333 3,305 129 5,523 Induced 131 5 145 395 490 1,250 5,226 146 7,787 Total 168 58 635 1,043 1,018 1,583 8,531 275 13,310 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 48 68 637 770 683 418 4,065 165 6,854 Induced 168 6 185 486 632 1,581 6,537 185 9,780 Total 216 74 822 1,256 1,315 1,999 10,602 350 16,634 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-39 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Massachusetts Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-40 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 136 0 0 0 0 136 Indirect 9 5 82 449 142 132 1,196 30 2,046 Induced 40 0 29 221 136 431 1,895 34 2,787 Total 50 6 111 806 278 564 3,091 63 4,968 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 193 0 0 0 0 193 Indirect 13 6 122 648 205 193 1,770 44 3,002 Induced 54 1 42 325 194 622 2,738 49 4,025 Total 67 7 164 1,167 399 815 4,507 93 7,220 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 355 0 0 0 0 355 Indirect 16 8 144 802 250 240 2,153 55 3,667 Induced 65 1 52 398 232 741 3,294 60 4,842 Total 81 8 196 1,555 482 981 5,447 115 8,865 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Massachusetts Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 324 0 0 0 0 324 Indirect 16 8 151 733 239 231 2,130 54 3,562 Induced 64 1 52 389 225 722 3,258 59 4,771 Total 80 9 203 1,446 464 953 5,389 113 8,657 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 396 0 0 0 0 396 Indirect 17 9 158 741 247 244 2,251 57 3,724 Induced 68 1 56 403 230 756 3,438 63 5,014 Total 85 10 214 1,539 477 1,000 5,688 120 9,134 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 615 0 0 0 0 615 Indirect 22 11 199 887 295 301 2,784 70 4,569 Induced 85 1 71 494 274 925 4,244 78 6,172 Total 107 13 270 1,995 569 1,225 7,029 148 11,356 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-41 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Michigan Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-42 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,230 0 5,738 0 0 0 0 6,968 Indirect 70 144 437 2,375 837 548 4,124 113 8,647 Induced 255 10 111 908 610 2,378 8,023 154 12,448 Total 325 1,384 548 9,021 1,446 2,925 12,147 267 28,063 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 890 0 8,217 0 0 0 0 9,107 Indirect 104 198 506 3,778 1,195 747 5,561 160 12,248 Induced 352 13 155 1,354 844 3,107 10,538 209 16,571 Total 455 1,102 661 13,349 2,038 3,853 16,099 369 37,926 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 573 0 10,981 0 0 0 0 11,554 Indirect 132 250 525 4,817 1,526 915 6,758 197 15,120 Induced 413 16 187 1,644 1,035 3,746 12,686 252 19,979 Total 545 839 712 17,442 2,561 4,661 19,445 449 46,653 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Michigan Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 363 0 10,317 0 0 0 0 10,680 Indirect 127 242 501 5,036 1,486 883 6,528 192 14,995 Induced 391 16 182 1,691 1,020 3,595 12,139 244 19,278 Total 518 621 683 17,044 2,507 4,478 18,667 436 44,953 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 259 0 11,648 0 0 0 0 11,907 Indirect 137 260 510 5,610 1,649 965 7,009 207 16,346 Induced 407 17 195 1,832 1,112 3,905 12,998 262 20,728 Total 544 536 705 19,089 2,761 4,870 20,007 469 48,982 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 294 0 15,657 0 0 0 0 15,951 Indirect 171 323 644 7,051 2,165 1,240 8,998 262 20,855 Induced 507 22 250 2,312 1,437 5,058 16,655 332 26,574 Total 678 639 895 25,020 3,602 6,299 25,653 595 63,380 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-43 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Minnesota Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-44 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 352 0 0 0 0 0 0 352 Indirect 72 123 123 1,142 318 246 1,756 58 3,837 Induced 271 4 41 568 290 786 3,054 67 5,082 Total 343 480 164 1,710 607 1,032 4,810 125 9,271 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 860 0 0 0 0 0 0 860 Indirect 104 187 178 1,679 491 382 2,700 91 5,811 Induced 388 7 65 877 428 1,237 4,722 104 7,827 Total 493 1,053 243 2,556 919 1,618 7,422 195 14,499 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 917 0 0 0 0 0 0 917 Indirect 130 225 210 2,068 596 462 3,286 112 7,087 Induced 464 8 79 1,068 508 1,467 5,669 125 9,388 Total 593 1,150 289 3,135 1,104 1,929 8,955 237 17,393 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Minnesota Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 778 0 0 0 0 0 0 778 Indirect 133 208 222 1,984 601 461 3,283 111 7,003 Induced 480 9 79 1,063 517 1,463 5,669 124 9,404 Total 614 994 301 3,046 1,118 1,924 8,953 235 17,184 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 731 0 0 0 0 0 0 731 Indirect 147 213 239 2,113 649 501 3,506 118 7,487 Induced 517 9 85 1,121 552 1,550 6,031 131 9,995 Total 663 953 324 3,234 1,201 2,050 9,537 250 18,213 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 822 0 0 0 0 0 0 822 Indirect 184 256 306 2,624 813 639 4,372 147 9,341 Induced 646 12 106 1,405 688 1,936 7,519 162 12,474 Total 830 1,090 411 4,030 1,501 2,576 11,891 310 22,638 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-45 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Mississppi Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-46 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 92 0 0 0 0 0 92 Indirect 54 40 61 389 185 78 497 33 1,338 Induced 145 6 15 275 176 296 877 37 1,829 Total 199 46 168 665 361 374 1,375 70 3,259 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 2,703 0 0 0 0 0 2,703 Indirect 88 63 101 619 369 293 1,362 59 2,953 Induced 233 9 35 419 319 694 1,991 71 3,772 Total 321 72 2,839 1,038 688 987 3,354 130 9,428 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 1,300 0 0 0 0 0 1,300 Indirect 98 70 111 700 397 216 1,201 65 2,857 Induced 284 11 32 506 362 645 1,902 74 3,815 Total 381 81 1,443 1,205 759 861 3,103 139 7,972 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Mississppi Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 765 0 0 0 0 0 765 Indirect 93 68 115 661 382 179 1,101 63 2,663 Induced 292 10 31 508 360 596 1,802 71 3,672 Total 385 78 911 1,170 743 775 2,904 134 7,099 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 681 0 0 0 0 0 681 Indirect 101 69 122 678 407 183 1,177 67 2,803 Induced 320 10 33 527 383 626 1,927 75 3,901 Total 420 79 836 1,205 790 809 3,104 142 7,386 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 614 0 0 0 0 0 614 Indirect 125 82 153 772 501 206 1,446 83 3,368 Induced 410 12 41 623 474 754 2,381 91 4,786 Total 535 94 808 1,396 974 960 3,827 174 8,768 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-47 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Missouri Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-48 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 343 0 3,790 0 0 0 0 4,133 Indirect 32 29 102 525 421 236 1,661 64 3,070 Induced 173 3 44 280 252 920 3,078 78 4,828 Total 206 375 146 4,596 673 1,156 4,739 142 12,031 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 539 0 5,467 0 0 0 0 6,005 Indirect 50 39 154 786 615 344 2,396 93 4,477 Induced 263 4 62 420 365 1,331 4,387 112 6,945 Total 313 582 216 6,672 980 1,675 6,783 205 17,427 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 697 0 7,005 0 0 0 0 7,702 Indirect 63 45 191 972 770 432 2,992 118 5,583 Induced 322 5 78 511 452 1,663 5,425 140 8,596 Total 386 747 269 8,489 1,222 2,095 8,416 257 21,881 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Missouri Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 647 0 7,196 0 0 0 0 7,843 Indirect 61 42 199 998 772 432 3,026 118 5,649 Induced 323 5 78 525 457 1,681 5,465 141 8,676 Total 384 694 278 8,719 1,229 2,112 8,491 260 22,168 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 699 0 8,003 0 0 0 0 8,702 Indirect 67 45 212 1,122 840 469 3,299 129 6,182 Induced 344 5 85 570 495 1,830 5,923 154 9,406 Total 411 749 297 9,695 1,334 2,299 9,222 283 24,290 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 885 0 9,861 0 0 0 0 10,746 Indirect 83 55 266 1,421 1,037 582 4,096 160 7,699 Induced 429 6 106 714 615 2,273 7,325 190 11,659 Total 513 947 372 11,996 1,651 2,855 11,421 351 30,105 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-49 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Montana Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-50 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 89 0 0 0 0 0 0 90 Indirect 22 76 49 55 79 39 267 13 600 Induced 92 9 9 35 71 156 514 15 902 Total 114 174 59 90 150 196 781 28 1,591 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 81 2 0 1 0 0 0 85 Indirect 35 130 57 79 119 54 374 19 866 Induced 150 15 11 52 106 211 718 21 1,285 Total 185 226 70 131 227 265 1,092 40 2,236 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 73 6 0 3 0 1 0 82 Indirect 47 160 57 96 143 64 455 23 1,045 Induced 195 18 13 63 125 253 857 26 1,551 Total 241 251 76 159 271 318 1,313 49 2,677 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Montana Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 66 5 0 2 0 1 0 74 Indirect 49 159 57 97 139 64 462 23 1,050 Induced 205 19 13 66 123 258 866 26 1,575 Total 254 244 75 163 264 322 1,328 49 2,699 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 57 5 0 2 0 1 0 65 Indirect 55 173 57 106 143 68 490 25 1,118 Induced 228 20 14 71 126 275 917 28 1,680 Total 283 251 75 177 272 343 1,408 53 2,862 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 60 5 0 2 0 1 0 69 Indirect 72 226 69 132 177 85 610 31 1,402 Induced 297 27 17 90 155 344 1,145 34 2,110 Total 369 313 92 222 335 429 1,756 65 3,582 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-51 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Nebraska Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-52 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 104 0 0 0 0 104 Indirect 45 10 66 229 283 99 566 25 1,323 Induced 169 1 18 177 175 276 930 26 1,773 Total 214 11 84 510 458 375 1,496 51 3,199 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 276 0 0 0 0 276 Indirect 67 12 96 341 462 169 940 41 2,127 Induced 249 1 25 267 274 430 1,453 40 2,739 Total 316 13 121 884 736 599 2,393 81 5,142 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 332 0 0 0 0 332 Indirect 90 16 111 433 579 206 1,208 51 2,695 Induced 318 2 30 328 338 528 1,815 48 3,407 Total 407 18 141 1,093 917 735 3,024 99 6,433 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Nebraska Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 364 0 0 0 0 364 Indirect 90 17 123 459 572 212 1,278 52 2,804 Induced 326 2 31 336 340 544 1,883 49 3,511 Total 416 19 154 1,160 911 757 3,161 101 6,679 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 405 0 0 0 0 405 Indirect 100 17 136 529 611 231 1,413 57 3,095 Induced 351 2 35 364 360 587 2,048 52 3,799 Total 452 19 171 1,298 971 817 3,461 109 7,299 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 498 0 0 0 0 498 Indirect 123 19 176 697 758 286 1,810 70 3,939 Induced 435 2 45 467 448 735 2,582 65 4,780 Total 557 21 221 1,662 1,206 1,021 4,393 135 9,216 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-53 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Nevada Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-54 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 498 7 0 0 0 0 505 Indirect 2 57 31 64 67 56 458 7 741 Induced 6 4 10 28 66 165 617 10 906 Total 8 60 539 99 134 221 1,075 17 2,153 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 10 0 0 0 0 10 Indirect 2 75 27 68 76 35 496 9 789 Induced 9 5 9 37 72 144 656 11 944 Total 12 79 36 116 148 180 1,153 20 1,743 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 80 13 0 0 0 0 93 Indirect 3 95 30 84 100 50 657 12 1,031 Induced 12 6 12 47 94 195 870 14 1,250 Total 15 101 122 144 194 245 1,527 26 2,375 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Nevada Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 12 0 0 0 0 12 Indirect 3 93 28 76 107 45 650 13 1,015 Induced 12 7 12 47 102 189 873 15 1,256 Total 15 100 41 135 209 235 1,522 28 2,284 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 13 0 0 0 0 13 Indirect 4 101 28 79 122 50 721 15 1,121 Induced 13 7 14 50 116 212 974 17 1,403 Total 17 108 42 142 238 262 1,696 32 2,537 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 17 0 0 0 0 17 Indirect 5 126 35 95 166 64 927 19 1,438 Induced 17 9 18 62 158 275 1,263 21 1,823 Total 22 135 53 174 324 339 2,190 41 3,278 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-55 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New Hampshire Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-56 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 4 1 10 109 18 22 118 4 286 Induced 7 0 3 32 17 77 219 5 361 Total 11 1 14 141 35 99 337 9 647 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 5 2 15 145 24 32 180 7 410 Induced 10 0 5 45 23 113 324 7 529 Total 15 2 20 190 47 145 504 14 938 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 6 2 19 171 31 43 230 8 511 Induced 13 0 6 55 28 142 407 9 661 Total 19 3 24 227 58 185 637 18 1,171 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New Hampshire Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 6 3 20 164 30 42 230 8 503 Induced 13 0 6 56 27 142 409 10 662 Total 19 3 25 220 57 184 639 18 1,165 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 6 3 21 168 32 47 250 9 536 Induced 14 0 6 60 29 153 441 10 713 Total 20 3 27 228 61 200 691 19 1,249 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 8 4 27 208 40 61 317 11 675 Induced 17 0 7 75 36 193 559 13 901 Total 25 4 35 283 75 254 876 25 1,576 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-57 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New Jersey Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-58 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 134 458 0 0 0 0 592 Indirect 10 7 98 434 278 241 1,556 45 2,669 Induced 36 1 34 280 256 622 2,323 52 3,604 Total 46 8 267 1,172 534 863 3,879 97 6,865 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 465 0 0 0 0 465 Indirect 15 9 139 554 407 333 2,220 64 3,742 Induced 52 1 46 378 373 877 3,265 72 5,064 Total 67 10 185 1,397 780 1,210 5,485 136 9,271 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 676 0 0 0 0 676 Indirect 18 11 176 652 507 412 2,684 80 4,540 Induced 64 1 58 453 457 1,102 3,932 88 6,156 Total 82 12 234 1,781 964 1,514 6,616 168 11,371 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New Jersey Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 602 0 0 0 0 602 Indirect 18 11 186 576 512 396 2,670 79 4,448 Induced 65 1 57 447 472 1,112 3,901 87 6,142 Total 83 12 243 1,625 984 1,508 6,571 166 11,192 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 709 0 0 0 0 709 Indirect 21 12 180 573 561 425 2,830 84 4,686 Induced 74 1 55 468 512 1,204 4,117 93 6,525 Total 96 13 235 1,750 1,074 1,629 6,947 177 11,920 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 1,063 0 0 0 0 1,063 Indirect 27 15 208 675 712 544 3,543 105 5,828 Induced 94 1 62 580 647 1,543 5,129 115 8,173 Total 121 16 271 2,318 1,359 2,087 8,672 220 15,064 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-59 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New Mexico Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-60 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 5,493 509 702 53 0 39 0 6,797 Indirect 14 203 1,065 141 394 513 3,032 101 5,462 Induced 98 24 90 104 370 1,843 5,483 149 8,159 Total 112 5,720 1,664 947 817 2,355 8,554 249 20,417 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4,823 109 1,006 60 0 18 0 6,017 Indirect 19 277 991 181 440 532 3,055 112 5,607 Induced 124 36 89 122 374 1,778 5,322 149 7,993 Total 143 5,137 1,188 1,309 874 2,310 8,395 261 19,617 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 3,653 109 1,084 63 0 17 0 4,928 Indirect 24 311 776 208 439 498 2,855 113 5,224 Induced 139 44 82 129 343 1,550 4,705 138 7,130 Total 163 4,009 967 1,421 846 2,048 7,577 251 17,282 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New Mexico Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 3,043 422 1,246 65 0 18 0 4,794 Indirect 24 317 674 197 438 505 2,788 110 5,052 Induced 139 46 79 125 325 1,448 4,426 131 6,720 Total 163 3,406 1,174 1,568 828 1,954 7,231 242 16,565 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 2,764 119 1,239 66 0 18 0 4,207 Indirect 26 339 627 194 439 485 2,726 113 4,949 Induced 146 50 79 127 317 1,385 4,270 129 6,503 Total 172 3,153 825 1,560 822 1,870 7,014 242 15,659 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 3,157 136 1,433 76 0 20 0 4,822 Indirect 32 437 735 228 521 568 3,238 136 5,894 Induced 183 65 97 156 377 1,640 5,075 155 7,747 Total 215 3,658 967 1,817 973 2,208 8,333 291 18,462 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-61 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New York Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-62 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 21 41 347 0 0 0 0 408 Indirect 51 57 467 1,615 846 685 6,770 206 10,696 Induced 179 6 164 871 826 2,187 11,316 234 15,783 Total 230 83 671 2,833 1,672 2,872 18,086 440 26,887 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 13 0 373 0 0 0 0 386 Indirect 76 81 559 2,274 1,196 1,000 10,196 303 15,684 Induced 260 8 215 1,239 1,158 3,150 16,612 334 22,977 Total 336 102 774 3,886 2,353 4,150 26,808 637 39,047 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 8 22 555 0 0 0 0 584 Indirect 94 105 602 2,727 1,352 1,226 12,161 373 18,639 Induced 314 11 253 1,463 1,292 3,858 19,783 403 27,377 Total 408 124 876 4,744 2,644 5,084 31,944 776 46,600 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New York Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 5 0 507 0 0 0 0 512 Indirect 93 107 588 2,507 1,226 1,207 12,012 368 18,108 Induced 319 11 248 1,422 1,190 3,845 19,612 401 27,049 Total 412 123 836 4,436 2,416 5,052 31,624 769 45,669 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 3 0 608 0 0 0 0 611 Indirect 106 115 559 2,567 1,241 1,297 12,527 392 18,803 Induced 352 12 249 1,478 1,199 4,066 20,427 425 28,208 Total 458 130 808 4,652 2,441 5,363 32,954 817 47,622 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4 0 923 0 0 0 0 927 Indirect 131 142 652 3,076 1,467 1,630 15,295 482 22,875 Induced 443 14 298 1,817 1,419 5,077 24,985 523 34,575 Total 574 160 950 5,816 2,886 6,707 40,279 1,005 58,377 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-63 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES North Carolina Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-64 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 102 0 0 0 0 0 102 Indirect 68 36 258 1,342 371 330 2,326 92 4,825 Induced 209 3 72 929 342 1,054 3,737 105 6,451 Total 277 40 432 2,271 713 1,384 6,063 197 11,377 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 92 49 379 1,896 525 480 3,519 139 7,078 Induced 308 5 106 1,350 477 1,558 5,536 153 9,493 Total 400 53 485 3,246 1,001 2,037 9,055 292 16,570 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 188 0 0 0 0 0 188 Indirect 109 57 472 2,334 645 608 4,474 177 8,877 Induced 370 6 139 1,626 580 1,913 7,021 193 11,847 Total 479 63 799 3,960 1,225 2,521 11,495 370 20,912 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES North Carolina Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 103 55 516 2,183 625 595 4,571 181 8,829 Induced 372 6 146 1,592 577 1,903 7,223 198 12,018 Total 475 61 663 3,775 1,202 2,499 11,794 379 20,847 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 110 60 568 2,234 661 646 5,009 199 9,487 Induced 396 6 165 1,646 611 2,055 7,961 216 13,055 Total 506 67 733 3,880 1,271 2,701 12,970 415 22,542 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 148 75 744 2,623 810 795 6,351 252 11,798 Induced 520 8 216 1,992 754 2,558 10,152 274 16,473 Total 668 83 960 4,615 1,564 3,353 16,503 526 28,271 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-65 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES North Dakota Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-66 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 27 89 25 70 60 40 169 10 489 Induced 98 15 8 38 49 112 321 12 652 Total 124 104 33 108 109 151 490 22 1,141 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 40 222 42 114 98 61 268 16 861 Induced 144 37 13 62 78 167 486 18 1,006 Total 184 260 56 176 177 228 754 33 1,867 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 52 299 51 153 120 74 351 20 1,118 Induced 178 51 16 85 94 207 616 22 1,269 Total 230 350 68 238 213 280 967 41 2,387 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES North Dakota Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 53 335 55 162 117 72 376 20 1,190 Induced 190 57 17 95 92 212 655 22 1,340 Total 243 392 72 257 209 284 1,031 42 2,531 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 58 375 61 188 124 77 425 22 1,331 Induced 203 65 19 110 97 230 734 24 1,482 Total 261 440 80 298 221 307 1,160 45 2,812 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 74 502 76 238 155 98 559 27 1,729 Induced 256 86 23 145 121 294 960 30 1,916 Total 330 588 99 383 276 392 1,519 57 3,645 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-67 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Ohio Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-68 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 653 0 4,326 0 0 0 0 4,979 Indirect 65 150 345 3,976 1,282 1,208 5,474 143 12,643 Induced 273 20 117 1,280 874 2,554 8,556 165 13,840 Total 338 824 462 9,581 2,156 3,762 14,030 309 31,462 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 727 0 5,049 0 0 0 0 5,776 Indirect 92 208 471 5,541 1,789 1,536 7,246 201 17,085 Induced 371 28 157 1,821 1,253 3,319 11,331 224 18,504 Total 463 963 628 12,410 3,043 4,855 18,578 425 41,366 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,055 0 7,820 0 0 0 0 8,875 Indirect 118 266 579 7,088 2,497 2,180 9,675 265 22,668 Induced 459 36 203 2,275 1,649 4,412 14,880 289 24,203 Total 576 1,358 781 17,183 4,147 6,592 24,555 554 55,747 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Ohio Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 938 0 7,110 0 0 0 0 8,048 Indirect 115 263 582 7,154 2,424 2,031 9,192 258 22,019 Induced 450 37 197 2,355 1,657 4,214 14,280 282 23,471 Total 565 1,238 779 16,619 4,080 6,245 23,473 540 53,538 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,115 0 8,473 0 0 0 0 9,588 Indirect 123 282 631 8,030 2,758 2,304 10,119 284 24,532 Induced 469 39 219 2,596 1,856 4,672 15,652 309 25,813 Total 592 1,437 850 19,099 4,615 6,976 25,771 593 59,933 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,700 0 12,678 0 0 0 0 14,378 Indirect 154 364 831 10,516 3,734 3,187 13,511 371 32,668 Induced 587 49 294 3,383 2,445 6,305 20,834 405 34,303 Total 741 2,114 1,125 26,577 6,180 9,492 34,345 776 81,349 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-69 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Oklahoma Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-70 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 3,482 2,918 1,657 295 0 284 0 8,636 Indirect 48 522 587 946 789 870 4,766 144 8,672 Induced 308 82 98 310 512 2,294 7,226 177 11,007 Total 356 4,086 3,603 2,912 1,597 3,165 12,277 321 28,315 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 5,298 2,646 2,893 944 0 435 0 12,217 Indirect 69 742 874 1,425 1,258 1,331 7,359 221 13,278 Induced 445 117 144 465 748 3,394 10,693 262 16,267 Total 515 6,157 3,665 4,783 2,950 4,724 18,487 482 41,763 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 6,425 2,993 3,589 1,131 0 461 0 14,598 Indirect 87 852 980 1,715 1,538 1,613 8,883 271 15,939 Induced 540 138 170 559 898 4,037 12,735 313 19,389 Total 626 7,414 4,142 5,863 3,566 5,649 22,080 585 49,925 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Oklahoma Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 6,802 3,346 3,444 1,174 0 478 0 15,245 Indirect 87 871 1,042 1,706 1,554 1,629 9,124 276 16,289 Induced 551 137 175 577 927 4,182 13,224 324 20,097 Total 638 7,811 4,562 5,728 3,655 5,811 22,827 600 51,631 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 7,348 3,707 3,649 1,337 0 539 0 16,580 Indirect 94 934 1,095 1,866 1,675 1,757 9,888 298 17,607 Induced 591 148 187 624 996 4,505 14,266 349 21,666 Total 685 8,431 4,989 6,139 4,007 6,262 24,693 647 55,853 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 9,137 4,665 4,368 1,690 0 677 0 20,537 Indirect 119 1,181 1,364 2,332 2,062 2,158 12,266 368 21,851 Induced 746 188 232 784 1,233 5,575 17,686 431 26,874 Total 865 10,505 6,261 7,484 4,985 7,733 30,629 798 69,261 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-71 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Oregon Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-72 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 438 232 0 0 0 0 670 Indirect 97 22 104 738 228 212 1,239 50 2,690 Induced 248 2 37 318 189 559 1,988 55 3,396 Total 344 24 580 1,288 417 771 3,227 105 6,756 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 185 0 0 0 0 185 Indirect 133 32 164 1,052 316 267 1,670 70 3,704 Induced 366 3 53 469 256 722 2,688 70 4,627 Total 500 35 217 1,706 572 989 4,358 140 8,516 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 216 0 0 0 0 216 Indirect 160 50 204 1,318 394 332 2,124 88 4,670 Induced 453 4 67 568 316 884 3,364 86 5,743 Total 613 55 271 2,102 710 1,216 5,489 174 10,629 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Oregon Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 163 0 0 0 0 163 Indirect 154 60 215 1,268 375 315 2,146 85 4,620 Induced 460 6 67 573 314 885 3,431 86 5,821 Total 614 66 282 2,004 689 1,201 5,577 171 10,604 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 136 0 0 0 0 136 Indirect 160 72 229 1,309 392 329 2,302 89 4,881 Induced 491 7 71 602 332 948 3,704 91 6,246 Total 650 79 300 2,047 724 1,277 6,006 181 11,264 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 142 0 0 0 0 142 Indirect 191 97 293 1,569 495 407 2,909 110 6,071 Induced 620 9 90 746 425 1,193 4,698 114 7,894 Total 812 107 382 2,457 920 1,600 7,607 224 14,107 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-73 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Pennsylvania Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-74 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4,991 4,718 2,231 1,122 0 531 0 13,594 Indirect 90 414 1,086 3,639 1,747 1,584 9,561 221 18,342 Induced 366 51 233 1,412 1,378 4,845 16,337 326 24,948 Total 456 5,456 6,038 7,282 4,247 6,429 26,429 547 56,884 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 16,603 4,846 2,280 1,505 0 774 0 26,007 Indirect 141 1,007 3,428 5,434 2,927 2,787 18,464 407 34,594 Induced 651 106 456 2,381 2,640 10,214 33,305 669 50,423 Total 792 17,715 8,730 10,095 7,072 13,000 52,543 1,076 111,024 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 26,424 7,367 3,956 2,413 0 1,098 0 41,258 Indirect 193 1,326 4,973 7,131 4,278 4,227 27,544 603 50,276 Induced 894 134 658 3,139 3,768 15,110 48,630 989 73,321 Total 1,088 27,885 12,998 14,225 10,460 19,336 77,272 1,592 164,856 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Pennsylvania Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 27,691 6,725 3,610 2,140 0 973 0 41,140 Indirect 189 1,359 5,492 6,809 4,217 4,181 27,612 604 50,463 Induced 923 135 672 3,182 3,884 15,572 50,056 1,021 75,445 Total 1,112 29,186 12,889 13,601 10,241 19,753 78,641 1,626 167,048 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 31,475 8,155 4,304 2,640 0 1,187 0 47,761 Indirect 214 1,479 6,048 7,420 4,770 4,807 31,366 687 56,790 Induced 1,027 146 751 3,473 4,333 17,566 56,219 1,155 84,671 Total 1,241 33,100 14,954 15,198 11,742 22,374 88,773 1,842 189,222 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 45,607 12,801 6,349 4,131 0 1,846 0 70,734 Indirect 289 1,990 8,514 9,653 6,736 6,906 44,750 969 79,807 Induced 1,404 193 1,050 4,655 6,081 25,046 79,449 1,639 119,518 Total 1,693 47,789 22,365 20,658 16,948 31,952 126,045 2,608 270,058 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-75 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Rhode Island Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-76 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 1 23 177 36 33 288 8 570 Induced 18 0 9 66 33 113 549 9 798 Total 22 2 33 243 69 145 837 17 1,368 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 5 2 28 257 52 49 415 12 820 Induced 25 0 13 97 47 169 784 13 1,148 Total 29 2 41 354 99 218 1,200 25 1,968 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 6 2 30 310 62 59 494 14 977 Induced 29 0 16 117 56 197 932 16 1,364 Total 35 3 46 427 118 256 1,426 30 2,341 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Rhode Island Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 6 3 29 288 59 58 488 14 944 Induced 27 0 16 116 55 193 929 16 1,351 Total 33 3 44 404 114 251 1,417 29 2,295 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 6 3 29 290 60 61 511 15 976 Induced 28 0 16 119 56 200 979 16 1,416 Total 34 3 45 410 116 262 1,490 31 2,391 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 8 4 35 340 72 74 623 18 1,173 Induced 34 1 20 145 67 243 1,201 20 1,731 Total 42 4 55 485 139 317 1,824 37 2,904 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-77 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES South Carolina Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-78 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 59 2 0 0 0 0 61 Indirect 43 14 110 974 188 137 1,034 46 2,545 Induced 103 1 29 431 166 505 1,713 52 3,001 Total 147 15 198 1,407 354 642 2,747 97 5,607 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 3 0 0 0 0 3 Indirect 62 23 170 1,444 284 208 1,554 67 3,813 Induced 143 2 42 644 245 741 2,520 74 4,411 Total 205 26 212 2,091 530 950 4,073 140 8,227 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 89 4 0 0 0 0 93 Indirect 73 30 215 1,789 356 264 1,982 85 4,794 Induced 174 3 53 789 302 906 3,168 92 5,487 Total 246 33 357 2,582 658 1,171 5,150 177 10,373 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES South Carolina Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 18 4 0 0 0 0 22 Indirect 68 30 226 1,834 350 258 2,020 85 4,871 Induced 175 3 52 823 301 900 3,225 93 5,573 Total 244 34 296 2,660 650 1,158 5,245 179 10,466 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 26 5 0 0 0 0 31 Indirect 72 35 241 2,042 374 278 2,221 93 5,357 Induced 189 4 56 906 319 969 3,522 101 6,066 Total 261 39 323 2,953 693 1,247 5,743 194 11,453 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 6 0 0 0 0 6 Indirect 86 46 304 2,583 461 341 2,805 115 6,742 Induced 238 5 71 1,157 394 1,202 4,430 125 7,621 Total 324 51 375 3,745 854 1,543 7,235 240 14,368 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-79 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES South Dakota Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-80 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 23 8 26 117 48 37 181 11 452 Induced 99 1 8 66 42 119 378 12 725 Total 122 9 34 183 90 157 559 22 1,176 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 39 12 36 168 72 56 277 17 677 Induced 160 1 11 103 61 179 560 18 1,093 Total 199 13 48 271 133 235 837 35 1,770 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 51 13 38 205 90 68 342 21 828 Induced 200 1 13 129 74 217 685 22 1,341 Total 251 15 51 334 164 286 1,027 43 2,169 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES South Dakota Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 51 13 36 194 92 68 352 21 829 Induced 206 1 13 130 77 220 703 22 1,372 Total 258 14 49 324 169 288 1,055 43 2,201 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 58 14 36 204 101 73 385 23 893 Induced 224 2 13 138 83 234 760 23 1,478 Total 282 16 49 342 184 308 1,145 46 2,372 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 74 18 43 244 126 89 484 28 1,107 Induced 286 2 16 169 104 290 954 29 1,852 Total 361 20 59 414 230 380 1,439 57 2,959 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-81 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Tennessee Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-82 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 142 0 0 0 0 142 Indirect 39 38 151 1,101 522 249 1,500 60 3,660 Induced 220 5 41 605 491 756 2,533 66 4,717 Total 258 43 192 1,848 1,013 1,005 4,033 126 8,519 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 62 0 0 0 0 62 Indirect 58 57 233 1,638 780 346 2,205 87 5,404 Induced 326 7 62 917 725 1,059 3,665 95 6,856 Total 385 64 295 2,616 1,505 1,405 5,870 182 12,323 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 147 0 0 0 0 147 Indirect 75 73 286 2,050 954 436 2,776 111 6,761 Induced 409 9 80 1,158 870 1,304 4,556 118 8,504 Total 485 82 366 3,355 1,824 1,741 7,333 228 15,412 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Tennessee Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 91 0 0 0 0 91 Indirect 77 73 304 2,105 945 432 2,840 111 6,887 Induced 423 9 82 1,224 874 1,309 4,637 119 8,678 Total 500 82 386 3,420 1,818 1,741 7,477 230 15,656 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 98 0 0 0 0 98 Indirect 87 77 324 2,370 1,012 467 3,092 120 7,549 Induced 462 9 90 1,356 929 1,413 5,024 128 9,412 Total 549 87 414 3,824 1,942 1,880 8,116 248 17,059 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 89 0 0 0 0 89 Indirect 113 95 417 3,014 1,265 576 3,893 150 9,522 Induced 592 11 117 1,742 1,162 1,770 6,321 161 11,876 Total 705 106 533 4,845 2,427 2,346 10,214 311 21,487 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-83 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Texas Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-84 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 27,081 22,368 19,477 2,934 0 1,883 0 73,744 Indirect 370 3,359 5,724 10,512 8,996 9,301 49,345 953 88,561 Induced 2,285 533 1,149 4,344 6,708 27,870 81,641 1,388 125,918 Total 2,655 30,972 29,241 34,334 18,638 37,171 132,869 2,341 288,222 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 40,817 17,440 27,925 5,025 0 2,632 0 93,838 Indirect 502 4,723 7,664 14,424 12,860 12,552 67,913 1,355 121,994 Induced 3,126 749 1,552 5,924 9,100 37,345 109,818 1,870 169,486 Total 3,628 46,289 26,657 48,273 26,986 49,897 180,363 3,225 385,318 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 54,613 23,199 37,529 7,210 0 3,332 0 125,882 Indirect 646 5,624 8,973 18,689 17,016 16,570 89,005 1,786 158,308 Induced 3,919 919 1,975 7,457 11,601 47,602 139,884 2,398 215,755 Total 4,566 61,155 34,147 63,675 35,826 64,172 232,221 4,184 499,946 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Texas Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 55,749 24,450 37,220 7,169 0 3,310 0 127,899 Indirect 644 5,851 9,570 18,582 17,251 16,761 91,004 1,831 161,495 Induced 4,017 934 2,037 7,622 11,958 48,975 144,051 2,487 222,082 Total 4,661 62,535 36,057 63,424 36,378 65,736 238,366 4,318 511,476 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 60,333 27,805 40,758 8,172 0 3,734 0 140,803 Indirect 702 6,193 10,076 20,303 18,886 18,349 99,463 2,017 175,989 Induced 4,325 999 2,218 8,203 12,959 53,054 156,156 2,711 240,624 Total 5,027 67,525 40,099 69,263 40,018 71,403 259,353 4,728 557,416 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 73,098 33,384 49,905 9,978 0 4,530 0 170,896 Indirect 863 7,675 12,482 25,038 23,195 22,438 122,239 2,504 216,434 Induced 5,347 1,238 2,741 10,117 15,946 65,032 191,648 3,342 295,411 Total 6,210 82,011 48,607 85,060 49,119 87,470 318,417 5,846 682,740 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-85 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Utah Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-86 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 2,389 4,611 1,689 1,285 0 430 0 10,404 Indirect 18 162 433 806 852 863 5,782 76 8,993 Induced 111 15 106 422 580 2,255 7,572 105 11,165 Total 129 2,566 5,150 2,917 2,717 3,118 13,784 181 30,561 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 3,708 3,202 2,073 1,686 0 563 0 11,232 Indirect 27 229 562 1,017 1,095 1,002 7,497 104 11,532 Induced 155 21 137 574 730 2,774 9,304 134 13,829 Total 182 3,957 3,900 3,664 3,511 3,776 17,364 238 36,593 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4,525 3,292 2,278 1,835 0 542 0 12,472 Indirect 33 284 630 1,203 1,252 1,130 8,626 124 13,281 Induced 184 25 155 675 839 3,158 10,610 156 15,803 Total 217 4,834 4,077 4,156 3,925 4,287 19,778 280 41,556 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Utah Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4,768 3,581 2,262 1,886 0 557 0 13,054 Indirect 34 290 680 1,180 1,296 1,174 9,025 130 13,810 Induced 193 26 160 691 875 3,324 11,179 165 16,613 Total 227 5,084 4,421 4,134 4,057 4,498 20,761 295 43,477 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4,923 3,639 2,331 1,949 0 570 0 13,412 Indirect 38 314 712 1,233 1,354 1,229 9,433 139 14,453 Induced 207 28 166 727 918 3,490 11,736 175 17,447 Total 246 5,265 4,517 4,292 4,221 4,719 21,738 314 45,312 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 5,257 3,966 2,684 2,118 0 615 0 14,640 Indirect 45 381 791 1,440 1,540 1,385 10,645 165 16,392 Induced 243 33 187 863 1,052 3,946 13,279 204 19,807 Total 289 5,671 4,943 4,988 4,709 5,331 24,539 369 50,839 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-87 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Vermont Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-88 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 10 6 18 91 33 23 142 7 330 Induced 32 1 7 55 31 93 291 8 518 Total 42 7 25 147 64 115 433 15 848 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 15 8 25 131 49 34 218 11 491 Induced 47 1 10 86 46 137 431 12 770 Total 63 8 35 217 96 171 649 22 1,261 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 20 8 30 158 60 41 267 13 597 Induced 58 1 11 109 56 166 517 14 933 Total 77 9 42 267 116 207 784 28 1,530 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Vermont Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 20 7 33 142 58 41 265 13 579 Induced 59 1 11 108 55 167 517 15 932 Total 79 8 44 250 113 207 782 28 1,510 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 21 7 35 142 60 43 278 14 600 Induced 62 1 12 111 56 177 545 16 980 Total 84 8 47 253 116 220 823 30 1,581 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 26 9 44 165 72 52 338 17 724 Induced 77 1 15 135 66 218 666 19 1,198 Total 104 10 59 300 138 270 1,004 37 1,922 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-89 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Virginia Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-90 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 502 157 209 39 0 16 0 923 Indirect 46 127 361 788 477 308 3,285 106 5,498 Induced 177 13 92 470 400 1,144 4,327 118 6,740 Total 223 643 611 1,467 916 1,452 7,627 224 13,162 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 458 67 217 25 0 10 0 777 Indirect 65 165 457 1,085 629 413 4,651 148 7,612 Induced 264 18 124 684 529 1,563 6,020 163 9,364 Total 328 641 648 1,985 1,183 1,976 10,681 311 17,753 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 407 71 322 27 0 10 0 838 Indirect 81 198 513 1,355 773 501 5,841 186 9,448 Induced 321 22 150 859 631 1,922 7,399 197 11,501 Total 402 628 734 2,536 1,432 2,423 13,250 382 21,787 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Virginia Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 362 76 295 28 0 10 0 772 Indirect 81 194 516 1,323 747 489 5,970 185 9,506 Induced 324 23 148 872 622 1,963 7,533 199 11,685 Total 405 579 741 2,490 1,397 2,452 13,514 385 21,963 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 341 77 357 29 0 10 0 815 Indirect 92 198 542 1,389 801 540 6,625 202 10,389 Induced 354 25 159 914 657 2,153 8,275 213 12,750 Total 446 564 778 2,661 1,487 2,693 14,910 415 23,953 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 387 88 549 33 0 12 0 1,069 Indirect 111 238 682 1,651 1,044 702 8,680 260 13,368 Induced 418 30 199 1,098 843 2,747 10,689 270 16,296 Total 529 655 970 3,299 1,920 3,449 19,381 530 30,732 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-91 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Washington Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-92 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 54 14 101 303 147 119 823 35 1,597 Induced 179 1 34 181 140 378 1,354 40 2,307 Total 233 15 135 484 287 497 2,177 76 3,904 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 81 14 152 374 223 180 1,283 53 2,360 Induced 282 1 51 242 213 569 2,021 59 3,438 Total 363 16 203 616 436 749 3,304 112 5,797 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 104 20 176 456 277 221 1,597 67 2,919 Induced 349 2 61 296 266 686 2,472 73 4,205 Total 454 22 237 752 543 907 4,069 140 7,123 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Washington Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 105 23 183 501 281 218 1,606 67 2,984 Induced 353 2 60 320 277 687 2,492 74 4,265 Total 458 24 244 820 557 905 4,098 142 7,249 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 112 26 191 589 303 234 1,708 72 3,236 Induced 373 2 64 359 299 731 2,648 80 4,556 Total 485 29 254 948 602 966 4,356 152 7,793 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 137 37 235 792 382 289 2,127 90 4,088 Induced 462 3 78 473 379 905 3,290 99 5,689 Total 599 40 313 1,264 761 1,194 5,417 189 9,777 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-93 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES West Virginia Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-94 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 3,905 1,673 230 748 0 315 0 6,871 Indirect 19 448 492 319 426 414 2,349 55 4,522 Induced 82 58 51 120 251 1,258 3,591 83 5,495 Total 102 4,411 2,216 670 1,425 1,672 6,255 138 16,888 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 9,372 2,014 260 843 0 369 0 12,857 Indirect 26 733 1,236 465 691 750 4,124 90 8,115 Induced 127 84 94 190 456 2,446 6,855 155 10,408 Total 153 10,190 3,345 915 1,990 3,196 11,347 245 31,380 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 13,466 2,891 386 1,281 0 496 0 18,520 Indirect 33 965 1,662 587 972 1,069 5,919 127 11,335 Induced 164 108 130 241 617 3,399 9,496 213 14,368 Total 197 14,539 4,684 1,214 2,870 4,468 15,911 340 44,223 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES West Virginia Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 14,025 2,764 354 1,157 0 448 0 18,748 Indirect 32 979 1,806 597 962 1,076 5,919 127 11,498 Induced 170 110 134 254 628 3,507 9,804 221 14,828 Total 203 15,114 4,704 1,205 2,747 4,583 16,171 348 45,074 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 15,523 3,274 429 1,394 0 534 0 21,154 Indirect 36 1,062 1,960 679 1,081 1,220 6,701 144 12,883 Induced 189 120 149 282 687 3,904 10,915 246 16,492 Total 225 16,705 5,383 1,389 3,162 5,125 18,150 390 50,529 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 21,843 4,974 659 2,111 0 803 0 30,390 Indirect 48 1,369 2,731 899 1,534 1,745 9,582 201 18,110 Induced 253 153 208 371 951 5,505 15,337 343 23,121 Total 301 23,365 7,913 1,929 4,597 7,251 25,722 545 71,620 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-95 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Wisconsin Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-96 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 85 0 52 0 0 0 0 137 Indirect 69 23 135 2,077 373 244 1,479 58 4,457 Induced 284 2 39 831 333 782 2,677 65 5,013 Total 352 110 175 2,960 706 1,026 4,156 123 9,608 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 200 0 62 0 0 0 0 263 Indirect 104 31 195 3,065 537 366 2,214 86 6,599 Induced 421 3 58 1,243 475 1,177 3,952 95 7,424 Total 525 234 253 4,370 1,012 1,544 6,166 182 14,285 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 226 0 95 0 0 0 0 321 Indirect 134 35 232 3,803 678 456 2,805 107 8,252 Induced 524 3 71 1,534 594 1,433 4,871 116 9,146 Total 658 265 303 5,432 1,272 1,889 7,676 224 17,719 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Wisconsin Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 248 0 84 0 0 0 0 333 Indirect 136 36 238 3,786 708 458 2,945 107 8,413 Induced 548 3 70 1,560 635 1,464 5,014 117 9,411 Total 684 287 308 5,430 1,342 1,922 7,959 224 18,156 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 280 0 102 0 0 0 0 382 Indirect 152 39 248 4,120 778 501 3,218 116 9,171 Induced 598 4 75 1,665 694 1,583 5,404 127 10,150 Total 750 322 322 5,887 1,472 2,085 8,622 243 19,703 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 348 0 158 0 0 0 0 506 Indirect 192 49 309 5,159 983 633 4,115 146 11,585 Induced 754 5 93 2,084 879 1,996 6,810 158 12,779 Total 946 402 402 7,402 1,861 2,628 10,925 304 24,871 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-97 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Wyoming Employment Contribution by State and Industry: Unconventional Gas* (Number of workers) B-98 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 10,134 2,674 1,025 636 0 284 0 14,753 Indirect 16 401 2,235 100 728 867 4,188 112 8,647 Induced 67 40 130 56 536 3,033 7,315 210 11,386 Total 83 10,574 5,039 1,181 1,900 3,900 11,787 322 34,787 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 12,836 3,283 767 1,388 0 643 0 18,917 Indirect 19 405 2,177 105 858 964 5,016 130 9,673 Induced 102 56 195 85 814 4,569 11,036 316 17,173 Total 121 13,297 5,655 957 3,060 5,533 16,695 446 45,763 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 14,317 3,404 808 1,538 0 631 0 20,698 Indirect 21 471 2,316 118 951 1,057 5,549 145 10,630 Induced 118 68 213 97 894 4,960 11,980 346 18,675 Total 139 14,856 5,933 1,023 3,383 6,017 18,159 491 50,002 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Wyoming Employment Contribution by State and Industry: Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 16,142 4,216 805 1,800 0 737 0 23,700 Indirect 22 503 2,599 126 1,064 1,203 6,330 162 12,010 Induced 126 70 240 107 1,007 5,620 13,568 391 21,129 Total 148 16,715 7,055 1,038 3,871 6,823 20,636 554 56,840 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 17,537 4,853 832 2,107 0 854 0 26,183 Indirect 25 541 2,762 139 1,166 1,329 7,011 178 13,152 Induced 137 76 261 118 1,095 6,115 14,767 426 22,994 Total 161 18,154 7,877 1,089 4,368 7,444 22,632 605 62,329 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 22,179 6,107 957 2,644 0 1,065 0 32,953 Indirect 31 686 3,546 174 1,465 1,677 8,860 224 16,664 Induced 174 95 332 150 1,392 7,760 18,733 540 29,176 Total 205 22,961 9,985 1,280 5,502 9,438 28,658 764 78,792 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-99 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Value Added Contribution by State and Industry Alabama Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-100 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 243 29 4 0 0 0 0 276 Indirect 4 19 15 115 35 18 130 5 341 Induced 8 3 3 59 33 48 173 7 335 Total 12 266 47 178 68 66 303 12 952 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 157 82 4 0 0 0 0 243 Indirect 5 25 15 171 49 28 176 7 477 Induced 11 5 4 86 47 66 234 10 463 Total 16 188 100 261 97 94 410 17 1,183 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 89 49 5 0 0 0 0 142 Indirect 6 33 14 209 52 28 174 8 525 Induced 13 7 4 104 50 65 235 10 488 Total 19 128 67 317 102 94 409 19 1,155 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Alabama Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 50 24 5 0 0 0 0 79 Indirect 6 34 13 219 50 25 162 8 517 Induced 13 7 4 109 48 60 219 10 470 Total 19 91 41 333 98 86 380 18 1,066 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 33 46 5 0 0 0 0 84 Indirect 6 38 13 254 55 30 182 9 587 Induced 13 8 4 122 53 67 245 11 523 Total 20 78 64 381 108 96 427 20 1,193 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 37 14 7 0 0 0 0 58 Indirect 8 48 17 330 67 32 210 11 722 Induced 16 10 5 158 65 76 282 13 624 Total 24 96 35 495 132 108 492 24 1,405 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-101 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Arizona Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-102 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 25 11 48 23 15 117 4 246 Induced 5 3 3 28 26 39 174 6 283 Total 7 28 14 76 50 54 291 10 529 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 35 17 67 36 23 177 6 364 Induced 8 4 5 39 41 58 263 8 426 Total 11 39 22 107 78 81 440 14 791 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 40 22 80 47 30 229 8 459 Induced 10 5 7 47 53 72 336 10 539 Total 13 45 28 127 100 102 565 19 998 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Arizona Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 38 25 75 50 32 246 9 476 Induced 10 5 7 46 57 74 358 11 567 Total 12 42 32 121 106 106 603 20 1,043 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 40 27 78 56 35 279 10 529 Induced 11 5 8 48 63 83 405 13 635 Total 14 45 35 126 119 119 683 23 1,164 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 4 51 34 96 74 45 368 13 684 Induced 13 6 10 59 84 107 530 17 826 Total 17 57 44 155 158 151 898 30 1,509 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-103 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Arkansas Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-104 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 2,498 46 107 74 0 20 0 2,745 Indirect 5 48 83 104 193 85 476 12 1,005 Induced 14 4 8 60 126 200 732 18 1,161 Total 19 2,549 137 271 393 284 1,229 29 4,910 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 3,725 65 195 63 0 21 0 4,068 Indirect 7 70 123 160 282 136 713 18 1,508 Induced 21 5 12 86 183 290 1,065 25 1,688 Total 28 3,800 200 441 527 427 1,799 43 7,264 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4,235 67 234 68 0 20 0 4,624 Indirect 8 80 139 200 335 166 833 21 1,781 Induced 25 6 14 102 211 337 1,234 30 1,959 Total 33 4,321 220 536 614 502 2,087 51 8,364 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Arkansas Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4,454 72 234 70 0 20 0 4,850 Indirect 8 83 147 203 344 171 875 22 1,853 Induced 26 6 15 106 217 352 1,292 31 2,045 Total 33 4,543 234 543 630 523 2,188 54 8,749 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4,485 73 249 71 0 21 0 4,900 Indirect 8 84 148 217 357 179 896 23 1,913 Induced 27 6 15 112 221 361 1,327 32 2,102 Total 35 4,576 236 578 649 540 2,244 56 8,914 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 5,281 83 302 80 0 24 0 5,769 Indirect 10 102 173 261 429 213 1,060 28 2,276 Induced 33 8 18 136 262 428 1,571 39 2,495 Total 42 5,390 274 699 771 641 2,655 67 10,540 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-105 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES California Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-106 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 59 0 446 0 0 0 0 505 Indirect 7 25 20 177 82 76 416 11 815 Induced 26 6 8 119 69 110 518 15 871 Total 34 90 28 742 150 187 935 26 2,192 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 97 45 609 0 0 0 0 751 Indirect 10 38 29 247 121 110 608 17 1,181 Induced 37 9 13 173 102 160 750 21 1,265 Total 48 144 87 1,029 223 270 1,359 38 3,197 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 102 0 720 0 0 0 0 823 Indirect 13 45 36 291 143 131 718 21 1,397 Induced 45 11 16 205 122 188 877 26 1,488 Total 58 158 52 1,215 265 319 1,595 46 3,708 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES California Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 98 0 687 0 0 0 0 785 Indirect 12 46 37 270 142 129 722 21 1,380 Induced 46 11 16 200 124 187 874 26 1,483 Total 58 154 54 1,156 267 315 1,596 46 3,648 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 96 0 708 0 0 0 0 804 Indirect 13 48 40 277 152 136 762 22 1,451 Induced 49 11 18 208 134 197 923 28 1,567 Total 62 155 58 1,193 286 333 1,685 50 3,822 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 106 0 822 0 0 0 0 928 Indirect 16 60 50 332 186 163 935 27 1,769 Induced 61 14 22 255 166 239 1,129 34 1,920 Total 77 180 72 1,408 353 402 2,064 61 4,617 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-107 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Colorado Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-108 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4,354 230 795 148 0 60 0 5,587 Indirect 3 143 174 139 342 258 1,811 43 2,913 Induced 37 20 28 117 303 613 2,579 60 3,758 Total 41 4,518 432 1,051 794 871 4,450 103 12,258 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 5,286 466 1,540 357 0 129 0 7,777 Indirect 6 205 193 250 565 466 2,861 68 4,613 Induced 58 32 43 180 471 941 3,956 91 5,772 Total 64 5,523 702 1,969 1,393 1,407 6,945 159 18,162 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 5,244 467 1,740 376 0 121 0 7,949 Indirect 7 233 186 284 607 514 3,062 74 4,967 Induced 63 38 46 196 501 997 4,196 98 6,135 Total 70 5,515 699 2,220 1,485 1,511 7,379 172 19,051 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Colorado Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4,573 362 1,631 277 0 89 0 6,932 Indirect 6 233 172 247 529 443 2,669 66 4,365 Induced 57 37 40 175 439 866 3,666 87 5,367 Total 63 4,843 573 2,053 1,245 1,309 6,424 152 16,664 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4,115 298 1,643 229 0 74 0 6,360 Indirect 6 244 160 235 498 415 2,483 63 4,103 Induced 55 39 37 168 412 808 3,432 82 5,033 Total 61 4,398 496 2,046 1,139 1,223 5,989 144 15,496 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4,583 308 1,918 237 0 77 0 7,123 Indirect 7 303 183 268 563 465 2,804 71 4,664 Induced 65 49 42 193 468 910 3,879 93 5,698 Total 72 4,934 533 2,379 1,268 1,375 6,759 164 17,485 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-109 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Connecticut Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-110 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 1 5 65 17 10 97 2 197 Induced 2 0 2 29 19 24 146 3 224 Total 2 2 7 94 35 34 243 5 422 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 2 8 86 23 15 137 3 275 Induced 2 0 2 41 25 35 204 4 313 Total 3 3 10 127 47 50 340 8 587 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 3 9 105 27 18 159 4 326 Induced 3 1 3 50 28 41 236 5 366 Total 3 3 12 155 55 59 395 10 693 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Connecticut Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 3 10 105 26 18 154 4 321 Induced 3 1 3 52 27 41 228 5 359 Total 3 3 13 158 52 59 382 9 679 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 2 10 117 27 19 157 4 338 Induced 3 0 3 58 27 43 232 6 371 Total 3 3 13 175 54 62 389 10 709 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 3 13 150 32 24 187 5 415 Induced 3 1 4 74 33 52 277 7 450 Total 4 3 16 225 65 76 464 12 865 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-111 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Delaware Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-112 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 25 0 0 0 0 25 Indirect 0 0 2 11 7 7 35 1 63 Induced 1 0 1 8 5 9 50 1 74 Total 1 0 3 44 12 16 85 2 163 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 32 0 0 0 0 32 Indirect 0 0 3 16 10 9 50 1 90 Induced 1 0 1 11 7 12 71 2 105 Total 1 0 4 59 17 21 121 3 226 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 54 0 0 0 0 54 Indirect 0 0 4 21 15 15 68 2 126 Induced 1 0 1 13 9 17 97 2 141 Total 1 0 6 88 24 32 165 4 321 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Delaware Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 49 0 0 0 0 49 Indirect 0 0 4 19 15 14 68 2 122 Induced 1 0 1 13 9 17 95 2 139 Total 1 0 6 81 24 31 163 4 310 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 59 0 0 0 0 59 Indirect 0 0 5 21 17 16 75 2 137 Induced 1 0 2 13 11 20 106 2 154 Total 1 0 6 93 28 36 180 4 349 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 90 0 0 0 0 90 Indirect 0 0 6 27 25 25 99 3 186 Induced 2 0 2 16 15 28 140 3 205 Total 2 0 8 134 40 52 240 6 482 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-113 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES District of Columbia Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-114 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 0 0 1 0 29 1 32 Induced 0 0 0 0 1 1 36 1 40 Total 0 0 0 0 2 1 65 2 72 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 0 0 1 1 44 1 48 Induced 0 0 0 0 1 2 54 2 60 Total 0 0 1 0 3 2 98 4 108 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 1 0 2 1 56 2 61 Induced 0 0 0 0 2 2 68 3 75 Total 0 0 1 1 3 3 123 5 135 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES District of Columbia Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 1 0 2 1 56 2 62 Induced 0 0 0 0 2 2 69 3 76 Total 0 0 1 1 4 3 125 5 138 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 1 0 2 1 60 2 66 Induced 0 0 0 0 2 2 74 3 82 Total 0 0 1 1 4 3 134 5 148 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 1 0 3 1 75 3 82 Induced 0 0 1 0 3 3 93 4 104 Total 0 0 2 1 6 4 168 7 186 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-115 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Florida Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-116 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 168 12 0 0 0 0 180 Indirect 4 6 17 55 41 36 247 6 413 Induced 12 1 6 40 49 82 371 9 570 Total 15 7 191 108 90 118 618 15 1,163 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 370 17 0 0 0 0 387 Indirect 6 10 26 92 70 63 419 10 695 Induced 18 1 10 63 83 138 626 14 953 Total 24 11 405 172 153 201 1,045 23 2,034 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 163 23 0 0 0 0 185 Indirect 6 9 31 93 74 59 436 11 720 Induced 19 1 11 68 85 136 631 15 965 Total 26 10 205 183 159 195 1,067 26 1,871 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Florida Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 41 23 0 0 0 0 65 Indirect 6 8 33 81 68 52 428 11 688 Induced 19 1 10 63 80 124 598 15 910 Total 24 9 85 167 148 176 1,026 26 1,662 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 251 26 0 0 0 0 277 Indirect 7 9 37 97 82 71 536 13 853 Induced 22 1 12 71 98 159 760 17 1,140 Total 28 11 300 194 180 231 1,295 31 2,270 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 29 32 0 0 0 0 61 Indirect 7 9 48 101 91 73 608 16 953 Induced 25 1 15 79 107 169 836 20 1,252 Total 32 11 91 212 197 242 1,444 36 2,266 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-117 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Georgia Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-118 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 6 103 0 0 0 0 109 Indirect 4 8 14 101 61 42 235 7 472 Induced 9 1 5 83 68 77 313 10 566 Total 13 8 24 287 129 119 548 17 1,147 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 136 0 0 0 0 136 Indirect 5 9 18 144 91 58 344 11 681 Induced 12 1 6 122 101 108 440 14 804 Total 18 11 25 402 192 166 784 25 1,622 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 9 69 0 0 0 0 77 Indirect 6 11 22 174 105 66 407 13 805 Induced 15 2 8 149 120 124 507 17 941 Total 21 13 39 391 225 190 915 30 1,823 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Georgia Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 3 20 0 0 0 0 23 Indirect 6 11 23 176 101 63 414 13 808 Induced 15 2 8 154 119 121 500 17 935 Total 21 13 34 351 220 184 913 30 1,766 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 4 93 0 0 0 0 97 Indirect 7 12 24 197 117 77 469 15 918 Induced 16 2 9 169 134 141 578 19 1,069 Total 24 14 38 459 251 219 1,047 33 2,084 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 14 0 0 0 0 14 Indirect 9 15 30 241 139 88 564 18 1,105 Induced 20 2 12 209 163 166 685 23 1,280 Total 29 17 42 464 302 254 1,249 41 2,398 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-119 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Idaho Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-120 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 5 3 17 7 4 27 1 66 Induced 6 0 1 13 8 10 37 2 77 Total 8 5 4 29 15 14 64 3 142 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 7 3 26 11 6 41 2 100 Induced 9 1 1 19 12 15 57 2 114 Total 12 8 4 45 23 21 97 4 214 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 5 11 3 31 13 8 50 2 124 Induced 11 1 1 22 14 19 71 3 142 Total 15 12 4 53 27 27 121 5 266 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Idaho Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 5 13 3 30 14 8 53 2 127 Induced 11 1 1 23 14 20 74 3 147 Total 16 14 4 53 28 28 126 6 275 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 5 15 3 31 15 9 58 3 138 Induced 12 1 1 25 16 21 81 3 160 Total 17 16 4 56 30 30 139 6 298 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 7 20 4 36 19 12 73 3 173 Induced 15 2 1 30 20 27 103 4 202 Total 21 21 5 66 39 39 176 8 375 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-121 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Illinois Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-122 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 329 0 66 0 0 0 0 395 Indirect 3 40 20 290 122 68 447 11 1,000 Induced 14 6 9 163 113 149 695 16 1,165 Total 17 375 29 518 235 217 1,142 26 2,560 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 457 0 66 0 0 0 0 523 Indirect 4 54 30 421 174 92 622 15 1,413 Induced 20 8 14 238 162 207 949 21 1,619 Total 25 520 44 724 335 300 1,571 36 3,555 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 646 0 80 0 0 0 0 727 Indirect 6 70 36 498 223 114 774 19 1,741 Induced 24 10 18 289 203 262 1,203 26 2,035 Total 30 726 54 868 427 376 1,977 45 4,502 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Illinois Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 598 0 79 0 0 0 0 677 Indirect 5 66 37 469 217 110 777 19 1,698 Induced 24 9 18 287 202 254 1,183 26 2,003 Total 29 673 54 835 418 364 1,960 45 4,378 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 688 0 84 0 0 0 0 772 Indirect 6 72 38 486 238 118 834 20 1,812 Induced 25 10 19 305 219 277 1,289 28 2,172 Total 31 770 57 875 457 395 2,123 48 4,757 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 982 0 105 0 0 0 0 1,087 Indirect 7 96 47 589 310 148 1,066 26 2,289 Induced 30 12 25 381 282 360 1,676 36 2,802 Total 36 1,091 72 1,075 593 508 2,742 62 6,178 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-123 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Indiana Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-124 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 54 0 0 0 0 54 Indirect 2 10 11 258 50 25 117 5 478 Induced 9 2 4 120 47 49 188 6 424 Total 11 12 15 433 97 74 305 11 957 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 62 0 0 0 0 62 Indirect 3 14 17 361 68 34 163 7 667 Induced 13 3 6 174 64 67 261 9 597 Total 16 16 23 597 132 101 424 15 1,326 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 94 0 0 0 0 94 Indirect 4 16 20 443 84 44 206 8 826 Induced 16 3 7 212 77 84 326 10 735 Total 20 20 27 749 161 128 531 19 1,656 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Indiana Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 86 0 0 0 0 86 Indirect 4 16 20 445 81 43 210 8 827 Induced 16 3 7 222 76 83 328 10 747 Total 20 19 27 754 157 126 538 19 1,660 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 104 0 0 0 0 104 Indirect 4 17 21 488 86 48 229 9 902 Induced 16 3 8 244 80 90 356 11 809 Total 20 20 28 835 167 138 584 20 1,814 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 158 0 0 0 0 158 Indirect 5 21 26 608 110 64 296 11 1,142 Induced 20 4 9 309 101 117 457 14 1,031 Total 25 25 36 1,074 212 181 753 25 2,331 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-125 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Iowa Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-126 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 33 0 3 0 0 0 0 36 Indirect 3 3 6 66 23 12 56 3 171 Induced 14 0 2 43 21 28 101 4 213 Total 17 37 8 112 45 40 156 7 420 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 65 0 9 0 0 0 0 75 Indirect 5 4 10 97 39 19 88 4 266 Induced 23 0 3 64 33 43 153 5 325 Total 28 70 13 170 71 62 241 10 665 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 76 0 12 0 0 0 0 89 Indirect 7 5 12 119 48 23 108 5 328 Induced 28 1 4 76 41 51 186 7 394 Total 35 82 16 208 89 75 294 12 811 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Iowa Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 76 0 15 0 0 0 0 91 Indirect 7 4 13 126 50 23 115 6 343 Induced 30 0 4 79 43 52 192 7 407 Total 37 80 17 219 93 75 308 12 841 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 83 0 17 0 0 0 0 101 Indirect 8 4 14 142 57 25 126 6 381 Induced 33 0 5 86 48 56 209 7 444 Total 40 87 19 245 105 81 335 13 926 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 109 0 21 0 0 0 0 131 Indirect 10 4 18 184 74 32 162 7 491 Induced 43 0 6 111 63 71 265 9 567 Total 53 114 24 316 137 102 427 16 1,189 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-127 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Kansas Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-128 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 44 0 55 0 0 0 0 99 Indirect 2 20 7 43 34 14 75 5 200 Induced 8 4 2 31 21 29 113 4 213 Total 9 68 9 129 55 43 188 10 512 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4 0 101 0 0 0 0 105 Indirect 2 28 8 64 56 22 106 9 295 Induced 12 6 3 48 31 40 156 6 302 Total 15 38 11 213 86 62 262 15 702 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 109 0 0 0 0 110 Indirect 3 31 9 80 64 25 127 10 349 Induced 15 6 3 58 37 47 185 7 360 Total 19 38 12 247 101 73 312 18 819 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Kansas Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 107 0 0 0 0 107 Indirect 3 30 9 86 64 25 129 10 357 Induced 16 6 3 62 38 48 189 7 369 Total 19 36 12 255 102 73 318 18 834 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 111 0 0 0 0 111 Indirect 4 31 9 101 69 27 141 11 392 Induced 17 6 3 69 41 51 205 8 400 Total 21 37 12 282 109 77 346 19 904 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 130 0 0 0 0 130 Indirect 5 37 11 135 85 32 180 13 498 Induced 22 8 4 91 52 62 259 10 506 Total 27 45 15 356 137 94 438 23 1,135 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-129 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Kentucky Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-130 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 384 14 26 21 0 6 0 451 Indirect 2 55 16 101 41 25 130 6 376 Induced 11 10 3 65 39 57 214 8 407 Total 13 449 33 192 101 82 351 13 1,234 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 459 14 29 13 0 5 0 519 Indirect 3 77 21 149 54 32 169 8 513 Induced 15 14 4 95 53 73 275 10 540 Total 19 549 39 273 120 105 449 18 1,572 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 420 15 50 14 0 4 0 503 Indirect 5 82 21 190 69 40 196 10 613 Induced 20 15 5 115 65 82 312 12 625 Total 25 517 41 356 147 123 512 21 1,741 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Kentucky Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 378 16 44 14 0 4 0 457 Indirect 5 75 21 200 71 39 191 10 609 Induced 21 14 5 120 68 79 304 12 622 Total 25 466 41 365 152 118 499 21 1,689 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 353 16 53 14 0 5 0 441 Indirect 5 75 21 229 79 42 197 11 659 Induced 23 14 5 132 74 82 316 13 659 Total 28 442 42 414 167 124 518 23 1,759 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 405 18 80 16 0 5 0 525 Indirect 7 90 26 296 101 55 243 14 831 Induced 29 17 6 166 94 101 389 16 818 Total 36 511 50 543 211 156 637 29 2,174 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-131 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Louisiana Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-132 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4,235 811 344 187 0 87 0 5,664 Indirect 9 213 145 274 315 232 1,291 17 2,497 Induced 22 33 23 99 284 514 1,851 34 2,859 Total 31 4,481 979 717 785 746 3,229 51 11,020 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 9,366 835 566 201 0 71 0 11,039 Indirect 12 390 328 419 529 356 2,089 27 4,151 Induced 36 52 38 163 477 868 3,125 56 4,815 Total 47 9,808 1,202 1,148 1,207 1,224 5,286 83 20,005 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 12,841 530 439 228 0 73 0 14,111 Indirect 12 495 443 449 627 382 2,456 33 4,897 Induced 42 62 45 194 566 1,037 3,727 67 5,741 Total 54 13,399 1,019 1,082 1,421 1,419 6,255 100 24,749 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Louisiana Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 15,456 520 394 234 0 74 0 16,678 Indirect 12 568 536 470 705 418 2,812 37 5,559 Induced 48 68 52 215 647 1,195 4,299 77 6,599 Total 60 16,093 1,108 1,079 1,585 1,613 7,185 114 28,837 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 16,252 438 424 239 0 76 0 17,429 Indirect 13 599 564 495 735 433 2,916 39 5,792 Induced 50 72 54 227 672 1,244 4,480 80 6,878 Total 62 16,922 1,056 1,146 1,646 1,677 7,472 119 30,100 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 20,716 447 409 310 0 99 0 21,981 Indirect 15 758 716 601 911 525 3,634 48 7,208 Induced 62 91 67 284 838 1,549 5,578 100 8,569 Total 77 21,565 1,230 1,295 2,059 2,074 9,311 148 37,759 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-133 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Maine Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-134 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 0 2 15 5 3 23 1 52 Induced 3 0 1 13 6 10 38 1 72 Total 5 0 3 28 11 13 61 2 124 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 0 3 21 7 5 33 2 74 Induced 5 0 1 18 8 14 55 2 103 Total 7 0 4 39 15 19 88 3 177 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 1 4 26 8 6 40 2 90 Induced 6 0 1 22 9 17 66 2 123 Total 9 1 5 48 17 23 106 4 213 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Maine Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 1 4 26 8 6 40 2 90 Induced 5 0 1 23 8 17 67 2 124 Total 9 1 6 49 16 23 107 4 214 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 4 1 5 28 8 6 43 2 96 Induced 6 0 1 25 8 18 71 2 132 Total 9 1 6 53 17 24 114 4 228 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 4 1 6 35 10 7 53 2 119 Induced 7 0 2 31 10 22 89 3 163 Total 12 2 8 65 20 29 141 5 282 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-135 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Maryland Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-136 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 3 15 41 26 14 151 5 255 Induced 3 0 5 28 30 36 192 7 300 Total 3 3 20 69 55 49 343 12 555 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 4 21 61 38 20 227 8 379 Induced 4 1 8 40 42 51 280 10 434 Total 5 5 28 101 79 70 506 18 814 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 6 26 74 46 24 277 10 464 Induced 5 1 9 48 50 61 341 12 527 Total 7 7 35 122 96 85 618 22 992 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Maryland Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 6 28 68 46 24 267 10 451 Induced 6 1 10 47 50 62 338 13 526 Total 7 7 38 115 96 86 606 23 977 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 7 31 68 51 25 277 11 471 Induced 6 1 10 48 53 67 359 14 558 Total 8 8 41 116 104 92 636 24 1,030 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 10 40 81 66 32 339 14 583 Induced 8 1 13 59 68 84 447 17 699 Total 10 11 53 140 134 116 786 31 1,281 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-137 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Massachusetts Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-138 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 13 0 0 0 0 13 Indirect 0 1 5 45 13 11 112 2 190 Induced 2 0 2 31 14 24 144 3 220 Total 2 1 7 88 27 35 256 5 423 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 18 0 0 0 0 18 Indirect 1 1 8 65 18 16 166 3 279 Induced 2 0 3 45 20 35 206 4 316 Total 3 1 11 129 38 51 372 8 613 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 32 0 0 0 0 32 Indirect 1 1 9 81 22 21 203 4 343 Induced 3 0 4 56 24 42 249 5 383 Total 4 1 13 169 46 63 452 10 758 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Massachusetts Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 29 0 0 0 0 29 Indirect 1 1 9 74 21 20 203 4 334 Induced 3 0 4 55 23 41 245 5 377 Total 4 1 13 159 44 61 448 10 740 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 36 0 0 0 0 36 Indirect 1 1 10 76 22 21 214 4 350 Induced 3 0 4 57 24 43 260 6 397 Total 4 2 14 169 46 65 474 10 783 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 56 0 0 0 0 56 Indirect 1 2 12 91 27 27 267 5 433 Induced 4 0 5 71 29 54 323 7 492 Total 5 2 17 217 55 81 590 13 981 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-139 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Michigan Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-140 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 364 0 495 0 0 0 0 859 Indirect 3 34 27 246 141 58 430 9 949 Induced 15 4 8 134 109 166 708 14 1,159 Total 18 401 36 875 250 225 1,138 23 2,966 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 266 0 711 0 0 0 0 977 Indirect 5 45 31 387 187 79 555 12 1,302 Induced 21 5 11 195 145 214 905 19 1,514 Total 26 317 43 1,293 331 293 1,460 31 3,794 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 170 0 946 0 0 0 0 1,116 Indirect 7 56 32 490 236 98 659 15 1,593 Induced 25 6 14 233 176 257 1,084 23 1,818 Total 31 231 46 1,669 412 356 1,743 39 4,527 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Michigan Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 108 0 888 0 0 0 0 996 Indirect 6 54 31 506 223 94 639 15 1,568 Induced 24 6 13 236 169 245 1,027 22 1,742 Total 30 167 44 1,629 392 338 1,666 37 4,306 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 77 0 1,002 0 0 0 0 1,079 Indirect 7 57 32 562 249 103 691 16 1,717 Induced 25 6 14 253 184 266 1,109 24 1,883 Total 32 140 46 1,817 433 370 1,800 40 4,679 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 88 0 1,353 0 0 0 0 1,441 Indirect 9 72 40 708 335 135 903 21 2,222 Induced 32 8 18 318 241 347 1,438 31 2,433 Total 41 168 58 2,378 576 482 2,342 51 6,096 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-141 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Minnesota Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-142 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 45 0 0 0 0 0 0 45 Indirect 3 21 8 108 34 20 157 5 355 Induced 12 1 3 70 33 47 222 6 396 Total 15 67 11 178 68 67 379 11 796 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 112 0 0 0 0 0 0 112 Indirect 4 30 11 160 57 32 239 7 541 Induced 18 1 5 111 51 76 348 9 619 Total 23 144 16 271 108 107 587 17 1,272 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 119 0 0 0 0 0 0 119 Indirect 6 36 13 197 68 38 286 9 653 Induced 22 2 6 135 60 89 412 11 736 Total 27 156 19 332 128 127 697 20 1,507 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Minnesota Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 101 0 0 0 0 0 0 101 Indirect 6 33 14 189 69 38 286 9 644 Induced 23 2 6 136 61 87 409 11 734 Total 29 136 19 325 130 125 695 20 1,480 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 95 0 0 0 0 0 0 95 Indirect 6 34 15 202 75 41 303 9 686 Induced 24 2 6 145 65 92 433 12 780 Total 31 130 21 347 140 133 737 21 1,561 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 107 0 0 0 0 0 0 107 Indirect 8 41 19 252 94 52 376 12 856 Induced 31 2 7 183 82 115 539 15 974 Total 39 151 27 435 176 168 915 27 1,937 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-143 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Mississippi Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-144 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 4 0 0 0 0 0 4 Indirect 3 10 4 42 19 6 36 3 122 Induced 7 2 1 31 22 16 55 3 138 Total 10 12 9 73 41 22 91 6 264 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 119 0 0 0 0 0 119 Indirect 5 16 6 68 40 21 97 4 258 Induced 11 3 2 48 43 41 143 6 298 Total 16 19 128 115 83 63 240 11 675 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 57 0 0 0 0 0 57 Indirect 5 17 7 77 42 16 84 5 254 Induced 13 4 2 58 46 36 127 7 293 Total 18 21 66 135 88 52 212 12 604 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Mississippi Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 33 0 0 0 0 0 33 Indirect 5 17 7 74 41 13 77 5 239 Induced 13 3 2 58 45 33 118 6 280 Total 18 20 43 132 86 46 195 11 551 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 30 0 0 0 0 0 30 Indirect 5 17 8 76 43 14 82 5 250 Induced 14 3 2 60 48 34 125 7 295 Total 20 20 40 136 92 48 207 12 575 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 26 0 0 0 0 0 26 Indirect 7 20 10 88 54 15 100 7 299 Induced 19 4 3 71 59 41 154 8 359 Total 25 24 39 159 113 56 254 15 685 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-145 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Missouri Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-146 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 42 0 271 0 0 0 0 314 Indirect 1 5 7 54 52 26 165 6 316 Induced 7 1 3 40 36 66 266 8 427 Total 9 48 10 365 88 92 431 14 1,057 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 67 0 394 0 0 0 0 461 Indirect 2 7 10 81 75 38 236 9 458 Induced 11 1 5 59 52 94 377 11 609 Total 13 75 14 534 127 132 613 20 1,529 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 86 0 501 0 0 0 0 587 Indirect 3 8 12 100 94 48 293 12 568 Induced 14 1 6 71 64 117 466 14 753 Total 16 95 18 672 158 165 759 25 1,908 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Missouri Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 80 0 514 0 0 0 0 594 Indirect 2 8 13 102 93 48 298 12 576 Induced 14 1 6 73 65 118 469 14 759 Total 16 89 18 689 158 166 767 26 1,929 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 86 0 571 0 0 0 0 657 Indirect 3 8 13 115 102 52 324 13 629 Induced 15 1 6 79 70 129 509 15 825 Total 17 96 20 764 172 181 833 28 2,111 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 110 0 703 0 0 0 0 814 Indirect 3 10 17 145 125 64 401 16 782 Induced 18 1 8 98 87 159 629 19 1,020 Total 22 122 25 947 213 224 1,029 35 2,616 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-147 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Montana Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-148 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 35 0 0 0 0 0 0 35 Indirect 1 15 3 6 10 3 21 1 60 Induced 4 2 1 5 10 9 35 1 67 Total 5 52 4 11 19 12 56 2 162 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 32 0 0 0 0 0 0 32 Indirect 2 26 3 9 14 4 28 1 89 Induced 6 4 1 7 14 12 48 2 94 Total 8 62 4 17 28 16 76 3 214 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 28 0 0 0 0 0 0 28 Indirect 2 32 3 11 17 5 34 2 106 Induced 8 5 1 9 16 14 57 2 112 Total 10 65 5 20 33 19 90 4 246 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Montana Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 25 0 0 0 0 0 0 26 Indirect 2 32 3 11 16 5 35 2 107 Induced 9 5 1 9 16 14 58 2 114 Total 11 63 5 20 32 19 92 4 246 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 22 0 0 0 0 0 0 22 Indirect 2 35 3 12 16 5 37 2 113 Induced 10 6 1 10 16 15 61 3 121 Total 12 63 5 22 33 20 98 5 257 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 23 0 0 0 0 0 0 24 Indirect 3 46 4 15 20 6 45 2 143 Induced 13 7 1 12 20 19 76 3 151 Total 16 77 6 27 40 25 122 6 318 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-149 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Nebraska Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-150 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 8 0 0 0 0 8 Indirect 2 2 4 23 31 9 48 2 120 Induced 8 0 1 20 21 16 68 2 137 Total 10 2 6 51 52 24 116 4 265 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 21 0 0 0 0 21 Indirect 3 2 6 35 52 16 79 3 197 Induced 12 0 2 31 33 24 107 4 212 Total 14 2 8 87 84 40 186 7 429 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 25 0 0 0 0 25 Indirect 4 3 7 46 64 19 104 4 252 Induced 15 0 2 38 40 30 133 4 263 Total 19 3 9 108 105 49 238 9 540 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Nebraska Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 27 0 0 0 0 27 Indirect 4 3 8 49 64 20 114 5 266 Induced 16 1 2 39 40 31 139 5 272 Total 19 4 10 116 104 51 252 9 565 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 30 0 0 0 0 30 Indirect 4 3 9 58 68 22 128 5 297 Induced 17 1 3 43 43 33 152 5 295 Total 21 4 11 131 111 55 279 10 622 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 37 0 0 0 0 37 Indirect 5 4 11 77 85 28 166 6 382 Induced 21 1 3 55 53 41 191 6 372 Total 26 4 14 169 138 69 357 12 791 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-151 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Nevada Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-152 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 40 1 0 0 0 0 41 Indirect 0 10 2 7 6 5 34 1 65 Induced 0 1 1 4 8 11 48 1 74 Total 0 11 43 11 14 16 83 2 180 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 2 0 0 0 0 2 Indirect 0 14 2 7 7 3 32 1 65 Induced 0 1 1 5 7 7 39 1 61 Total 0 15 2 13 14 10 71 2 128 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 6 2 0 0 0 0 9 Indirect 0 18 2 8 9 4 43 1 85 Induced 1 2 1 6 9 10 53 1 83 Total 1 19 9 16 18 14 96 2 177 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Nevada Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 2 0 0 0 0 2 Indirect 0 18 2 7 9 3 43 1 83 Induced 1 2 1 6 10 9 52 1 81 Total 1 19 3 15 19 13 94 2 167 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 2 0 0 0 0 2 Indirect 0 19 2 8 11 4 47 1 92 Induced 1 2 1 6 11 11 58 2 91 Total 1 21 3 16 22 14 105 3 185 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 3 0 0 0 0 3 Indirect 0 24 2 9 14 5 61 2 117 Induced 1 2 1 8 15 14 75 2 117 Total 1 27 3 20 29 19 136 3 237 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-153 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New Hampshire Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-154 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 1 10 2 2 10 0 25 Induced 0 0 0 4 2 4 15 0 27 Total 1 0 1 15 3 6 25 1 52 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 1 14 2 3 15 1 36 Induced 1 0 0 6 2 6 23 1 39 Total 1 0 1 20 5 9 38 1 75 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 1 16 3 4 19 1 45 Induced 1 0 0 7 3 8 29 1 49 Total 1 0 2 23 6 12 48 1 94 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New Hampshire Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 1 16 3 4 19 1 44 Induced 1 0 0 7 3 8 29 1 49 Total 1 0 2 23 6 12 48 2 93 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 1 16 3 4 21 1 47 Induced 1 0 0 8 3 9 32 1 53 Total 1 0 2 24 6 13 53 2 100 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 1 2 20 4 6 27 1 60 Induced 1 0 1 9 4 11 41 1 68 Total 1 1 2 29 8 17 68 2 128 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-155 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New Jersey Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-156 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 10 71 0 0 0 0 81 Indirect 0 1 6 48 25 23 146 4 253 Induced 2 0 2 46 26 39 185 5 306 Total 2 1 19 165 51 62 331 8 640 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 73 0 0 0 0 73 Indirect 1 1 9 61 35 30 207 5 349 Induced 3 0 3 62 37 53 252 6 418 Total 3 1 12 197 72 84 459 11 841 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 106 0 0 0 0 106 Indirect 1 2 11 72 43 38 254 6 426 Induced 3 0 4 75 46 66 305 8 508 Total 4 2 15 253 89 104 559 14 1,040 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New Jersey Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 94 0 0 0 0 94 Indirect 1 2 12 63 43 36 257 6 419 Induced 3 0 4 75 47 66 303 8 505 Total 4 2 16 233 90 101 560 14 1,019 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 111 0 0 0 0 111 Indirect 1 2 11 64 47 38 275 7 445 Induced 4 0 4 79 51 71 322 9 539 Total 5 2 15 253 98 109 597 15 1,095 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 167 0 0 0 0 167 Indirect 1 2 13 76 61 50 348 8 559 Induced 5 0 5 98 65 91 406 11 680 Total 6 2 18 341 125 142 754 19 1,406 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-157 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New Mexico Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-158 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,990 26 68 4 0 3 0 2,091 Indirect 1 49 64 17 78 44 268 10 529 Induced 6 8 6 14 63 134 489 15 736 Total 7 2,047 96 99 146 178 760 24 3,356 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,784 6 102 5 0 2 0 1,898 Indirect 1 70 58 22 83 47 265 10 556 Induced 7 13 6 17 62 126 462 14 706 Total 7 1,867 70 141 149 173 729 25 3,160 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,329 5 115 5 0 1 0 1,456 Indirect 1 80 46 25 77 44 242 10 525 Induced 7 15 6 18 54 107 398 13 617 Total 8 1,424 57 159 136 151 641 24 2,599 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New Mexico Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,109 21 127 5 0 2 0 1,263 Indirect 1 82 40 24 74 45 235 10 510 Induced 7 16 5 18 50 99 371 13 579 Total 8 1,206 66 168 129 144 608 23 2,352 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,001 6 132 5 0 2 0 1,146 Indirect 1 88 37 24 73 44 228 10 505 Induced 7 17 5 19 47 94 354 12 556 Total 8 1,106 48 174 126 138 584 23 2,206 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,153 7 155 6 0 2 0 1,323 Indirect 1 114 43 28 86 51 270 12 606 Induced 8 23 7 23 56 110 418 15 660 Total 10 1,290 56 206 148 161 690 27 2,589 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-159 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New York Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-160 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 27 3 31 0 0 0 0 61 Indirect 2 10 30 164 79 57 635 16 994 Induced 8 1 11 118 89 127 884 21 1,260 Total 10 39 45 314 167 184 1,519 37 2,316 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 17 0 33 0 0 0 0 50 Indirect 3 14 35 235 111 82 954 23 1,458 Induced 12 2 15 169 124 181 1,284 30 1,816 Total 15 34 50 436 236 263 2,238 53 3,325 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 10 2 49 0 0 0 0 60 Indirect 4 18 38 282 127 101 1,145 29 1,744 Induced 15 3 17 199 140 221 1,530 36 2,162 Total 19 31 56 531 267 322 2,675 65 3,967 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New York Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 6 0 45 0 0 0 0 51 Indirect 4 18 37 262 117 99 1,144 29 1,709 Induced 15 3 17 195 131 220 1,518 36 2,135 Total 19 27 54 502 248 319 2,661 65 3,895 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4 0 53 0 0 0 0 57 Indirect 5 19 35 270 119 107 1,196 31 1,782 Induced 17 3 17 204 133 234 1,583 39 2,229 Total 22 27 52 528 252 341 2,779 69 4,069 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 5 0 80 0 0 0 0 85 Indirect 6 24 41 327 141 136 1,469 38 2,182 Induced 21 4 20 252 158 294 1,936 47 2,732 Total 27 33 61 660 299 430 3,405 85 5,000 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-161 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES North Carolina Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-162 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 5 0 0 0 0 0 5 Indirect 3 5 17 135 33 26 187 7 414 Induced 9 1 5 120 37 61 247 10 490 Total 13 6 27 255 71 87 434 17 909 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 5 7 24 195 47 38 280 11 605 Induced 14 1 8 175 51 89 362 14 712 Total 18 8 31 369 98 127 641 25 1,318 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 9 0 0 0 0 0 9 Indirect 5 8 30 240 56 48 349 14 752 Induced 16 1 10 210 62 110 459 17 885 Total 22 9 48 450 118 158 808 31 1,645 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES North Carolina Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 5 8 32 226 53 47 357 14 744 Induced 16 1 10 206 60 109 470 18 890 Total 21 9 43 432 113 157 827 32 1,634 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 5 9 36 232 56 51 388 16 793 Induced 17 1 12 213 63 118 518 20 962 Total 23 10 47 445 118 170 906 35 1,754 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 7 11 46 273 68 63 489 20 978 Induced 23 2 15 258 77 147 660 25 1,206 Total 31 13 62 531 145 210 1,149 45 2,185 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-163 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES North Dakota Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-164 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 22 2 6 7 3 14 1 55 Induced 5 5 1 4 6 7 21 1 50 Total 6 26 2 11 13 10 35 2 105 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 56 3 10 11 5 21 1 110 Induced 7 12 1 7 10 10 32 2 81 Total 8 68 4 17 21 15 53 3 190 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 75 3 14 14 6 28 2 143 Induced 8 17 1 9 12 12 41 2 102 Total 11 91 4 23 26 18 69 4 245 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES North Dakota Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 84 3 15 14 6 30 2 156 Induced 9 18 1 10 12 13 44 2 109 Total 11 103 5 25 26 18 74 4 265 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 94 4 17 15 6 34 2 174 Induced 10 21 1 12 13 14 50 2 122 Total 12 115 5 29 28 20 84 4 296 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 127 5 21 19 8 45 2 230 Induced 12 28 2 16 16 17 66 3 160 Total 15 155 6 37 35 25 111 5 390 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-165 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Ohio Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-166 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 82 0 457 0 0 0 0 539 Indirect 3 32 22 448 155 136 494 12 1,302 Induced 14 6 9 177 118 171 694 16 1,204 Total 16 120 30 1,081 274 307 1,188 28 3,045 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 83 0 536 0 0 0 0 620 Indirect 4 46 29 623 210 171 644 16 1,743 Induced 18 8 11 251 162 216 890 21 1,579 Total 22 137 40 1,410 373 387 1,535 37 3,942 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 109 0 827 0 0 0 0 936 Indirect 5 60 35 808 298 249 862 22 2,338 Induced 24 11 15 315 215 293 1,191 28 2,091 Total 29 180 50 1,950 513 542 2,053 49 5,366 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Ohio Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 96 0 750 0 0 0 0 846 Indirect 5 59 36 806 282 230 823 21 2,263 Induced 23 11 14 325 210 277 1,132 27 2,019 Total 28 166 50 1,881 492 507 1,955 48 5,127 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 112 0 890 0 0 0 0 1,002 Indirect 6 64 39 906 320 264 909 23 2,530 Induced 25 12 16 359 234 310 1,256 30 2,241 Total 30 187 54 2,155 554 574 2,166 53 5,774 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 171 0 1,329 0 0 0 0 1,500 Indirect 7 84 51 1,195 439 372 1,226 31 3,405 Induced 32 15 21 470 313 425 1,702 39 3,017 Total 39 270 72 2,994 752 797 2,929 70 7,921 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-167 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Oklahoma Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-168 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,364 133 368 37 0 22 0 1,924 Indirect 2 168 30 128 170 89 451 15 1,053 Induced 13 34 6 47 107 169 637 17 1,031 Total 15 1,566 169 543 314 259 1,111 32 4,008 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 2,062 122 587 113 0 37 0 2,922 Indirect 3 242 44 196 263 142 684 22 1,595 Induced 18 50 9 70 157 249 937 25 1,517 Total 21 2,355 175 853 533 391 1,658 47 6,033 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 2,372 136 744 132 0 39 0 3,422 Indirect 4 278 49 235 318 172 812 27 1,894 Induced 22 59 11 83 186 296 1,112 31 1,800 Total 26 2,708 195 1,062 636 468 1,962 58 7,116 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Oklahoma Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 2,538 151 738 138 0 41 0 3,606 Indirect 4 285 52 234 323 173 847 28 1,944 Induced 23 58 11 85 192 307 1,157 32 1,866 Total 27 2,881 215 1,057 653 480 2,045 60 7,416 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 2,699 168 804 155 0 46 0 3,872 Indirect 4 305 55 254 347 186 912 30 2,092 Induced 25 63 12 92 207 331 1,250 34 2,014 Total 29 3,067 234 1,150 709 517 2,208 65 7,978 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 3,375 209 973 195 0 57 0 4,809 Indirect 5 386 68 315 427 228 1,132 37 2,598 Induced 31 80 15 115 256 410 1,548 42 2,498 Total 36 3,842 292 1,402 878 638 2,738 80 9,905 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-169 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Oregon Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-170 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 25 24 0 0 0 0 50 Indirect 6 3 7 79 23 20 100 4 242 Induced 12 0 3 39 22 35 140 5 256 Total 18 3 35 143 45 55 240 9 548 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 23 0 0 0 0 23 Indirect 7 4 10 115 32 26 131 6 331 Induced 17 0 4 58 28 43 178 6 334 Total 25 5 14 196 60 68 309 12 689 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 27 0 0 0 0 27 Indirect 9 7 13 145 39 32 165 7 417 Induced 21 1 5 71 34 52 221 8 412 Total 30 8 18 243 73 84 385 15 856 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Oregon Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 21 0 0 0 0 21 Indirect 8 8 13 139 37 29 166 7 408 Induced 21 1 5 72 34 52 221 8 413 Total 30 9 18 232 70 81 387 15 842 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 17 0 0 0 0 17 Indirect 9 10 14 144 37 30 175 7 426 Induced 22 1 5 75 35 55 236 8 439 Total 31 11 19 237 73 84 411 16 883 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 18 0 0 0 0 18 Indirect 10 14 18 173 46 36 218 9 525 Induced 28 2 6 93 45 69 296 10 550 Total 38 16 25 284 91 105 515 19 1,093 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-171 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Pennsylvania Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-172 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,647 308 239 185 0 64 0 2,444 Indirect 5 96 74 437 252 179 1,101 18 2,162 Induced 19 17 19 220 224 371 1,614 32 2,515 Total 23 1,760 401 896 662 550 2,779 49 7,121 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 6,173 320 243 240 0 87 0 7,063 Indirect 7 249 232 676 505 311 2,458 33 4,471 Induced 35 37 38 390 470 806 3,433 64 5,272 Total 42 6,458 589 1,310 1,215 1,117 5,977 97 16,806 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 9,392 479 410 375 0 120 0 10,777 Indirect 10 337 336 918 760 483 3,692 49 6,585 Induced 49 48 55 529 694 1,208 5,097 96 7,774 Total 59 9,777 870 1,857 1,828 1,691 8,909 145 25,136 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Pennsylvania Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 10,254 437 375 334 0 107 0 11,507 Indirect 10 350 371 880 770 475 3,825 49 6,730 Induced 51 48 56 538 715 1,247 5,262 99 8,015 Total 61 10,652 864 1,792 1,819 1,721 9,194 148 26,252 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 11,460 530 445 407 0 131 0 12,973 Indirect 12 383 408 970 874 550 4,328 56 7,582 Induced 57 53 63 593 808 1,415 5,948 112 9,047 Total 69 11,896 1,001 2,008 2,089 1,965 10,407 169 29,603 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 16,495 823 653 633 0 204 0 18,808 Indirect 16 527 574 1,294 1,250 800 6,201 80 10,741 Induced 79 72 89 811 1,156 2,033 8,490 159 12,889 Total 95 17,093 1,486 2,758 3,038 2,833 14,896 239 42,438 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-173 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Rhode Island Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-174 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 2 17 3 3 24 1 49 Induced 1 0 1 8 3 6 37 1 57 Total 1 0 2 25 6 9 62 1 107 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 2 25 5 4 35 1 72 Induced 1 0 1 12 5 9 53 1 82 Total 1 0 3 37 9 13 88 2 153 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 2 30 5 5 41 1 85 Induced 1 0 1 14 5 11 63 1 97 Total 2 0 3 45 10 15 104 3 182 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Rhode Island Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 2 28 5 5 41 1 83 Induced 1 0 1 14 5 11 63 1 96 Total 1 1 3 42 10 15 104 3 179 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 1 2 28 5 5 43 1 85 Induced 1 0 1 14 5 11 66 1 100 Total 2 1 3 43 10 16 110 3 186 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 1 2 33 6 6 53 1 103 Induced 2 0 1 17 6 13 81 2 123 Total 2 1 3 51 12 19 134 3 225 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-175 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES South Carolina Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-176 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 3 1 0 0 0 0 3 Indirect 2 2 7 99 20 11 73 4 216 Induced 5 0 2 55 21 28 108 5 224 Total 7 2 12 154 40 39 181 8 444 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 1 0 0 0 0 1 Indirect 4 3 11 148 29 16 108 5 324 Induced 7 0 3 83 30 42 158 7 330 Total 11 4 14 231 60 58 266 12 655 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 4 1 0 0 0 0 5 Indirect 4 4 13 183 36 21 137 7 405 Induced 9 1 4 102 37 51 200 8 411 Total 13 5 22 285 73 72 337 15 822 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES South Carolina Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 1 1 0 0 0 0 2 Indirect 4 4 14 187 36 20 141 7 413 Induced 9 1 4 107 37 51 204 8 420 Total 12 5 19 295 73 71 345 15 835 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 1 1 0 0 0 0 3 Indirect 4 5 15 207 38 22 155 7 454 Induced 9 1 4 118 39 55 225 9 460 Total 13 6 21 327 78 77 380 16 917 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 2 0 0 0 0 2 Indirect 5 7 19 262 47 27 197 9 573 Induced 11 1 5 151 49 68 284 11 581 Total 16 8 24 415 96 95 481 20 1,155 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-177 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES South Dakota Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-178 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 1 2 11 5 3 14 1 37 Induced 4 0 1 7 5 7 26 1 51 Total 5 2 2 18 10 10 40 2 88 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 2 2 16 8 4 21 1 56 Induced 7 0 1 11 7 10 38 2 76 Total 8 2 3 27 15 15 59 3 132 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 2 2 19 10 5 26 2 68 Induced 9 0 1 14 9 13 46 2 93 Total 11 3 3 33 18 18 72 4 161 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES South Dakota Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 2 2 18 10 5 27 2 69 Induced 9 0 1 14 9 13 47 2 95 Total 11 3 3 32 19 18 74 4 163 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 2 2 19 12 6 29 2 74 Induced 10 0 1 15 10 14 51 2 102 Total 12 3 3 33 22 19 80 4 176 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 3 3 23 15 7 36 2 92 Induced 13 0 1 18 13 17 64 3 128 Total 16 4 4 40 28 24 100 5 220 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-179 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Tennessee Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-180 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 12 0 0 0 0 12 Indirect 2 6 10 111 42 21 114 5 310 Induced 8 1 3 78 49 44 172 6 361 Total 9 7 13 201 90 65 286 11 683 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 5 0 0 0 0 5 Indirect 2 9 15 168 60 29 167 7 458 Induced 11 2 5 119 71 62 246 9 523 Total 14 11 19 292 131 90 413 16 986 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 13 0 0 0 0 13 Indirect 3 12 18 211 73 37 210 9 573 Induced 14 2 6 150 83 76 306 11 648 Total 18 14 24 374 156 113 516 20 1,233 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Tennessee Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 8 0 0 0 0 8 Indirect 3 12 19 217 71 36 219 9 586 Induced 15 2 6 159 82 77 312 11 664 Total 18 14 25 384 154 113 531 20 1,258 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 8 0 0 0 0 8 Indirect 4 12 20 244 76 39 238 10 642 Induced 16 2 6 176 87 83 339 12 721 Total 20 14 27 428 163 122 576 21 1,372 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 7 0 0 0 0 7 Indirect 5 15 26 310 95 48 300 12 810 Induced 21 3 8 226 108 103 425 15 909 Total 26 18 34 543 203 151 725 27 1,727 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-181 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Texas Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-182 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 14,752 1,368 2,788 498 0 216 0 19,621 Indirect 20 1,654 380 1,742 2,122 1,233 6,422 63 13,636 Induced 121 424 94 878 1,612 2,391 9,109 109 14,739 Total 141 16,830 1,842 5,408 4,233 3,624 15,746 172 47,995 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 20,276 1,078 3,983 823 0 303 0 26,463 Indirect 26 2,279 498 2,390 3,007 1,699 8,674 89 18,662 Induced 164 591 126 1,189 2,162 3,174 12,092 146 19,643 Total 189 23,147 1,702 7,563 5,991 4,873 21,070 235 64,768 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 24,667 1,411 5,238 1,147 0 377 0 32,840 Indirect 34 2,738 582 3,091 3,856 2,251 11,054 118 23,722 Induced 207 732 160 1,494 2,744 4,042 15,380 187 24,945 Total 241 28,136 2,153 9,823 7,747 6,292 26,811 305 81,507 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Texas Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 25,997 1,486 5,190 1,144 0 377 0 34,194 Indirect 34 2,833 620 3,092 3,930 2,271 11,479 122 24,380 Induced 213 742 165 1,526 2,814 4,154 15,838 195 25,648 Total 247 29,573 2,270 9,808 7,888 6,425 27,694 317 84,223 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 27,455 1,690 5,678 1,291 0 425 0 36,540 Indirect 37 3,009 651 3,369 4,259 2,484 12,409 135 26,353 Induced 231 797 179 1,641 3,044 4,501 17,162 213 27,767 Total 267 31,261 2,520 10,688 8,594 6,985 29,997 347 90,660 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 33,667 2,009 6,975 1,565 0 516 0 44,731 Indirect 45 3,724 805 4,139 5,220 3,038 15,222 168 32,359 Induced 285 987 220 2,014 3,727 5,507 20,996 263 33,998 Total 330 38,377 3,034 13,127 10,513 8,545 36,733 431 111,089 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-183 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Utah Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-184 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 695 247 161 116 0 38 0 1,256 Indirect 1 30 26 93 120 84 495 6 855 Induced 7 4 8 60 96 172 659 9 1,015 Total 8 729 281 313 331 256 1,192 16 3,126 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 960 173 199 147 0 48 0 1,527 Indirect 1 43 34 118 153 100 639 8 1,096 Induced 10 6 10 82 118 208 799 12 1,243 Total 11 1,008 217 398 419 308 1,485 20 3,866 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,122 175 216 156 0 46 0 1,714 Indirect 2 51 38 139 173 112 729 10 1,254 Induced 11 7 11 96 134 234 904 14 1,411 Total 13 1,180 224 451 462 346 1,679 24 4,379 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Utah Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,207 190 216 161 0 47 0 1,821 Indirect 2 52 40 138 180 116 770 11 1,309 Induced 12 7 12 99 139 245 954 15 1,482 Total 14 1,266 242 453 480 362 1,770 25 4,613 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,256 193 223 164 0 48 0 1,885 Indirect 2 56 42 145 187 121 802 11 1,368 Induced 13 7 12 105 145 256 1,000 16 1,553 Total 15 1,320 248 473 497 377 1,850 27 4,807 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,344 209 256 177 0 52 0 2,038 Indirect 2 68 47 171 212 136 903 13 1,552 Induced 14 9 14 124 164 286 1,124 18 1,753 Total 17 1,421 269 551 553 422 2,079 32 5,343 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-185 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Vermont Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-186 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 1 1 10 3 2 11 1 29 Induced 1 0 0 8 4 5 20 1 39 Total 2 1 2 18 7 6 31 1 68 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 1 2 14 5 2 17 1 43 Induced 2 0 1 12 5 7 30 1 58 Total 3 1 2 26 10 9 47 2 101 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 1 2 17 6 3 21 1 52 Induced 3 0 1 15 6 8 36 1 70 Total 4 1 3 32 12 11 57 2 123 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Vermont Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 1 2 15 6 3 22 1 50 Induced 3 0 1 14 6 8 36 1 70 Total 4 1 3 29 12 11 58 2 121 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 1 2 15 6 3 23 1 52 Induced 3 0 1 15 7 9 38 1 73 Total 4 1 3 29 12 12 61 3 125 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 1 3 17 7 4 28 1 62 Induced 4 0 1 17 8 11 47 2 89 Total 5 1 4 35 15 14 74 3 152 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-187 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Virginia Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-188 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 122 9 41 5 0 2 0 179 Indirect 2 22 23 81 69 27 324 9 556 Induced 7 3 7 58 49 67 335 11 538 Total 9 147 39 180 124 94 661 20 1,273 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 112 4 45 3 0 1 0 165 Indirect 3 29 29 112 86 35 441 12 746 Induced 10 4 9 84 64 88 449 15 723 Total 14 144 41 241 154 123 891 27 1,634 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 95 4 67 3 0 1 0 170 Indirect 4 35 32 141 110 42 545 15 924 Induced 13 5 11 104 77 106 549 18 883 Total 17 135 47 311 190 148 1,095 34 1,977 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Virginia Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 84 4 61 4 0 1 0 154 Indirect 4 34 32 138 104 40 561 15 929 Induced 13 5 10 105 75 107 558 19 893 Total 17 123 47 304 183 147 1,120 34 1,976 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 78 4 74 4 0 1 0 161 Indirect 5 36 34 145 116 45 621 17 1,017 Induced 15 6 11 111 80 117 615 20 974 Total 19 119 49 329 200 162 1,237 37 2,152 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 89 5 114 4 0 1 0 213 Indirect 6 45 42 173 159 59 820 22 1,326 Induced 17 7 14 133 104 150 799 25 1,250 Total 23 141 61 420 267 210 1,621 47 2,789 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-189 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Washington Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-190 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 2 6 30 13 9 68 3 134 Induced 8 0 2 22 15 22 91 4 164 Total 11 2 9 52 28 31 158 6 298 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 4 2 10 38 20 14 106 4 198 Induced 13 0 4 30 23 32 136 5 243 Total 17 2 13 68 43 46 242 10 441 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 5 3 11 47 25 18 132 5 246 Induced 16 0 4 37 29 39 166 7 298 Total 21 3 15 84 53 56 299 12 544 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Washington Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 5 4 11 51 25 17 135 5 253 Induced 16 0 4 40 30 39 168 7 304 Total 22 4 16 91 55 56 303 12 557 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 5 4 12 60 27 19 143 6 275 Induced 17 0 4 45 32 41 179 7 327 Total 23 5 16 105 59 60 322 13 602 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 7 6 15 80 34 23 179 7 350 Induced 22 1 5 59 41 51 223 9 411 Total 28 7 20 139 75 74 403 16 761 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-191 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES West Virginia Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-192 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 996 96 55 87 0 28 0 1,261 Indirect 1 87 33 40 88 35 198 4 487 Induced 3 15 4 18 49 85 310 7 491 Total 4 1,098 132 112 225 120 536 11 2,239 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 2,446 117 62 95 0 31 0 2,751 Indirect 1 150 81 61 152 62 366 7 880 Induced 4 23 7 29 92 165 599 14 932 Total 6 2,618 204 153 339 227 996 20 4,563 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 3,394 165 92 141 0 41 0 3,832 Indirect 2 197 108 79 212 89 519 9 1,216 Induced 5 29 10 37 125 229 832 19 1,285 Total 7 3,620 283 208 478 318 1,392 28 6,333 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES West Virginia Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 3,605 157 84 128 0 37 0 4,011 Indirect 2 202 117 81 213 89 529 9 1,243 Induced 6 30 10 38 127 236 860 19 1,326 Total 7 3,836 285 204 468 326 1,425 29 6,580 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 3,949 186 102 152 0 44 0 4,434 Indirect 2 220 127 92 239 102 594 11 1,387 Induced 6 32 11 42 140 263 959 22 1,476 Total 8 4,202 325 236 531 365 1,597 32 7,297 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 5,567 280 157 229 0 67 0 6,299 Indirect 3 289 177 124 340 146 847 15 1,941 Induced 8 42 16 56 196 372 1,352 30 2,072 Total 11 5,898 473 337 765 519 2,266 45 10,313 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-193 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Wisconsin Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-194 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 11 0 6 0 0 0 0 17 Indirect 3 3 9 195 34 19 120 4 386 Induced 12 0 3 99 35 44 181 6 380 Total 15 15 12 299 69 63 300 10 783 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 27 0 7 0 0 0 0 34 Indirect 4 4 12 287 50 29 180 7 573 Induced 18 0 4 148 50 66 265 9 560 Total 22 31 16 442 100 95 445 15 1,167 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 30 0 10 0 0 0 0 40 Indirect 6 5 15 354 62 36 227 8 713 Induced 23 1 5 181 62 80 327 10 689 Total 28 35 20 545 124 116 554 19 1,442 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Wisconsin Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 33 0 9 0 0 0 0 42 Indirect 6 5 15 351 65 37 244 8 730 Induced 24 1 5 184 65 82 339 11 710 Total 30 38 20 544 130 118 583 19 1,482 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 37 0 11 0 0 0 0 48 Indirect 6 5 16 380 71 40 269 9 796 Induced 26 1 5 196 71 89 368 11 768 Total 33 43 21 587 142 129 637 21 1,613 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 47 0 17 0 0 0 0 64 Indirect 8 6 19 476 90 51 348 11 1,011 Induced 33 1 7 245 90 112 467 14 970 Total 42 54 26 738 181 163 815 26 2,044 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-195 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Wyoming Value Added Contribution by State and Industry: Unconventional Gas* ($M) B-196 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4,639 164 112 76 0 23 0 5,014 Indirect 1 79 136 11 156 66 351 8 807 Induced 3 10 9 7 102 186 608 16 940 Total 4 4,727 308 129 334 252 981 24 6,760 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 5,436 204 103 160 0 50 0 5,953 Indirect 1 100 161 14 214 93 504 11 1,099 Induced 6 19 16 13 193 348 1,139 30 1,763 Total 7 5,555 381 129 568 441 1,692 41 8,815 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 5,858 208 107 173 0 48 0 6,394 Indirect 1 114 171 16 232 102 551 13 1,200 Induced 7 22 17 14 209 376 1,231 33 1,910 Total 8 5,993 397 137 614 479 1,829 46 9,503 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Wyoming Value Added Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 6,590 257 104 203 0 56 0 7,211 Indirect 1 121 192 17 255 117 631 14 1,348 Induced 8 22 20 16 236 426 1,397 37 2,162 Total 9 6,734 469 136 694 543 2,085 52 10,722 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 7,056 296 105 236 0 65 0 7,758 Indirect 1 130 204 18 274 129 693 16 1,465 Induced 9 24 21 17 257 464 1,521 41 2,354 Total 10 7,210 522 141 766 593 2,280 57 11,578 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 9,029 369 120 294 0 82 0 9,894 Indirect 1 165 261 23 344 162 878 20 1,855 Induced 11 31 27 21 326 589 1,929 52 2,986 Total 13 9,226 657 164 964 751 2,889 72 14,735 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-197 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Labor Income Contribution by State and Industry Alabama Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-198 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 88 28 1 0 0 0 0 117 Indirect 2 10 14 84 24 13 85 5 237 Induced 4 2 3 40 22 35 117 7 229 Total 6 100 44 125 46 48 202 12 583 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 57 77 1 0 0 0 0 135 Indirect 3 14 14 125 35 20 125 7 343 Induced 6 3 3 58 33 48 162 10 322 Total 9 73 95 184 68 69 287 17 801 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 32 46 2 0 0 0 0 80 Indirect 4 19 14 154 39 22 133 8 393 Induced 7 4 4 70 36 51 178 11 361 Total 11 55 63 226 75 73 312 19 834 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Alabama Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 18 23 2 0 0 0 0 42 Indirect 4 20 13 163 38 21 128 8 394 Induced 7 4 3 74 36 49 175 10 359 Total 10 42 39 239 74 69 303 19 795 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 12 44 2 0 0 0 0 57 Indirect 4 22 13 188 42 24 145 9 447 Induced 7 5 4 83 39 53 193 11 396 Total 11 39 61 273 81 77 337 20 900 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 14 13 2 0 0 0 0 29 Indirect 4 28 16 246 53 27 170 11 556 Induced 9 6 4 108 49 63 231 14 484 Total 13 48 34 356 102 90 402 25 1,069 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-199 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Arizona Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-200 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 15 10 36 19 13 98 4 197 Induced 3 2 3 19 20 33 148 6 233 Total 4 17 13 55 39 46 246 10 430 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 20 17 50 29 20 148 7 292 Induced 5 2 5 27 32 49 223 9 351 Total 6 23 21 77 61 69 371 15 643 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 24 21 60 38 26 192 9 372 Induced 5 3 6 32 40 61 286 11 445 Total 7 27 27 92 79 87 478 20 816 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Arizona Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 23 25 56 40 27 205 9 387 Induced 5 3 7 31 43 63 304 12 469 Total 7 25 31 87 84 90 509 21 855 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 24 26 58 45 31 233 11 430 Induced 6 3 7 33 49 71 344 14 526 Total 8 27 34 91 94 101 577 24 956 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 30 33 71 60 39 307 14 557 Induced 7 4 9 41 65 91 450 18 684 Total 9 34 43 112 124 129 757 32 1,241 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-201 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Arkansas Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-202 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 999 43 68 46 0 14 0 1,171 Indirect 2 17 78 66 82 46 261 9 561 Induced 6 2 6 35 63 110 345 15 582 Total 8 1,018 127 170 191 156 620 25 2,314 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,482 61 127 39 0 16 0 1,725 Indirect 4 24 116 99 120 73 388 14 838 Induced 9 2 9 50 91 160 501 22 845 Total 12 1,508 186 276 250 233 905 36 3,407 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,702 63 156 42 0 15 0 1,979 Indirect 4 28 130 124 144 89 458 17 995 Induced 10 3 11 61 105 186 584 26 986 Total 15 1,733 205 341 292 275 1,057 43 3,960 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Arkansas Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,782 68 156 43 0 16 0 2,066 Indirect 4 29 138 126 147 92 477 18 1,032 Induced 11 3 11 63 107 194 611 27 1,027 Total 15 1,814 218 346 297 286 1,104 45 4,124 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,805 69 167 44 0 16 0 2,102 Indirect 4 30 139 135 153 96 492 19 1,068 Induced 11 3 12 67 109 200 629 28 1,059 Total 15 1,838 220 369 306 296 1,137 47 4,229 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 2,137 78 202 50 0 18 0 2,485 Indirect 5 36 163 164 184 114 583 23 1,273 Induced 14 4 14 82 130 238 747 34 1,262 Total 19 2,177 256 447 364 352 1,349 57 5,020 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-203 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES California Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-204 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 44 0 305 0 0 0 0 349 Indirect 4 14 19 120 55 50 309 12 584 Induced 14 3 8 76 47 81 378 15 620 Total 18 62 27 501 102 131 686 27 1,553 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 72 42 433 0 0 0 0 547 Indirect 6 21 29 167 81 73 452 17 847 Induced 19 5 12 110 69 117 546 22 900 Total 25 98 83 710 151 190 998 39 2,295 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 76 0 525 0 0 0 0 601 Indirect 7 26 35 199 99 89 540 21 1,014 Induced 23 6 15 132 84 139 645 26 1,069 Total 31 107 50 855 183 227 1,184 47 2,685 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES California Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 72 0 506 0 0 0 0 578 Indirect 7 26 37 184 99 87 543 21 1,005 Induced 24 6 15 129 86 139 646 26 1,071 Total 31 104 52 819 186 226 1,189 47 2,655 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 71 0 526 0 0 0 0 598 Indirect 8 28 39 190 107 93 576 23 1,063 Induced 25 6 16 134 94 147 685 28 1,136 Total 33 105 56 850 201 239 1,261 51 2,797 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 79 0 614 0 0 0 0 693 Indirect 10 34 49 228 133 112 710 28 1,303 Induced 31 8 20 165 117 180 845 35 1,401 Total 41 121 69 1,007 250 291 1,555 63 3,397 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-205 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Colorado Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-206 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,588 218 618 92 0 46 0 2,561 Indirect 1 60 163 79 151 135 953 32 1,575 Induced 8 9 22 56 140 325 1,213 49 1,822 Total 9 1,657 402 753 382 461 2,213 81 5,958 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,989 441 1,193 221 0 99 0 3,943 Indirect 2 88 181 138 256 242 1,566 51 2,524 Induced 12 14 33 86 216 499 1,856 75 2,790 Total 14 2,091 656 1,417 693 741 3,521 126 9,258 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 2,017 442 1,354 233 0 94 0 4,140 Indirect 3 106 175 159 280 269 1,710 57 2,758 Induced 14 17 36 95 234 532 1,986 81 2,994 Total 17 2,140 653 1,609 746 801 3,791 137 9,893 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Colorado Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,738 342 1,275 171 0 69 0 3,597 Indirect 2 110 162 140 246 233 1,484 50 2,426 Induced 13 18 31 87 207 465 1,755 71 2,648 Total 16 1,866 535 1,502 625 698 3,308 121 8,671 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,557 282 1,294 142 0 58 0 3,333 Indirect 3 119 151 135 233 220 1,392 48 2,300 Induced 14 19 29 84 197 437 1,663 68 2,511 Total 16 1,695 462 1,513 573 656 3,112 116 8,143 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,727 292 1,514 147 0 60 0 3,739 Indirect 3 150 172 156 266 247 1,578 55 2,628 Induced 17 24 33 98 226 495 1,898 77 2,868 Total 20 1,901 497 1,768 639 742 3,536 132 9,236 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-207 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Connecticut Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-208 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 1 5 49 13 9 81 2 160 Induced 1 0 2 20 14 21 124 3 184 Total 1 1 7 68 28 29 205 6 344 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 1 8 64 18 13 114 4 222 Induced 1 0 2 28 19 29 173 5 257 Total 1 1 10 92 37 42 287 8 479 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 2 9 78 22 16 133 4 265 Induced 1 0 3 34 21 35 200 6 301 Total 2 2 12 113 43 50 334 10 566 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Connecticut Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 2 10 79 21 15 129 4 259 Induced 1 0 3 36 20 34 193 6 294 Total 2 2 12 114 41 50 322 10 554 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 1 10 87 22 17 131 5 273 Induced 1 0 3 39 21 36 197 6 304 Total 2 2 13 127 43 53 328 10 577 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 2 12 112 26 21 156 6 335 Induced 2 0 3 51 25 44 235 7 367 Total 2 2 16 163 52 64 391 13 702 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-209 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Delaware Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-210 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 16 0 0 0 0 16 Indirect 0 0 2 7 4 4 27 1 46 Induced 0 0 1 5 3 7 37 1 55 Total 0 0 3 29 7 11 64 2 116 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 21 0 0 0 0 21 Indirect 0 0 3 11 6 5 39 1 65 Induced 0 0 1 7 4 9 54 2 78 Total 1 0 4 39 10 15 93 3 164 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 36 0 0 0 0 36 Indirect 0 0 4 14 8 9 52 2 89 Induced 1 0 1 9 6 12 71 2 102 Total 1 0 5 58 14 21 123 4 226 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Delaware Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 32 0 0 0 0 32 Indirect 0 0 4 12 8 8 52 2 87 Induced 1 0 1 8 6 13 71 2 102 Total 1 0 5 53 14 21 123 4 221 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 39 0 0 0 0 39 Indirect 0 0 5 13 10 10 56 2 96 Induced 1 0 1 9 7 14 78 2 112 Total 1 0 6 61 17 24 134 4 247 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 60 0 0 0 0 60 Indirect 0 0 6 16 14 14 74 3 127 Induced 1 0 2 11 9 20 101 3 146 Total 1 0 8 87 23 34 174 6 334 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-211 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES District of Columbia Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-212 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 0 0 1 0 24 1 27 Induced 0 0 0 0 1 1 31 2 34 Total 0 0 0 0 1 1 55 2 61 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 0 0 1 1 37 2 40 Induced 0 0 0 0 1 1 46 2 51 Total 0 0 1 0 2 2 83 4 91 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 1 0 1 1 47 2 51 Induced 0 0 0 0 1 2 57 3 64 Total 0 0 1 0 3 2 104 5 115 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES District of Columbia Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 1 0 1 1 47 2 52 Induced 0 0 0 0 1 2 59 3 65 Total 0 0 1 0 3 2 106 5 117 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 1 0 2 1 50 2 55 Induced 0 0 0 0 2 2 63 3 70 Total 0 0 1 0 3 2 113 5 126 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 1 0 2 1 63 3 69 Induced 0 0 1 0 2 2 79 4 89 Total 0 0 1 0 4 3 142 7 158 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-213 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Florida Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-214 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 159 12 0 0 0 0 171 Indirect 2 3 17 38 31 27 193 6 318 Induced 6 0 6 26 34 62 280 9 424 Total 8 4 181 76 65 89 473 15 912 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 350 16 0 0 0 0 366 Indirect 3 5 25 62 51 45 318 10 519 Induced 9 1 9 40 55 101 451 14 679 Total 12 6 384 118 106 146 769 23 1,564 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 154 22 0 0 0 0 176 Indirect 4 5 31 67 57 46 349 12 570 Induced 10 1 10 45 61 108 498 15 748 Total 14 6 195 133 118 154 847 27 1,494 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Florida Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 39 22 0 0 0 0 62 Indirect 3 5 33 59 54 43 350 12 559 Induced 10 1 10 43 60 103 495 15 736 Total 13 5 82 124 114 146 845 27 1,357 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 237 25 0 0 0 0 262 Indirect 4 5 36 69 63 55 425 14 670 Induced 11 1 11 46 70 124 590 18 872 Total 15 6 285 140 133 179 1,015 31 1,804 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 28 31 0 0 0 0 58 Indirect 4 6 47 75 73 61 500 17 781 Induced 13 1 14 54 81 141 697 21 1,021 Total 18 6 88 159 153 202 1,196 38 1,860 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-215 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Georgia Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-216 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 5 57 0 0 0 0 63 Indirect 3 5 14 74 45 32 187 8 366 Induced 5 1 4 56 49 61 245 10 431 Total 8 5 23 187 95 93 432 18 860 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 76 0 0 0 0 76 Indirect 3 6 18 105 69 45 275 11 532 Induced 7 1 6 82 74 86 349 15 619 Total 10 6 24 263 143 131 624 26 1,226 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 8 38 0 0 0 0 46 Indirect 4 7 21 129 83 54 335 14 645 Induced 8 1 7 101 90 102 416 18 743 Total 12 8 37 268 172 156 750 31 1,434 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Georgia Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 3 11 0 0 0 0 14 Indirect 4 7 23 131 81 53 343 14 656 Induced 8 1 8 105 91 102 420 18 753 Total 12 8 33 248 172 155 763 32 1,422 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 4 51 0 0 0 0 55 Indirect 4 7 24 146 91 63 383 15 735 Induced 9 1 9 115 101 116 474 20 844 Total 13 8 37 312 192 179 857 35 1,633 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 8 0 0 0 0 8 Indirect 5 9 30 180 112 75 470 19 900 Induced 11 1 11 143 125 140 579 24 1,035 Total 16 10 41 331 238 216 1,049 43 1,943 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-217 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Idaho Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-218 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 3 3 13 6 4 22 1 52 Induced 3 0 1 9 6 9 32 2 61 Total 5 3 4 21 12 12 54 3 113 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 4 3 19 9 5 34 2 78 Induced 5 0 1 13 9 13 48 2 91 Total 7 5 4 32 17 18 82 4 169 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 7 3 23 10 7 42 3 97 Induced 6 1 1 15 11 16 60 3 112 Total 9 7 4 38 21 23 102 6 210 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Idaho Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 8 3 22 11 7 44 3 100 Induced 6 1 1 16 11 17 62 3 117 Total 9 8 4 38 22 23 106 6 216 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 9 3 23 12 7 48 3 108 Induced 6 1 1 17 12 18 69 4 127 Total 9 10 4 40 24 25 117 6 235 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 4 12 4 27 15 10 60 4 135 Induced 8 1 1 21 15 23 87 4 160 Total 12 13 5 48 30 33 147 8 295 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-219 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Illinois Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-220 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 244 0 47 0 0 0 0 291 Indirect 2 18 20 211 77 50 342 11 729 Induced 7 3 8 106 75 107 487 16 808 Total 9 264 28 364 152 156 829 26 1,828 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 339 0 48 0 0 0 0 387 Indirect 3 24 30 307 112 70 479 15 1,039 Induced 10 4 13 155 108 150 674 21 1,136 Total 13 366 42 510 220 220 1,154 36 2,562 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 479 0 60 0 0 0 0 539 Indirect 3 30 35 365 141 86 595 19 1,274 Induced 12 4 16 189 135 187 838 26 1,407 Total 15 513 51 614 276 272 1,433 45 3,220 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Illinois Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 443 0 59 0 0 0 0 502 Indirect 3 28 36 343 139 83 597 19 1,247 Induced 12 4 16 188 135 183 833 26 1,397 Total 15 475 52 590 274 265 1,430 45 3,146 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 510 0 63 0 0 0 0 573 Indirect 3 30 37 356 150 88 640 20 1,326 Induced 12 4 18 199 146 197 898 28 1,502 Total 15 544 55 618 296 285 1,538 48 3,400 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 727 0 80 0 0 0 0 807 Indirect 4 39 46 431 192 109 810 26 1,657 Induced 14 5 22 247 185 252 1,148 35 1,909 Total 18 772 68 758 377 362 1,958 61 4,374 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-221 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Indiana Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-222 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 34 0 0 0 0 34 Indirect 1 6 11 190 37 19 93 5 362 Induced 5 1 4 82 34 39 149 6 320 Total 6 7 14 306 72 58 242 11 716 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 39 0 0 0 0 39 Indirect 2 8 16 265 52 26 130 7 506 Induced 7 2 6 118 47 54 210 9 454 Total 9 10 22 422 99 81 341 16 999 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 60 0 0 0 0 60 Indirect 2 10 19 326 63 34 164 9 626 Induced 9 2 7 144 57 67 259 11 556 Total 11 12 26 530 120 101 423 20 1,243 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Indiana Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 55 0 0 0 0 55 Indirect 2 9 20 328 61 33 167 9 629 Induced 8 2 7 151 56 67 263 11 567 Total 11 11 27 534 117 100 431 20 1,250 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 66 0 0 0 0 66 Indirect 2 10 21 359 65 36 181 9 684 Induced 9 2 7 166 60 73 283 12 611 Total 11 12 28 591 124 109 465 21 1,361 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 100 0 0 0 0 100 Indirect 3 12 26 446 81 48 233 12 861 Induced 10 2 9 210 74 93 359 15 773 Total 13 15 35 756 156 141 592 26 1,734 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-223 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Iowa Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-224 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 25 0 2 0 0 0 0 27 Indirect 2 2 6 49 17 10 45 3 133 Induced 8 0 2 29 16 22 80 4 161 Total 10 27 8 80 32 32 125 7 321 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 49 0 7 0 0 0 0 56 Indirect 3 2 9 72 27 15 70 4 203 Induced 12 0 3 43 24 34 119 6 241 Total 16 51 12 121 50 49 189 10 499 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 57 0 9 0 0 0 0 66 Indirect 4 3 11 88 34 18 87 6 251 Induced 15 0 4 52 29 41 145 7 293 Total 19 60 15 149 63 59 232 13 610 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Iowa Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 57 0 11 0 0 0 0 67 Indirect 4 2 13 93 35 18 92 6 263 Induced 16 0 4 54 31 41 150 7 303 Total 20 59 17 157 66 59 242 13 633 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 62 0 12 0 0 0 0 75 Indirect 5 2 14 105 40 19 101 6 292 Induced 17 0 4 59 35 44 162 7 329 Total 22 64 18 176 75 63 263 14 696 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 82 0 15 0 0 0 0 97 Indirect 6 2 18 136 52 24 129 7 376 Induced 23 0 6 75 46 55 205 9 420 Total 29 84 24 227 98 80 335 17 892 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-225 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Kansas Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-226 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 16 0 36 0 0 0 0 52 Indirect 1 12 7 31 20 10 56 5 142 Induced 4 2 2 21 15 22 83 4 153 Total 5 30 8 88 35 32 139 9 347 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 2 0 63 0 0 0 0 64 Indirect 1 16 8 47 31 16 81 7 207 Induced 6 3 2 32 22 30 117 6 219 Total 8 21 10 142 53 46 197 14 491 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 67 0 0 0 0 67 Indirect 2 18 9 58 38 19 98 9 250 Induced 8 4 3 39 27 36 141 7 265 Total 10 22 11 165 64 55 239 16 582 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Kansas Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 66 0 0 0 0 67 Indirect 2 18 9 63 38 19 100 8 257 Induced 8 4 3 42 27 37 144 8 273 Total 10 21 12 172 66 56 244 16 596 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 69 0 0 0 0 69 Indirect 2 18 9 75 41 20 110 9 283 Induced 9 4 3 47 30 39 157 8 297 Total 11 21 12 191 71 59 267 17 649 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 80 0 0 0 0 80 Indirect 3 22 11 99 52 24 140 11 362 Induced 12 4 4 62 38 48 200 10 377 Total 14 26 15 241 89 72 340 21 819 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-227 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Kentucky Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-228 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 139 13 16 13 0 4 0 186 Indirect 1 30 15 73 27 17 89 5 257 Induced 6 6 3 42 26 39 136 7 265 Total 7 175 31 132 66 55 230 12 708 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 170 14 19 8 0 3 0 214 Indirect 2 42 20 108 37 22 118 7 355 Induced 8 8 4 63 36 51 183 10 361 Total 10 220 37 189 81 73 304 17 930 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 157 14 33 9 0 3 0 216 Indirect 3 46 20 138 47 28 139 9 430 Induced 10 8 4 77 45 58 213 11 427 Total 13 211 39 248 101 86 355 21 1,073 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Kentucky Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 142 15 29 9 0 3 0 199 Indirect 3 41 20 146 49 27 136 9 431 Induced 11 8 4 80 48 57 210 11 429 Total 14 191 39 255 106 83 349 21 1,059 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 133 15 35 9 0 3 0 196 Indirect 3 42 20 167 55 29 142 10 469 Induced 12 8 4 88 53 59 220 12 458 Total 15 183 40 291 117 88 366 22 1,122 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 153 17 53 10 0 4 0 237 Indirect 4 50 25 216 71 37 174 13 590 Induced 15 9 6 111 67 73 272 16 570 Total 19 212 48 381 148 110 450 28 1,396 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-229 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Louisiana Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-230 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,587 766 202 115 0 70 0 2,740 Indirect 4 81 137 147 145 123 720 14 1,371 Induced 7 12 17 55 126 278 856 30 1,381 Total 12 1,680 920 403 386 401 1,645 44 5,492 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 3,422 789 333 124 0 56 0 4,723 Indirect 5 136 309 220 228 188 1,102 23 2,210 Induced 12 18 28 89 210 467 1,432 48 2,304 Total 17 3,576 1,126 642 562 655 2,589 71 9,238 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4,703 501 271 141 0 57 0 5,672 Indirect 5 171 417 238 264 203 1,269 27 2,594 Induced 14 22 33 107 250 559 1,706 58 2,749 Total 19 4,896 951 616 654 762 3,032 85 11,015 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Louisiana Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 5,641 491 247 144 0 58 0 6,581 Indirect 5 192 504 245 290 221 1,423 30 2,911 Induced 15 24 38 117 283 641 1,956 66 3,140 Total 21 5,857 1,033 609 717 862 3,438 96 12,632 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 5,932 414 267 147 0 60 0 6,820 Indirect 6 203 531 259 301 229 1,472 31 3,032 Induced 16 25 39 124 294 668 2,039 69 3,274 Total 21 6,160 984 651 742 897 3,571 100 13,126 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 7,562 422 267 191 0 78 0 8,519 Indirect 7 257 674 317 371 277 1,826 38 3,767 Induced 20 32 49 156 366 831 2,535 85 4,075 Total 26 7,850 1,145 740 929 1,109 4,439 124 16,361 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-231 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Maine Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-232 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 0 2 11 4 3 19 1 42 Induced 2 0 1 9 4 8 33 1 58 Total 3 0 3 20 9 11 52 3 100 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 0 3 16 6 4 28 2 60 Induced 3 0 1 12 6 12 47 2 83 Total 4 0 4 28 12 16 75 4 143 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 0 4 19 7 5 33 2 73 Induced 3 0 1 15 7 14 56 2 99 Total 5 0 5 35 13 19 90 4 172 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Maine Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 0 4 19 6 5 34 2 73 Induced 3 0 1 16 6 14 57 2 100 Total 5 0 5 35 13 19 90 4 173 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 1 5 21 7 5 36 2 78 Induced 3 0 1 17 6 15 61 3 106 Total 5 1 6 38 13 20 96 5 184 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 1 6 26 8 6 44 2 96 Induced 4 0 2 21 8 19 75 3 131 Total 6 1 7 47 16 25 119 6 227 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-233 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Maryland Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-234 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 2 14 31 20 12 127 5 211 Induced 1 0 5 19 23 30 163 7 249 Total 2 2 19 50 43 42 290 12 460 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 2 21 45 30 17 189 8 313 Induced 2 0 7 27 32 43 237 11 360 Total 3 3 28 73 62 60 427 19 674 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 4 26 55 37 21 232 10 385 Induced 3 0 9 33 38 52 290 13 438 Total 4 4 35 88 75 72 522 23 823 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Maryland Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 4 28 51 37 20 223 10 374 Induced 3 0 9 32 38 53 288 14 437 Total 4 4 37 83 75 73 511 24 811 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 4 30 51 41 22 231 11 392 Induced 3 1 10 33 41 57 305 14 464 Total 4 5 40 84 82 79 536 25 855 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 6 39 60 53 28 283 14 484 Induced 4 1 12 41 53 72 379 18 580 Total 6 7 52 101 105 99 662 32 1,064 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-235 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Massachusetts Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-236 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 12 0 0 0 0 12 Indirect 0 0 5 33 10 9 93 2 153 Induced 1 0 2 21 11 20 120 3 178 Total 1 0 7 67 21 29 212 6 343 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 17 0 0 0 0 17 Indirect 0 1 8 48 15 13 137 4 225 Induced 1 0 3 31 15 29 171 5 255 Total 2 1 10 97 29 42 308 8 498 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 31 0 0 0 0 31 Indirect 0 1 9 60 18 17 167 5 276 Induced 2 0 3 38 18 35 205 6 307 Total 2 1 12 129 35 51 372 10 614 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Massachusetts Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 28 0 0 0 0 28 Indirect 0 1 9 55 17 16 166 4 269 Induced 2 0 3 37 17 34 203 6 302 Total 2 1 13 121 34 50 369 10 599 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 35 0 0 0 0 35 Indirect 0 1 10 56 17 17 176 5 282 Induced 2 0 4 39 18 36 214 6 318 Total 2 1 13 130 35 53 390 11 634 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 54 0 0 0 0 54 Indirect 1 1 12 68 21 21 217 6 347 Induced 2 0 5 48 21 44 264 8 391 Total 3 1 17 169 42 65 481 13 791 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-237 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Michigan Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-238 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 135 0 406 0 0 0 0 541 Indirect 2 15 26 174 71 38 276 9 612 Induced 6 1 7 85 59 106 419 14 698 Total 8 152 33 665 130 144 695 23 1,851 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 99 0 585 0 0 0 0 684 Indirect 3 22 30 275 99 52 370 13 864 Induced 9 2 10 126 81 139 550 19 935 Total 12 122 40 986 180 191 920 32 2,483 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 63 0 776 0 0 0 0 839 Indirect 4 28 31 350 126 65 446 16 1,066 Induced 11 2 12 151 99 167 658 23 1,123 Total 14 93 43 1,276 225 232 1,104 39 3,028 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Michigan Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 40 0 727 0 0 0 0 767 Indirect 4 28 30 363 123 63 439 15 1,064 Induced 10 2 12 153 97 161 634 22 1,093 Total 14 70 42 1,243 220 224 1,073 38 2,924 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 28 0 820 0 0 0 0 849 Indirect 4 30 31 404 136 69 476 17 1,166 Induced 11 3 13 165 106 175 680 24 1,176 Total 15 61 43 1,388 242 244 1,156 41 3,190 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 33 0 1,104 0 0 0 0 1,136 Indirect 5 37 39 507 180 89 618 21 1,495 Induced 13 3 16 206 137 227 871 31 1,504 Total 18 73 55 1,817 317 315 1,489 52 4,135 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-239 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Minnesota Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-240 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 34 0 0 0 0 0 0 34 Indirect 2 12 8 80 25 17 129 5 277 Induced 7 1 3 48 24 38 179 6 305 Total 8 46 11 128 49 55 307 11 616 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 83 0 0 0 0 0 0 83 Indirect 3 17 11 119 39 26 193 7 415 Induced 10 1 4 74 36 59 271 10 465 Total 12 101 15 193 75 85 464 17 963 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 88 0 0 0 0 0 0 88 Indirect 3 20 13 146 48 32 232 9 504 Induced 11 1 5 91 43 70 324 12 557 Total 15 109 18 238 91 101 556 21 1,149 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Minnesota Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 75 0 0 0 0 0 0 75 Indirect 3 19 14 141 50 32 233 9 500 Induced 12 1 5 92 44 69 325 12 560 Total 15 95 19 233 93 101 558 21 1,136 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 70 0 0 0 0 0 0 70 Indirect 4 19 15 151 55 35 248 10 535 Induced 13 1 6 98 47 74 347 13 599 Total 17 91 20 249 102 108 595 22 1,204 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 80 0 0 0 0 0 0 80 Indirect 5 23 19 188 70 44 308 12 669 Induced 16 1 7 124 60 93 434 15 751 Total 21 105 26 313 130 137 742 28 1,500 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-241 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Mississippi Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-242 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 4 0 0 0 0 0 4 Indirect 2 6 4 31 16 5 30 3 95 Induced 4 1 1 21 17 14 46 4 107 Total 5 7 9 52 32 19 76 6 206 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 113 0 0 0 0 0 113 Indirect 3 9 6 48 29 14 70 5 184 Induced 6 2 2 32 29 29 94 6 201 Total 9 11 121 80 58 43 165 11 497 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 53 0 0 0 0 0 53 Indirect 3 10 7 57 33 12 66 5 192 Induced 7 2 2 39 34 28 96 7 215 Total 10 12 62 96 66 40 161 12 460 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Mississippi Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 31 0 0 0 0 0 31 Indirect 3 10 7 54 32 10 62 5 184 Induced 7 2 2 40 34 27 93 7 211 Total 10 12 41 94 66 37 155 12 426 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 28 0 0 0 0 0 28 Indirect 3 10 7 56 35 11 66 5 194 Induced 8 2 2 41 36 28 100 7 225 Total 11 12 38 97 71 39 166 13 446 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 25 0 0 0 0 0 25 Indirect 4 12 9 65 43 12 81 7 233 Induced 10 2 3 49 45 34 125 9 276 Total 14 14 37 114 88 46 206 15 534 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-243 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Missouri Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-244 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 31 0 226 0 0 0 0 258 Indirect 1 2 6 38 29 16 111 5 209 Induced 3 0 3 23 21 40 159 7 257 Total 4 34 9 288 50 57 269 13 724 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 50 0 329 0 0 0 0 379 Indirect 1 3 9 57 43 24 158 8 304 Induced 5 0 4 35 30 58 224 10 367 Total 6 54 13 421 73 82 383 18 1,049 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 64 0 418 0 0 0 0 482 Indirect 1 4 12 70 53 30 197 10 377 Induced 6 1 5 42 37 72 275 13 451 Total 8 68 17 530 90 102 472 23 1,310 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Missouri Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 60 0 428 0 0 0 0 488 Indirect 1 4 12 72 53 30 199 10 381 Induced 6 0 5 43 37 73 277 13 455 Total 8 64 17 543 90 102 476 23 1,323 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 64 0 476 0 0 0 0 540 Indirect 2 4 13 81 58 32 216 11 416 Induced 7 1 5 47 40 79 299 14 492 Total 8 69 18 603 98 111 515 25 1,448 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 82 0 586 0 0 0 0 668 Indirect 2 5 16 103 71 40 267 14 518 Induced 9 1 7 58 50 98 369 17 609 Total 11 87 23 746 121 138 636 31 1,794 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-245 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Montana Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-246 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 13 0 0 0 0 0 0 13 Indirect 1 9 3 5 7 2 15 1 43 Induced 2 1 1 3 7 7 26 1 49 Total 3 23 3 8 14 9 42 2 104 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 12 0 0 0 0 0 0 12 Indirect 1 16 3 7 11 3 21 2 64 Induced 3 2 1 5 10 9 37 2 70 Total 4 30 4 12 21 13 59 4 146 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 10 0 0 0 0 0 0 11 Indirect 1 19 3 8 13 4 26 2 77 Induced 4 3 1 6 12 11 45 2 85 Total 6 32 4 14 25 15 72 4 173 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Montana Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 9 0 0 0 0 0 0 10 Indirect 1 19 3 8 12 4 27 2 78 Induced 5 3 1 6 12 11 46 3 87 Total 6 32 4 15 24 15 74 4 174 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 8 0 0 0 0 0 0 8 Indirect 1 21 3 9 13 4 29 2 83 Induced 5 3 1 7 12 12 50 3 93 Total 7 32 4 16 25 17 79 5 184 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 8 0 0 0 0 0 0 9 Indirect 2 28 4 11 16 5 36 3 105 Induced 7 4 1 8 15 15 62 3 117 Total 9 40 5 20 31 21 99 6 230 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-247 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Nebraska Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-248 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 5 0 0 0 0 5 Indirect 1 1 4 17 25 7 39 2 95 Induced 4 0 1 14 16 13 56 3 107 Total 5 1 5 35 40 20 96 5 207 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 13 0 0 0 0 13 Indirect 2 1 6 26 40 11 63 3 152 Induced 6 0 2 21 25 20 87 4 164 Total 8 1 8 60 64 31 150 7 329 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 16 0 0 0 0 16 Indirect 2 2 7 33 50 14 84 4 195 Induced 8 0 2 26 30 24 108 5 203 Total 10 2 9 75 80 38 192 9 415 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Nebraska Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 18 0 0 0 0 18 Indirect 2 2 8 36 49 14 90 4 205 Induced 8 0 2 27 31 25 112 5 210 Total 11 2 10 81 80 39 203 9 433 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 20 0 0 0 0 20 Indirect 2 2 8 42 52 15 102 5 229 Induced 9 0 2 29 32 26 122 5 227 Total 12 2 11 91 85 42 224 10 476 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 25 0 0 0 0 25 Indirect 3 2 11 56 65 19 133 6 295 Induced 11 0 3 37 40 33 154 6 286 Total 14 2 14 119 106 52 287 12 606 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-249 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Nevada Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-250 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 38 1 0 0 0 0 38 Indirect 0 6 2 5 4 3 26 1 47 Induced 0 0 1 2 5 7 31 1 49 Total 0 7 41 7 10 11 57 2 133 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 1 0 0 0 0 1 Indirect 0 8 2 5 5 2 27 1 50 Induced 0 1 1 3 5 6 33 1 50 Total 0 9 2 9 11 8 59 2 101 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 6 1 0 0 0 0 7 Indirect 0 11 2 6 7 3 35 1 65 Induced 0 1 1 4 7 8 43 1 66 Total 0 12 9 11 14 11 79 2 138 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Nevada Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 1 0 0 0 0 1 Indirect 0 11 2 5 8 3 35 1 65 Induced 0 1 1 4 8 8 44 1 66 Total 0 12 3 10 15 11 79 2 132 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 1 0 0 0 0 1 Indirect 0 12 2 6 9 3 39 1 71 Induced 0 1 1 4 9 9 49 2 74 Total 0 13 3 11 17 12 88 3 146 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 1 0 0 0 0 1 Indirect 0 14 2 7 11 4 50 2 91 Induced 0 1 1 5 11 12 63 2 96 Total 1 16 3 13 23 16 113 4 189 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-251 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New Hampshire Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-252 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 1 8 1 1 8 0 20 Induced 0 0 0 3 1 3 13 0 21 Total 0 0 1 11 3 5 21 1 41 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 1 10 2 2 12 1 28 Induced 0 0 0 4 2 5 19 1 31 Total 0 0 1 14 4 7 31 1 59 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 1 12 2 3 16 1 35 Induced 0 0 0 5 2 6 23 1 38 Total 1 0 2 17 4 9 39 2 73 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New Hampshire Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 1 12 2 3 16 1 35 Induced 0 0 0 5 2 6 23 1 38 Total 1 0 2 17 4 9 39 2 73 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 1 12 2 3 17 1 37 Induced 0 0 0 5 2 7 25 1 41 Total 1 0 2 17 5 10 42 2 78 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 2 15 3 4 21 1 47 Induced 0 0 1 6 3 9 32 1 52 Total 1 0 2 21 6 13 53 2 99 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-253 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New Jersey Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-254 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 10 52 0 0 0 0 62 Indirect 0 1 6 35 19 17 116 4 198 Induced 1 0 2 31 19 31 147 5 237 Total 1 1 18 118 38 49 263 9 497 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 54 0 0 0 0 54 Indirect 0 1 9 45 27 24 167 5 278 Induced 1 0 3 42 28 44 206 7 330 Total 2 1 12 141 55 67 373 12 662 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 78 0 0 0 0 78 Indirect 0 1 11 52 33 29 205 7 339 Induced 2 0 4 51 34 54 247 8 400 Total 2 1 15 181 67 83 452 15 817 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New Jersey Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 69 0 0 0 0 69 Indirect 0 1 12 46 34 28 208 6 335 Induced 2 0 4 50 35 54 247 8 400 Total 2 1 15 166 69 81 454 15 804 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 82 0 0 0 0 82 Indirect 1 1 11 46 37 30 222 7 355 Induced 2 0 4 53 38 58 261 9 425 Total 2 1 15 181 75 87 483 16 861 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 123 0 0 0 0 123 Indirect 1 1 13 55 47 38 279 9 443 Induced 2 0 4 66 48 74 325 11 531 Total 3 1 17 243 95 112 605 20 1,097 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-255 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New Mexico Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-256 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 710 24 45 3 0 3 0 785 Indirect 0 26 60 11 32 24 154 8 314 Induced 2 5 5 8 30 72 228 13 362 Total 3 740 89 64 64 95 385 20 1,461 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 633 5 67 3 0 1 0 709 Indirect 0 38 55 15 35 26 157 9 335 Induced 3 7 5 10 30 70 226 13 363 Total 3 678 65 92 69 95 384 21 1,407 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 472 5 75 3 0 1 0 556 Indirect 1 45 43 18 35 25 151 9 324 Induced 3 9 4 11 28 61 206 12 334 Total 4 526 53 103 65 86 357 21 1,215 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New Mexico Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 394 20 82 3 0 1 0 500 Indirect 1 46 37 16 34 25 147 9 315 Induced 3 9 4 11 26 58 196 12 318 Total 4 449 62 109 63 83 344 20 1,134 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 356 6 85 3 0 1 0 451 Indirect 1 50 35 16 34 25 145 9 315 Induced 3 10 4 12 25 55 192 11 313 Total 4 416 45 113 62 80 338 20 1,079 Induced 4 13 5 15 30 66 229 14 376 Total 5 489 53 134 74 95 404 24 1,277 2035 Direct Indirect Agriculture 0 1 Mining 410 65 Construction 6 41 Manufacturing 100 19 Transportation and Utilities 4 40 Retail And WholesaleTrade 0 29 Services 1 173 Government 0 11 Total 522 379 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-257 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New York Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-258 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 10 3 26 0 0 0 0 39 Indirect 1 6 30 121 61 47 522 17 806 Induced 4 1 11 80 66 105 737 22 1,026 Total 6 17 43 227 127 152 1,259 39 1,871 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 6 0 28 0 0 0 0 35 Indirect 2 8 35 173 88 69 787 25 1,186 Induced 7 1 14 114 94 151 1,078 32 1,490 Total 9 16 49 316 181 220 1,864 56 2,710 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4 1 42 0 0 0 0 47 Indirect 3 11 37 209 100 84 948 31 1,423 Induced 8 1 16 136 106 184 1,283 38 1,772 Total 10 16 55 386 206 269 2,231 69 3,242 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES New York Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 2 0 38 0 0 0 0 40 Indirect 3 11 36 194 92 83 944 30 1,393 Induced 8 2 16 133 99 184 1,275 38 1,754 Total 11 15 52 365 191 267 2,219 68 3,187 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 2 0 45 0 0 0 0 47 Indirect 3 11 34 200 94 89 988 32 1,453 Induced 9 2 16 139 100 196 1,327 41 1,829 Total 12 15 50 385 194 285 2,315 73 3,328 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 2 0 69 0 0 0 0 71 Indirect 4 14 40 242 111 113 1,208 40 1,772 Induced 11 2 19 171 118 245 1,616 50 2,233 Total 15 18 59 482 229 358 2,825 90 4,075 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-259 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES North Carolina Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-260 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 4 0 0 0 0 0 4 Indirect 2 3 16 101 27 22 156 8 335 Induced 5 0 5 82 29 51 209 10 391 Total 7 3 26 182 55 74 365 18 731 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 4 23 144 38 33 233 11 490 Induced 7 1 7 119 39 75 308 15 571 Total 10 5 31 263 77 108 541 26 1,061 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 8 0 0 0 0 0 8 Indirect 3 5 29 179 46 41 292 15 610 Induced 9 1 9 143 47 93 388 18 708 Total 12 6 47 322 93 134 680 33 1,326 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES North Carolina Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 5 32 168 43 41 298 15 605 Induced 9 1 10 141 46 93 400 19 717 Total 12 5 42 309 89 134 698 34 1,323 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 5 35 173 45 44 325 16 647 Induced 9 1 11 146 48 100 440 21 776 Total 13 6 46 319 94 145 765 37 1,424 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 4 7 46 204 55 54 409 21 800 Induced 13 1 15 177 59 125 560 26 975 Total 17 8 60 380 115 179 969 47 1,775 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-261 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES North Dakota Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-262 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 13 2 5 6 3 11 1 41 Induced 3 3 1 3 5 6 18 1 39 Total 3 16 2 8 10 8 30 2 79 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 33 3 8 9 4 18 1 77 Induced 4 7 1 5 8 9 27 2 62 Total 5 40 4 12 17 13 45 3 138 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 45 3 10 11 5 23 2 101 Induced 5 10 1 6 9 11 35 2 78 Total 6 54 4 17 20 16 58 4 179 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES North Dakota Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 50 3 11 11 5 25 2 109 Induced 5 11 1 7 9 11 37 2 83 Total 6 61 5 18 21 16 62 4 192 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 56 4 12 12 5 29 2 122 Induced 5 12 1 8 10 12 42 2 93 Total 7 69 5 21 22 17 71 4 215 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 76 5 16 15 7 38 2 160 Induced 7 16 2 11 12 15 56 3 122 Total 8 92 6 27 28 22 94 5 282 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-263 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Ohio Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-264 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 51 0 322 0 0 0 0 372 Indirect 2 17 21 307 92 81 342 11 873 Induced 6 3 7 115 75 113 451 16 786 Total 8 70 28 744 167 194 792 27 2,031 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 55 0 378 0 0 0 0 434 Indirect 2 24 28 431 129 103 456 16 1,189 Induced 9 4 10 164 106 148 599 21 1,061 Total 11 83 38 973 235 251 1,055 37 2,684 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 78 0 582 0 0 0 0 660 Indirect 3 30 34 552 177 146 599 21 1,563 Induced 11 6 13 205 138 194 773 27 1,367 Total 14 114 47 1,340 315 340 1,372 48 3,590 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Ohio Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 69 0 527 0 0 0 0 596 Indirect 3 31 35 556 170 136 575 21 1,526 Induced 11 6 12 213 137 186 747 27 1,338 Total 14 105 47 1,296 306 322 1,322 47 3,460 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 81 0 626 0 0 0 0 708 Indirect 3 33 38 623 190 155 630 23 1,694 Induced 11 6 14 235 151 205 814 29 1,466 Total 15 120 51 1,484 342 360 1,443 52 3,867 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 125 0 934 0 0 0 0 1,059 Indirect 4 42 49 814 255 214 831 30 2,240 Induced 14 8 18 305 198 275 1,070 38 1,927 Total 18 175 67 2,054 453 489 1,901 68 5,225 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-265 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Oklahoma Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-266 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 515 126 221 23 0 19 0 903 Indirect 1 81 28 78 74 49 240 11 563 Induced 5 17 5 26 50 95 313 15 527 Total 6 613 159 326 147 144 572 26 1,993 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 766 115 357 70 0 29 0 1,338 Indirect 2 115 42 118 115 76 365 17 850 Induced 7 24 7 39 73 140 460 22 774 Total 9 906 164 515 258 216 854 39 2,961 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 895 128 450 82 0 30 0 1,585 Indirect 2 133 46 142 140 93 438 21 1,015 Induced 9 28 8 47 88 167 548 26 922 Total 11 1,056 183 639 309 260 1,016 47 3,522 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Oklahoma Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 955 143 444 85 0 32 0 1,659 Indirect 2 136 49 141 142 93 452 21 1,037 Induced 9 28 9 48 90 173 569 27 954 Total 11 1,119 201 633 317 266 1,053 49 3,649 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,019 159 482 96 0 36 0 1,791 Indirect 2 146 52 153 152 100 490 23 1,118 Induced 10 30 9 52 97 186 614 29 1,028 Total 12 1,195 220 688 345 286 1,139 52 3,937 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,275 198 582 120 0 45 0 2,219 Indirect 3 185 64 191 187 123 607 29 1,389 Induced 13 39 11 65 120 231 762 36 1,276 Total 15 1,499 273 838 427 353 1,414 65 4,885 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-267 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Oregon Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-268 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 24 15 0 0 0 0 39 Indirect 3 2 7 56 16 14 77 4 179 Induced 6 0 2 26 15 26 106 5 188 Total 10 2 33 97 31 41 183 10 406 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 16 0 0 0 0 16 Indirect 4 3 10 82 22 19 104 6 251 Induced 9 0 3 39 21 34 143 7 257 Total 14 3 14 138 43 53 248 13 524 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 20 0 0 0 0 20 Indirect 5 4 13 104 28 23 132 7 317 Induced 11 0 4 48 25 42 178 8 318 Total 17 5 17 172 53 65 310 16 654 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Oregon Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 15 0 0 0 0 15 Indirect 5 5 13 101 27 22 134 7 314 Induced 11 1 4 49 25 42 181 8 322 Total 16 6 18 164 52 64 315 15 651 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 12 0 0 0 0 12 Indirect 5 6 14 105 28 23 143 7 331 Induced 12 1 5 51 27 45 195 9 344 Total 17 7 19 169 55 68 338 16 688 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 13 0 0 0 0 13 Indirect 6 8 18 127 35 28 179 9 410 Induced 15 1 6 64 34 57 246 11 433 Total 21 9 24 203 69 85 424 20 856 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-269 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Pennsylvania Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-270 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 601 292 156 115 0 46 0 1,210 Indirect 3 45 70 286 135 103 668 16 1,326 Induced 8 8 16 126 117 217 920 28 1,439 Total 11 654 378 567 367 320 1,634 45 3,975 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 2,293 303 169 149 0 67 0 2,981 Indirect 4 106 218 433 243 175 1,317 30 2,526 Induced 14 17 30 209 229 450 1,838 57 2,844 Total 18 2,416 552 811 621 626 3,222 87 8,351 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 3,521 453 289 233 0 93 0 4,590 Indirect 6 137 316 572 356 267 1,956 44 3,654 Induced 20 21 43 273 329 663 2,660 83 4,093 Total 25 3,680 813 1,134 918 930 4,709 127 12,336 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Pennsylvania Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 3,822 413 265 207 0 83 0 4,791 Indirect 5 141 349 546 357 262 1,975 44 3,679 Induced 20 21 44 276 339 683 2,734 86 4,204 Total 26 3,984 807 1,087 903 945 4,792 130 12,674 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 4,283 501 315 253 0 102 0 5,453 Indirect 6 152 384 596 403 302 2,238 50 4,130 Induced 22 23 49 301 380 771 3,062 97 4,706 Total 29 4,458 935 1,211 1,036 1,072 5,401 147 14,289 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 6,174 779 462 393 0 158 0 7,966 Indirect 8 203 539 776 569 433 3,178 70 5,777 Induced 30 30 69 402 536 1,097 4,304 137 6,606 Total 39 6,408 1,388 1,640 1,498 1,531 7,640 207 20,349 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-271 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Rhode Island Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-272 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 1 13 3 2 20 1 40 Induced 0 0 1 6 2 5 32 1 47 Total 1 0 2 18 5 7 52 2 87 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 2 19 4 3 29 1 58 Induced 1 0 1 8 3 8 45 1 67 Total 1 0 3 27 7 11 74 2 125 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 2 23 4 4 35 1 69 Induced 1 0 1 10 4 9 53 2 79 Total 1 0 3 32 8 13 88 3 148 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Rhode Island Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 2 21 4 4 35 1 67 Induced 1 0 1 9 4 9 53 2 79 Total 1 0 3 31 8 13 88 3 146 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 2 21 4 4 36 1 69 Induced 1 0 1 10 4 9 56 2 83 Total 1 0 3 31 8 14 93 3 152 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 0 2 25 5 5 44 1 83 Induced 1 0 1 12 5 11 69 2 101 Total 1 1 3 37 9 16 113 3 184 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-273 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES South Carolina Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-274 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 3 0 0 0 0 0 3 Indirect 2 1 7 73 16 9 61 4 172 Induced 3 0 2 37 16 24 91 5 178 Total 4 1 12 111 32 33 152 9 353 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 2 11 110 24 14 90 5 257 Induced 4 0 3 56 23 35 134 7 263 Total 6 2 13 166 47 49 224 12 521 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 4 0 0 0 0 0 4 Indirect 3 3 13 136 29 18 114 7 323 Induced 5 0 4 69 28 43 169 9 327 Total 7 3 21 206 58 61 283 16 654 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES South Carolina Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 1 0 0 0 0 0 1 Indirect 2 3 14 139 29 17 117 7 329 Induced 5 0 4 73 28 43 173 9 335 Total 7 3 18 212 57 60 291 16 665 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 1 1 0 0 0 0 2 Indirect 2 3 15 155 31 19 130 8 362 Induced 5 0 4 81 30 46 190 10 367 Total 7 4 20 236 61 65 320 17 731 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 1 0 0 0 0 1 Indirect 3 4 19 195 38 23 165 9 457 Induced 6 1 5 104 38 57 241 12 463 Total 9 5 24 300 76 81 405 21 921 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-275 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES South Dakota Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-276 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 1 2 8 4 3 12 1 30 Induced 2 0 1 5 4 6 22 1 40 Total 3 1 2 13 7 8 33 2 70 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 1 2 12 6 4 17 1 44 Induced 4 0 1 7 5 9 32 2 60 Total 5 1 3 19 11 13 50 3 104 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 1 2 14 7 5 21 2 54 Induced 5 0 1 9 6 11 39 2 73 Total 6 2 3 23 14 15 60 4 127 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES South Dakota Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 1 2 13 8 5 22 2 54 Induced 5 0 1 9 7 11 40 2 75 Total 6 2 3 23 14 15 62 4 129 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 1 2 14 8 5 24 2 58 Induced 5 0 1 10 8 11 43 2 80 Total 7 2 3 24 16 16 67 4 139 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 2 3 17 11 6 30 2 72 Induced 7 0 1 12 10 14 53 3 100 Total 9 2 4 29 20 20 83 5 173 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-277 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Tennessee Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-278 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 7 0 0 0 0 7 Indirect 1 4 10 83 33 17 94 5 246 Induced 4 1 3 53 37 37 143 6 284 Total 5 4 12 143 70 54 237 11 537 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 3 0 0 0 0 3 Indirect 1 5 14 125 48 24 139 7 364 Induced 6 1 4 81 54 52 207 9 414 Total 8 6 19 209 102 76 346 16 782 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 8 0 0 0 0 8 Indirect 2 7 18 157 58 30 175 9 456 Induced 8 1 5 102 64 64 257 11 513 Total 10 8 23 267 122 95 432 20 977 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Tennessee Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 5 0 0 0 0 5 Indirect 2 7 19 161 57 30 181 9 467 Induced 8 1 6 108 63 65 264 11 526 Total 10 8 24 275 121 95 445 21 998 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 5 0 0 0 0 5 Indirect 2 7 20 181 61 32 197 10 512 Induced 9 1 6 120 67 70 286 12 571 Total 11 9 26 307 128 102 483 22 1,089 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 5 0 0 0 0 5 Indirect 3 9 26 231 76 40 249 12 646 Induced 11 1 8 154 83 87 359 15 720 Total 14 11 34 390 160 127 608 28 1,371 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-279 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Texas Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-280 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 5,749 1,294 1,860 306 0 168 0 9,377 Indirect 9 578 358 910 873 648 3,097 64 6,538 Induced 41 135 71 406 687 1,283 4,194 108 6,925 Total 50 6,463 1,723 3,176 1,866 1,931 7,459 172 22,840 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 8,049 1,020 2,677 505 0 235 0 12,486 Indirect 12 809 470 1,257 1,242 894 4,218 91 8,993 Induced 56 189 95 554 928 1,713 5,611 145 9,291 Total 67 9,046 1,584 4,488 2,676 2,607 10,065 237 30,769 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 9,962 1,335 3,543 705 0 295 0 15,840 Indirect 15 965 549 1,626 1,608 1,186 5,494 120 11,562 Induced 69 232 120 695 1,179 2,181 7,127 187 11,790 Total 84 11,159 2,004 5,864 3,492 3,367 12,915 307 39,192 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Texas Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 10,427 1,405 3,500 704 0 295 0 16,331 Indirect 15 1,004 584 1,618 1,638 1,195 5,643 124 11,822 Induced 71 235 124 709 1,211 2,243 7,345 194 12,132 Total 86 11,666 2,114 5,827 3,553 3,439 13,283 318 40,285 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 11,060 1,599 3,825 794 0 333 0 17,610 Indirect 16 1,062 615 1,765 1,781 1,308 6,156 137 12,840 Induced 76 252 135 762 1,311 2,431 7,964 212 13,144 Total 92 12,374 2,348 6,352 3,886 3,740 14,454 348 43,594 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 13,545 1,900 4,695 962 0 404 0 21,507 Indirect 20 1,319 759 2,177 2,187 1,602 7,555 170 15,788 Induced 94 312 167 938 1,610 2,981 9,769 262 16,133 Total 114 15,176 2,826 7,810 4,759 4,583 17,727 432 53,427 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-281 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Utah Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-282 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 259 233 97 72 0 28 0 689 Indirect 0 16 25 55 60 45 294 5 501 Induced 2 2 6 33 48 94 326 8 520 Total 2 278 264 185 180 139 648 14 1,710 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 379 164 127 91 0 37 0 799 Indirect 1 23 32 73 78 54 380 7 648 Induced 3 3 8 46 61 115 405 11 651 Total 3 406 204 246 230 169 823 18 2,098 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 454 166 138 97 0 36 0 889 Indirect 1 28 36 88 89 61 440 9 752 Induced 4 4 9 55 70 130 465 13 750 Total 4 486 210 281 255 192 941 22 2,391 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Utah Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 486 180 137 100 0 37 0 939 Indirect 1 29 39 87 93 64 461 9 782 Induced 4 4 9 57 72 137 492 13 788 Total 4 518 228 281 265 200 990 23 2,509 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 504 183 141 102 0 38 0 968 Indirect 1 31 40 92 97 67 484 10 822 Induced 4 4 10 60 76 143 521 14 832 Total 5 540 233 293 275 210 1,042 25 2,623 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 540 197 162 110 0 41 0 1,050 Indirect 1 38 45 109 112 76 551 12 944 Induced 5 5 11 73 87 162 598 17 958 Total 6 583 253 344 309 238 1,190 29 2,952 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-283 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Vermont Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-284 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 1 1 8 3 1 9 1 23 Induced 1 0 0 5 3 4 17 1 31 Total 1 1 2 13 5 5 26 1 54 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 0 1 2 11 4 2 14 1 35 Induced 1 0 1 8 4 6 25 1 46 Total 2 1 2 19 8 8 40 2 81 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 1 2 13 5 2 18 1 42 Induced 2 0 1 10 5 7 31 1 56 Total 2 1 3 23 10 10 49 2 99 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Vermont Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 1 2 11 5 2 18 1 41 Induced 2 0 1 10 5 7 31 1 56 Total 2 1 3 21 10 9 49 2 97 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 1 2 11 5 3 19 1 42 Induced 2 0 1 10 5 7 32 1 59 Total 2 1 3 21 10 10 51 3 101 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 1 1 3 13 6 3 23 1 51 Induced 2 0 1 12 6 9 40 2 72 Total 3 1 4 25 12 12 63 3 122 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-285 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Virginia Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-286 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 45 9 23 3 0 1 0 81 Indirect 1 12 22 59 39 20 243 9 405 Induced 4 2 6 39 35 51 256 11 403 Total 5 58 37 121 77 71 500 20 889 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 41 4 25 2 0 1 0 73 Indirect 2 15 28 83 52 27 341 12 560 Induced 5 2 8 56 46 69 355 16 558 Total 7 59 40 164 100 96 697 28 1,191 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 36 4 37 2 0 1 0 80 Indirect 2 19 31 104 65 32 430 15 699 Induced 7 3 10 70 55 84 437 19 686 Total 9 57 45 211 123 117 868 35 1,465 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Virginia Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 31 4 34 2 0 1 0 73 Indirect 2 19 32 102 63 31 443 15 707 Induced 7 3 10 71 55 85 447 19 698 Total 9 53 45 207 120 117 892 35 1,478 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 29 4 41 2 0 1 0 78 Indirect 3 19 33 107 69 35 493 17 776 Induced 8 3 10 75 59 94 493 21 762 Total 10 52 48 223 129 128 988 38 1,616 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 34 5 63 2 0 1 0 105 Indirect 3 24 42 128 91 45 650 22 1,004 Induced 9 4 13 90 76 120 639 26 977 Total 12 61 59 281 169 165 1,291 48 2,086 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-287 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Washington Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-288 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 1 6 22 10 8 57 3 110 Induced 4 0 2 15 12 18 77 4 133 Total 6 1 9 37 22 26 134 7 243 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 2 1 9 28 16 12 89 4 163 Induced 7 0 3 20 18 27 115 6 197 Total 9 1 13 49 34 40 204 10 360 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 2 11 35 20 15 111 6 202 Induced 9 0 4 25 22 33 142 7 242 Total 12 2 15 60 42 48 252 13 444 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Washington Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 2 11 38 20 15 112 6 207 Induced 9 0 4 27 23 33 143 7 246 Total 12 2 15 65 43 48 255 13 454 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 3 3 12 44 22 16 120 6 225 Induced 9 0 4 31 25 35 152 8 264 Total 13 3 16 75 47 51 272 14 490 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 0 0 0 0 0 0 0 0 Indirect 4 4 14 59 27 20 150 7 286 Induced 12 0 5 41 31 43 190 10 332 Total 16 4 20 100 59 63 339 17 617 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-289 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES West Virginia Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-290 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 362 91 30 54 0 20 0 556 Indirect 1 46 31 26 37 19 118 4 281 Induced 1 9 3 11 24 48 152 7 254 Total 2 416 124 67 114 67 290 11 1,091 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 899 110 34 59 0 24 0 1,126 Indirect 1 73 76 39 61 34 209 6 497 Induced 2 12 5 17 42 91 284 12 466 Total 3 984 191 89 161 125 517 19 2,088 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,260 156 50 87 0 32 0 1,585 Indirect 1 95 102 49 84 48 296 9 684 Induced 2 16 7 21 56 125 390 17 635 Total 3 1,371 265 120 227 173 719 26 2,904 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES West Virginia Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,332 149 45 79 0 29 0 1,634 Indirect 1 97 111 50 83 48 298 9 698 Induced 2 16 8 22 56 129 403 18 655 Total 3 1,445 267 118 219 177 730 26 2,986 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,463 176 55 94 0 35 0 1,823 Indirect 1 106 120 58 93 54 336 10 777 Induced 3 18 8 25 61 144 448 20 726 Total 4 1,587 304 137 248 198 819 29 3,326 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 2,065 265 85 142 0 52 0 2,609 Indirect 1 137 167 76 130 78 477 14 1,080 Induced 3 23 12 32 84 202 625 27 1,008 Total 5 2,224 443 193 356 279 1,155 41 4,697 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-291 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Wisconsin Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-292 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 8 0 4 0 0 0 0 12 Indirect 2 2 9 144 26 16 99 5 303 Induced 7 0 3 68 26 36 150 6 296 Total 8 10 11 216 53 52 249 11 611 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 20 0 5 0 0 0 0 25 Indirect 3 2 12 213 39 24 148 7 447 Induced 10 0 4 100 37 54 219 9 434 Total 12 23 16 318 76 78 367 16 906 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 22 0 7 0 0 0 0 29 Indirect 3 3 14 263 48 30 188 9 559 Induced 12 0 5 124 46 66 270 11 534 Total 16 25 19 393 95 96 458 20 1,122 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Wisconsin Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 25 0 6 0 0 0 0 31 Indirect 3 3 15 261 50 30 201 9 572 Induced 13 0 5 125 49 68 280 11 551 Total 16 28 19 392 100 98 481 20 1,154 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 28 0 8 0 0 0 0 35 Indirect 4 3 15 283 55 33 222 9 625 Induced 14 0 5 134 54 73 303 12 596 Total 18 31 20 424 109 107 525 21 1,256 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 35 0 12 0 0 0 0 47 Indirect 5 4 19 354 70 42 286 12 792 Induced 18 0 6 167 68 92 384 15 751 Total 23 39 25 533 138 135 670 27 1,590 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-293 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Wyoming Labor Income Contribution by State and Industry: Unconventional Gas* ($M) B-294 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,650 155 61 47 0 17 0 1,931 Indirect 0 35 128 6 55 34 163 6 428 Induced 1 5 6 4 40 96 228 14 394 Total 1 1,691 289 71 142 130 408 20 2,753 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 1,965 193 55 100 0 39 0 2,351 Indirect 0 45 152 8 78 48 240 9 580 Induced 2 10 11 7 75 180 428 25 738 Total 2 2,019 357 71 252 228 706 34 3,669 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 2,134 197 58 108 0 38 0 2,534 Indirect 0 52 162 10 85 53 264 10 637 Induced 2 11 13 8 82 195 464 28 804 Total 2 2,198 371 76 275 248 766 38 3,974 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Wyoming Labor Income Contribution by State and Industry: Unconventional Gas* (Continued) ($M) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 2,402 243 56 126 0 44 0 2,872 Indirect 0 55 181 10 95 60 302 11 715 Induced 2 12 14 9 92 221 525 31 907 Total 2 2,469 439 75 313 281 872 43 4,494 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 2,579 280 57 146 0 51 0 3,114 Indirect 0 59 192 11 103 66 334 13 778 Induced 2 13 15 10 101 241 572 34 988 Total 3 2,651 488 77 350 307 957 47 4,880 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 3,298 349 65 183 0 64 0 3,958 Indirect 1 75 246 13 129 83 422 16 986 Induced 3 16 20 13 128 306 725 43 1,252 Total 3 3,389 615 91 439 389 1,211 59 6,196 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS B-295 The Economic and Employment Contributions of Unconventional Gas Development in State Economies Appendix C. Economic Contributions Excluding Cross-State Contributions by State and Year Prepared for: AMERICA'S NATURAL GAS ALLIANCE Submitted by: IHS Inc. 1150 Connecticut Avenue NW, Suite 401 Washington, DC 20036 June 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES About IHS (ihs.com) IHS Inc. (NYSE: IHS) is a leading source of information and insight in critical areas that shape today's business landscape, including energy and power; design and supply chain; defense, risk and security; environmental, health and safety, and sustainability; country and industry forecasting; and commodities, pricing and cost. IHS has been in business since 1959 and became a publicly traded company on the New York Stock Exchange in 2005. Headquartered in Englewood, Colorado, USA, IHS employs more than 5,100 people in more than 30 countries around the world. About IHS Global Insight IHS Global Insightis one of the leading economic analysis and forecasting firms in the world. With over 600 economists, statisticians, and industry specialists in 25 offices worldwide, IHS Global Insight has an established track record for providing rigorous, objective forecast analysis and data to governments and businesses around the world. Among our areas of expertise are the economic impact, tax implications, and job-creation dynamics within multiple sectors core to national, state and local economies. It helps governments and companies at all levels interpret the impact of proposed investments, policies, programs, and projects. IHS Global Insight was formed by the merger of DRI and WEFA. Still active in an advisory capacity to the firm is the original founder of WEFA, Lawrence R. Klein, the 1980 winner of the Nobel Prize in Economics. For more information, contact: Richard F. Fullenbaum Vice President, Public Sector, IHS Richard.Fullenbaum@ihs.com John W. Larson Vice President, Public Sector, IHS John.Larson@ihs.com For press information, contact: Jim Dorsey Senior Manager Media Relations, IHS Jim.Dorsey@ihs.com IHS 1150 Connecticut Avenue NW, Suite 401 Washington, DC 20036 © 2012 IHS. All information contained herein is obtained by IHS Inc. from sources believed by it to be accurate and reliable. All forecasts and predictions contained herein are believed by IHS, Inc. to be as accurate as the data and methodologies will allow. However, because of the possibilities of human and mechanical error, as well as other factors such as unforeseen and unforeseeable changes in political and economic circumstances beyond IHS's control, the information herein is provided "as is" without warranty of any kind and IHS Inc., AND ALL THIRD PARTY PROVIDERS MAKE NO REPRESENTATIONS OR WARRANTIES EXPRESS OR IMPLIED TO ANY SUBSCRIBER OR ANY OTHER PERSON OR ENTITY AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY OF THE INFORMATION OR FORECASTS CONTAINED HEREIN. ii JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Appendix C. Economic Contributions Excluding Cross-State Contributions by State and Year Appendix C presents three different types of detailed tables by state in five-year increments over the forecast horizon (2010, 2015, 2020, 2025, 2030 and 2035). The tables presented in this appendix are similar in structure to the tables presented in Appendix A; however, these tables present the indirect and induced contributions generated by the direct activity in each state independent of all other states. In doing so, these tables present only the indirect and induced employment, value added, and labor income contributions attributed to supporting those directly employed by the industry's unconventional gas activity in the source state through production and/or capital expenditure. In other words, the indirect and induced contributions do not include leakages (cross-state contributions) in the supply chain from activities supported outside of the reported state. As a function of this methodology, all direct contributions remain unchanged from Appendix A and changes are only observed within the indirect and induced contributions. The results in this appendix are obtained directly from the IMPLAN model's single state runs. Results for the following three concepts are presented: 1) Employment Contribution 2) Value Added Contribution 3) Labor Income Contribution Each contribution table is split out into direct, indirect, induced and total contribution. Also included are state multipliers defined as (indirect contribution + induced contribution) / direct contribution For each concept, there is a separate table for each of our forecast years. A summary description of the tables is as follows: 1. Employment Contribution Excluding Cross-State Contributions: Alphabetical by State. These tables present the direct, indirect, induced, and total employment contributions for 2010, 2015, 2020, 2025, 2030, and 2035 alphabetically by state. 2. Value Added Contribution Excluding Cross-State Contributions: Alphabetical by State. These tables present the direct, indirect, induced, and total value added contributions for 2010, 2015, 2020, 2025, 2030, and 2035 alphabetically by state. 3. Labor Income Contribution Excluding Cross-State Contributions: Alphabetical by State. These tables present the direct, indirect, induced, and total value added contributions for 2010, 2015, 2020, 2025, 2030, and 2035 alphabetically by state. The tables present the indirect and induced contributions generated by the direct activity in each state independent of all other states’ activity—the indirect and induced contributions do not include leakages (cross-state contributions) in the supply chain from activities supported outside of the reported state. IHS C-1 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Employment Contribution Excluding Cross-State Contributions: Alphabetical by State US State-L Level Employment Contribution of Unconventional Gas* Excluding Cross-S State Contributions, 2010 (Number of workers) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming US Total Direct 1,195 0 13,640 4,718 22,535 0 187 0 3,204 952 0 2,814 516 315 658 2,145 29,896 0 0 136 6,968 352 92 4,133 90 104 505 0 592 6,797 408 102 0 4,979 8,636 670 13,594 0 61 0 142 73,744 10,404 0 923 0 6,871 137 14,753 Indirect 702 0 7,353 5,753 17,985 0 151 0 1,754 486 0 1,363 412 87 355 1,115 18,486 0 0 110 3,064 125 31 1,353 75 86 196 0 470 4,108 287 38 0 4,786 6,041 462 9,580 0 27 0 112 71,300 7,021 0 729 0 3,028 93 7,406 Induced 943 0 9,296 5,076 26,230 0 152 0 2,087 679 0 2,623 378 182 470 1,504 23,313 0 0 135 5,636 284 31 2,401 110 62 251 0 511 5,912 368 44 0 4,928 7,552 463 13,028 0 28 0 97 97,671 8,126 0 775 0 3,682 124 9,475 Total 2,839 0 30,289 15,547 66,750 0 490 0 7,044 2,117 0 6,800 1,306 584 1,484 4,764 71,694 0 0 380 15,668 762 153 7,887 275 252 952 0 1,573 16,816 1,063 184 0 14,693 22,229 1,595 36,201 0 116 0 351 242,714 25,551 0 2,428 0 13,581 354 31,635 237,968 176,528 234,626 649,122 State Multiplier 1.38 0.00 1.22 2.30 1.96 0.00 1.62 0.00 1.20 1.22 0.00 1.42 1.53 0.85 1.25 1.22 1.40 0.00 0.00 1.80 1.25 1.16 0.68 0.91 2.07 1.43 0.88 0.00 1.66 1.47 1.60 0.81 0.00 1.95 1.57 1.38 1.66 0.00 0.90 0.00 1.46 2.29 1.46 0.00 1.63 0.00 0.98 1.57 1.14 1.73 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight C-2 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Employment Contribution of Unconventional Gas* Excluding Cross-S State Contributions, 2015 (Number of workers) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming US Total Direct 2,042 0 19,767 6,970 40,115 0 236 0 6,838 1,106 0 3,724 586 650 824 2,336 40,341 0 0 193 9,107 860 2,703 6,005 85 276 10 0 465 6,017 386 0 0 5,776 12,217 185 26,007 0 3 0 62 93,838 11,232 0 777 0 12,857 263 18,917 Indirect 933 0 11,099 8,031 29,308 0 207 0 3,658 578 0 1,658 469 206 518 1,251 28,681 0 0 153 3,763 306 909 1,960 70 251 19 0 424 3,850 270 0 0 5,643 9,154 376 20,237 0 6 0 70 94,117 8,331 0 681 0 5,670 139 9,301 Induced 1,087 0 13,720 7,434 40,923 0 202 0 4,385 822 0 3,376 429 382 618 1,709 38,716 0 0 188 7,059 694 920 3,494 101 175 9 0 456 5,367 336 0 0 5,749 11,071 289 30,191 0 4 0 53 128,173 9,386 0 711 0 7,346 225 11,349 Total 4,063 0 44,586 22,435 110,347 0 645 0 14,882 2,506 0 8,758 1,484 1,239 1,960 5,296 107,738 0 0 534 19,929 1,860 4,532 11,460 256 702 38 0 1,345 15,234 992 0 0 17,168 32,442 850 76,436 0 13 0 185 316,129 28,948 0 2,169 0 25,873 626 39,567 333,779 252,299 337,148 923,226 State Multiplier 0.99 0.00 1.26 2.22 1.75 0.00 1.73 0.00 1.18 1.27 0.00 1.35 1.53 0.90 1.38 1.27 1.67 0.00 0.00 1.76 1.19 1.16 0.68 0.91 2.02 1.54 2.66 0.00 1.89 1.53 1.57 0.00 0.00 1.97 1.66 3.60 1.94 0.00 3.54 0.00 1.99 2.37 1.58 0.00 1.79 0.00 1.01 1.38 1.09 1.77 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS C-3 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Employment Contribution of Unconventional Gas* Excluding Cross-S State Contributions, 2020 (Number of workers) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 1,232 0 22,868 7,582 43,714 0 402 0 3,274 734 0 5,295 898 782 880 2,517 40,665 0 0 355 11,554 917 1,300 7,702 82 332 93 0 676 4,928 584 188 0 8,875 14,598 216 41,258 0 93 0 147 125,882 12,472 0 838 0 18,520 321 20,698 Indirect 569 0 13,063 9,246 31,791 0 371 0 1,862 363 0 2,277 714 256 559 1,444 33,514 0 0 274 4,647 327 437 2,512 65 318 50 0 614 3,251 380 70 0 8,844 11,120 467 32,426 0 42 0 125 124,485 9,467 0 803 0 8,217 187 10,221 Induced 657 0 15,983 8,467 44,012 0 356 0 2,189 498 0 4,728 655 461 659 1,802 46,838 0 0 337 8,759 740 442 4,484 92 218 50 0 663 4,336 461 82 0 8,909 13,363 356 47,602 0 43 0 105 166,567 10,632 0 815 0 10,493 280 12,415 Total 2,458 0 51,914 25,296 119,517 0 1,129 0 7,325 1,594 0 12,300 2,267 1,500 2,099 5,762 121,017 0 0 967 24,960 1,983 2,179 14,697 240 867 194 0 1,953 12,515 1,426 340 0 26,628 39,081 1,040 121,286 0 178 0 377 416,935 32,571 0 2,455 0 37,230 788 43,333 US Total 403,473 315,383 419,547 1,138,404 State Multiplier 1.00 0.00 1.27 2.34 1.73 0.00 1.81 0.00 1.24 1.17 0.00 1.32 1.52 0.92 1.38 1.29 1.98 0.00 0.00 1.72 1.16 1.16 0.68 0.91 1.93 1.61 1.08 0.00 1.89 1.54 1.44 0.81 0.00 2.00 1.68 3.82 1.94 0.00 0.91 0.00 1.57 2.31 1.61 0.00 1.93 0.00 1.01 1.45 1.09 1.82 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight C-4 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Employment Contribution of Unconventional Gas* Excluding Cross-S State Contributions, 2025 (Number of workers) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 628 0 23,720 7,247 37,733 0 363 0 1,084 220 0 4,918 820 798 874 2,345 44,245 0 0 324 10,680 778 765 7,843 74 364 12 0 602 4,794 512 0 0 8,048 15,245 163 41,140 0 22 0 91 127,899 13,054 0 772 0 18,748 333 23,700 Indirect 306 0 13,561 8,881 27,263 0 337 0 743 112 0 2,130 650 279 547 1,340 38,078 0 0 250 4,238 277 257 2,561 59 366 22 0 538 3,100 334 0 0 8,026 11,448 352 32,817 0 15 0 100 127,234 9,930 0 732 0 8,326 179 11,612 Induced 353 0 16,642 8,150 38,344 0 323 0 827 151 0 4,397 598 475 650 1,654 54,164 0 0 307 8,023 627 260 4,558 84 247 11 0 587 3,963 402 0 0 8,076 13,941 268 49,234 0 13 0 76 171,641 11,216 0 742 0 10,800 286 14,073 Total 1,287 0 53,922 24,278 103,340 0 1,023 0 2,653 482 0 11,445 2,068 1,552 2,071 5,340 136,487 0 0 881 22,942 1,682 1,282 14,962 217 977 46 0 1,728 11,857 1,248 0 0 24,150 40,633 783 123,191 0 50 0 267 426,774 34,201 0 2,246 0 37,874 797 49,385 US Total 400,958 317,000 426,163 1,144,121 State Multiplier 1.05 0.00 1.27 2.35 1.74 0.00 1.82 0.00 1.45 1.19 0.00 1.33 1.52 0.94 1.37 1.28 2.08 0.00 0.00 1.72 1.15 1.16 0.68 0.91 1.93 1.68 2.66 0.00 1.87 1.47 1.44 0.00 0.00 2.00 1.67 3.81 1.99 0.00 1.25 0.00 1.93 2.34 1.62 0.00 1.91 0.00 1.02 1.40 1.08 1.85 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS C-5 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Employment Contribution of Unconventional Gas* Excluding Cross-S State Contributions, 2030 (Number of workers) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 1,047 0 24,272 7,461 35,346 0 438 0 4,926 835 0 5,634 986 891 902 2,365 44,571 0 0 396 11,907 731 681 8,702 65 405 13 0 709 4,207 611 0 0 9,588 16,580 136 47,761 0 31 0 98 140,803 13,412 0 815 0 21,154 382 26,183 Indirect 450 0 13,873 9,180 25,122 0 410 0 2,742 428 0 2,399 781 316 569 1,388 39,351 0 0 305 4,708 260 229 2,842 52 418 24 0 629 2,880 394 0 0 9,464 12,361 295 37,885 0 19 0 104 138,443 10,225 0 810 0 9,392 210 12,708 Induced 483 0 16,990 8,435 35,724 0 391 0 3,245 600 0 5,014 719 532 674 1,654 56,238 0 0 375 8,904 590 232 5,055 73 280 12 0 690 3,618 471 0 0 9,565 15,060 225 56,408 0 17 0 80 185,984 11,587 0 811 0 12,089 330 15,314 Total 1,980 0 55,135 25,076 96,192 0 1,239 0 10,914 1,863 0 13,047 2,486 1,739 2,144 5,407 140,160 0 0 1,076 25,520 1,581 1,142 16,599 190 1,103 49 0 2,028 10,705 1,476 0 0 28,617 44,001 656 142,053 0 66 0 283 465,229 35,224 0 2,436 0 42,634 921 54,205 US Total 435,045 341,664 458,469 1,235,178 State Multiplier 0.89 0.00 1.27 2.36 1.72 0.00 1.83 0.00 1.22 1.23 0.00 1.32 1.52 0.95 1.38 1.29 2.14 0.00 0.00 1.72 1.14 1.16 0.68 0.91 1.93 1.72 2.66 0.00 1.86 1.54 1.42 0.00 0.00 1.98 1.65 3.81 1.97 0.00 1.17 0.00 1.89 2.30 1.63 0.00 1.99 0.00 1.02 1.41 1.07 1.84 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight C-6 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Employment Contribution of Unconventional Gas* Excluding Cross-S State Contributions, 2035 (Number of workers) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 401 0 28,524 8,617 39,723 0 673 0 990 113 0 7,879 1,503 1,150 1,035 2,879 53,428 0 0 615 15,951 822 614 10,746 69 498 17 0 1,063 4,822 927 0 0 14,378 20,537 142 70,734 0 6 0 89 170,896 14,640 0 1,069 0 30,390 506 32,953 Indirect 213 0 16,253 10,609 27,928 0 633 0 765 63 0 3,282 1,193 401 669 1,766 48,387 0 0 474 6,368 293 207 3,507 55 520 30 0 939 3,309 595 0 0 13,904 15,232 308 55,639 0 11 0 108 168,726 11,160 0 1,137 0 13,490 299 16,023 Induced 244 0 19,949 9,766 40,045 0 603 0 826 86 0 6,967 1,097 684 786 2,028 69,516 0 0 583 11,963 663 209 6,247 78 347 15 0 1,034 4,159 710 0 0 14,190 18,589 234 82,294 0 8 0 79 226,717 12,602 0 1,124 0 17,230 443 19,365 Total 857 0 64,726 28,992 107,696 0 1,910 0 2,581 262 0 18,128 3,793 2,235 2,490 6,673 171,331 0 0 1,673 34,282 1,779 1,030 20,501 201 1,364 62 0 3,036 12,290 2,232 0 0 42,473 54,358 684 208,666 0 25 0 275 566,339 38,402 0 3,331 0 61,109 1,248 68,340 US Total 539,398 424,496 571,480 1,535,374 State Multiplier 1.14 0.00 1.27 2.36 1.71 0.00 1.84 0.00 1.61 1.33 0.00 1.30 1.52 0.94 1.41 1.32 2.21 0.00 0.00 1.72 1.15 1.16 0.68 0.91 1.92 1.74 2.66 0.00 1.86 1.55 1.41 0.00 0.00 1.95 1.65 3.81 1.95 0.00 3.54 0.00 2.11 2.31 1.62 0.00 2.12 0.00 1.01 1.47 1.07 1.85 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS C-7 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Value Added Contribution Excluding Cross-State Contributions: Alphabetical by State US State-L Level Value Added Contribution of Unconventional Gas* Excluding Cross-S State Contributions, 2010 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 276 0 2,745 505 5,587 0 25 0 180 109 0 395 54 36 99 451 5,664 0 0 13 859 45 4 314 35 8 41 0 81 2,091 61 5 0 539 1,924 50 2,444 0 3 0 12 19,621 1,256 0 179 0 1,261 17 5,014 Indirect 72 0 643 630 2,059 0 16 0 146 46 0 182 34 9 36 98 1,732 0 0 13 345 15 2 127 7 7 17 0 57 330 40 3 0 439 588 42 1,086 0 2 0 9 9,249 550 0 100 0 263 8 722 Induced 65 0 608 446 2,134 0 11 0 164 49 0 237 24 12 30 102 1,614 0 0 12 406 23 2 159 7 4 21 0 47 397 36 3 0 328 508 33 1,068 0 2 0 7 8,079 530 0 63 0 241 9 695 Total 413 0 3,995 1,581 9,780 0 53 0 490 204 0 814 112 57 165 650 9,010 0 0 38 1,609 84 8 600 49 18 80 0 186 2,818 137 11 0 1,306 3,020 125 4,598 0 7 0 28 36,949 2,335 0 342 0 1,765 34 6,430 US Total 52,004 19,722 18,176 89,902 State Multiplier 0.50 0.00 0.46 2.13 0.75 0.00 1.11 0.00 1.72 0.88 0.00 1.06 1.06 0.57 0.67 0.44 0.59 0.00 0.00 1.95 0.87 0.84 1.00 0.91 0.41 1.39 0.92 0.00 1.28 0.35 1.24 1.29 0.00 1.42 0.57 1.51 0.88 0.00 1.14 0.00 1.33 0.88 0.86 0.00 0.91 0.00 0.40 1.00 0.28 0.73 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight C-8 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Value Added Contribution of Unconventional Gas* Excluding Cross-S State Contributions, 2015 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 243 0 4,068 751 7,777 0 32 0 387 136 0 523 62 75 105 519 11,039 0 0 18 977 112 119 461 32 21 2 0 73 1,898 50 0 0 620 2,922 23 7,063 0 1 0 5 26,463 1,527 0 165 0 2,751 34 5,953 Indirect 87 0 983 898 3,294 0 22 0 306 56 0 227 39 20 53 113 2,923 0 0 19 414 37 61 185 7 21 1 0 52 312 38 0 0 524 906 37 2,589 0 0 0 6 12,518 669 0 97 0 519 13 908 Induced 78 0 908 667 3,376 0 15 0 349 59 0 310 27 25 39 118 2,789 0 0 17 507 58 58 234 7 10 1 0 42 362 32 0 0 385 766 19 2,580 0 0 0 4 10,876 629 0 58 0 494 16 854 Total 408 0 5,959 2,315 14,447 0 70 0 1,042 251 0 1,059 128 120 197 749 16,752 0 0 54 1,898 207 239 880 45 51 4 0 167 2,572 120 0 0 1,528 4,594 79 12,232 0 1 0 15 49,857 2,824 0 321 0 3,764 63 7,716 US Total 77,007 28,953 26,770 132,730 State Multiplier 0.68 0.00 0.46 2.08 0.86 0.00 1.19 0.00 1.69 0.84 0.00 1.03 1.06 0.61 0.87 0.44 0.52 0.00 0.00 1.96 0.94 0.84 1.00 0.91 0.42 1.50 1.07 0.00 1.27 0.36 1.39 0.00 0.00 1.47 0.57 2.42 0.73 0.00 0.73 0.00 1.83 0.88 0.85 0.00 0.94 0.00 0.37 0.86 0.30 0.72 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS C-9 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Value Added Contribution of Unconventional Gas* Excluding Cross-S State Contributions, 2020 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 142 0 4,624 823 7,949 0 54 0 185 77 0 727 94 89 110 503 14,111 0 0 32 1,116 119 57 587 28 25 9 0 106 1,456 60 9 0 936 3,422 27 10,777 0 5 0 13 32,840 1,714 0 170 0 3,832 40 6,394 Indirect 51 0 1,144 1,019 3,485 0 40 0 156 35 0 309 58 25 57 126 3,439 0 0 34 501 39 29 236 6 26 4 0 74 259 52 5 0 816 1,079 45 4,051 0 3 0 11 15,993 745 0 113 0 736 17 979 Induced 46 0 1,043 745 3,553 0 27 0 171 37 0 430 41 30 41 121 3,321 0 0 30 621 61 28 298 6 13 4 0 60 287 44 6 0 592 906 24 3,993 0 3 0 7 13,874 698 0 65 0 695 19 919 Total 239 0 6,811 2,587 14,986 0 121 0 512 149 0 1,466 194 144 207 750 20,871 0 0 96 2,238 219 113 1,120 40 63 17 0 241 2,002 157 20 0 2,344 5,407 96 18,821 0 11 0 30 62,707 3,157 0 349 0 5,263 77 8,292 US Total 93,261 35,799 32,857 161,917 State Multiplier 0.68 0.00 0.47 2.14 0.89 0.00 1.24 0.00 1.76 0.92 0.00 1.02 1.06 0.62 0.89 0.49 0.48 0.00 0.00 1.96 1.01 0.84 1.00 0.91 0.43 1.56 0.96 0.00 1.26 0.37 1.59 1.29 0.00 1.50 0.58 2.51 0.75 0.00 1.13 0.00 1.43 0.91 0.84 0.00 1.05 0.00 0.37 0.91 0.30 0.74 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight C-10 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Value Added Contribution of Unconventional Gas* Excluding Cross-S State Contributions, 2025 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 79 0 4,850 785 6,932 0 49 0 65 23 0 677 86 91 107 457 16,678 0 0 29 996 101 33 594 26 27 2 0 94 1,263 51 0 0 846 3,606 21 11,507 0 2 0 8 34,194 1,821 0 154 0 4,011 42 7,211 Indirect 28 0 1,190 978 2,982 0 36 0 65 11 0 290 53 27 55 116 3,939 0 0 31 454 33 17 240 5 30 2 0 65 243 45 0 0 741 1,111 34 4,167 0 1 0 8 16,380 780 0 103 0 752 17 1,105 Induced 24 0 1,089 717 3,057 0 24 0 63 11 0 401 38 31 40 111 3,838 0 0 27 567 52 16 302 6 14 1 0 53 259 39 0 0 537 943 18 4,130 0 1 0 5 14,228 733 0 59 0 716 20 1,040 Total 130 0 7,129 2,480 12,971 0 109 0 192 45 0 1,368 177 148 203 684 24,455 0 0 87 2,017 186 67 1,136 37 71 5 0 213 1,766 135 0 0 2,124 5,660 73 19,804 0 4 0 21 64,802 3,334 0 316 0 5,479 79 9,355 US Total 97,518 36,135 33,211 166,863 State Multiplier 0.66 0.00 0.47 2.16 0.87 0.00 1.24 0.00 1.97 0.94 0.00 1.02 1.05 0.64 0.89 0.50 0.47 0.00 0.00 1.96 1.03 0.84 1.00 0.91 0.43 1.63 1.07 0.00 1.25 0.40 1.66 0.00 0.00 1.51 0.57 2.50 0.72 0.00 0.94 0.00 1.78 0.90 0.83 0.00 1.05 0.00 0.37 0.87 0.30 0.71 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS C-11 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Value Added Contribution of Unconventional Gas* Excluding Cross-S State Contributions, 2030 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming US Total Direct 84 0 4,900 804 6,360 0 59 0 277 97 0 772 104 101 111 441 17,429 0 0 36 1,079 95 30 657 22 30 2 0 111 1,146 57 0 0 1,002 3,872 17 12,973 0 3 0 8 36,540 1,885 0 161 0 4,434 48 7,758 Indirect 37 0 1,214 1,008 2,731 0 44 0 228 41 0 327 64 30 58 119 4,075 0 0 37 503 31 15 265 5 34 2 0 76 226 53 0 0 873 1,194 29 4,757 0 1 0 9 17,650 800 0 113 0 842 19 1,196 Induced 33 0 1,106 740 2,813 0 29 0 253 43 0 456 45 35 41 110 3,972 0 0 33 628 49 14 334 5 16 1 0 62 235 45 0 0 635 1,016 15 4,707 0 1 0 6 15,344 754 0 64 0 798 23 1,126 Total 154 0 7,219 2,552 11,904 0 132 0 758 181 0 1,555 213 165 210 670 25,476 0 0 106 2,210 175 59 1,256 32 80 5 0 250 1,607 156 0 0 2,510 6,081 61 22,437 0 5 0 23 69,533 3,439 0 338 0 6,073 91 10,081 103,505 38,704 35,588 177,797 State Multiplier 0.84 0.00 0.47 2.17 0.87 0.00 1.25 0.00 1.74 0.87 0.00 1.01 1.05 0.64 0.89 0.52 0.46 0.00 0.00 1.96 1.05 0.84 1.00 0.91 0.43 1.66 1.07 0.00 1.24 0.40 1.71 0.00 0.00 1.50 0.57 2.49 0.73 0.00 0.98 0.00 1.73 0.90 0.82 0.00 1.11 0.00 0.37 0.88 0.30 0.72 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight C-12 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Value Added Contribution of Unconventional Gas* Excluding Cross-S State Contributions, 2035 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming US Total Direct 58 0 5,769 928 7,123 0 90 0 61 14 0 1,087 158 131 130 525 21,981 0 0 56 1,441 107 26 814 24 37 3 0 167 1,323 85 0 0 1,500 4,809 18 18,808 0 2 0 7 44,731 2,038 0 213 0 6,299 64 9,894 Indirect 20 0 1,435 1,164 3,042 0 68 0 67 6 0 452 97 39 68 152 5,077 0 0 58 683 35 14 328 5 42 2 0 113 261 80 0 0 1,284 1,476 30 6,972 0 1 0 9 21,590 873 0 160 0 1,210 28 1,517 Induced 17 0 1,308 857 3,147 0 45 0 62 6 0 639 69 45 48 134 4,963 0 0 51 844 55 13 413 5 20 1 0 94 272 68 0 0 943 1,259 15 6,895 0 0 0 5 18,756 820 0 89 0 1,142 31 1,432 Total 94 0 8,511 2,949 13,311 0 204 0 190 26 0 2,178 324 214 247 810 32,021 0 0 165 2,967 198 53 1,555 34 100 6 0 374 1,856 234 0 0 3,727 7,544 63 32,676 0 3 0 22 85,076 3,731 0 462 0 8,651 122 12,843 130,520 48,458 44,566 223,544 State Multiplier 72.47 0.00 642.57 629.93 2,059.06 0.00 16.22 0.00 146.00 46.18 0.00 181.76 33.77 8.64 35.81 97.60 1,731.86 0.00 0.00 13.36 344.59 14.91 2.05 126.88 6.99 7.01 16.76 0.00 56.84 329.60 40.36 2.92 0.00 439.01 587.99 42.50 1,085.60 0.00 1.97 0.00 9.47 9,249.34 549.58 0.00 99.88 0.00 262.69 8.31 721.87 0.71 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS C-13 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Labor Income Contribution Excluding Cross-State Contributions: Alphabetical by State US State-L Level Labor Income Contribution of Unconventional Gas* Excluding Cross-S State Contributions, 2010 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 117 0 1,171 349 2,561 0 16 0 171 63 0 291 34 27 52 186 2,740 0 0 12 541 34 4 258 13 5 38 0 62 785 39 4 0 372 903 39 1,210 0 3 0 7 9,377 689 0 81 0 556 12 1,931 Indirect 40 0 401 400 1,276 0 10 0 98 28 0 114 21 5 21 62 1,110 0 0 9 204 9 1 81 4 4 12 0 37 218 25 2 0 277 338 27 683 0 1 0 6 5,128 363 0 55 0 169 5 448 Induced 35 0 331 249 1,174 0 6 0 89 27 0 133 13 7 16 56 887 0 0 7 223 13 1 89 4 2 11 0 26 211 20 2 0 183 274 18 606 0 1 0 4 4,341 293 0 34 0 130 5 337 Total 192 0 1,903 998 5,011 0 32 0 357 117 0 538 68 39 89 305 4,738 0 0 28 968 56 6 428 20 11 61 0 125 1,214 85 8 0 832 1,516 84 2,499 0 5 0 17 18,846 1,345 0 169 0 855 23 2,716 US Total 24,755 11,693 9,858 46,305 State Multiplier 0.64 0.00 0.63 1.86 0.96 0.00 1.03 0.00 1.09 0.87 0.00 0.85 0.98 0.43 0.71 0.63 0.73 0.00 0.00 1.27 0.79 0.65 0.65 0.66 0.61 1.32 0.59 0.00 1.01 0.55 1.17 0.83 0.00 1.23 0.68 1.18 1.07 0.00 0.82 0.00 1.34 1.01 0.95 0.00 1.09 0.00 0.54 0.82 0.41 0.87 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight C-14 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Labor Income Contribution of Unconventional Gas* Excluding Cross-S State Contributions, 2015 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 135 0 1,725 547 3,943 0 21 0 366 76 0 387 39 56 64 214 4,723 0 0 17 684 83 113 379 12 13 1 0 54 709 35 0 0 434 1,338 16 2,981 0 0 0 3 12,486 799 0 73 0 1,126 25 2,351 Indirect 53 0 611 572 2,082 0 14 0 206 33 0 142 24 12 30 71 1,802 0 0 13 249 22 42 119 4 13 1 0 33 204 24 0 0 330 522 23 1,525 0 0 0 4 6,905 435 0 52 0 330 8 560 Induced 41 0 492 371 1,849 0 9 0 189 32 0 173 15 14 21 64 1,513 0 0 10 278 32 31 130 4 6 0 0 23 192 18 0 0 215 411 11 1,448 0 0 0 2 5,806 344 0 31 0 263 9 412 Total 230 0 2,828 1,491 7,874 0 43 0 761 141 0 702 78 81 115 350 8,038 0 0 40 1,210 138 186 628 19 32 2 0 110 1,106 77 0 0 978 2,271 50 5,953 0 1 0 9 25,198 1,577 0 156 0 1,718 42 3,323 US Total 36,028 17,069 14,459 67,556 State Multiplier 0.70 0.00 0.64 1.72 1.00 0.00 1.08 0.00 1.08 0.86 0.00 0.81 0.98 0.46 0.79 0.63 0.70 0.00 0.00 1.27 0.77 0.65 0.65 0.66 0.61 1.39 1.58 0.00 1.04 0.56 1.22 0.00 0.00 1.26 0.70 2.05 1.00 0.00 1.07 0.00 1.69 1.02 0.98 0.00 1.14 0.00 0.53 0.70 0.41 0.88 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS C-15 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Labor Income Contribution of Unconventional Gas* Excluding Cross-S State Contributions, 2020 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 80 0 1,979 601 4,140 0 36 0 176 46 0 539 60 66 67 216 5,672 0 0 31 839 88 53 482 11 16 7 0 78 556 47 8 0 660 1,585 20 4,590 0 4 0 8 15,840 889 0 80 0 1,585 29 2,534 Indirect 32 0 712 650 2,222 0 25 0 104 21 0 194 36 15 31 80 2,102 0 0 22 302 24 20 151 3 16 3 0 47 169 33 4 0 512 625 28 2,405 0 2 0 7 8,948 486 0 61 0 469 11 605 Induced 24 0 567 415 1,953 0 15 0 92 20 0 240 22 16 22 66 1,808 0 0 17 340 34 15 166 3 7 2 0 33 152 25 3 0 330 488 13 2,247 0 2 0 4 7,427 383 0 35 0 371 11 444 Total 136 0 3,258 1,666 8,316 0 75 0 372 87 0 973 118 97 121 363 9,582 0 0 71 1,481 146 88 799 17 39 12 0 159 877 105 15 0 1,502 2,698 60 9,242 0 8 0 18 32,215 1,759 0 175 0 2,425 51 3,583 US Total 43,717 21,177 17,815 82,709 State Multiplier 0.70 0.00 0.65 1.77 1.01 0.00 1.11 0.00 1.12 0.88 0.00 0.80 0.97 0.47 0.80 0.68 0.69 0.00 0.00 1.27 0.77 0.65 0.65 0.66 0.62 1.43 0.71 0.00 1.03 0.58 1.25 0.83 0.00 1.28 0.70 2.10 1.01 0.00 0.82 0.00 1.41 1.03 0.98 0.00 1.20 0.00 0.53 0.74 0.41 0.89 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight C-16 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Labor Income Contribution of Unconventional Gas* Excluding Cross-S State Contributions, 2025 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 42 0 2,066 578 3,597 0 32 0 62 14 0 502 55 67 67 199 6,581 0 0 28 767 75 31 488 10 18 1 0 69 500 40 0 0 596 1,659 15 4,791 0 1 0 5 16,331 939 0 73 0 1,634 31 2,872 Indirect 17 0 741 624 1,896 0 22 0 42 6 0 182 33 16 31 74 2,399 0 0 20 274 20 12 154 3 18 1 0 41 158 29 0 0 464 643 21 2,448 0 1 0 5 9,136 510 0 55 0 480 11 685 Induced 13 0 591 399 1,686 0 14 0 34 6 0 224 20 17 22 61 2,091 0 0 16 310 29 9 168 3 8 0 0 30 138 22 0 0 299 508 10 2,327 0 0 0 3 7,628 404 0 32 0 382 11 503 Total 72 0 3,398 1,601 7,178 0 68 0 138 26 0 907 107 100 119 334 11,071 0 0 64 1,351 124 52 809 16 45 2 0 140 796 91 0 0 1,359 2,810 45 9,566 0 2 0 13 33,094 1,853 0 160 0 2,496 53 4,060 US Total 44,834 21,271 18,017 84,123 State Multiplier 0.70 0.00 0.64 1.77 1.00 0.00 1.11 0.00 1.23 0.89 0.00 0.81 0.97 0.49 0.79 0.68 0.68 0.00 0.00 1.27 0.76 0.65 0.65 0.66 0.62 1.47 1.58 0.00 1.02 0.59 1.27 0.00 0.00 1.28 0.69 2.10 1.00 0.00 0.90 0.00 1.65 1.03 0.97 0.00 1.20 0.00 0.53 0.71 0.41 0.88 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS C-17 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Labor Income Contribution of Unconventional Gas* Excluding Cross-S State Contributions, 2030 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 57 0 2,102 598 3,333 0 39 0 262 55 0 573 66 75 69 196 6,820 0 0 35 849 70 28 540 8 20 1 0 82 451 47 0 0 708 1,791 12 5,453 0 2 0 5 17,610 968 0 78 0 1,823 35 3,114 Indirect 24 0 756 644 1,736 0 27 0 152 24 0 204 39 18 32 76 2,477 0 0 25 304 19 10 170 3 21 1 0 48 146 34 0 0 547 693 17 2,810 0 1 0 6 9,896 524 0 61 0 538 12 744 Induced 18 0 602 412 1,556 0 16 0 137 23 0 255 24 19 23 60 2,166 0 0 19 343 27 8 186 3 9 0 0 35 125 26 0 0 353 549 8 2,656 0 1 0 3 8,240 416 0 34 0 427 13 546 Total 99 0 3,459 1,654 6,625 0 83 0 552 103 0 1,032 129 111 123 332 11,463 0 0 78 1,496 116 46 896 14 50 3 0 165 723 107 0 0 1,608 3,033 38 10,920 0 3 0 14 35,746 1,908 0 173 0 2,787 61 4,403 US Total 47,974 22,841 19,336 90,152 State Multiplier 0.74 0.00 0.65 1.77 0.99 0.00 1.11 0.00 1.10 0.87 0.00 0.80 0.97 0.49 0.79 0.70 0.68 0.00 0.00 1.27 0.76 0.65 0.65 0.66 0.62 1.49 1.58 0.00 1.02 0.60 1.28 0.00 0.00 1.27 0.69 2.10 1.00 0.00 0.88 0.00 1.63 1.03 0.97 0.00 1.23 0.00 0.53 0.72 0.41 0.88 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight C-18 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US State-L Level Labor Income Contribution of Unconventional Gas* Excluding Cross-S State Contributions, 2035 ($M) Alabama Arizona Arkansas California Colorado Connecticut Delaware District of Columbia Florida Georgia Idaho Illinois Indiana Iowa Kansas Kentucky Louisiana Maine Maryland Massachusetts Michigan Minnesota Mississippi Missouri Montana Nebraska Nevada New Hampshire New Jersey New Mexico New York North Carolina North Dakota Ohio Oklahoma Oregon Pennsylvania Rhode Island South Carolina South Dakota Tennessee Texas Utah Vermont Virginia Washington West Virginia Wisconsin Wyoming Direct 29 0 2,485 693 3,739 0 60 0 58 8 0 807 100 97 80 237 8,519 0 0 54 1,136 80 25 668 9 25 1 0 123 522 71 0 0 1,059 2,219 13 7,966 0 1 0 5 21,507 1,050 0 105 0 2,609 47 3,958 Indirect 12 0 892 745 1,929 0 42 0 43 4 0 283 60 23 38 96 3,080 0 0 39 411 21 9 210 3 26 1 0 72 169 52 0 0 804 856 18 4,135 0 0 0 6 12,088 571 0 86 0 773 18 943 Induced 9 0 711 477 1,740 0 25 0 33 3 0 357 37 24 26 74 2,703 0 0 29 461 31 7 230 3 11 1 0 52 145 38 0 0 524 679 9 3,889 0 0 0 3 10,064 452 0 47 0 610 17 693 Total 49 0 4,088 1,914 7,409 0 127 0 135 15 0 1,447 197 144 144 407 14,302 0 0 122 2,008 132 41 1,107 14 62 3 0 247 836 161 0 0 2,388 3,754 40 15,989 0 1 0 14 43,658 2,073 0 238 0 3,992 82 5,594 US Total 60,162 28,557 24,216 112,935 State Multiplier 0.71 0.00 0.65 1.76 0.98 0.00 1.12 0.00 1.31 0.90 0.00 0.79 0.97 0.49 0.80 0.72 0.68 0.00 0.00 1.27 0.77 0.65 0.65 0.66 0.62 1.51 1.58 0.00 1.01 0.60 1.28 0.00 0.00 1.25 0.69 2.10 1.01 0.00 1.07 0.00 1.76 1.03 0.97 0.00 1.27 0.00 0.53 0.75 0.41 0.88 NOTE: *Unconventional gas includes gas from shale, tight sands, and coal bed methane. Source: IHS Global Insight IHS C-19 The Economic and Employment Contributions of Unconventional Gas Development in State Economies Appendix D. The Economic and Employment Contributions of Non-Shale Unconventional Gas in the United States Prepared for: AMERICA'S NATURAL GAS ALLIANCE Submitted by: IHS Inc. 1150 Connecticut Avenue NW, Suite 401 Washington, DC 20036 June 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES About IHS (ihs.com) IHS Inc. (NYSE: IHS) is a leading source of information and insight in critical areas that shape today's business landscape, including energy and power; design and supply chain; defense, risk and security; environmental, health and safety, and sustainability; country and industry forecasting; and commodities, pricing and cost. IHS has been in business since 1959 and became a publicly traded company on the New York Stock Exchange in 2005. Headquartered in Englewood, Colorado, USA, IHS employs more than 5,100 people in more than 30 countries around the world. About IHS Global Insight IHS Global Insightis one of the leading economic analysis and forecasting firms in the world. With over 600 economists, statisticians, and industry specialists in 25 offices worldwide, IHS Global Insight has an established track record for providing rigorous, objective forecast analysis and data to governments and businesses around the world. Among our areas of expertise are the economic impact, tax implications, and job-creation dynamics within multiple sectors core to national, state and local economies. It helps governments and companies at all levels interpret the impact of proposed investments, policies, programs, and projects. IHS Global Insight was formed by the merger of DRI and WEFA. Still active in an advisory capacity to the firm is the original founder of WEFA, Lawrence R. Klein, the 1980 winner of the Nobel Prize in Economics. For more information, contact: Richard F. Fullenbaum Vice President, Public Sector, IHS Richard.Fullenbaum@ihs.com John W. Larson Vice President, Public Sector, IHS John.Larson@ihs.com For press information, contact: Jim Dorsey Senior Manager Media Relations, IHS Jim.Dorsey@ihs.com IHS 1150 Connecticut Avenue NW, Suite 401 Washington, DC 20036 © 2012 IHS. All information contained herein is obtained by IHS Inc. from sources believed by it to be accurate and reliable. All forecasts and predictions contained herein are believed by IHS, Inc. to be as accurate as the data and methodologies will allow. However, because of the possibilities of human and mechanical error, as well as other factors such as unforeseen and unforeseeable changes in political and economic circumstances beyond IHS's control, the information herein is provided "as is" without warranty of any kind and IHS Inc., AND ALL THIRD PARTY PROVIDERS MAKE NO REPRESENTATIONS OR WARRANTIES EXPRESS OR IMPLIED TO ANY SUBSCRIBER OR ANY OTHER PERSON OR ENTITY AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY OF THE INFORMATION OR FORECASTS CONTAINED HEREIN. D-ii JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Project Team Authors Mohsen Bonakdarpour, Director, Economic Analysis and Planning, IHS Consulting Bob Flanagan, Director, Economic Analysis and Planning, IHS Consulting John W. Larson, Vice President, Public Sector, IHS Consulting Contributors Project Manager: Tabitha M. Bailey, Senior Associate, Public Sector, IHS Consulting Special Advisor: Richard F. Fullenbaum, Vice President, Public Sector, IHS Consulting Acknowledgments We would like to acknowledge IHS Cambridge Energy Research Associates (IHS CERA) on which we have relied for oil and gas expertise and analysis. For the data on oil and gas production, holdings, and reserves, we have used IHS's extensive oil and gas databases. In particular, we want to thank Dr. Mary Barcella, IHS CERA Director, North American Natural Gas and team leader; Samuel Andrus, Director, North American Natural Gas, IHS CERA; and James Osten, Director, North American Natural Gas, IHS CERA. We would also like to thank the additional subject matter experts, technical experts, industry experts and analysts that have contributed to this study: Parker Andrews, John Anton, Rick Chamberlain, Laura Hand, Miguel Goncalves, Yanni He, Dewey Johnson, Rafael McDonald, Joe Michael, Michael Montgomery, Walter Moody, John Mothersole, Shane Norton, Sunaina Ocalan, Rajeevee Panditharatna, Frantz Price, Surya Rajan, Curtis Smith, Tom Runiewicz, Mark Wegenka, and Steve Zinger IHS offers an independent assessment of the importance unconventional gas to the overall US economy. This research was supported by the America's Natural Gas Alliance (ANGA). IHS is exclusively responsible for all of the analysis and content contained herein. The analyses and metrics developed during the course of this research are intended to contribute to the national dialogue on the role of unconventional gas in terms of production, employment, economic growth, and energy security. IHS D-iii THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Key Findings: The Economic and Employment Contributions of Non-Shale Unconventional Gas in the United States As a companion to the IHS Global Insight study "The Economic and Employment Contributions of Shale Gas in the United States," this study examines the growth in production of natural gas extracted from unconventional sources other than shale—namely, tight sands and coal bed methane (CBM)—and the economic benefits of this growth, including the additional employment generated by the increased activity. The same technologies that have allowed the development of natural gas from shale formations have also opened up the development of non-shale types of unconventional gas extracted from tight sands and CBM. Natural gas extracted from these non-shale unconventional sources will be referred to in this report as "other" unconventional gas. This report focuses on the economic impact of other unconventional gas development and production: • In 2010, total unconventional gas (from shale and other) represented 53 percent of all US natural gas production. By 2035, their combined share will be 79 percent - 60 percent shale gas and 19 percent other unconventional gas. The growth will be driven by strong growth in shale gas production and some additional growth in other unconventional gas production throughout the forecast time horizon, 2010 through 2035. • Nearly $1.3 trillion in cumulative capital investment in other unconventional gas alone is expected between 2010 and 2035. This, combined with capital investments in shale gas, will amount to nearly a $3.2 trillion investment in unconventional gas production during this time. • In 2010, other unconventional gas activity supported 407,000 jobs; by 2015, employment will expand to nearly 594,000 and, by 2035, to nearly 779,000. When combined with shale gas, unconventional natural gas activity supported just over 1 million jobs in 2010; this will increase to 1.7 million jobs in 2015 and more than 2.4 million jobs in 2035. • The contribution to US gross domestic product (GDP) from other unconventional gas activity was $57 billion in 2010. This will increase to $78 billion by 2015 and to $101 billion in 2035. • In 2010, other unconventional gas production contributed over $15 billion in federal, state and local government tax revenues, and this will nearly double to nearly $28 billion in 2035. Between 2010 and 2035, other unconventional gas activity will generate a total of nearly $566 billion in government tax revenues. As with shale gas activity, the dramatic impact on employment and the economy from other unconventional gas activity reflects the significant capital intensity of the industry, the ability to source inputs from domestic US sources, the coast-to-coast structure of the supply chain, and the high quality of the jobs created.1 1 For more information, see "The Economic and Employment Contributions of Shale Gas in the United States:" http://www.ihs.com/info/ecc/a/shale-gas-jobs-report.aspx IHS D-v THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Table of Contents Key Findings: The Economic and Employment Contributions of Non-Shale Unconventional Gas in the United States . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-v Executive Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-1 Jobs: Nearly 600,000 by 2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-2 Value Added to GDP: $100 Billion by 2035 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-2 Government Revenues: Nearly $566 Billion in 2010-35 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-3 Capital Investment: $1.3 Trillion in 2010-2035 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-3 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-4 1.Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-5 The Structure of This Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-5 2. An Introduction to Unconventional Gas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-6 Unconventional Gas Supply and Costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-7 3. Outlook for Production and Capital Expenditures for Other Unconventional Gas . . . . . . . . . . . . . . . . . . . .D-10 The Process of Natural Gas Development . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-11 Prospecting and Exploration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-11 Well Construction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-11 Production . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-12 Estimating Production Profiles for Other Unconventional Gas Plays . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-12 Drilling Costs and Expenditures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-13 4.Economic Contribution Assessment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-15 Approach and Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-15 How to Define the Economic Contribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-15 Modeling the Economic Contribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-15 Measuring the Economic Contributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-16 Employment Contribution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-17 Value Added to GDP and Labor Income Contributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-18 Government Revenues and Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-18 5. Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-20 Appendix A. Future Production and Capital Expenditure Outlook: Other Unconventional Gas . . . . . . . . . . . .D-21 Production Profiles . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-21 Well Capital Expenditures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-21 North American Modeling Methodology and Process Description . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-23 North American Gas Modeling Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-23 Appendix B. Economic Contribution Assessment Detailed Tables: Other Unconventional Gas . . . . . . . . . . .D-27 Other Unconventional Gas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-28 Total Unconventional Gas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-35 Appendix C: IHS Global Insight Economic Contribution Assessment: Other Unconventional Gas . . . . . . . . .D-42 Data Requirements and Assumptions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-42 Other Unconventional Gas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-43 Total Unconventional Gas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .D-45 IHS D-vii THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Executive Summary IHS Global Insight’s December report, “The Economic and Employment Contributions of Shale Gas in the United States,” the first in a series of studies about natural gas development in North America, presented the economic contribution of increasing development of US shale gas plays.2 This new companion study focuses on the economic contributions of what is called “other,” or non-shale, sources of unconventional gas, namely tight sands and coal bed methane (CBM). Like the prior shale study, this study examines the impact in terms of jobs, economic growth, and labor income and government revenues—today and in the future – from the development of other unconventional natural gas. This research demonstrates that other unconventional gas will make a significant and steady economic contribution in the near term upon which the strong, long-term growth offered by natural gas development will be built. For the reader’s convenience, this study provides the economic and related impacts of natural gas development in two ways: 1) for other unconventional gas (tight sands and CBM) and 2) for total unconventional gas (shale, tight sands, and CBM). The shale gas story over the next quarter century is one of powerful growth—in investment, production, employment, and economic growth. But other unconventional gas will also be an important story of a secure and steady foundation that will provide an additional production source of natural gas that will also contribute to US economic growth. But because other unconventional gas production is forecast to grow more slowly than shale gas production, its share of total unconventional gas production will decline. In 2010, unconventional gas represented 53 percent of total US natural gas production—27 percent from shale gas and 26 percent from other unconventional.3 By 2035, unconventional gas will account for 79 percent of total US gas production—60 percent from shale gas and 19 percent from other unconventional gas. The following is a breakdown of the economic benefits from other unconventional natural gas activity in terms of employment growth, GDP growth, tax revenues and capital expenditures. S h a r e o f N a t u r a l G a s P r o d u c t i o n b y T yp e, 2010 S h a r e o f N a t u r a l G a s P r o d u c t i o n b y T yp e, 2035 47% 19% 21% 26% 27% 60% Shale Other Unconventional Conventional Shale Other Unconventional Conventional 2 A "play" is a geographic area associated with a petroleum-bearing geologic formation 3 The remainder is conventional natural gas production, which involves accessing the most readily available sources of natural gas, using wells drilled vertically into gas reserves. Unconventional gas production, as discussed in prior reports, requires horizontal or other unconventional drilling techniques. IHS D-1 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Jobs: Nearly 600,000 by 2015 The economic contribution of other unconventional gas is measured by the sum of the direct contribution to employment, the indirect contribution through the reliance on supplier industries, and the so-called “induced” contribution that results when workers in the gas and supplier industries spend their additional incomes on consumer and other goods, boosting the entire economy. In 2010, other unconventional gas activity supported more than 407,000 jobs in total; this was made up of nearly 90,000 direct jobs in the United States, more than 133,000 indirect jobs in supplier industries, and more than 184,000 induced jobs. US Employment Contribution (Number of workers) Other Unconventional Gas* Direct Indirect Induced Total 2010 2015 2035 89,824 133,289 184,195 407,308 135,781 196,297 261,687 593,765 179,063 259,704 340,021 778,787 2010 237,968 326,999 443,690 1,008,657 2015 333,780 479,487 650,182 1,463,449 2035 539,398 806,810 1,092,669 2,438,877 Total Unconventional Gas** Direct Indirect Induced Total Source: IHS Global Insight NOTES: *Other unconventional gas includes gas from tight sands and coal bed methane. **Total unconventional gas includes gas from shale, tight sands, and coal bed methane. Value Added to GDP: $100 Billion by 2035 In terms of its contribution to GDP, other unconventional gas activity contributed more than $56 billion to the US economy in 2010 alone. This will increase to more than $78 billion by 2015 and to more than $100 billion in 2035. The growth in other unconventional gas production and capital expenditures begins with strong expansion during the first decade, followed by more moderate growth during the last fifteen years of the 25-year forecast. Due to the slowdown in the growth of production during the second part of the forecast, the value added to GDP during the first decade of the forecast period will exceed gains made in the remaining years of the forecast. US Value Added Contribution ($M) Other Unconventional Gas* Direct Indirect Induced Total 2010 2015 2035 22,822 15,885 17,818 56,525 29,944 22,940 25,418 78,302 37,477 30,112 33,079 100,667 2010 52,004 38,301 43,101 133,405 2015 77,007 56,441 63,069 196,516 2035 130,520 95,346 105,862 331,728 Total Unconventional Gas** Direct Indirect Induced Total Source: IHS Global Insight NOTES: *Other unconventional gas includes gas from tight sands and coal bed methane. **Total unconventional gas includes gas from shale, tight sands, and coal bed methane. D-2 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Government Revenues: Nearly $566 Billion in 2010-35 In 2010, other unconventional gas activity contributed just over $15 billion to federal, state, and local governments through income taxes, royalty payments, and other taxes. By 2035, these revenues will grow to nearly $28 billion. During the entire forecast period, 2010 through 2035, other unconventional gas will contribute nearly $566 billion in total government revenues.4 US Estimated Government Revenue ($M) Other Unconventional Gas* Federal Taxes State and Local Taxes Federal Royalty Payments Total Government Revenue Lease Payments to Private Landowners 2010 6,888 7,597 700 15,185 2015 9,733 10,121 916 20,770 2035 12,619 13,690 1,539 27,847 2010-2035 262,165 276,003 27,524 565,692 127 239 484 8,263 2010 6,888 7,597 700 15,185 2015 9,733 10,121 916 20,770 2035 12,619 13,690 1,539 27,847 2010-2035 262,165 276,003 27,524 565,692 127 239 484 8,263 Total Unconventional Gas** Federal Taxes State and Local Taxes Federal Royalty Payments Total Government Revenue Lease Payments to Private Landowners Source: IHS Global Insight NOTES: *Other unconventional gas includes gas from tight sands and coal bed methane. **Total unconventional gas includes gas from shale, tight sands, and coal bed methane. Capital Investment: $1.3 Trillion in 2010-2035 Continued expected growth in the demand for other unconventional gas over the next 25 years will drive the need for higher levels of capital expenditures. IHS expects capital investment in other unconventional gas production to total nearly $1.3 trillion between 2010 and 2035. Capital expenditure growth is forecast to be stronger during the initial ten years compared with the remainder of the forecast horizon. US Annual Capital Expenditure by Type: Other Unconventional Gas* ($M) Total Upstream Capital Expenditure Infrastructure Capital Expenditure TOTAL CAPITAL EXPENDITURE 2010 2015 2035 17,614 1,630 19,244 33,195 2,903 36,097 67,093 6,010 73,104 2010 2015 2035 42,455 10,049 52,505 72,882 11,922 84,804 183,898 15,797 199,695 Total 2010-2035** 1,190,908 106,605 1,297,513 Source: IHS CERA NOTES: *Other unconventional gas includes gas from tight sands and coal bed methane. **Total 2010-2035 represents the total for all years including those years not reported. US Annual Capital Expenditure by Type: Total Unconventional Gas** ($M) Total Upstream Capital Expenditure Infrastructure Capital Expenditure TOTAL CAPITAL EXPENDITURE Total 2010-2035** 2,845,224 328,145 3,173,369 Source: IHS CERA NOTES: *Total unconventional gas includes gas from shale, tight sands, and coal bed methane. **Total 2010-2035 represents the total for all years including those years not reported. 4 This results from summing government revenues for each year in the 25-year period. IHS D-3 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Conclusion Although other unconventional gas production will not keep pace with that exhibited by shale gas activity, the level of capital intensity required by other unconventional gas production ensures that it will still have an important role to play in the total unconventional gas activity’s overall economic and employment contribution. Similar to contributions brought about by shale gas activity, other unconventional gas activity’s economic and employment contributions will be led by direct employment, indirect employment through a broad supplier base supporting the activity, and the tremendous income effects brought about by consumer spending as a result of these direct and indirect employment opportunities. At a time when the US economy continues to struggle to pull out of the Great Recession and create enough jobs to reduce the high US unemployment rate, a thriving natural gas industry based not just on shale gas, but also on other unconventional gas, offers great prospects for future employment and other growth opportunities for the US economy. D-4 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES 1. Introduction The supply of natural gas in North America, long viewed as being in decline, is now expanding at a rapid pace. Rising production, fueled by technological advances, has significantly reduced gas prices. Natural gas prices plunged from a 2008 high of $8.84 per million British thermal units (MMBtus) to less than $3 per MMBtus currently. Natural gas production in the United States has grown so much that the market’s future expansion is now contingent on new demand—supply is no longer a constraint. The resurgence of the US natural gas industry is being driven primarily by development of new shale gas resources, which have fundamentally changed the outlook for natural gas supply and price in North America. Shale gas development has provided substantial benefits to employment and the economy, which were documented in our December 2011 report, “The Economic and Employment Contributions of Shale Gas in the United States.”5 However, this is just one aspect of a revolution in unconventional gas that has wider effects. The same technologies that have opened up the development of shale gas have also permitted the development of other types of unconventional gas—specifically, gas from tight sands and coal bed methane (CBM). Over the next 25 years, this other unconventional gas production will supplement declining traditional gas supplies at the same time that shale gas production also steadily expands. The production mix of the two will be determined by the economics of individual plays and individual wells within each play. IHS has produced two reports on unconventional gas development in North America. The first report was limited to shale gas production and the economic impact to the US economy of developing this unconventional form of gas. This report looks at other unconventional gas development in the United States. This analysis begins with production outlooks for major tight sands gas and CBM plays in the United States through 2035. In addition to production, IHS CERA’s analysis of each play calculates the investment of capital, labor, and other inputs required for the projected level of output. The benefits of these investments are then calculated using IHS Global Insight’s proprietary economic impact assessment and macroeconomic models to generate the employment, GDP growth, labor income, and tax revenues that will result from this higher level of unconventional gas development. The Structure of This Report The remainder of this report is divided into three sections and three appendices. • The next section, Section 2, provides an overview of other unconventional gas. • Section 3 presents the critical inputs to the economic analysis, namely, the production and capital expenditure outlooks for other unconventional gas. The outlook for other unconventional gas is consistent with forecasts for the US natural gas market supply and demand through 2035 presented in the IHS Global Insight study “The Economic and Employment Contributions of Shale Gas in the United States.” • Section 4 presents the results of IHS Global Insight’s economic contribution analysis. • Appendices are provided to facilitate the readers’ understanding of the methodologies, research, and data used in our analysis and to present more detailed results from our study. • Appendix A contains the underlying methodology and detailed data related to the assumed future production profile and capital expenditure outlook for other unconventional gas. • Appendix B provides detailed results of the economic contribution assessment. • Appendix C presents the data and modeling approach underlying the economic contribution assessment. 5 http://www.ihs.com/info/ecc/a/shale-gas-jobs-report.aspx IHS D-5 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES 2. An Introduction to Unconventional Gas In a conventional natural gas reservoir, oil or natural gas has migrated upward over geologic time from a lower source rock, through permeable rocks until it hits an impermeable layer of rock and then moves along this hard barrier until it encounters a “trap.”6 These accumulations of natural gas are sometimes found in association with crude oil and sometimes not. A well is usually drilled vertically into the reservoir to allow the oil and/or natural gas to flow into the wellbore and up to the surface. Historically, these reservoirs have been relatively “easy” to access using traditional technology. Unconventional gas, by contrast, is embedded in impermeable geologic formations that restrict the flow of gas. Shale gas is contained in shale rock with low permeability, tight sands gas is contained in low-permeability sandstone, and CBM is contained in low-permeability coal seams. Permeability is what drives whether development requires conventional techniques or newer approaches to extract natural gas or oil in an economically feasible manner. The Geology of Conventional and Unconventional Oil and Gas Source: EIA 10402-4 It has long been known that the low-permeability source rock existed and that it contained significant amounts of natural gas and oil. However, conventional well-completion techniques did not generally yield sufficient production to justify developing these gas reserves. Through innovation and technological evolution in the oil and gas industry, production techniques have been developed over the past two decades that allow the economical extraction of natural gas and oil from low-permeability source rock. Two technologies in particular are critical—both of them with long histories of use preceding unconventional gas development. Conventional well-completion techniques for decades have turned to either to horizontal drilling or to hydraulic fracturing to improve oil or gas flow. These well-completion technologies were used primarily in the startup phase of traditional wells to initiate production and, less often, to sustain production in an already producing well. Horizontal drilling techniques were also adapted to produce unconventional hydrocarbons, including natural gas. Horizontal drilling involves first drilling a vertical well to the desired depth and then drilling laterally to access a larger portion of the source rock and to intersect natural fractures in the rock in order to enhance flow. Hydraulic fracturing involves the injection of fluid (usually a mixture of water, sand, and chemicals) under high pressure into a natural gas or oil well to create new fractures in the source rock. The sand prevents the cracks from closing when the 6 Permeability refers to how easily gasses and fluids are able to flow through a rock. D-6 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES U S L o w e r 4 8 N a t u r a l G a s P r o d u c t i o n B y T y p e : 2 0 0 0 t o 2010 water pressure is removed, creating permeable pathways for natu- Bcf per Day ral gas to move into the wellbore 70 and then to the surface. Hydraulic fracturing is a one-time process 60 that takes place over a few days to release the flow of gas from the 50 impermeable rock into the well40 bore. Some of the injected water returns to the surface and is re30 covered and some remains in the reservoir. Over the course of 20 hours or days, this “flowback” is increasingly dominated by the 10 natural gas that is the goal of the production process. Once gas is 0 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 flowing, the well is connected to gathering pipelines that send the Conventional Tight Gas Shale Gas Coalbed Methane gas to processing facilities and Source: EIA, IHS CERA from there to the consumer market. No further hydraulic fracturing takes place unless later, during the producing life of the well (typically years later), remedial work is required to enhance well flow. The combination of horizontal drilling and hydraulic fracturing allows producers to access large areas of source rock with a single well and allows commercial production from formations so tight or lacking in permeability that significant amounts of oil and/or gas had never been able to escape over millions of years. The unconventional gas revolution began in the Barnett shale gas play in Texas, where, over the course of two decades, the combination of horizontal drilling and hydraulic fracturing in well completions showed impressive results in hydrocarbon production. The technology spread to other shale and tight sands plays throughout the United States, leading to a long-term climb in US gas production beginning in 2007, which was interrupted only by Hurricane Ike in 2008 and the Great Recession in 2009. In January 2007, total natural gas production in the US lower 48 states was 49.7 billion cubic feet (Bcf) per day. By July 2008, it had climbed to 56.1 Bcf per day and currently exceeds 64 Bcf per day. Unconventional Gas Supply and Costs Significant differences exist between conventional and unconventional natural gas in terms of the unique geology, technology, and productivity of each. But technically there is very little difference between most shale and tight sands formations. Many plays contain both types of formations, and the designation of a particular play as a shale or a tight sand play is usually the result of geologists’ consensus based on the predominant rock characteristics (portions of a play can vary from shale-dominant to tight sands-dominant by depth or geographical location). Once designated a shale play, all gas production from that play is considered shale gas, even though it may have come from a sandstone formation within the larger play. Similarly, all natural gas produced from a tight sands play is considered to be tight sands gas, even though it may have originated in shale rock within the tight sands play. Well productivity and costs are roughly similar for the two types of unconventional gas. Differences in production cost are driven by the characteristics and complexities of individual plays or well requirements rather than by the play’s designation as shale or tight sands. In comparison to conventional gas, production per well for all types of unconventional gas is usually much higher, which drives down their unit costs of production. This also demonstrates that the availability of other unconventional gas reinforces the price and supply effects of the shale-gas revolution discussed in the previous report: IHS D-7 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Because so much unconventional gas resource is available at a low cost, the supply curve for natural gas has become relatively elastic. In other words, the US natural gas resource base can now accommodate significant increases in demand without requiring a higher price to elicit new supply7. There is one significant difference between tight sands gas and shale gas in the US lower 48, however. The estimated recoverable resource base for tight sands gas is much less than for shale gas, and the outlook for growth in tight sands gas production is below that of shale gas. An IHS CERA study published in February 2010, “Fueling North America’s Energy Future,” examined nine tight sands gas plays and six shale plays in the US lower 48 and estimated the recoverable resource in each play. The tight sands gas plays—the Cotton Valley, Bossier, Deep Bossier, Colony Wash, Granite Wash, Piceance, Jonah, Pinedale, and Natural Buttes—contain an estimated 200 trillion cubic feet (Tcf) of recoverable resources. In contrast, shale gas resources were estimated to be more than 1,100 Tcf in the US lower 48. The February study did not estimate CBM resources, but the Potential Gas Committee at the Colorado School of Mines put CBM resources in the US lower 48 at 101 Tcf. Major Unconventional Gas Plays in North America 7 IHS Global Insight, "The Economic and Employment Contributions of Shale Gas in the United States", December 2011, p. 8. D-8 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Tight sands have played a significant role in the US gas supply picture for many years. According to the US Energy Information Administration, tight sands gas production peaked in 2008 at more than 18 Bcf per day, accounting for more than half of US lower 48 gas supply. IHS CERA expects tight sands gas to continue to provide substantial volumes in the future, though it is unlikely to exhibit the rapid growth expected from shale gas plays. CBM supply has grown from about 1 Bcf per day in the 1990s to 5 Bcf today and is unlikely to increase further. U S L o w e r 4 8 N a t u r a l G a s P r o d u c t i v e C a p a c i t y O u t l o o k b y T y p e: 2010 to 2035 Bcf per Day 90 80 70 60 50 40 30 20 10 0 2010 Shale 2015 Tight Sands 2020 CBM 2025 2030 Conventional 2035 Associated Source: EIA, IHS CERA IHS D-9 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES 3. Outlook for Production and Capital Expenditures for Other Unconventional Gas IHS CERA's outlook for other unconventional gas in the US lower 48 comprises production from 23 tight gas plays and sub-plays and 14 coal bed methane plays. The 37 other unconventional gas plays considered for this analysis are: Unconventional Gas Plays Play Type Geographic Extent of Play* Big Sandy Tight Sand Kentucky, Virginia, West Virginia Trenton-Black River Tight Sand Kentucky, New York, Ohio, Pennsylvania, Virginia, West Virginia Cotton Valley Tight Sand Louisiana Vernon/Terryville Tight Sand Louisiana E. Cotton Valley Tight Sand Texas W. Cotton Valley Tight Sand Texas Deep Bossier (>14k feet) Tight Sand Texas S Texas Wilcox (Lobo) Tight Sand Texas Granite Wash Tight Sand Texas, Oklahoma Sahara Tight Sand Oklahoma Colony Wash Tight Sand Arkansas Hartshorne Tight Sand Oklahoma Haley Deep Tight Sand Texas Wattenberg-Niobrara-Codell Tight Sand Colorado Wamwash-Lewis MV Tight Sand Colorado ,Wyoming Jonah Tight Sand Wyoming Pinedale Tight Sand Wyoming Mamm Creek - Williams Fork Tight Sand Colorado Piceance Emerging Tight Sand Colorado Lower Cretaceous-Mesozoic Tight Sand Colorado Natural Buttes Tight Sand Utah Buttes Deep Tight Sand Utah Lance Tight Sand Wyoming Coal Bed Methane (Appalachian, avg) Coal Bed Methane Pennsylvania, Virginia, West Virginia CBM (Black Warrior - Pottsville) Coal Bed Methane Alabama CBM (Arkoma - Hartshorne) Coal Bed Methane Oklahoma CBM (Chatauqua) Coal Bed Methane Oklahoma CBM (Cherokee) Coal Bed Methane Kansas CBM (E. Green River) Coal Bed Methane Wyoming Las Vegas (LV Raton) Coal Bed Methane Colorado, New Mexico CBM (Piceance) Coal Bed Methane Colorado Big George (Powder River) Coal Bed Methane Wyoming, Montana Wyodak (Powder River) Coal Bed Methane Wyoming, Montana Canyon (Powder River) Coal Bed Methane Wyoming, Montana Anderson (Powder River) Coal Bed Methane Wyoming, Montana Other Coal (Powder River) Coal Bed Methane Wyoming, Montana CBM (Uinta) Coal Bed Methane Utah Fruitland (San Juan) Coal Bed Methane New Mexico, Colorado *The list of gas plays provides the state location or locations of the full extent of the underground gas play. However, states containing part of a play do not necessarily have production from that play. For example, the Marcellus play extends into Virginia and Kentucky, but no extractions of Marcellus gas take place in those states at present or in the outlook for this study. This study also assumes that no Marcellus production is forthcoming from New York. D-10 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES The Process of Natural Gas Development Gas produced from conventional and unconventional sources are virtually identical in the fundamental aspects of their exploration, development, production, transportation, processing, and marketing. In terms of well construction, however, unconventional wells tend to be more capital intensive due to the more difficult drilling requirements for long horizontal wellbores and due to the far greater complexity of well completion, which requires multi-stage hydraulic fractures during the production start-up stage. Prospecting and Exploration Numerous geological evaluations, seismic surveys, pilot drilling and testing, and land acquisitions are required to determine whether a gas field has the potential for commercial development. Once an operator has acquired a prospective lease for mineral rights, the producer is typically bound to drill and/or produce in the time period specified by the lease and stands to forfeit leasing rights if the deadline is not met or an extension is not negotiated. Lease terms are typically three to five years, and the effective date of the lease starts the clock on well construction. Development plans are formulated with an eye toward minimizing environmental and other local disturbances and ensuring all necessary permits are secured. Well Construction Well construction starts with detailed planning of the location of a well, both at the surface and for the trajectory and target below ground. Once a well location has been surveyed and staked out, and a drilling permit has been granted by the state and/or local regulatory authorities (or by federal authorities if on federal land), the site is prepared for drilling. Surface preparation is performed to ensure even, stable ground on which a rig can stand erect and operate. Tie-in lines are laid from the well site to the nearest gathering and sales pipeline. Drilling A drilling rig penetrates the ground by means of a rotating drill bit attached to the bottom of a steel pipe, known as the drill string. Often, a specialized “mud” is continuously pumped down the drill string and up the wellbore in order to keep the drill bit cool and lift rock cuttings away from the bit and up to the surface. As drilling progresses, steel sleeves, also known as casing, are lowered and cemented in place, starting at the surface and moving downward, to isolate the wellbore from the adjacent formations. After drilling the vertical segment, the drill bit is directed to “kick off” in an arc until it reaches a target horizontal trajectory, where it continues with a lateral segment to a designed length, often 5,000-10,000 feet. Completion Well completion is the process of preparing a well, after drilling, to begin production. Completion steps include installation of the remainder of the casing, followed by perforation. To draw the natural gas IHS D-11 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES from the source rock up through the well, the steel and cement barriers in the wellbore are perforated within the targeted zone only, creating holes in the well through which the gas will flow. Perforation is accomplished by means of controlled explosive charges set off at the correct position in the wellbore and mounted in specially designed “guns.” Once the casing is perforated, the target zone area accessed by the well is ready to be hydraulically fractured. Pumps inject large volumes of water down the well bore, under very high pressure. The pressure from the pumps is propagated by the fluid coursing down the wellbore and against the reservoir rock, creating fractures in the geologic matrix. The water contains small quantities of additives and sand, which remain in the fractures to prop them open. Natural gas then migrates into the fractures, travels along the fractures to the wellbore, up the wellbore to the surface wellhead, and on to gathering facilities leading to processing plans and then to sales and marketing pipelines. A well is typically hydraulically fractured in several stages, from 10 to as many as 25 stages per well. This technique exposes only a small horizontal segment at a time to fracturing fluids and pressure, increasing the intensity of hydraulic fracturing in each segment. Fractured stages are separated by cement plugs drilled out after the last stage is hydraulically fractured. During drill-out, the plugs, plug debris and excessive fluid and sand left in the wellbore can be cleaned out. This may be done using a lighter rig called a workover rig or a coiled tubing unit. Once plug drill-out and wellbore cleanup are complete, the well is ready for flowback. In most cases, the reservoir pressure, along with compressed gas and the stored energy from the fracturing fluids pumped in, is adequate to push up against the column of fluid in the wellbore and progressively “clean up” the well. Water flowing up and out of the wellbore is directed through surface flow lines to a collection or gathering point where any gas can be separated out. A water pipeline system or water disposal trucks periodically haul away collected flowback water to designated sites for recycling, injection into dedicated disposal wells, or other means of disposal that meet environmental requirements. Production After completion, production goes into full swing. Local production tie-in lines lead to compression stations located in the production area. Excess water that is mingled with gas—a byproduct of production—is stripped out of the gas by means of dehydrators, and this “cleaner” gas is transported through a network of gathering pipelines that continually collect gas from various leases and feed it to processing plants. Gas processing plants extract natural gas liquids such as ethane, propane, butane, isobutene, and pentane for sale in their respective markets. The processing plants also extract contaminants such as hydrogen sulfide, carbon dioxide, and nitrogen contained in the natural gas itself. Dry gas then enters a pipeline for delivery to end markets such as power plants or urban distribution networks. Estimating Production Profiles for Other Unconventional Gas Plays Estimating the outlook for production profiles for other unconventional gas plays follows the same procedure as for the shale plays discussed in the previous report. Production forecasts were developed based on detailed analyses of each play. These analyses used IHS energy databases and internal research and also considered variables such as rig counts, number of days required to drill a well, total area available to be developed, well spacing, and expected decline rates (see Appendix A). The outlook scenarios for other unconventional gas were constrained to be consistent with IHS CERA’s forecasts of natural gas demand, price, and pipeline infrastructure requirements as reported in our “North American Natural Gas Market Briefing” in September 2011. This assessment shows that other unconventional gas production is expected to grow slowly, from 5.5 Tcf in 2010 to 5.9 Tcf in 2035, as its share of total gas production declines from 26 percent in 2010 to 19 percent by 20358. 8 Note, however, that total production will continue to increase, albeit slightly, even as drilling declines due to the continued output by wells drilled in previous years. D-12 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US Lower 48 Annual Natural Gas Production and Well Completions: Other Unconventional Gas* vs. Total Gas 2010 2015 2020 2025 2030 2035 5,512,297,522 5,528,478,777 5,458,495,669 5,572,393,935 5,704,099,381 5,925,977,626 3,919,979,770 4,189,135,644 4,345,136,944 4,567,079,807 4,744,306,084 4,968,805,590 1,592,317,752 1,339,343,133 1,113,358,725 1,005,314,129 959,793,297 957,172,036 21,229,024,284 23,276,996,872 26,000,032,080 27,769,207,506 29,114,085,717 31,263,775,082 PRODUCTION Other Uncon. Gas (Mcf) Tight Sands Coal Bed Methane Total Gas (Mcf) Other Uncon. Share of Total 26% 24% 21% 20% 20% 19% 1,597 2,356 2,587 2,318 2,234 2,198 1,163 1,899 1,925 1,683 1,623 1,599 434 457 662 635 611 600 17,858 18,344 19,532 17,355 16,213 16,224 9% 13% 13% 13% 14% 14% 4.38 4.77 4.57 4.84 4.91 5.15 WELL COMPLETIONS Other Uncon. Gas Tight Sands Coal Bed Methane Total Gas Other Unconventional Share of Total Henry Hub Price (Constant 2010 $US per MMBtu) Source: IHS CERA and EIA NOTE: *Other unconventional gas includes gas from tight sands and coal bed methane. Drilling Costs and Expenditures An unconventional gas well in a shale or tight sand target can cost anywhere between $3.5 million and $12 million to drill and prepare for production, while a well targeting CBM costs less than $1.5 million. Well costs depend on several physical factors, including the vertical depth of the gas reservoir, length of the lateral pipe, reservoir pressure, rock characteristics, number of fracture stages, as well as commercial factors such as ease of access to materials and services, and the price and supply of water, fluid, sand, drilling and completion services. Capital expenditures are categorized in this study by lease acquisitions, drilling, completion, facilities, gathering, processing, and compression. In addition, the development of a major play requires additional pipeline capacity to get the gas to market. IHS CERA estimated the costs associated with the production outlook for other unconventional gas based on data and analysis from IHS databases and proprietary models (these are discussed further in Appendix A). This analysis found that nearly $1.3 trillion in capital expenditures will take place between 2010 and 2035 for other unconventional gas development. These expenditures will clearly have a significant economic impact, in terms of jobs creation, value added to GDP, labor income, and tax revenues. These effects are discussed in the following sections. IHS D-13 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US Annual Capital Expenditure by Type: Other Unconventional Gas* ($M) 2010 2015 2020 2025 2030 2035 Total 2010-2035** 7,046 13,278 17,281 20,708 23,615 26,837 476,363 Drilling 4,721 8,896 11,578 13,874 15,822 17,981 319,163 Support Services 2,325 4,382 5,703 6,834 7,793 8,856 157,200 Drilling Capital Expenditure Completion Capital Expenditure 8,807 16,597 21,601 25,885 29,519 33,547 595,454 Hydraulic Fracturing 7,046 13,278 17,281 20,708 23,615 26,837 476,363 Other 1,761 3,319 4,320 5,177 5,904 6,709 119,091 Facilities Capital Expenditure Material Fabricaton Project Management Other TOTAL Upstream Capital Expenditure Infrastructure Capital Expenditure Gathering and Processing TOTAL CAPITAL EXPENDITURE 1,761 3,319 4,320 5,177 5,904 6,709 119,091 1,057 1,992 2,592 3,106 3,542 4,026 71,454 440 830 1,080 1,294 1,476 1,677 29,773 88 166 216 259 295 335 5,955 176 332 432 518 590 671 11,909 17,614 33,195 43,202 51,770 59,037 67,093 1,190,908 1,630 2,903 3,890 4,659 5,307 6,010 106,605 1,630 2,903 3,890 4,659 5,307 6,010 106,605 19,244 36,097 47,092 56,429 64,344 73,104 1,297,513 Source: IHS CERA NOTES: *Other unconventional gas includes gas from tight sands and coal bed methane. **Total 2010-2035 represents the total for all years including those years not reported. D-14 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES 4. Economic Contribution Assessment Approach and Methodology How to Define the Economic Contribution The objective of measuring the economic contribution of future production of other unconventional gas—or any economic activity—is to capture all of the multitude of that activity’s effects on the broader US economy. First, this analysis requires an integration of the capital expenditure forecast and the natural gas production forecast presented in Section 3 into the IMPLAN and IHS Global Insight’s proprietary macroeconomic modeling systems. Such a framework and forecasts form the foundation for any economic contribution assessment. A second step in an economic contribution assessment is an assessment of each individual component of commercial activity within an industry and, equally important, its impacts on other industries—in this study, these are the diverse suppliers required for other unconventional gas activity. To estimate the net impact of other unconventional gas activity as it feeds these complex commercial interactions, economic activity was divided into three stages: the “direct,” “indirect” and “induced” contributions on the broader economy. The direct, indirect and induced contributions are defined as follows: • The directt conttributtion is the effect of other unconventional gas development and production on output, employment, and income. For example, direct impacts are generated by the exploration, production, transport, and delivery of unconventional gas and by purchases of critical on-site services. Spending and investments in these activities also have a direct impact on production levels, the number of workers employed, and how much those workers are paid and otherwise compensated—these are the direct contributions to US economic activity. • Changes in the direct purchasing activities as a result of other unconventional gas production also create indirectt conttributtionss, which are felt by all of the suppliers. Changes in demand (from the direct industries) lead to corresponding changes in output, employment, and income throughout the supply chains, as well as supplier’s interindustry linkages. Suppliers who support other unconventional gas activity affected by such changes span the majority of industries in the US economy. • Finally, workers and their families in both the direct and indirect industries spend their income on food, housing, leisure, autos, household items, clothing, and other consumer goods. The additional output, employment, and other income effects that result from these consumer spending activities are categorized as the induced conttributtion. Modeling the Economic Contribution The approach used for assessing the economic contribution of other unconventional gas follows the same logic and process explained in the previous report, “The Economic and Employment Contributions of Shale Gas Industry in United States.” Each of the three distinct levels of economic contribution—direct, indirect, and induced—were quantified in terms of their contribution on employment, value added to GDP, and labor income. Estimates of federal, state, and local tax revenues were also calculated to assess the contribution on the public sector. The outlooks for US production and capital expenditures for other unconventional gas were developed in the same fashion as in the shale gas analysis. The production profile was compiled from expected production of other unconventional gas for each year of the forecast time horizon, 2010 through 2035. Similarly, the capital expenditure profile was estimated using the anticipated annual investment in drilling, completion, facilities, and infrastructure. The production and capital outlooks were developed in nominal US dollars to capture the effects of price and quantity increases. IHS Global Insight then used the capital expenditure outlook to modify and customize the production function for unconventional gas. The process used to transform the subcategories of capital expenditures into a set of sector- IHS D-15 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES level transactions for industry investments, purchases and services was the same as the process applied in the shale gas report. This focused approach provided an appropriate set of capital expenditure estimates for other unconventional gas activity, which was then used to exercise the IMPLAN model (a detailed explanation and table in Appendix C of the shale gas industry report exhibits the industry model sectors for each of the broad capital expenditure categories). The modeling process used was the same as for the shale gas industry analysis: the IMPLAN model quantified the direct and indirect contributions of other unconventional gas activity, and the US Macroeconomic model enhanced IMPLAN’s standard methodology by measuring the induced economic contribution. Measuring the Economic Contributions Similar to the report on the shale gas industry’s economic contribution, IHS’ US macroeconomic forecast provided the baseline upon which to evaluate and assess the contributions to economic growth and tax revenues of other unconventional gas over the next 25 years. The findings of our study indicate that other unconventional gas production will undergo a strong initial expansion during the initial 10 years of the forecast period, followed by a slower and flatter growth path toward the middle and end of the 25-year forecast period. The initial ramp up of investment and production will trigger economic ripples that will make a positive contribution to the growth of the US economy. The growth in investment and production will moderate after the first decade but will continue to generate more modest economic and employment contributions. This section presents snapshots of the economic contribution of other unconventional gas activity in five-year increments, from 2010 to 2035. As in the companion report, we present a summary of the economic contribution in four key dimensions: employment, value added to GDP, labor income, and government tax revenues. For the contribution on employment, value added to GDP, labor income and tax revenues, we show the results in two ways: the contribution of “other” unconventional gas activity on the economy and the contribution of “total” unconventional gas activity, which includes the previously reported contribution of shale gas. For the contribution on value added to GDP per employee and labor income per employee, we show results only for other unconventional gas. US Economic Contribution Summary: Other Unconventional Gas* Employment (Number of workers) Direct 2010 2015 2020 2025 2030 2035 89,824 135,781 154,752 159,234 156,665 179,063 Indirect 133,289 196,297 223,936 230,063 226,179 259,704 Induced 184,195 261,687 292,746 300,280 295,130 340,021 407,30 593,765 671,434 689,577 677,974 778,787 Total Value Added ($M) D-16 2010 2015 2020 2025 2030 2035 Direct 22,822 29,944 32,135 32,827 32,236 37,477 Indirect 15,885 22,940 25,940 26,625 26,170 30,112 Induced 17,818 25,418 28,486 29,225 28,725 33,079 Total 56,525 78,302 86,561 88,677 87,131 100,667 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES US Economic Contribution Summary: Other Unconventional Gas* (Continued) Labor Income ($M) 2010 2015 2020 2025 2030 2035 10,315 14,302 15,749 16,137 15,858 18,308 Indirect 9,286 13,628 15,533 15,955 15,685 18,019 Induced 10,062 14,354 16,086 16,503 16,221 18,680 Total 29,662 42,284 47,368 48,595 47,764 55,007 Direct Source: IHS Global Insight NOTE: *Other unconventional gas includes gas from tight sands and coal bed methane. US Economic Contribution Summary: Total Unconventional Gas* Employment (Number of workers) 2010 2015 2020 2025 2030 2035 Direct 237,968 333,780 403,473 400,959 435,046 539,398 Indirect 326,999 479,487 583,817 598,495 644,444 806,810 Induced Total 443,690 650,182 797,484 812,501 871,325 1,092,669 1,008,657 1,463,449 1,794,775 1,811,954 1,950,815 2,438,877 Value Added ($M) 2010 2015 2020 2025 2030 2035 Direct 52,004 77,007 93,261 97,518 103,505 130,52 Indirect 38,301 56,441 69,779 70,793 76,021 95,346 Induced 43,101 63,069 77,363 78,706 84,456 105,862 133,405 196,516 240,403 247,017 263,982 331,728 2010 2015 2020 2025 2030 2035 Direct 24,755 36,028 43,717 44,834 47,974 60,162 Indirect 22,633 33,309 41,307 41,695 44,865 56,212 Induced 24,339 35,615 43,687 44,445 47,692 59,780 Total 71,727 104,951 128,711 130,974 140,531 176,154 Total Labor Income ($M) Source: IHS Global Insight NOTE: *Other unconventional gas includes gas from tight sands and coal bed methane. Employment Contribution IHS Global Insight estimates that other unconventional gas activity contributed more than 407,000 jobs in 2010. That will surge to 594,000 by 2015 and to 779,000 by 2035. A 7.8 percent annual growth rate]] during the early years of the forecast horizon will result from large capital investments in gas development that will spread throughout the broader US economy. In contrast to the shale gas industry, which exhibits a prolonged expansion that will boost the economy over the 25-year forecast, other unconventional gas activity shows a stronger ramp up during the initial decade, followed by slower growth in 2020 through 2035, which will nevertheless provide a stable contribution to the US economy. IHS D-17 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES This initial surge in direct economic activity in the mining, construction, and manufacturing industries will require support from the other unconventional gas supplier chain, which will generate jobs and incomes for workers, thereby inducing impacts in manufacturing and services jobs, as well as retail and wholesale trade. The fact that a limited number of jobs will be in the mining sector (where natural gas extraction jobs are categorized) illustrates that the disproportionate contribution of this industry extends far beyond the industry itself (additional industry-level detail is provided in Appendix B). Value Added to GDP and Labor Income Contributions The often cited US GDP is simply the summation of value added across all products and services produced in the United States. GDP is generally considered the broadest measure of the health of the US economy. Value added is the difference between the production cost of the products or services and the sales price (in other words, total value added is revenue less purchases of material and services). Thus, assessing the value added contribution of other unconventional gas activity demonstrates the vital role it plays in the overall US economy. Also discussed in the December 2011 report on shale gas, a common measure of the relative contribution of an industry to the overall economy is the value added per worker. The higher the ratio, the greater the contribution to GDP made by each worker. In 2010, the average employee who participates directly in production of other unconventional gas contributed just over $254,000. The contribution stays high, at nearly $221,000 in 2015 and just about $210,000 in 2035 due to the ongoing flow of capital expenditures associated with unconventional gas development. This contribution is dramatically higher than for the average workers in the US economy overall: the national average “value added” per employee in 2010 was $112,000 and is projected to be $118,000 in 2015. The higher value added nature of the jobs attributable to this sector indicates this sector is a potential growth engine of the US economy over the forecast period. Note that there is a modest downward trend in direct value added and labor income per employee. This is due to a small shift in the mix of capital expenditures over the period from more labor intensive activity to less labor intensive activity. Government Revenues and Taxes An Economic Growth Engine In 2010, the average direct employee in the other unconventional gas industry contributed $254,000 in "value added" contributions to the US economy. By 2015, this contribution will continue to outpace economy-wide growth. The relatively higher average "value added" nature of the jobs attributable to this sector indicates this sector is a potential growth engine of the US economy over the forecast period. US Contribution Per Employee: Other Unconventional Gas* Value Added ($) Direct Indirect Induced Total 2010 2015 2035 254,073 119,178 96,734 138,777 220,531 116,862 97,133 131,873 209,295 115,946 97,284 129,262 2010 114,833 69,666 54,625 72,825 2015 105,334 69,425 54,851 71,213 2035 102,246 69,382 54,937 70,631 Labor Income ($) Direct Indirect Induced Total Source: IHS Global Insight Increased commercial activity associated with NOTES: Figures in the table are average ratios by category and are not intended to sum to the total. other unconventional gas will increase govern*Other unconventional gas includes gas from tight sands and coal bed ment taxes paid by natural gas and oil producmethane. ers, their employees, and the extensive supply chain and ancillary industries. As depicted in the table below, IHS Global Insight estimates that annual government revenues from other unconventional gas activity will be just over $15 billion in 2010 alone, comprising nearly half of the taxes paid as a result of commercial activity associated with total unconventional gas. Taxes paid as a result of activity associated with other unconventional gas will rise to nearly $23 billion in 2020 and just about $28 billion D-18 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES by 2035; it will become a smaller share of unconventional gas total payments as tax payments resulting from shale gas activity increase due to rapid growth. With respect to the federal royalty payments, it should be noted that the share of federal government land leased by the operators for other unconventional gas activity is greater than for shale gas. Between 32 percent and 40 percent of other unconventional gas production is subject to federal royalty payments; in dollar terms, they were about $700 million in 2010 and will grow to $952 million in 2020 and to $1.5 billion in 2035. Royalty payments to the federal government also indirectly support state budgets, which will benefit based on each state’s participation in the production of natural gas on federal land and offshore areas. Other unconventional gas producers also pay lease payments to private landowners, which were forecast to reach $239 million in 2015 and more than $484 million by 2035. While these payments were considered for their impact on government revenues, they were excluded in IHS Global Insight’s estimates of economic impacts. Contribution to US Government Revenue and Private Lease Payments: Other Unconventional Gas* ($M) 2010 2015 2020 2025 2030 2035 2010-2035 6,888 9,733 10,862 11,138 10,946 12,619 262,165 Personal Taxes 5,266 7,557 8,494 8,717 8,568 9,861 204,498 Corporate Taxes 1,623 2,176 2,368 2,421 2,378 2,758 57,667 7,597 10,121 10,897 11,608 11,930 13,690 276,003 Federal Taxes State and Local Taxes Personal Taxes 906 1,292 1,448 1,486 1,460 1,681 34,897 Corporate Taxes 4,568 6,126 6,665 6,816 6,695 7,763 162,342 Severance Taxes 1,403 1,728 1,749 2,038 2,293 2,566 48,956 720 975 1,036 1,269 1,482 1,679 29,808 Ad Valorem Taxes Federal Royalty Payments Total Government Revenue Lease Payments to Private Landowners 700 916 952 1,159 1,359 1,539 27,524 15,185 20,770 22,711 23,906 24,236 27,847 565,692 127 239 311 372 425 484 8,263 Source: IHS Global Insight NOTE: *Other unconventional gas includes gas from tight sands and coal bed methane. Contribution to US Government Revenue and Private Lease Payments: Total Unconventional Gas* ($M) Federal Taxes Personal Taxes Corporate Taxes 2010 2015 2020 2025 2030 2035 2010-2035 16,509 24,231 29,712 30,329 32,499 40,776 727,067 12,779 18,699 22,966 23,321 25,043 31,382 560,548 3,731 5,533 6,746 7,008 7,455 9,394 166,519 16,422 23,948 28,829 31,068 33,952 42,226 735,607 Personal Taxes 2,191 3,206 3,933 4,001 4,293 5,381 96,093 Corporate Taxes 10,540 15,586 18,978 19,707 20,971 26,411 468,584 Severance Taxes 2,578 3,555 4,078 5,038 5,927 7,136 117,277 Ad Valorem Taxes 1,112 1,601 1,841 2,323 2,761 3,298 53,653 861 1,155 1,245 1,522 1,799 2,122 36,057 33,792 49,335 59,786 62,918 68,250 85,123 1,498,731 306 525 741 825 1,049 1,325 19,777 State and Local Taxes Federal Royalty Payments Total Government Revenue Lease Payments to Private Landowners Source: IHS Global Insight NOTE: *Other unconventional gas includes gas from tight sands and coal bed methane. IHS D-19 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES 5. Conclusion The same technologies that have expanded the development of the nation’s shale gas fields have led to the development of other, non-shale types of unconventional gas. This study forecasts steady production of other unconventional gas—tight sands and CBM—during the next 25 years and the economic benefits of this growth throughout the US economy. IHS Global Insight has found that these benefits include increases in investment, more job opportunities, and higher economic productivity. In 2010, unconventional gas activity (shale and other) represented 53 percent of US natural gas production. By 2035, the unconventional gas share of total natural production will be 79 percent. The industry’s increased importance to the economy will be driven by strong growth in shale gas production, but it will be supported by a stable foundation of other unconventional gas production. The following is an inventory of the economic and government revenue contributions resulting from the continued development of other unconventional gas: • A total of $1.3 trillion in capital investments are expected during the 25-year period 2010 through 2035. • In 2010, other unconventional gas activity supported 407,000 jobs; by 2015 this will grow to nearly 594,000 and, by 2035, to nearly 779,000. Given that overall unconventional gas activity supported more than 1 million jobs in 2010, 1.5 million jobs in 2015, and 2.4 million jobs in 2035, other unconventional gas represents 40 percent, 41 percent, and 32 percent of the overall unconventional gas industry’s employment contributions respectively over the forecast horizon. • The other unconventional gas contribution to GDP exceeded $57 billion in 2010. This will surge to $78 billion by 2015 and to $101 billion in 2035. • In 2010, other unconventional gas production added just over $15 billion in government tax receipts, and this will approach $28 billion in 2035. Over the entire 25-year forecast period, other unconventional gas will generate nearly $566 billion in government tax revenues. At a time that the US economy is struggling to pull out of the Great Recession and create enough jobs to reduce the high US unemployment rate, a thriving natural gas industry based on strong production of other unconventional sources of gas will be a contributor to future employment prospects and the health of the US economy. D-20 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Appendix A. Future Production and Capital Expenditure Outlook: Other Unconventional Gas IHS CERA’s estimates for production outlooks for non-shale, or “other,” unconventional gas plays, shown in detail in this appendix, followed the same procedure as for the shale plays discussed in the previous report. Play-level production profiles and well construction costs were developed from IHS CERA’s proprietary databases and internal research. Estimates of play-level productive capacity were constrained to ensure consistency with IHS CERA’s outlook for natural gas demand, price, and infrastructure as reported in its September 2011 report, “North American Natural Gas Market Briefing.” Production Profiles The variables used to derive production profiles for each play were obtained from IHS databases and internal research. These variables include: 1. Rig count (including ramp up, maximum rigs, time at plateau, ramp down) 2. Number of days to drill a well 3. Type curves showing production decline rates over time 4. Acreage (total area to be developed) 5. Well spacing 6. Likelihood of geologic success. The number of possible locations to be developed was derived from the last three items. Type curves were derived for each play using the IHS databases (Enerdeq, Power Tools, and ArcGIS) and are based on actual well data. The three driving variables in a type curve are initial production, estimated ultimate recovery per well, and the rate of decline of the well. Number of days to drill a well (including mobilization and demobilization of the rigs) was obtained from well data available in IHS databases. IHS CERA developed rig forecasts for each play based on historic rig counts and rig counts for 2011, as well as per-well economics of each individual play. Well Capital Expenditures Capital expenditures associated with unconventional gas depend on well costs, which were estimated using IHS CERA proprietary databases. Well capital expenditures were divided into the following three main categories, each of which was further subdivided as detailed below: Drilling Completions Facilities 40% 50% 10% Drilling Capital Expenditure was further subdivided into the following categories: Steel Consumables Rigs Site Preparation Cement Rig Labor Other* IHS 21% 21% 21% 12% 9% 7% 9% Lining, casing, tubing Bits, rig consumables (mud etc.) Rig rental Rig crew D-21 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES * Other” drilling capital expenditures are further divided into the following subcategories: Insurance Land Lease Finding and Development (including seismic) Other Drilling Contingencies 40% 20% 20% 20% Completions capital expenditures were further subdivided into the following categories: Hydraulic Fracturing Materials Hydraulic Fracturing Rentals* Equipment Labor Hydraulic Fracturing Other Other 38% 25% 15% 8% 5% 9% Proppants, fluids Equipment, rig rentals Xmas trees, well heads, sleeves, packers Well testing crew Generators, catering, onsite containers Contingency and insurance *Hydraulic fracturing related rentals are further divided into the following subcategories: Equipment Labor 80% 20% Facilities capital expenditures were further subdivided into the following categories: Materials and Equipment Fabrication Project Management Other* 60% 25% 5% 10% Fuel, insurance, permits etc. Capital expenditures for mid-stream gathering infrastructure were assumed to be $500,000 per well and this includes capital for separators, dehydrators, headers and flares, battery compression, and main compression. It was assumed that 12 wells were drilled per pad with battery compression and that 10 batteries were connected to each main compression with additional pipelines to the central processing facility. Gathering lines of 1.5 miles of 8 inch diameter were assumed from the well pad to main compression, with another 10 miles of 12-inch diameter lines to the central processing at the tie in to the interstate pipeline system. This midstream capital expenditure is broken down as follows, on a per-well basis: Component D-22 Cost/Well Allocation Assumptions Separators/dehydrators/motor control center/headers & flares $28,000 5.6% Battery compression $219,000 43.8% Based on compression costs of $2,189/installed hp and 100 hp/mmcf/d of production, average production of 1 mmcf/d/well Main compression $109,000 21.8% Based on compression costs of $2,189/installed hp and 50 hp/mmcf/d of production Pipelines $54,000 10.8% Gathering lines of 8'' (@ $201k/mi) for 1.5 miles from pad to central compression and 12'' (@ $241k/mi) for 10 miles to gas processing plant Processing $90,000 18.0% $8.9 MM per plant Total $500,000 100% JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES All capital costs were escalated using a normalized version of the Upstream Capital Costs Index developed by IHS CERA to reflect projected cost increases for the inputs to oil and gas development. North American Modeling Methodology and Process Description IHS CERA developed the outlook in this study for the US natural gas market using its Integrated Modeling System. This approach was required in order to assess the production outlook in the context of overall market supply and demand. In other words, when potential supply greatly exceeds demand, as is the case today, simply having the capability to understand the geologic potential of the various natural gas plays is insufficient to predict production capacity. A prediction of operator behavior must be tested against what the market can bear using system-wide modeling of the entire North American market, which refers to the integrated markets in the United States, Canada, and Mexico. IHS CERA’s Integrated Modeling System for North America employs a number of analytical models: the AURORA™ power market simulation model and the Gas Pipeline Competition Model (GPCM™), both using proprietary IHS CERA inputs; as well as our expert analysis of environmental policies and markets. IHS CERA also incorporates its upstream and downstream oil analytical frameworks. These models and analyses are used as a basis for IHS CERA’s own gas, power and oil services, and they are regularly maintained by a team of qualified researchers. Power Market Module IHS CERA Capacity Expansion Model Electric sector coal demand forecast AURORATM IHS CERA Scenarios Database Electric sector natural gas demand forecast IHS CERA Productive Capacity Oil price Model forecast IHS CERA Capacity Price Model IHS CERA Coal Market Analysis IHS CERA Emissions Market Analysis Emissions permit price forecast, coal price forecast IHS CERA IHS Global Insight Power Demand Macroeconomic Natural gas Model Regional Outlook price forecast Economic Growth Natural Gas Market Module GPCMTM IHS CERA Gas Market Database Regional Economic Growth IHS CERA Gas Demand Model LNG price forecast IHS CERA Global Oil Outlook Oil price forecast IHS CERA Global LNG Outlook North American Gas Modeling Methodology IHS CERA’s natural gas projections are developed based upon several detailed analytical models as well as judgments formed by IHS CERA’s research. The projections cover the integrated North America market. Natural gas supply estimates are stated in terms of productive capacity at the wellhead, as opposed to production. These estimates are developed at a play level. The basic approach is to assess the geologic potential of the producing area, projects known to be under development, the potential results of new development activity, and anticipated changes in the investment behavior of major producers. Assessments of geological potential take into consideration both oil and gas reserves. New development activity is projected by using trends in initial production rates, decline rates, and reserve amounts associated with each completion. The investment behavior of major producers is a major factor in the projection of productive capacity. IHS CERA estimates this effect based on its conversations with various companies as well as on its observations of behavior by the same companies. IHS D-23 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES The methodology IHS CERA employs to develop its supply forecast has been enhanced by its completion of several multi-client studies including: “Diminishing Returns: The Cost of North American Gas Supply in an Unconventional Era” (February 2007); “Rising to the Challenge” (February 2009); “Fueling North America’s Energy Future” (January 2010); and “Cream of the Crop” (February 2010). These studies made extensive use of the IHS well and production database to develop an understanding of the resource base and cost picture for North American gas supply. It is important to note that costs were calculated utilizing the entire IHS catalogue of North American well and production information, rather than from a subset of wells or from a collection of publications. Selected thirdparty rig and cost information was purchased to augment the IHS databases. Finally, IHS CERA made several benchmarking efforts to check calculated estimates. The result is a productive capacity outlook for 284 individual plays, which were then consolidated into 130 basins or sub-basins. The analysis has produced, among other insights, a detailed understanding of initial production rates and decline curves by play, and is used to estimate rig activity on a localized basis. IHS CERA’s North American Natural Gas and Global LNG groups develop the LNG import outlook jointly within the context of a global supply/demand balance for LNG. These projections take into consideration price, regulatory hurdles, and conditions in the global LNG market that may impose constraints on LNG import levels. Residential and commercial demand is forecast based on weather normalized to a rolling 15-year historical period and then projected to the state level. The demand forecast is influenced by several other variables including GDP growth, efficiency gains, and market penetration by gas, as opposed to other fuels. Industrial demand is developed on a state basis by examining the economic role played by gas in key industrial sectors, as well as through regression analyses. Projections of future gas use are made based on numerous factors, including GDP growth, projected growth by industry sector, the impact of gas prices on margins in the sector, fuel switching potential and activity, and plant closures. In this effort, IHS CERA makes use of detailed macroeconomic forecasts produced by IHS Global Insight. Gas burned in the generation of electricity is estimated based on a dispatch model (Aurora) maintained by the North American Electric Power Team. The dispatch model analyzes North American’s power industry by assessing future activity in local markets. In certain states, such as those with large metropolitan areas or significant gas transmission constraints, demand and supply projections are broken down geographically below the state level. This process involves allocations that take into account historical activity levels, population trends, manufacturing employment, local seasonality, and the addition or retirement of industrial or generation facilities. The projected figures are reviewed on a continental basis to assess the reasonableness of the overall supply/demand balance. Upon completion of this review, one or more of the preceding steps may be revisited. Detailed analysis follows satisfactory balancing of the continental aggregates. The allocated state level detail is loaded into the RBAC’s GPCM™ (Gas Pipeline Competition Model) system. The GPCM™ system, developed in 1997, has been commercially available since 1998 and is widely used in the gas industry to assess market fundamentals, including flows and prices. A key member of IHS CERA’s North American Natural Gas team, working with the software developer, developed the specifications for the system and generated the original database for the GPCM™ system. GPCM™ is a network linear programming system designed to optimize flows across complex systems such as pipeline networks. In addition to IHS CERA’s supply and demand projections, the system requires a model of the North American gas grid to produce results. The grid model provided by the software developer has been customized by IHS CERA based upon a variety of publicly available data, including pipeline schematics filed by interstate pipelines with the US government (now no longer publicly available), data from pipeline bulletin boards, regulatory filings, US Energy Information Administration data, federal data on storage activity, a census of storage facilities performed by Natural Gas Intelligence, the American Gas Association Survey of Underground Storage of Natural Gas, IHS CERA’s assessment of discounting behavior, and conversations with industry personnel. D-24 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES The GPCM™ system develops an equilibrium set of spot prices and flows based on the specified inputs. The objective function seeks to maximize the sum of producer and consumer surpluses less transportation costs. IHS CERA maintains a proprietary version of supply and demand projections and an outlook for infrastructure expansions that are the product of our independent research and analysis. These projections are then entered into IHS CERA’s customized GPCM™ database. As of June 2011, IHS CERA’s GPCM™ database included 207 North America pipelines broken into 932 pipeline segments. The model also includes 439 storage facilities. Connecting these elements are 3,688 nodes. Demand is modeled in 110 geographic areas for each of the four customer classes. Supply is forecast for 275 plays throughout North America, which are then aggregated into 178 producing regions for modeling purposes. These producing regions are spread over 130 geographic locations. Model output includes a flow and a price for each location for each month, which IHS CERA summarizes into several standard reports. However, data can be mined below the detail included in the standard reports. It is important to note that the degree to which the model can discriminate between geographic areas in terms of price or flows is limited by the level of detail specified for supply, demand, and infrastructure. While several detailed models are used in the development of a projection, the results that IHS CERA ultimately reports to a client represent IHS CERA’s best judgment informed by the analysis performed, and do not necessarily agree with model output. For example, IHS CERA may, in its judgment, adjust the output obtained to account for market conditions that differ from those that would be obtained in a purely spot market. The tables provided on the following pages present our estimates of other unconventional gas production and its share of overall natural gas production in the US lower 48 states over the 2010-2035 period (Table A.1); snapshots of US annual capital expenditures, in five-year increments, associated with other unconventional gas development (Table A.2); and cumulative totals, over five year periods, of capital expenditures associated with other unconventional gas development (Table A.3) (please note that the sum across all of the capital expenditure columns in Table A.3 does not match the total capital expenditure for years 2010 through 2035 in Table A.2 because Table A.2 includes an extra year (2010)). Table A.1 US Lower 48 Annual Natural Gas Production and Well Completions: Other Unconventional Gas* vs. Total Gas 2010 2015 2020 2025 2030 2035 5,512,297,522 5,528,478,777 5,458,495,669 5,572,393,935 5,704,099,381 5,925,977,626 3,919,979,770 4,189,135,644 4,345,136,944 4,567,079,807 4,744,306,084 4,968,805,590 1,592,317,752 1,339,343,133 1,113,358,725 1,005,314,129 959,793,297 957,172,036 21,229,024,284 23,276,996,872 26,000,032,080 27,769,207,506 29,114,085,717 31,263,775,082 PRODUCTION Other Uncon. Gas (Mcf) Tight Sands Coal Bed Methane Total Gas (Mcf) Other Uncon. Share of Total 26% 24% 21% 20% 20% 19% 1,597 2,356 2,587 2,318 2,234 2,198 1,163 1,899 1,925 1,683 1,623 1,599 434 457 662 635 611 600 17,858 18,344 19,532 17,355 16,213 16,224 9% 13% 13% 13% 14% 14% 4.38 4.77 4.57 4.84 4.91 5.15 WELL COMPLETIONS Other Uncon. Gas Tight Sands Coal Bed Methane Total Gas Other Unconventional Share of Total Henry Hub Price (Constant 2010 $US per MMBtu) Source: IHS CERA and EIA NOTE: *Other unconventional gas includes gas from tight sands and coal bed methane. IHS D-25 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Table A.2 US Annual Capital Expenditure by Type: Other Unconventional Gas* ($M) 2010 2015 2020 2025 2030 2035 Total 2010-2035** 7,046 13,278 17,281 20,708 23,615 26,837 476,363 Drilling 4,721 8,896 11,578 13,874 15,822 17,981 319,163 Support Services 2,325 4,382 5,703 6,834 7,793 8,856 157,200 Drilling Capital Expenditure Completion Capital Expenditure 8,807 16,597 21,601 25,885 29,519 33,547 595,454 Hydraulic Fracturing 7,046 13,278 17,281 20,708 23,615 26,837 476,363 Other 1,761 3,319 4,320 5,177 5,904 6,709 119,091 1,761 3,319 4,320 5,177 5,904 6,709 119,091 1,057 1,992 2,592 3,106 3,542 4,026 71,454 440 830 1,080 1,294 1,476 1,677 29,773 88 166 216 259 295 335 5,955 Facilities Capital Expenditure Material Fabricaton Project Management Other TOTAL Upstream Capital Expenditure Infrastructure Capital Expenditure Gathering and Processing TOTAL CAPITAL EXPENDITURE 176 332 432 518 590 671 11,909 17,614 33,195 43,202 51,770 59,037 67,093 1,190,908 1,630 2,903 3,890 4,659 5,307 6,010 106,605 1,630 2,903 3,890 4,659 5,307 6,010 106,605 19,244 36,097 47,092 56,429 64,344 73,104 1,297,513 Source: IHS CERA NOTES: *Other unconventional gas includes gas from tight sands and coal bed methane. **Total 2010-2035 represents the total for all years including those years not reported. Table A.3 US Five Year Cumulative Totals of Capital Expenditure by Type: Other Unconventional Gas* ($M) 2011-2015 2016-2020 2021-2025 2026-2030 2031-2035 54,367 7,329 99,661 110,923 127,037 Drilling 36,426 51,810 66,773 74,319 85,115 Support Services 17,941 25,519 32,888 36,605 41,922 Drilling Capital Expenditure Completion Capital Expenditure 67,958 96,661 124,577 138,654 158,797 Hydraulic Fracturing 54,367 77,329 99,661 110,923 127,037 Other 13,592 19,332 24,915 27,731 31,759 Facilities Capital Expenditure 13,592 19,332 24,915 27,731 31,759 Material 8,155 11,599 14,949 16,639 19,056 Fabricaton 3,398 4,833 6,229 6,933 7,940 680 967 1,246 1,387 1,58 1,359 1,933 2,492 2,773 3,176 135,916 193,322 249,153 277,309 317,593 11,979 17,097 22,285 25,128 28,484 Project Management Other TOTAL Upstream Capital Expenditure Infrastructure Capital Expenditure Gathering and Processing TOTAL CAPITAL EXPENDITURE 11,979 17,097 22,285 25,128 28,484 147,896 210,419 271,439 302,437 346,077 Source: IHS CERA NOTE: *Other unconventional gas includes gas from tight sands and coal bed methane. D-26 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Appendix B. Economic Contribution Assessment Detailed Tables: Other Unconventional Gas Appendix B contains two summary tables showing the impact on the US economy and government revenues generated by other, non-shale, unconventional gas activity. It also contains eight tables that provide the distribution of these impacts at various levels, including industries outside of the energy industry—retail, real estate, services and others—that are slated to benefit from growth in unconventional gas activity. Table B.1 provides an aggregate view of our findings for other non-shale unconventional gas in five-year increments over the forecast horizon (2010, 2015, 2020, 2025, 2030, and 2035) for direct, indirect and induced contributions for the following concepts: employment, value added to US GDP, and labor income. Table B.2 provides estimated tax revenues from non-shale unconventional gas activity for the same five-year increments from federal, state and local sources, and separately from lease and federal royalty sources. Tables B.3 through B.5 present the same results for other unconventional gas– employment, value added and labor income—disaggregated by industry. Table B.3 presents estimates of employment contributions on a direct, indirect, and induced basis, by industry, for each five-year increment from 2010 through 2035. Tables B.4 and B.5 contain estimates of value added to GDP and labor income contributions, respectively, on a similar basis, that is, on a direct, indirect, and induced basis by industry for each five-year increment. To provide some additional context, Appendix B also provides this data for total unconventional gas, specifically other unconventional gas plus shale gas. Table B.6 provides the economic contributions of total unconventional gas activity, in five-years increments from 2010 through 2035, for direct, indirect and induced contributions for the following concepts: employment, value added to US GDP, and labor income. Table B.7 provides estimated tax revenues from total unconventional gas activity, for the same five-year increments from federal, state and local sources, and separately from lease and federal royalty sources. Tables B.8 through B.10 present the same results for total unconventional gas– employment, value added and labor income—disaggregated by industry. Table B.8 presents estimates of employment contributions on a direct, indirect, and induced basis, by industry, for each five-year increment from 2010 through 2035. Tables B.9 and B.10 contain estimates of value added to GDP and labor income contributions, respectively, on a similar basis, that is, on a direct, indirect, and induced basis by industry for each five-year increment. IHS D-27 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Other Unconventional Gas Table B.1 US Economic Contribution Summary: Other Unconventional Gas* Employment (Number of workers) Direct 2010 2015 2020 2025 2030 2035 89,824 135,781 154,752 159,234 156,665 179,063 Indirect 133,289 196,297 223,936 230,063 226,179 259,704 Induced 184,195 261,687 292,746 300,280 295,130 340,021 407,30 593,765 671,434 689,577 677,974 778,787 2010 2015 2020 2025 2030 2035 Direct 22,822 29,944 32,135 32,827 32,236 37,477 Indirect 15,885 22,940 25,940 26,625 26,170 30,112 Induced 17,818 25,418 28,486 29,225 28,725 33,079 Total 56,525 78,302 86,561 88,677 87,131 100,667 2010 2015 2020 2025 2030 2035 Total Value Added ($M) Labor Income ($M) Direct 10,315 14,302 15,749 16,137 15,858 18,308 Indirect 9,286 13,628 15,533 15,955 15,685 18,019 Induced 10,062 14,354 16,086 16,503 16,221 18,680 Total 29,662 42,284 47,368 48,595 47,764 55,007 Source: IHS Global Insight NOTE: *Other unconventional gas includes gas from tight sands and coal bed methane. Table B.2 Contribution to US Government Revenue and Private Lease Payments: Other Unconventional Gas* ($M) 2010 2015 2020 2025 2030 2035 2010-2035 6,888 9,733 10,862 11,138 10,946 12,619 262,165 Personal Taxes 5,266 7,557 8,494 8,717 8,568 9,861 204,498 Corporate Taxes 1,623 2,176 2,368 2,421 2,378 2,758 57,667 7,597 10,121 10,897 11,608 11,930 13,690 276,003 906 1,292 1,448 1,486 1,460 1,681 34,897 Corporate Taxes 4,568 6,126 6,665 6,816 6,695 7,763 162,342 Severance Taxes 1,403 1,728 1,749 2,038 2,293 2,566 48,956 720 975 1,036 1,269 1,482 1,679 29,808 700 916 952 1,159 1,359 1,539 27,524 15,185 20,770 22,711 23,906 24,236 27,847 565,692 127 239 311 372 425 484 8,263 Federal Taxes State and Local Taxes Personal Taxes Ad Valorem Taxes Federal Royalty Payments Total Government Revenue Lease Payments to Private Landowners Source: IHS Global Insight NOTE: *Other unconventional gas includes gas from tight sands and coal bed methane. D-28 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Table B.3 US Employment Contribution by Industry: Other Unconventional Gas* (Number of workers) 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And Wholesale Trade Service Government Total Direct 0 42,689 16,303 23,921 4,650 0 2,261 0 89,824 Indirect 983 3,894 11,127 20,279 12,628 11,378 71,148 1,851 133,289 Induced 4,224 483 1,803 9,923 10,247 36,889 118,150 2,478 184,195 Total 5,496 43,846 27,466 51,870 27,184 50,598 196,438 4,409 407,308 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And Wholesale Trade Service Government Total Direct 0 59,840 24,280 40,312 7,891 0 3,458 0 135,781 Indirect 1,540 5,343 13,298 31,689 19,351 17,388 104,896 2,793 196,297 Induced 6,014 687 2,561 14,112 14,563 52,375 167,852 3,522 261,687 Total 7,980 61,368 37,736 82,325 41,193 73,198 283,531 6,433 593,765 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And Wholesale Trade Service Government Total Direct 0 68,043 25,779 48,027 9,249 0 3,653 0 154,752 Indirect 1,797 5,840 13,509 36,985 22,467 20,203 119,917 3,219 223,936 Induced 6,736 770 2,865 15,794 16,295 58,573 187,772 3,942 292,746 Total 9,017 69,551 39,661 96,286 47,267 82,665 319,695 7,292 671,434 IHS D-29 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Table B.3 US Employment Contribution by Industry: Other Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And Wholesale Trade Service Government Total Direct 0 69,672 26,594 49,630 9,561 0 3,776 0 159,234 Indirect 1,851 5,981 13,721 38,100 23,119 20,789 123,193 3,310 230,063 Induced 6,910 789 2,938 16,202 16,715 60,078 192,605 4,043 300,280 Total 9,258 71,218 40,698 99,261 48,624 84,864 328,165 7,489 689,577 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And Wholesale Trade Service Government Total Direct 0 68,425 26,280 48,841 9,405 0 3,715 0 156,665 Indirect 1,821 5,876 13,457 37,479 22,734 20,446 121,112 3,255 226,179 Induced 6,791 776 2,888 15,924 16,428 59,048 189,301 3,974 295,130 Total 9,102 69,946 40,106 97,647 47,809 83,424 322,579 7,361 677,974 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And Wholesale Trade Service Government Total Direct 0 79,268 29,488 55,398 10,689 0 4,222 0 179,063 Indirect 2,079 6,797 15,839 42,762 26,022 23,386 139,089 3,731 259,704 Induced 7,823 894 3,327 18,344 18,926 68,033 218,095 4,578 340,021 Total 10,463 81,014 45,781 111,289 54,777 95,927 371,075 8,461 778,787 Source: IHS Global Insight NOTE: *Other unconventional gas includes gas from tight sands and coal bed methane. D-30 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Table B.4 US Value Added Contribution by Industry: Other Unconventional Gas* ($) 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And Wholesale Trade Service Government Total Direct 0 18,271,829,931 950,560,357 2,766,792,181 596,966,723 0 235,782,618 0 22,821,931,810 Indirect 48,542,195 1,296,287,157 702,369,854 2,476,174,373 2,161,377,776 1,248,774,750 7,799,349,498 152,230,882 15,885,106,483 Induced 217,760,891 261,976,768 136,393,430 1,460,574,995 1,759,381,935 2,735,147,021 11,019,933,973 226,743,657 17,817,912,670 Total 266,303,086 19,830,093,855 1,789,323,640 6,703,541,549 4,517,726,434 3,983,921,771 19,055,066,088 378,974,539 56,524,950,963 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And Wholesale Trade Service Government Total Direct 0 22,512,982,852 1,415,701,333 4,646,802,514 1,011,219,449 0 357,245,581 0 29,943,951,729 Indirect 75,901,344 1,745,751,364 839,346,650 3,863,140,242 3,210,465,247 1,951,687,417 11,026,227,578 227,052,019 22,939,571,860 Induced 311,223,920 374,209,062 194,426,885 2,086,353,155 2,511,456,596 3,900,661,780 15,716,412,530 323,596,010 25,418,339,937 Total 387,125,264 24,632,943,278 2,449,474,869 10,596,295,911 6,733,141,291 5,852,349,197 27,099,885,688 550,648,029 78,301,863,526 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And Wholesale Trade Service Government Total Direct 0 23,558,605,354 1,503,089,239 5,516,697,261 1,182,976,993 0 374,125,990 0 32,135,494,836 Indirect 88,644,235 1,892,274,010 852,636,017 4,515,546,705 3,673,058,545 2,296,188,993 12,361,415,937 260,042,703 25,939,807,145 Induced 349,106,453 419,641,297 217,807,764 2,339,687,144 2,815,437,347 4,370,718,174 17,610,713,801 362,722,474 28,485,834,455 Total 437,750,688 25,870,520,661 2,573,533,020 12,371,931,110 7,671,472,885 6,666,907,168 30,346,255,728 622,765,178 86,561,136,437 IHS D-31 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Table B.4 US Value Added Contribution by Industry: Other Unconventional Gas* (Continued) ($) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And Wholesale Trade Service Government Total Direct 0 23,965,971,791 1,550,630,379 5,700,766,578 1,222,821,387 0 386,727,081 0 32,826,917,216 Indirect 91,293,351 1,935,897,267 866,012,017 4,650,832,482 3,774,847,312 2,364,591,686 12,674,712,432 267,302,687 26,625,489,235 Induced 358,194,332 430,554,324 223,450,960 2,400,535,282 2,888,567,141 4,484,052,225 18,067,395,377 372,140,219 29,224,889,860 Total 449,487,683 26,332,423,383 2,640,093,356 12,752,134,341 7,886,235,840 6,848,643,911 31,128,834,890 639,442,907 88,677,296,312 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And Wholesale Trade Service Government Total Direct 0 23,510,263,420 1,532,295,610 5,609,982,815 1,202,893,732 0 380,424,870 0 32,235,860,447 Indirect 89,817,911 1,901,592,460 849,389,537 4,574,724,642 3,710,912,258 2,325,690,320 12,455,468,878 262,779,181 26,170,375,187 Induced 352,074,117 423,195,689 219,628,079 2,359,508,376 2,839,182,689 4,407,354,738 17,758,368,427 365,777,191 28,725,089,307 Total 441,892,028 25,835,051,570 2,601,313,226 12,544,215,834 7,752,988,678 6,733,045,058 30,594,262,176 628,556,372 87,131,324,941 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And Wholesale Trade Service Government Total Direct 0 27,595,365,782 1,719,329,744 6,363,000,776 1,367,038,087 0 432,336,871 0 37,477,071,260 Indirect 102,539,749 2,203,925,100 999,696,889 5,222,529,158 4,259,930,211 2,656,637,478 14,364,856,081 301,550,960 30,111,665,624 Induced 405,361,518 487,273,776 252,933,218 2,716,765,485 3,269,285,615 5,075,479,228 20,450,340,457 421,197,333 33,078,636,630 Total 507,901,266 30,286,564,657 2,971,959,852 14,302,295,419 8,896,253,914 7,732,116,706 35,247,533,409 722,748,293 100,667,373,515 Source: IHS Global Insight NOTE: *Other unconventional gas includes gas from tight sands and coal bed methane. D-32 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Table B.5 US Labor Income Contribution by Industry: Other Unconventional Gas* ($) 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And Wholesale Trade Service Government Total Direct 0 6,935,569,911 899,018,752 1,930,947,063 368,331,900 0 180,983,614 0 10,314,851,241 Indirect 26,657,954 526,077,426 667,802,312 1,594,941,536 1,061,807,586 730,659,428 4,535,204,214 142,472,789 9,285,623,245 Induced 94,706,258 99,109,217 111,695,308 868,419,360 916,501,047 1,635,186,806 6,119,808,593 216,269,385 10,061,695,974 Total 121,364,212 7,560,756,555 1,678,516,371 4,394,307,959 2,346,640,533 2,365,846,233 10,835,996,421 358,742,174 29,662,170,460 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And Wholesale Trade Service Government Total Direct 0 8,803,897,677 1,338,938,701 3,258,800,709 624,209,739 0 276,511,687 0 14,302,358,513 Indirect 41,585,217 709,639,304 797,847,983 2,499,484,742 1,591,147,932 1,141,120,817 6,632,585,522 214,521,148 13,627,932,667 Induced 135,323,250 141,569,230 159,263,912 1,239,902,098 1,307,757,927 2,331,894,011 8,729,432,356 308,604,395 14,353,747,180 Total 176,908,467 9,655,106,211 2,296,050,596 6,998,187,549 3,523,115,599 3,473,014,828 15,638,529,566 523,125,543 42,284,038,360 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And Wholesale Trade Service Government Total Direct 0 9,417,563,660 1,421,588,232 3,887,042,139 730,564,205 0 291,974,726 0 15,748,732,962 Indirect 48,512,336 770,224,602 810,350,193 2,925,524,826 1,828,930,809 1,342,021,434 7,560,756,889 246,909,515 15,533,230,604 Induced 151,777,555 158,757,570 178,440,979 1,390,125,055 1,465,755,468 2,612,854,223 9,782,427,413 345,893,793 16,086,032,056 Total 200,289,891 10,346,545,832 2,410,379,404 8,202,692,019 4,025,250,481 3,954,875,657 17,635,159,028 592,803,308 47,367,995,621 IHS D-33 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Table B.5 US Labor Income Contribution by Industry: Other Unconventional Gas* (Continued) ($) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And Wholesale Trade Service Government Total Direct 0 9,596,254,073 1,466,551,576 4,016,953,382 755,170,673 0 301,808,847 0 16,136,738,552 Indirect 49,958,531 788,030,340 823,049,601 3,013,806,744 1,880,298,853 1,381,966,676 7,764,237,826 253,901,925 15,955,250,496 Induced 155,726,961 162,886,214 183,066,534 1,426,246,914 1,503,800,597 2,680,601,729 10,036,183,977 354,872,311 16,503,385,237 Total 205,685,493 10,547,170,627 2,472,667,711 8,457,007,040 4,139,270,123 4,062,568,405 18,102,230,651 608,774,236 48,595,374,285 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And Wholesale Trade Service Government Total Direct 0 9,416,500,002 1,449,210,957 3,952,538,185 742,864,059 0 296,890,476 0 15,858,003,680 Indirect 49,154,668 774,080,775 807,249,136 2,964,568,431 1,848,603,592 1,359,229,740 7,632,355,472 249,624,671 15,684,866,485 Induced 153,065,864 160,102,325 179,934,996 1,401,865,583 1,478,085,795 2,634,750,506 9,864,538,196 348,804,121 16,221,147,387 Total 202,220,532 10,350,683,102 2,436,395,089 8,318,972,199 4,069,553,446 3,993,980,245 17,793,784,145 598,428,792 47,764,017,551 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And Wholesale Trade Service Government Total Direct 0 11,016,025,604 1,626,103,675 4,484,631,086 844,233,760 0 337,403,547 0 18,308,397,672 Indirect 56,108,974 897,016,627 950,131,821 3,382,930,609 2,120,312,133 1,552,711,053 8,773,407,213 286,205,704 18,018,824,135 Induced 176,236,705 184,344,050 207,215,395 1,614,198,565 1,702,063,605 3,034,171,468 11,359,705,152 401,658,088 18,679,593,028 Total 232,345,680 12,097,386,282 2,783,450,891 9,481,760,260 4,666,609,497 4,586,882,522 20,470,515,912 687,863,793 55,006,814,835 Source: IHS Global Insight NOTE: *Other unconventional gas includes gas from tight sands and coal bed methane. D-34 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Total Unconventional Gas Table B.6 US Economic Contribution Summary: Total Unconventional Gas* Employment (Number of workers) 2010 2015 2020 2025 2030 2035 Direct 237,968 333,780 403,473 400,959 435,046 539,398 Indirect 326,999 479,487 583,817 598,495 644,444 806,810 Induced 443,690 650,182 797,484 812,501 871,325 1,092,669 1,008,657 1,463,449 1,794,775 1,811,954 1,950,815 2,438,877 2010 2015 2020 2025 2030 2035 Direct 52,004 77,007 93,261 97,518 103,505 130,52 Indirect 38,301 56,441 69,779 70,793 76,021 95,346 Induced 43,101 63,069 77,363 78,706 84,456 105,862 133,405 196,516 240,403 247,017 263,982 331,728 2010 2015 2020 2025 2030 2035 Direct 24,755 36,028 43,717 44,834 47,974 60,162 Indirect 22,633 33,309 41,307 41,695 44,865 56,212 Induced 24,339 35,615 43,687 44,445 47,692 59,780 Total 71,727 104,951 128,711 130,974 140,531 176,154 Total Value Added ($M) Total Labor Income ($M) Source: IHS Global Insight NOTE: *Other unconventional gas includes gas from tight sands and coal bed methane. Table B.7 Contribution to US Government Revenue and Private Lease Payments: Total Unconventional Gas* ($M) 2010 2015 2020 2025 2030 2035 2010-2035 16,509 24,231 29,712 30,329 32,499 40,776 727,067 Personal Taxes 12,779 18,699 22,966 23,321 25,043 31,382 560,548 Corporate Taxes 3,731 5,533 6,746 7,008 7,455 9,394 166,519 16,422 23,948 28,829 31,068 33,952 42,226 735,607 Federal Taxes State and Local Taxes Personal Taxes 2,191 3,206 3,933 4,001 4,293 5,381 96,093 Corporate Taxes 10,540 15,586 18,978 19,707 20,971 26,411 468,584 Severance Taxes 2,578 3,555 4,078 5,038 5,927 7,136 117,277 Ad Valorem Taxes 1,112 1,601 1,841 2,323 2,761 3,298 53,653 Federal Royalty Payments Total Government Revenue Lease Payments to Private Landowners 861 1,155 1,245 1,522 1,799 2,122 36,057 33,792 49,335 59,786 62,918 68,250 85,123 1,498,731 306 525 741 825 1,049 1,325 19,777 Source: IHS Global Insight NOTE: *Other unconventional gas includes gas from tight sands and coal bed methane. IHS D-35 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Table B.8 US Employment Contribution by Industry: Total Unconventional Gas* (Number of workers) D-36 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 94,223 64,220 62,867 11,207 0 5,451 0 237,968 Indirect 2,559 9,059 23,941 52,525 31,267 29,046 174,090 4,512 326,999 Induced 10,186 1,165 4,343 23,915 24,688 88,829 284,595 5,970 443,690 Total 13,034 101,227 90,736 137,053 66,822 120,206 469,015 10,563 1,008,657 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 148,625 68,919 91,318 17,326 0 7,591 0 333,780 Indirect 3,699 13,414 35,659 75,432 46,240 42,008 256,334 6,701 479,487 Induced 14,927 1,707 6,364 35,045 36,177 130,169 417,046 8,749 650,182 Total 19,052 159,244 108,539 198,008 99,130 175,612 688,297 15,567 1,463,449 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 190,114 67,909 114,706 22,039 0 8,705 0 403,473 Indirect 4,593 16,341 42,447 93,507 57,940 52,175 318,431 8,383 593,817 Induced 18,318 2,094 7,805 42,994 44,377 159,636 511,527 10,732 797,484 Total 23,395 203,448 115,670 246,687 123,612 215,701 847,016 19,246 1,794,775 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Table B.8 US Employment Contribution by Industry: Total Unconventional Gas* (Continued) (Number of workers) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 196,314 64,768 110,315 21,191 0 8,370 0 400,959 Indirect 4,535 16,837 45,752 92,287 57,722 51,944 321,025 8,393 598,495 Induced 18,650 2,132 7,953 43,790 45,207 162,674 521,163 10,932 812,501 Total 23,682 210,060 115,918 241,721 123,350 218,615 859,149 19,460 1,811,954 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 209,150 72,574 120,950 23,205 0 9,166 0 435,046 Indirect 4,929 17,973 47,983 100,211 62,420 56,222 345,649 9,056 644,444 Induced 20,005 2,287 8,528 46,966 48,483 174,438 558,893 11,724 871,325 Total 25,423 224,280 126,566 263,531 133,350 234,591 922,160 20,914 1,950,815 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 265,089 82,946 150,494 29,297 0 11,572 0 539,398 Indirect 6,135 22,633 60,846 124,680 78,142 70,064 432,953 11,357 806,810 Induced 25,085 2,868 10,695 58,894 60,798 218,757 700,870 14,702 1,092,669 Total 31,781 284,647 151,615 328,854 167,376 293,330 1,155,063 26,211 2,438,877 Source: IHS Global Insight NOTE: *Total unconventional gas includes gas from shale, tight sands, and coal bed methane. IHS D-37 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Table B.9 US Value Added Contribution: Total Unconventional Gas* ($) D-38 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 38,990,821,746 3,744,446,981 7,261,356,459 1,438,871,864 0 568,308,023 0 52,003,805,073 Indirect 127,150,503 2,996,071,128 1,511,158,988 6,362,682,461 5,228,579,332 3,175,044,400 18,531,923,644 368,115,842 38,300,726,298 Induced 527,272,610 634,146,322 329,797,458 3,535,551,577 4,257,303,191 6,615,137,812 26,652,953,214 548,602,250 43,100,764,434 Total 654,423,113 42,621,039,196 5,585,403,427 17,159,590,497 10,924,754,387 9,790,182,212 45,753,184,881 916,718,091 133,405,295,805 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 59,470,411,909 4,018,461,358 10,513,494,519 2,220,225,211 0 784,365,505 0 77,006,958,502 Indirect 183,130,931 4,426,886,284 2,250,758,829 9,203,773,792 7,763,526,485 4,647,192,273 27,418,406,380 547,172,139 56,440,847,113 Induced 771,556,551 927,941,672 482,584,599 5,173,547,532 6,229,657,535 9,679,774,945 39,000,729,435 802,761,935 63,068,554,203 Total 954,687,482 64,825,239,865 6,751,804,786 24,890,815,842 16,213,409,231 14,326,967,218 67,203,501,320 1,349,934,074 196,516,359,818 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 72,432,526,708 3,959,547,776 13,159,089,496 2,818,731,108 0 891,446,371 0 93,261,341,459 Indirect 227,137,324 5,372,023,635 2,679,192,351 11,457,734,252 9,677,192,749 5,841,719,616 33,841,672,100 682,611,238 69,779,283,266 Induced 946,816,861 1,138,583,031 591,858,198 6,347,975,078 7,642,649,607 11,872,782,050 47,837,067,348 984,792,399 77,362,524,572 Total 1,173,954,185 78,943,133,374 7,230,598,325 30,964,798,827 20,138,573,464 17,714,501,667 82,570,185,819 1,667,403,637 240,403,149,297 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Table B.9 US Value Added Contribution: Total Unconventional Gas* (Continued) ($) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 77,516,670,263 3,776,455,561 12,657,278,520 2,710,271,477 0 857,145,096 0 97,517,820,918 Indirect 224,387,631 5,567,252,082 2,887,849,629 11,327,321,399 9,735,494,438 5,784,567,079 34,580,740,614 685,807,914 70,793,420,785 Induced 962,703,133 1,157,886,991 602,275,840 6,455,543,536 7,773,816,671 12,080,071,510 48,671,698,284 1,001,763,959 78,705,759,923 Total 1,187,090,763 84,241,809,337 7,266,581,031 30,440,143,455 20,219,582,585 17,864,638,588 84,109,583,994 1,687,571,873 247,017,001,625 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 81,493,122,682 4,231,574,269 13,874,267,025 2,967,873,930 0 938,614,138 0 103,505,452,045 Indirect 243,857,218 5,929,782,003 3,028,688,687 12,290,792,903 10,486,166,804 6,271,344,361 37,031,040,581 739,005,474 76,020,678,030 Induced 1,033,269,337 1,242,676,371 646,219,014 6,928,292,919 8,342,411,299 12,962,163,383 52,225,962,132 1,075,005,947 84,456,000,403 Total 1,277,126,556 88,665,581,056 7,906,481,971 33,093,352,847 21,796,452,032 19,233,507,744 90,195,616,851 1,814,011,421 263,982,130,478 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 103,488,880,543 4,836,342,782 17,263,093,619 3,746,955,549 0 1,185,005,035 0 130,520,277,529 Indirect 303,283,129 7,469,699,469 3,840,561,623 15,309,207,272 13,157,495,447 7,824,369,987 46,514,006,556 927,467,930 95,346,091,414 Induced 1,295,044,785 1,557,544,359 810,033,260 8,683,764,061 10,456,517,757 16,247,687,988 65,463,599,336 1,347,444,390 105,861,635,935 Total 1,598,327,914 112,516,124,371 9,486,937,665 41,256,064,952 27,360,968,753 24,072,057,975 113,162,610,927 2,274,912,320 331,728,004,878 Source: IHS Global Insight NOTE: *Total unconventional gas includes gas from shale, tight sands, and coal bed methane. IHS D-39 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Table B.10 US Labor Income Contribution: Total Unconventional Gas* ($) D-40 2010 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 14,905,390,828 3,541,414,304 4,983,920,674 887,792,227 0 436,225,714 0 24,754,743,747 Indirect 70,592,935 1,217,548,501 1,436,602,317 4,106,089,651 2,587,096,068 1,857,966,198 11,010,450,407 346,729,923 22,633,076,001 Induced 229,287,878 239,906,766 270,117,288 2,101,615,154 2,217,258,606 3,954,731,220 14,802,784,290 523,220,839 24,338,922,041 Total 299,880,813 16,362,846,094 5,248,133,910 11,191,625,479 5,692,146,902 5,812,697,419 26,249,460,411 869,950,762 71,726,741,790 2015 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 22,931,629,616 3,800,570,997 7,317,783,155 1,370,509,846 0 607,106,822 0 36,027,600,436 Indirect 100,880,113 1,799,223,332 2,139,720,020 5,936,599,157 3,835,728,138 2,718,390,883 16,263,038,600 514,956,806 33,308,537,048 Induced 335,515,888 351,053,834 395,256,680 3,075,269,727 3,244,478,933 5,786,863,711 21,660,636,367 765,621,087 35,614,696,226 Total 436,396,001 25,081,906,782 6,335,547,696 16,329,652,039 8,450,716,917 8,505,254,594 38,530,781,788 1,280,577,892 104,950,833,711 2020 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 28,286,082,582 3,744,851,852 9,249,868,629 1,740,747,316 0 695,700,951 0 43,717,251,330 Indirect 124,595,663 2,184,793,284 2,546,875,269 7,393,715,001 4,789,223,006 3,415,831,432 20,208,013,203 643,786,294 41,306,833,152 Induced 411,707,742 430,743,265 484,786,272 3,772,972,260 3,980,029,034 7,097,850,748 26,569,269,606 939,200,042 43,686,558,968 Total 536,303,405 30,901,619,132 6,776,513,394 20,416,555,889 10,509,999,356 10,513,682,180 47,472,983,760 1,582,986,336 128,710,643,451 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Table B.10 US Labor Income Contribution: Total Unconventional Gas* (Continued) ($) 2025 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 30,021,188,680 3,571,687,313 8,898,795,254 1,673,766,564 0 668,931,623 0 44,834,369,435 Indirect 123,100,696 2,263,241,325 2,745,436,901 7,297,769,809 4,804,978,208 3,382,988,747 20,432,109,872 644,933,956 41,694,559,516 Induced 418,645,380 438,045,212 493,277,038 3,837,472,274 4,048,832,355 7,221,857,445 27,031,406,201 955,427,580 44,444,963,485 Total 541,746,076 32,722,475,217 6,810,401,252 20,034,037,337 10,527,577,128 10,604,846,193 48,132,447,697 1,600,361,536 130,973,892,436 2030 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 31,658,120,250 4,002,128,411 9,748,602,036 1,832,852,591 0 732,511,517 0 47,974,214,805 Indirect 133,821,493 2,411,077,470 2,879,246,754 7,923,072,571 5,181,182,916 3,667,478,556 21,973,061,031 695,747,082 44,864,687,874 Induced 449,319,669 470,122,682 529,285,097 4,118,259,696 4,344,765,788 7,749,165,447 29,005,977,469 1,025,264,338 47,692,160,186 Total 583,141,163 34,539,320,402 7,410,660,262 21,789,934,303 11,358,801,295 11,416,644,002 51,711,550,017 1,721,011,420 140,531,062,865 2035 Agriculture Mining Construction Manufacturing Transportation and Utilities Retail And WholesaleTrade Services Government Total Direct 0 40,184,983,926 4,574,104,979 12,164,036,621 2,313,985,491 0 924,799,454 0 60,161,910,471 Indirect 166,161,555 3,036,749,571 3,651,106,261 9,867,740,597 6,496,171,815 4,575,521,115 27,546,379,045 872,626,544 56,212,456,503 Induced 563,159,258 589,241,648 663,448,631 5,161,845,050 5,445,900,634 9,713,366,077 36,357,794,816 1,285,105,074 59,779,861,187 Total 729,320,812 43,810,975,145 8,888,659,871 27,193,622,267 14,256,057,941 14,288,887,192 64,828,973,315 2,157,731,618 176,154,228,161 Source: IHS Global Insight NOTE: *Total unconventional gas includes gas from shale, tight sands, and coal bed methane. IHS D-41 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Appendix C: IHS Global Insight Economic Contribution Assessment: Other Unconventional Gas Data Requirements and Assumptions IHS Global Insight, with support from IHS CERA, compiled the data required to undertake an economic contribution analysis of unconventional gas in the United States. Upstream unconventional gas was segmented to distinguish the economic activity for shale gas versus other unconventional gas in the United States. Other unconventional gas is comprised of coal bed methane and gas from tight sands formations. Both production and capital expenditure requirements were summed to undertake the economic contribution analysis. Similar to the shale gas sector, the following sector activities were determined to be the major, direct contributors for other unconventional gas: • Oil and natural gas extraction • Oil and natural gas drilling • Support activities for oil and natural gas • Construction of facilities, related materials and machinery for hydraulic fracturing and completions, and construction of natural gas pipeline For the IMPLAN model, forecasts of other unconventional gas production were transformed into the value of output using the corresponding Henry Hub price and conversion factor. Drilling capital expenditure and support services for gas operations directly correspond to sectors within the model. The breakdown of completion, facilities, gathering and processing, and pipeline construction were mapped to the detailed categories of the IMPLAN model. The final set of transformed capital expenditures for the IMPLAN model sectors are presented in Table C.2. For the US Macro model, production forecasts were transformed into quadrillion Btus by using corresponding conversion ratios. Drilling, completion, facilities, gathering and processing, and pipeline construction were summed to represent total investment in nonresidential structures for the mining and petroleum sector. This sector is a standalone investment category in the US Macro Model. All dollar estimates were transformed to 2005-based estimates and input into the US Macro Model (see Table C.3). To provide some context, the three tables described above are repeated for total unconventional gas. Table C.4 presents production, price and value for total unconventional gas. Table C.5 presents capital expenditures input to the IMPLAN model for total unconventional gas. Table C.6 presents inputs to the US Macro Model for total unconventional gas. This integrated approach methodology was used to undertake the economic contribution analysis for other unconventional gas. IMPLAN and the US Macro Model were used to arrive at the economic contributions and the process followed the same steps described in Appendix C of the shale gas report. D-42 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Other Unconventional Gas Table C.1 US Production, Price and Value: Other Unconventional Gas* 2010 2015 2020 Employment Production (Mcf) 2025 2030 2035 5,512,297,522 5,528,478,777 5,458,495,669 5,572,393,935 5,704,099,381 5,925,977,626 Tight Sands 3,919,979,770 4,189,135,644 4,345,136,944 4,567,079,807 4,744,306,084 4,968,805,590 Coal Bed Methane 1,592,317,752 1,339,343,133 1,113,358,725 1,005,314,129 959,793,297 957,172,036 4.38 5.18 5.42 6.21 6.89 7.90 24,766,904,691 29,353,983,019 30,335,287,344 35,519,374,808 40,342,909,571 48,038,587,174 Henry Hub Price (Nominal US$) Value of Production ($) Source: IHS CERA and EIA NOTE: *Other Unconventional gas includes gas from tight sands and coal bed methane. IHS D-43 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Table C.2 US Capital Expenditure Input to the IMPLAN Model: Other Unconventional Gas* IMPLAN Sector Description 2010 Capital Expenditure ($) DRILLING CAPEX 28 Drilling oil and gas wells 493,195,766 29 Support activities for oil and gas operations 1,542,998,181 36 Construction of other new nonresidential structures 1,479,587,297 160 Cement manufacturing 171 Steel product manufacturing from purchased steel 1,479,587,297 220 Cutting tool and machine tool accessory manufacturing 1,479,587,297 357 Insurance carriers 253,643,537 369 Architectural, engineering, and related services 126,821,768 63,410,884 COMPLETIONS CAPEX 26 Sand, gravel, clay, and ceramic and refractory minerals mining and quarrying 1,271,740,510 28 Drilling oil and gas wells 1,144,918,742 29 Support activities for oil and gas operations 1,232,989,414 33 Water, sewage and other systems 635,870,255 36 Construction of other new nonresidential structures 462,371,030 121 Industrial gas manufacturing 635,870,255 125 All other basic inorganic chemical manufacturing 635,870,255 201 Fabricated pipe and pipe fitting manufacturing 206 Mining and oil and gas field machinery manufacturing 226 Pump and pumping equipment manufacturing 638,512,375 227 Air and gas compressor manufacturing 539,432,869 335 Truck transportation 255,404,950 36 Construction of other new nonresidential structures 268,615,543 188 Power boiler and heat exchanger manufacturing 189 Metal tank (heavy gauge) manufacturing 431,546,283 201 Fabricated pipe and pipe fitting manufacturing 308,247,345 206 Mining and oil and gas field machinery manufacturing 145,316,605 222 Turbine and turbine generator set units manufacturing 28,622,968 226 Pump and pumping equipment manufacturing 63,851,236 227 Air and gas compressor manufacturing 247 Other electronic component manufacturing 184,948,407 251 Industrial process variable instruments manufacturing 123,298,938 256 Other measuring and controlling device manufacturing 61,649,469 369 Architectural, engineering, and related services 88,070,670 201 Fabricated pipe and pipe fitting manufacturing 176,072,752 206 Mining and oil and gas field machinery manufacturing 227 Air and gas compressor manufacturing 99,079,506 1,255,007,082 FACILITIES CAPEX 28,622,968 28,622,968 GATHERING CAPEX 384,751,568 1,069,478,936 PIPELINE INFRASTRUCTURE 36 Construction of other new nonresidential structures 201 Fabricated pipe and pipe fitting manufacturing 210,433,758 90,185,896 PRODUCTION 20 Extraction of Oil and Gas 24,766,904,691 Source: IHS CERA and IHS Global Insight NOTE: *Other unconventional gas includes gas from tight sands and coal bed methane. D-44 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Table C.3 Inputs to the US Macro Model: Other Unconventional Gas* 2010 2015 2020 Employment Production (Quadrillion Btu) Mining & Petroleum Nonresidential Structures Investment ($M) 2025 2030 2035 5.65562 5.67222 5.60042 5.71728 5.85241 6.08005 19,244 36,097 47,092 56,429 64,344 73,104 Source: IHS CERA and IHS Global Insight NOTE: *Other unconventional gas includes gas from tight sands and coal bed methane. Total Unconventional Gas Table C.4 US Production, Price and Value: Total Unconventional Gas* 2010 2015 2020 Employment Production (Mcf) 2025 2030 2035 11,283,859,513 15,427,348,660 18,457,307,340 20,598,479,016 22,368,861,678 24,825,154,416 Shale Gas 5,771,561,991 9,898,869,883 12,998,811,671 15,026,085,081 16,664,762,297 18,899,176,790 Tight Sands 3,919,979,770 4,189,135,644 4,345,136,944 4,567,079,807 4,744,306,084 4,968,805,590 Coal Bed Methane 1,592,317,752 1,339,343,133 1,113,358,725 1,005,314,129 959,793,297 957,172,036 4.38 5.18 5.42 6.21 6.89 7.90 Henry Hub Price (Nominal US $) Value of Production ($) 50,698,691,786 81,912,972,600 102,575,463,223 131,298,164,693 158,206,388,705 201,243,646,150 Source: IHS CERA and EIA NOTE: *Total unconventional gas includes gas from shale, tight sands, and coal bed methane. IHS D-45 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Table C.5 US Capital Expenditure Input to the IMPLAN Model: Total Unconventional Gas* IMPLAN Sector Description 2010 Capital Expenditure ($) DRILLING CAPEX 28 Drilling oil and gas wells 1,188,752,201 29 Support activities for oil and gas operations 3,719,096,173 36 Construction of other new nonresidential structures 3,566,256,604 160 Cement manufacturing 171 Steel product manufacturing from purchased steel 3,566,256,604 220 Cutting tool and machine tool accessory manufacturing 3,566,256,604 357 Insurance carriers 611,358,275 369 Architectural, engineering, and related services 305,679,137 152,839,569 COMPLETIONS CAPEX 26 Sand, gravel, clay, and ceramic and refractory minerals mining and quarrying 3,065,282,462 28 Drilling oil and gas wells 2,759,603,325 29 Support activities for oil and gas operations 2,971,880,503 33 Water, sewage and other systems 1,532,641,231 36 Construction of other new nonresidential structures 1,114,455,189 121 Industrial gas manufacturing 1,532,641,231 125 All other basic inorganic chemical manufacturing 1,532,641,231 201 Fabricated pipe and pipe fitting manufacturing 206 Mining and oil and gas field machinery manufacturing 3,024,949,798 226 Pump and pumping equipment manufacturing 1,539,009,546 227 Air and gas compressor manufacturing 1,300,197,720 335 Truck transportation 615,603,819 36 Construction of other new nonresidential structures 647,445,377 188 Power boiler and heat exchanger manufacturing 189 Metal tank (heavy gauge) manufacturing 201 Fabricated pipe and pipe fitting manufacturing 742,970,105 206 Mining and oil and gas field machinery manufacturing 350,257,335 222 Turbine and turbine generator set units manufacturing 68,990,081 226 Pump and pumping equipment manufacturing 227 Air and gas compressor manufacturing 247 Other electronic component manufacturing 445,782,063 251 Industrial process variable instruments manufacturing 297,188,042 256 Other measuring and controlling device manufacturing 148,594,021 369 Architectural, engineering, and related services 212,277,173 201 Fabricated pipe and pipe fitting manufacturing 435,995,056 206 Mining and oil and gas field machinery manufacturing 227 Air and gas compressor manufacturing 238,811,826 FACILITIES CAPEX 68,990,081 1,040,158,147 153,900,950 68,990,081 GATHERING CAPEX 952,729,938 2,648,266,269 PIPELINE INFRASTRUCTURE 36 Construction of other new nonresidential structures 4,208,675,164 201 Fabricated pipe and pipe fitting manufacturing 1,803,717,928 PRODUCTION 20 Extraction of Oil and Gas 50,698,691,786 Source: IHS CERA and IHS Global Insight NOTE: *Total unconventional gas includes gas from shale, tight sands, and coal bed methane. D-46 JUNE 2012 THE ECONOMIC AND EMPLOYMENT CONTRIBUTIONS OF UNCONVENTIONAL GAS DEVELOPMENT IN STATE ECONOMIES Table C.6 Inputs to the US Macro Model: Total Unconventional Gas* 2010 2015 2020 Employment Production (Quadrillion Btu) Mining and Petroleum Nonresidential Structures Investment ($M) 2025 2030 2035 11.5772 15.8285 18.9372 21.1340 22.9505 25.4706 52,505 84,804 114,683 126,590 161,172 199,695 Source: IHS CERA and IHS Global Insight NOTE: *Other unconventional gas includes gas from tight sands and coal bed methane. IHS D-47