2/24/2010

Chapter 5

The Behavior of

Interest Rates

(pp.111-121)

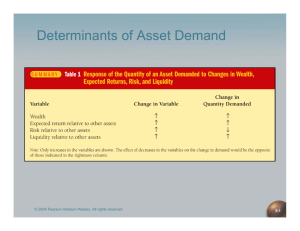

The Liquidity Preference Framework

• A Keynesian model which determines

the equilibrium interest rate in terms of

the supply and demand for money

• Two types of assets:

Money

Bonds

• Total Wealth: M+B

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

5-2

The Model

• M = Currency + Deposits

Narrowest definition of Money, think of M1

Assumptions:

p

• Money has no rate of return.

• Bonds have an expected return equal to

“i” (nominal int. rate).

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

5-3

1

2/24/2010

• As interest rate increases, the expected return on

money relative to bonds decreases

• FACT:

Price of a bond is negatively related to i

i (up),

(up) P (down)

bond

• Æi (up), P (down), D (up), D

bond

bond

money

(down)

• OR: As interest rate increases, opportunity cost of

holding money increases

• Æ Downwards sloping demand curve

5-4

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

• Assume central bank

inelastically supplied Ms=300

• Equilibrium is stable.

• At point A, Md<Ms : excess

supply of M

M.

Æpeople buy bonds

Dbond (up), Pbond (up), i (down)

• At point E, Md>Ms : excess

demand for M.

Æ people sell bonds.

Dbond (down) , Pbond (down), i

(up)

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

5-5

Changes in equilibrium interest rates

• Refresh our background:

• When you plot a function such as:

Md = a – b * i

Any change in the independent var. (i.e. i)

causes a movement along the curve

Any other change shifts the demand curve

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

5-6

2

2/24/2010

Shifts in the Demand for Money

• Income Effect —a higher level of income causes the

demand for money at each interest rate to increase

and the demand curve to shift to the right

Wealth effect (store of value)

T

Transaction

ti effect

ff t

• Price-Level Effect —a rise in the price level causes

the demand for money at each interest rate to

increase and the demand curve to shift to the right

To purchase as many real goods and services

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

5-7

Shifts in the Supply of Money

• Assume that the supply of money is

controlled by the central bank

pp y

• An increase in the moneyy supply

engineered by the Federal Reserve

will shift the supply curve of money to

the right

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

5-8

• What are the effects of these shifts in

equilibrium interest rates?

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

5-9

3

2/24/2010

5-10

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

• The “Liquidity Effect” : M (up), i (down)

S

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

5-11

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

5-12

4

2/24/2010

Everything Else Remaining Equal?

• So far the analysis was conducted in a static

framework, assuming everything else remains

constant.

• Liquidity preference framework leads to the conclusion

that an increase in the money supply will lower interest

rates the liquidity effect: MS (up),

rates—the

(up) i (down)

• However, in a dynamic framework, the liquidity effect

is followed by the following offsetting effects:

Income effect

Price Level effect

Expected inflation effect

5-13

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

Income Effect

• Recall from econ.202 that expansionary monetary policy

increases income

M (up), i (down) ÆI (up)ÆY (up)Æ M (up)Æi (up)

S

d

After th

Aft

the iinitial

iti l liliquidity

idit effect,

ff t th

the iincome effect

ff t causes iinterest

t

t rates

t

rise because increasing the money supply is an expansionary

influence on the economy.

• Æ What is the net impact on i?

• In the money market: Supply shift followed by a demand shift

5-14

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

Price Level Effect

• Recall from quantity theory that an increase in the

money supply leads to a an increase in the price level.

• When the price level increases, money demand

increases as well:

M (up), i (down) ÆY (up)Æ P (up)Æ M (up) Æi (up)

S

d

• Æ What is the net impact on i?

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

5-15

5

2/24/2010

Expected Inflation Effect

• An increase in the money supply may lead people to

expect a higher price level in the future.

MS (up), i (down) Æπe (up)Æ i (up): Fisher

effect: i = ir + πe

Liquidity effect is followed by an upwards movement

in interest rates

• Æ What is the net impact on i?

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

5-16

Price-Level Effect

vs. Expected-Inflation Effect

• A one time increase in the money supply will cause

prices to rise to a permanently higher level by the

end of the year. The interest rate will rise via the

increased prices.

• Price

Price-level

level effect remains even after prices have

stopped rising.

• A rising price level will raise interest rates because

people will expect inflation to be higher over the

course of the year. When the price level stops rising,

expectations of inflation will return to zero.

• Expected-inflation effect persists only as long as the

price level continues to rise.

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

5-17

How do these effects interfere with the

liquidity effect ?

• The final outcome of a monetary policy

action on interest rate depends on the

timing and the magnitude of offsetting

shifts

hift in

i the

th economy

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

5-18

6

2/24/2010

Copyright © 2007 Pearson Addison-Wesley. All rights reserved.

5-19

7