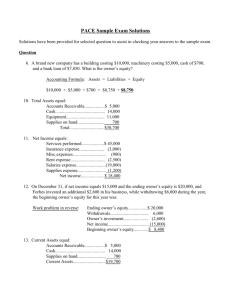

Study Guide for CC2101 Financial Accounting

advertisement