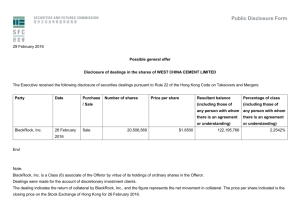

New Hong Kong Companies Ordinance

– Accounting & Reporting Alert

No-par value for shares

What’s the issue?

Issue 1

February 2014

From 3 March 2014, all shares, whether

issued before or after that date, will lose their

nominal (also known as “par”) value. This

applies to both existing and new companies

incorporated in Hong Kong. This change is

brought about by the new Hong Kong

Companies Ordinance Cap. 622 (“new CO”),

which abolishes par value. Also affected will

be share premium, capital redemption

reserve and the requirement for authorised

capital.

Consequently, companies will need to record

these changes in their accounting records

and in their financial statements for periods

ending on or after 3 March 2014.

What are the key changes?

• All shares have no nominal (par) value.

• Share premium account, capital

redemption reserve and authorised share

capital are abolished.

• All proceeds from an issue of shares are

recorded as “share capital”.

• Any amounts standing to the credit of share

premium account and capital redemption

reserve at 3 March 2014 are amalgamated

with the existing amount of share capital.

• “Share capital” can be used in similar ways

as share premium account to write off:

- preliminary expenses of the company; or

- any permitted commission paid; or

- any other expenses of any issue of shares.

• Bonus shares can be issued without

capitalising distributable profits or other

appropriate reserves.

Am I affected?

All existing and new Hong Kong incorporated

companies with share capital are affected by

the abolition of nominal value of share.

Do companies need to do

anything?

Companies do not have to do anything to

convert their shares to no-par value or

convert the “share premium” and “capital

redemption reserve” into “share capital”. The

new CO deems all shares issued before

abolition to have no par value and the

transitional provisions provide for the

amalgamation of the share premium account

and the capital redemption reserve with

share capital.

What accounting entries need to

be made?

However, on 3 March 2014 or after, a

company with share capital needs to transfer

any amounts standing to the credit of the

share premium account and capital

redemption reserve to share capital in its

accounting records.

What will financial statements

show?

Financial statements for periods ending

before 3 March 2014 should continue to

present share capital – authorised, issued,

class, number of shares in each class,

nominal value per share and aggregate

nominal value ; share premium account and

capital redemption reserve, if relevant.

What will financial statements show?

(continued)

What impact is there on classes of shares

and dividends?

That is, there is no change from existing presentation and

disclosure.

There is no impact on the classes of shares that a company

has in issue or the class rights attached to those shares. Where

rights to dividends on existing shares are expressed by

reference to their par value, for example, some preference

shares, the transitional provisions in the new CO will apply to

give affect as if their par value still exists.

Financial statements for periods ending on or after 3 March

2014 should show the transfer of the balances on the share

premium account and capital redemption reserve to “share

capital” in the Statement of Changes in Equity. Accordingly,

only the class, the number of shares in each class and the

aggregate amount credited to “share capital” will be

presented as “share capital” in the 2014 balance sheet and its

notes. The share capital note should provide a narrative

explanation that the changes are a result of the abolition of

nominal value of shares under the new CO.

The equity section of A Co., Ltd’s balance sheet and its

Statement of Changes in Equity are illustrated in the

Appendix.

Are the comparative balance sheet and its

notes restated?

The comparative balance sheet and its notes will not be

restated, as the changes are prospective from 3 March 2014.

Consequently, the comparative balance sheet and notes will

present the previously reported share capital, share premium

and capital redemption reserve amounts as separate line

items with accompanying details.

Which companies and their financial

statements will be affected first?

Companies (private and listed) with a financial year ending

on 31 March 2014 will be the first affected and have to deal

with the changes in their annual financial statements for that

year.

Hong Kong incorporated companies listed on the Stock

Exchange of Hong Kong or other bourses with a financial

year ending on or after 30 September 2014, which report half

yearly, will first deal with the changes in their interim

financial statements for the 6 months ending on or after

31 March 2014. Those listed companies that report quarterly

will deal with the changes in the interim financial statements

for the quarter ending on or after 31 March 2014.

PwC help

If you have questions or require further information,

please speak to your regular PwC contact.

www.pwchk.com

www.pwccn.com

2

Is the calculation of earnings per share

affected?

No. The abolition of nominal value will have no impact on the

calculation of earnings per share (EPS), as the number of

shares is unaffected by the change. For the purpose of

calculating basic and diluted EPS, the weighted number of

shares to be used will still be calculated in accordance with

paragraphs 19, 26 and 36 of Hong Kong Accounting Standard

33, Earnings per Share.

Are companies not incorporated in Hong

Kong affected?

No. Companies incorporated outside of Hong Kong are not

affected. They will continue to comply with the legal

requirements on share capital of the country in which they are

incorporated.

Do directors need to take any other action?

The transitional provisions in the new CO are intended to

provide legislative safeguards to ensure that contractual

rights defined by reference to par value and related concepts

will not be affected by the abolition of par.

However, the Hong Kong Companies Registry suggests in its

External Circular No. 7/2012 that directors may wish to

review their companies particular situations before 3 March

2014 to determine whether they need to introduce more

specific changes to their companies’ documents. Examples

could include their Memorandum and Articles of Association,

contracts, trust deeds, convertible bonds or preference shares

and share certificates. Directors should seek independent

legal advice, if necessary.

Further information

Hong Kong Companies Registry website provides further

information on the abolition of par value and other aspects of

the new CO.

www.cr.gov.hk/en/companies_ordinance/index.htm

APPENDIX

Application of the new no-par value regime

Effect on financial statements for accounting periods ending on 31 March 2014

A Co., Ltd is an existing Hong Kong incorporated company, with a 31 March year end. It has in issue 1,000 shares with

nominal value of HK$1 each and has a share premium account of HK$9,000. It also has a capital redemption reserve of

HK$500 arising from the redemption of some shares in a previous year.

In the year to 31 March 2014, there are no changes to the number of issued shares, but A Co., Ltd earns profits of HK$200. It

had HK$1,000 of retained earnings at 31 March 2013.

Illustrative A Co., Ltd balance sheet equity section

31 March

2014

HK$

Share capital (1,000 shares issued and fully paid) (Note 1)

Share premium

Capital redemption reserve

Retained earnings

Total equity

10,500

1,200

11,700

2013

HK$

1,000

9,000

500

1,000

11,500

Note 1

2014 - Share capital note will disclose class(es) of issued shares, number of issued shares and aggregate monetary

amount per class. It should also provide a narrative explanation of the changes due to the abolition of par value of

shares.

2013 – Share capital note will disclose authorised share capital, class(es) of issued shares, nominal value per share of

each class and aggregate nominal value per class.

Illustrative A Co., Ltd Statement of Changes in Equity

Balance at 1 April 2013

Transfers on 3 March 2014

Profit for the year

Balance at 31 March 2014

Share capital

HK$

1,000

Share

premium

HK$

9,000

Capital

redemption

Reserve

HK$

500

Retained

earnings

HK$

1,000

Total

equity

HK$

11,500

9,500

10,500

(9,000)

-

(500)

-

200

1,200

200

11,700

This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

© 2014 PricewaterhouseCoopers. All rights reserved. PwC refers to the Hong Kong member firm, and may sometimes refer to the PwC network.

Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.

3