Year-end report

advertisement

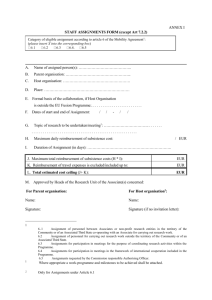

Year-end report For the period January–December 2012 • February 15, 2013, 2.00 pm The fourth quarter of 2012 Compared to the third quarter of 2012 •Net operating profit amounted to EUR 14.5 M (-0.5). Of this, EUR 13.8 M was proceeds from the divestment of the Bank’s Swedish subsidiary, which had been emptied of operations. • Profit for the period attributable to shareholders was EUR 14.9 M (-0.3). • Net interest income decreased by 3 per cent to EUR 9.9 M (10.2). • Net commission income increased by 20 per cent to EUR 9.2 M (7.7). • Total expenses increased by 17 per cent to EUR 25.2 M (21.5). • Net loan losses were EUR 3.1 M (1.0), including EUR 2.0 M in group impairment losses for the shipping industry. • Earnings per share amounted to EUR 1.03 (-0.02). January−December 2012 Compared to January−December 2011 •Net operating profit amounted to EUR 10.0 M (-5.7). Net operating profit EUR M 15 9 3 -2 -8 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12 Deposits and lending EUR M 3,000 2,861 2,737 2,762 2,544 2,551 2,591 2,557 2,447 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12 2,500 2,895 2,906 2,000 • Profit for the period attributable to shareholders was EUR 11.6 M (-6.5). • Net interest income decreased by 4 per cent to EUR 41.2 M (43.1). 1,500 • Net commission income decreased by 16 per cent to EUR 32.7 M (38.7). • Deposits • Lending • Total expenses decreased by 9 per cent to EUR 94.0 M (103.1). • Net loan losses were EUR 6.4 M (1.8), equivalent to a loan loss level of 0.22 (0.07) per cent. • Return on equity after taxes (ROE) amounted to 6.4 per cent (-3.9). • Earnings per share amounted to EUR 0.80 (-0.54). • The Tier 1 capital ratio increased to 10.9 per cent (8.4). • The Board of Directors proposes a dividend of EUR 0.15 (0.00) per share. • The Bank’s earnings performance is determined to a significant degree by external factors that are difficult to predict. Since new securities legislation removes the explicit obligation in an interim report to provide an account of probable developments during the current financial period, the Bank of Åland is henceforth choosing to refrain from providing earnings forecasts in interim reports. In accordance with legislative requirements, the future outlook is presented in the Bank’s Annual Report. . “The fourth quarter was strong in terms of earnings, mainly due to income from the d ­ ivestment of the Swedish subsidiary, which had been emptied of operations. At the quarterly level, however, we can also see that our measures to improve profitability are beginning to have an impact. Yet the conditions for conducting banking operations in the euro zone remain challenging, although there are signs of increased optimism both in the stock market and the fixed income market. The significant cost increases affecting banks because of new legislation and expanded regulatory requirements will be passed on to customers. This will lead to a continued rise in ­margins, especially on lending.” Peter Wiklöf, Managing Director Tier 1 capital ratio Per cent 12 9 6 3 0 Q4 11 Q1 12 Q2 12 Q3 12 Q4 12 Q3 12 Q4 12 Managed assets EUR M 5,000 4,000 3,000 2,000 1,000 0 Q4 11 Q1 12 Q2 12 The Bank of Åland is a bank with strong customer relationships and personal service. The Bank has extensive financial investment expertise and at the same time can offer good financing services. The commercial bank was founded in 1919 and has been listed on the Nasdaq OMX Helsinki Oy (Helsinki Stock Exchange) since 1942. The Bank of Åland’s Head Office is in Mariehamn. The Bank has eight offices in the Åland Islands and seven offices elsewhere in Finland. The Bank has three offices in Sweden. A total of seven subsidiaries, whose operations are connected in various ways to banking, belong to the Bank of Åland Group. Bank of Åland Plc. Registered office: Mariehamn Address: Nygatan 2, FI-22100 Mariehamn, Åland, Finland Business Identity Code: 0145019-3. Telephone: +358 204 29 011. Website: www.alandsbanken.fi Earnings and profitability MACRO SITUATION AND REGULATORY REQUIREMENTS The euro zone debt crisis has dominated economic developments during 2012. The 3-month Euribor benchmark interest rate fell from 1.34 per cent to a record-low 0.19 per cent in one year. Since the 3-month Euribor determines a large proportion of customer lending rates, while the Bank’s borrowing cost is not at all affected to the same extent by lower benchmark interest rates, this squeezes the Bank’s net interest income. Regulatory requirements such as higher capital adequacy ratios, larger liquidity buffers, longer maturity on borrowings and increased administration for risk management and reporting also squeeze profitability – the latter especially in small banks. The estimated total additional cost of the new regulatory requirements is equivalent to a 0.6-1.0 percentage point increase in lending rates. Finland has also introduced a banking tax amounting to 0.125 per cent of risk-weighted assets, which further increases the Bank’s lending costs starting in 2013. The Bank of Åland, like other banks, thus needs to raise its margins. During the latest period, we have seen a clear tendency towards higher lending margins in Finland. We expect lending margins to rise significantly from their current levels. BENCHMARK INTEREST R ATES, AVER AGES, PER CENT Euribor 3 mo Euribor 12 mo Stibor 3 mo Stibor 12 mo Euribor 3 mo Euribor 12 mo Stibor 3 mo Stibor 12 mo Q4 2012 Q3 2012 Q4 2011 0.19 0.60 1.45 1.78 0.36 0.89 1.95 2.40 1.50 2.05 2.61 2.80 2012 2011 0.57 1.11 2.00 2.40 1.39 2.01 2.46 2.85 During 2012, the value of the Swedish krona in relation to the euro averaged 4 per cent higher than during the equivalent period of 2011. Compared to its year-end 2011 position, the krona appreciated more than 4 per cent. This represents a strong krona in historical terms. When translating the income statement of the Bank of Åland’s Swedish operations to euros, average exchange rates for the period are used, while the balance sheet is translated at the exchange rate prevailing on the closing day. IMPORTANT EVENTS During 2012, the Bank of Åland completed the restructuring of its operations in Sweden, which means that Swedish operations are now being pursued in the form of the Swedish branch of the parent Bank. This new, simplified corporate structure means more efficient capital utilisation and a more efficient tax situation, as well as more cost-effective corporate governance. During the fourth quarter, the Bank completed the divestment of its Swedish subsidiary, which had been emptied of operations, with a positive impact on earnings of EUR 13.8 M. During 2012, for the first time in its history the Bank of Åland received a credit rating. The Bank received a BBB/A-3, i.e. investment grade credit rating with a stable outlook for its long-term and short-term borrowing from the rating agency Standard & Poor’s. The Bank’s covered bonds received an AA credit rating from Standard & Poor’s. During the third quarter, the Bank of Åland issued covered bonds for the first time, totalling EUR 300 M. During the fourth quarter, the Bank issued more than EUR 170 M worth of additional covered bonds, this time in Swedish kronor and mainly to Swedish investors. Covered bonds have provided the Bank of Åland with access to a new, efficient funding source. The covered bond market is liquid and is the portion of the capital market that has functioned best throughout the financial crisis. The interest cost is substantially lower than for non-covered bonds. By issuing covered bonds, the Bank of Åland increases its long-term funding as a share of total funding, which is in line with the new capital adequacy regulations. During 2012, the Bank implemented a significant reorganisation and extensive efficiency-raising measures. During the first quarter, the number of positions in the Group was reduced by about 50, of which 30 in the Åland Islands, 10 on the Finnish mainland and 10 in Sweden. During the fourth quarter, the number of positions in the Group was further reduced by more than 30, of which about 20 in the subsidiary Crosskey Banking Solutions. The number of offices in Åland was reduced from 16 to eight plus two representative offices. On the Finnish mainland, institutional equities trading operations were closed. Extensive changes occurred in the corporate units of the Group. During the first quarter of 2012, the Finnish Financial Supervisory Authority approved the Bank’s application to be allowed to calculate the capital requirement for credit risk according to the Internal Ratings Based (IRB) approach for the Finnish household portfolio. The transition from the standardised approach to the IRB approach for the Finnish household portfolio temporarily reduced the Bank’s risk-weighed assets by EUR 355 M. The Bank is continuing its efforts to implement the IRB approach in the Finnish corporate portfolio and the Swedish loan portfolio as well. The Bank of Åland received the 2012 Morningstar Funds Award as the best fixed interest fund manager in Finland. The Bank earned the award for its three euro-denominated fixed income funds: Ålandsbanken Cash Manager, a short-term fixed income fund; Ålandsbanken Euro Bond, a medium-term fixed income fund; and Ålandsbanken Euro High Yield, a fixed income fund with higher potential return and risk than traditional fixed income funds. On April 19, 2012, the Annual General Meeting elected Folke Husell, Anders Å Karlsson and Annika Wijkström as new members of the Bank’s Board of Directors. Board members Kaj-Gustaf Bergh, Agneta Karlsson and Anders Wiklöf were re-elected. At the statutory meeting of the Board the same day, Kaj-Gustaf Bergh was elected Chairman and Folke Husell was elected Vice Chairman of the Board. EARNINGS FOR THE FOURTH QUARTER OF 2012 Net operating profit in the fourth quarter amounted to EUR 14.5 M, compared to EUR -0.5 M in the third quarter. The main explanation for these very good quarterly earnings was the divestment of the Bank’s Swedish subsidiary, which had been emptied of operations. This divestment resulted in income of EUR 13.8 M, of which EUR 6.3 M was a capital gain and EUR 7.5 M a currency translation gain. Bank of Åland Plc Year-end Report, January–December 2012 2 At the same time, nonrecurring expenses in the range of EUR 3.2 M plus EUR 2.0 in group loss impairments for lending exposures to the shipping industry were charged to fourth quarter earnings. Earnings from underlying banking business developed favourably. Total income amounted to EUR 42.7 M. Excluding the divestment income from the Swedish subsidiary and the associated company Ålands Företagsbyrå, income amounted to EUR 27.9 M. This was EUR 5.9 M or 26 per cent higher than the preceding quarter, adjusted for the impairment loss on the Bank’s shareholding in the equities-trading platform Burgundy. The Bank was able to offset the effects of falling benchmark interest rates by adjusting its lending prices. Overall net interest income decreased by EUR 0.3 M or 3 per cent from the preceding quarter to EUR 9.9 M. Net commission income increased by EUR 1.5 M or 20 per cent to EUR 9.2 M due to higher securities brokerage commissions and asset management commissions. Total expenses were EUR 25.2 M, which was EUR 3.7 M or 17 per cent higher than in the second quarter. In addition to seasonal variations, EUR 1.1 M in expenses related to staff cutbacks, EUR 0.5 M in administrative expenses for problem loans, EUR 1.0 M in impairment losses and conversion expenses for IT systems, EUR 0.3 M in expenses related to phasing out surplus premises and EUR 0.3 M in other expenses were noted. Loan losses increased to EUR 3.1 M (1.0), of which EUR 2.0 M was related to increased group impairment losses for exposures to the shipping industry. These increased group impairment losses were recognised because there was another downturn in economic conditions at the end of 2012, which will affect the export sector and thus also shipping. Even though the Bank’s customers have demonstrated an ability to weather bad times, a continued and deepened economic slowdown increases risks. The Bank’s customers in the shipping industry have already experienced two years of weak market conditions. Profit for the period attributable to shareholders was EUR 14.9 M (-0.3). Return on equity after taxes amounted to 33.3 (-0.4) per cent. EARNINGS FOR JANUARY-DECEMBER 2012 Net operating profit in 2012 amounted to EUR 10.0 M, compared to EUR -5.7 M in the preceding year. Both 2012 and 2011 earnings included a number of nonrecurring items related to the restructuring of operations. The most significant items were EUR 13.8 M in income from the divestment of the Bank’s Swedish subsidiary, which had been emptied of operations, a capital gain of EUR 1.0 M from the divestment of the associated company Ålands Företagsbyrå, plus impairment losses of EUR 0.8 M in 2012 and EUR 1.1 M in 2011 on the Bank’s shareholding in the equities-trading platform Burgundy and restructuring expenses of EUR 1.1 M in 2012 and EUR 5.7 M in 2011 related to staff cutbacks. Excluding these nonrecurring items, net operating profit decreased from EUR 1.1 M to EUR -2.9 M in 2012. However, thanks to the measures that were undertaken, the trend of earnings before loan losses and nonrecurring items turned upward during the second half of 2012. Earnings bottomed out in the second quarter of 2012, when quarterly profit before loan losses and nonrecurring items was EUR -1.4 M. In the third quarter, this measure of earnings increased to EUR 1.3 M. In the fourth quarter it improved further to EUR 3.9 M. Total income increased by EUR 11.2 M or 11 per cent to EUR 110.4 M (99.2). Of this increase, EUR 15.0 M was explained by the abovementioned nonrecurring items. Because of price adjustments in the lending portfolio and higher volume, the Bank was largely able to offset the negative impact of sharply falling money market interest rates on net interest income. Net interest income fell by EUR 1.9 M or 4 per cent to EUR 41.2 M. In the Sweden business area, net interest income increased by EUR 2.3 M or 25 per cent. Net commission income fell by EUR 6.0 M or 16 per cent to EUR 32.7 M. Of this decrease, EUR 6.4 M was attributable to securities brokerage income, among other things due to the closure of institutional equities trading operations, which had income of EUR 2.2 M in 2011. Net income from securities transactions and foreign exchange dealing amounted to EUR 10.1 M, compared to EUR 1.9 M in 2011. The increase consisted mainly of foreign exchange gains related to the divestment of the Bank’s Swedish subsidiary. Underlying earnings from financial asset management also developed favourably. Net income from financial assets available for sale increased to EUR 10.8 M (-0.7). EUR 6.3 M in capital gains on the divestment of the Bank’s Swedish subsidiary and EUR 1.0 M on the divestment of Ålands Företagsbyrå were the most important explanations for the increase, but underlying earnings from financial asset management also increased strongly. Net income from investment properties was EUR 0.0 M. In 2011 this item amounted to EUR 0.9 M, of which EUR 0.8 M was related to a divestment gain. Information technology (IT) income from Crosskey’s operations increased by EUR 1.1 M or 8 per cent to EUR 14.5 M (13.4). Total expenses fell by EUR 9.1 M or 9 per cent and amounted to EUR 94.0 M (103.1). Adjusted for restructuring expenses related to staff cutbacks both in 2012 and 2011, this was a decrease of EUR 4.4 M. Adjusted for exchange rate effects, the decrease was EUR 5.7 M or 6 per cent. The Bank of Åland previously announced cost savings in the range of EUR 10 M annually from the measures undertaken during 2011 and 2012. Of these, EUR 4 M was related to the closure of institutional equities trading in Sweden in June 2011, while EUR 4 M was related to the reorganisation that was implemented in the first quarter of 2012 and approximately EUR 2 M was related to the measures implemented in the fourth quarter of 2012. Savings targets have been achieved by a wide margin. Expenses recognised for the full year 2012 were more than EUR 5 M lower than for the full year 2011 due to these measures, of which EUR 2 M was attributable to a full rather than a half year without institutional equities trading in Sweden and more than EUR 3 M was attributable to measures in 2012 totalling EUR 6 M. All else being equal, full year 2013 expenses will be about EUR 3 M lower than full year 2012 expenses due to these measures. Net loan losses were EUR 6.4 M (1.8). Of impairment losses, EUR 2.0 M consisted of group impairment losses for exposures to the shipping industry. The loan loss level was 0.22 per cent, compared to 0.07 per cent the preceding year. The tax effect was positive and amounted to EUR 2.2 M (0.4). The favourable tax situation is explained primarily by tax-exempt capital gains, while it was possible to reverse certain deferred tax liabilities. The tax situation also improved because Swedish operations now take place in the form of a branch of the Parent Company. In addition, Finnish corporate tax has been lowered from 26 to 24.5 per cent. Bank of Åland Plc Year-end Report, January–December 2012 3 Profit for the year attributable to shareholders was EUR 11.6 M, compared to EUR -6.5 M in the preceding year. Return on equity after taxes was 6.4 per cent (-3.9). Net operating profit deteriorated in the Åland and Finnish Mainland business areas as well as in Crosskey Banking Solutions. Earnings in the Sweden business area improved. The effects on the consolidated financial statements of the divestment of the Swedish subsidiary are reported as part of the Sweden business area. Business operations in the Sweden business area also substantially improved their earnings. Expenses decreased throughout all business areas due to efficiency-raising measures. Net interest income in the Åland business area decreased by 18 per cent due to lower Euribor rates, while EUR 3.6 M in impairment losses mainly connected to shipping loans and about EUR 0.7 M in expenses for administration of these loans was charged to earnings. Net interest income in the Finnish Mainland business area also fell sharply as a consequence of lower Euribor rates. Compared to the preceding year, the business area did not include the closed-down Equities operations. Aside from lower net interest income, the lower net operating profit in the Finnish Mainland business area was also due to lower earnings at Ålandsbanken Asset Management. The improvement in the earnings of the Sweden business area primarily arose by means of cost reductions. BUSINESS VOLUME Managed assets increased by EUR 478 M or 13 per cent during 2012 and amounted to EUR 4,292 M (3,814). Managed assets in the Bank of Åland Group’s own mutual funds rose by EUR 110 M or 15 per cent during 2012 to EUR 867 M (757). Assets under discretionary management rose by EUR 194 M or 11 per cent to EUR 1,991 M (1,798), which was the highest figure ever. Assets under advisory management rose by EUR 173 M or 14 per cent to EUR 1,433 M (1,260). Of total managed assets, the Sweden business area accounted for EUR 2,424 M or 56 (57) per cent. Deposits from the public – including certificates of deposit, index bonds and debentures issued to retail customers – decreased by EUR 97 M during 2012 and amounted to EUR 2,447 M (2,544). Because of the Bank’s successful covered bond issues, these bonds have partly replaced more expensive time deposits. In Sweden, the Åland Account continued to attract new customers. During 2012, Åland Account and fixed interest rate deposits increased by about EUR 100 M. Lending to the public totalled EUR 2,906 M (2,737). This represented an increase of EUR 169 M or 6 per cent. The lending increase was primarily related to home mortgage loans in the Swedish market. CREDIT QUALIT Y Lending to private individuals comprises nearly two thirds of the loan portfolio. Home mortgage loans account for about two thirds of lending to private individuals. Loans for the purchase of securities, with market-listed securities as collateral, comprise the second-largest type of lending to private individuals. Loan-to-value ratios are conservative. Historically, the Bank of Åland has never had any substantial loan losses on this type of lending. The corporate portfolio has a close affinity with the household portfolio, since many of the companies are owned by customers who, as individuals, are also Private Banking customers. During 2012, gross non-performing loans (more than 90 days) decreased by EUR 0.7 M to EUR 18.6 M (19.3). As a share of lending to the public, non-performing loans fell from 0.70 per cent to 0.64 per cent during the year. The level of provisions for doubtful receivables, i.e. individual impairment losses as a proportion of all doubtful receivables, was 84 per cent compared to 62 per cent at year-end 2011. Including group impairment losses, the level of provisions amounted to 108 per cent, compared to 71 per cent at year-end 2011. The Bank of Åland Group had EUR 13.6 M in impairment loss provisions, including individual impairments of EUR 10.6 M and group impairment losses of EUR 3.1 M. LIQUIDIT Y AND BORROWING The Bank of Åland’s liquidity reserve in the form of cash, account balances and investments with other banks, liquid interest-bearing securities plus holdings of unencumbered covered bonds issued by the Bank amounted to EUR 483 M (410) on December 31, 2012. This was equivalent to 13 per cent of total assets (12) and 17 (15) per cent of lending to the public. Given the Bank’s ability to issue highquality covered bonds, there is an additional unutilised liquidity reserve. The Bank has no significant long-term borrowing maturities during 2013. Seventy-four per cent of the Bank of Åland’s funding comes from deposits from the public, including certificates of deposit, index bonds and subordinated debentures. The Bank of Åland thus has a relatively small need for borrowing in the capital market. Of deposits from the public, EUR 140 M (155) consisted of time deposits, index bonds and debentures with a maturity of more than one year. Although the remainder consisted of sight deposits or has contractually shorter maturities than 1 year, this funding can largely be regarded as stable, based on historical customer behaviour. The Bank of Åland’s core funding ratio, defined as lending to the public divided by deposits from the public including certificates of deposit, index bonds and subordinated debentures issued to the public, plus covered bonds issued, amounted to 104 per cent at the end of 2012 (108). CAPITAL ADEQUACY Equity capital increased in the amount of total profit for the period, EUR 5.6 M, to EUR 186 M. The equity/assets ratio decreased to 5.1 per cent from a 5.3 per cent position at the end of 2011. Core Tier 1 capital as defined in capital adequacy regulations amounted to EUR 152.9 M (145.5). During the first quarter of 2012, the Finnish Financial Supervisory Authority approved the Bank’s application to be allowed to calculate the capital requirement for credit risk according to the Internal Ratings Based (IRB) approach for the Finnish household portfolio. Risk-weighted assets decreased by EUR 327 M or 19 per cent during 2012 and amounted to EUR 1,402 M (1,729). Risk-weighted assets attributable to credit risks decreased by EUR 311 M or 20 per cent despite the increase in lending, since the IRB approach is being used instead of the standardised approach for the Finnish household portfolio. The core Tier 1 capital ratio increased to 10.9 (8.4) per cent, without taking transitional rules into account. Since the Bank of Åland has no hybrid capital, its core Tier 1 capital ratio is the same as its Tier 1 capital ratio. The total capital ratio was 16.1 (12.8) per cent. In accordance with the 2011 Annual General Meeting’s decision on Bank of Åland Plc Year-end Report, January–December 2012 4 purchases of the Bank’s own shares for the purpose of implementing a share-based compensation programme for senior executives, the Bank has purchased its own shares. On December 31, 2012 this holding amounted to 25,000 Series B shares. CHANGES IN GROUP STRUCTURE During the fourth quarter, the Bank of Åland Plc completed its divestment of the wholly owned subsidiary Ålandsbanken Asset Management AB in Sweden. It also completed its merger with the wholly owned subsidiary Ålandsbanken Equities Research Ab. Both of these companies were emptied of business operations. During the fourth quarter, the Bank also sold its shares in the associated company Ålands Företagsbyrå Ab. DIVIDEND In light of positive earnings attributable to the shareholders, the improved capital adequacy situation and a positive belief in the Bank’s trend of earnings and capital generating capacity, the Board of Directors proposes that the Annual General Meeting approve the payment of a dividend of EUR 0.15 per share, equivalent to a total amount of EUR 2.2 M. The poorer economic outlook has adversely affected the shipping industry, among others. The risk of loan losses from this industry is thus high. We are focusing especially on these customers. The Bank of Åland’s total lending to companies in the shipping industry represents about 3 per cent of its overall lending volume. Based on the positive future expectations at Compass Card, a deferred tax asset of EUR 0.9 M was recognised. If the conditions affecting the company should change dramatically, in such a way that the company will not achieve a profit, the value of this asset may need to be re-assessed. FUTURE OUTLOOK The Bank’s earnings performance is determined to a significant degree by external factors that are difficult to predict. Since new securities legislation removes the explicit obligation in an interim report to provide an account of probable developments during the current financial period, the Bank of Åland is henceforth choosing to refrain from providing earnings forecasts in interim reports. In accordance with legislative requirements, the future outlook is presented in the Bank’s Annual Report. IMPORTANT EVENTS AFTER THE CLOSE OF THE REPORT PERIOD GENER AL MEETINGS In January, the Bank of Åland issued EUR 100 M worth of covered bonds with a 10-year maturity. An Extraordinary General Meeting will be held in Mariehamn on Tuesday, March 5, 2013. The Annual General Meeting will be held in Mariehamn on Thursday, April 18, 2013. The Bank of Åland published a notice to convene an Extraordinary General Meeting of shareholders in Mariehamn, Åland, Finland on March 5. For the purpose of modernising the Articles of Association, the Board of Directors proposes that the Extraordinary General Meeting approve the removal of the regulation that a person who has reached the age of 67 may not be elected as a Board member. The Annual Report will be published on Wednesday, March 20, 2013. The Corporate Governance Report is included in the Annual Report. FINANCIAL INFORMATION The Interim Report for January–March 2013 will be published on April 29, 2013. RISKS AND UNCERTAINTIES The Bank of Åland’s earnings are affected by external changes that the Company itself cannot control. Among other things, the Group’s trend of earnings is affected by macroeconomic changes and changes in general interest rates, share prices and exchange rates, along with higher expenses due to regulatory decisions and directives as well as the competitive situation. The Group aims at achieving operations with reasonable and carefully considered risks. The Group is exposed to credit risk, liquidity risk, market risk, operational risk and business risk. The Interim Report for January–June 2013 will be published on July 29, 2013. The Interim Report for January–September 2013 will be published on October 28, 2013. The figures in this Year-end Report are unaudited. Mariehamn, February 15, 2013 THE BOARD OF DIRECTORS The Bank does not engage in trading for its own account. The Bank of Åland has no exposure to the “GIIPS” countries (Greece, Italy, Ireland, Portugal and Spain). Bank of Åland Plc Year-end Report, January–December 2012 5 Financial summary Q4 2012 Q3 2012 Income Net interest income Net commission income Other income Total income 9.9 9.2 23.6 42.7 10.2 7.7 4.1 22.0 Staff costs Other expenses Total expenses -13.7 -11.5 -25.2 -12.3 -9.2 -21.5 Profit before loan losses etc. 17.5 0.5 Impairment losses on loans and other ­commitments Net operating profit -3.1 14.5 Income taxes Profit for the report period Attributable to: Non-controlling interests Shareholders in Bank of Åland Plc Bank of Åland Group % Q4 2011 % 2012 2011 % -18 11 86 41.2 32.7 36.5 110.4 43.1 38.7 17.4 99.2 -4 -16 94 12.1 8.3 2.6 23.0 11 26 17 -16.7 -12.6 -29.3 -18 -8 -14 -52.3 -41.7 -94.0 -60.0 -43.1 -103.1 -13 -3 -9 -6.3 16.4 -3.9 -1.0 -0.5 -0.8 -7.1 -6.4 10.0 -1.8 -5.7 0.6 15.1 0.3 -0.2 2.6 -4.5 -75 2.2 12.2 0.4 -5.3 0.2 14.9 0.2 -0.3 56 0.2 -4.7 32 0.6 11.6 1.2 -6.5 2,906 2,447 4,292 186 3,637 1,402 2,895 2,557 4,230 178 3,620 1,420 0 -4 1 5 0 -1 2,737 2,544 3,814 181 3,400 1,729 6 -4 13 3 7 -19 33.3 59 0.42 0.64 108 104 5.1 10.9 1.03 12.70 10.04 7.10 -0.4 98 0.14 0.86 67 106 4.9 9.7 -0.02 12.12 10.04 7.77 -11.4 127 0.12 0.70 71 108 5.3 8.4 -0.34 12.34 14.15 8.68 6.4 85 0.22 0.64 108 104 5.1 10.9 0.80 12.70 10.04 7.10 -3.9 104 0.07 0.70 71 108 5.3 8.4 -0.54 12.34 14.15 8.68 14,395 14,395 14,441 14,395 14,441 626 633 697 640 690 EUR M Volume Lending to the public Deposits from the public 1 Managed assets Equity capital Balance sheet total Risk-weighted assets Financial ratios Return on equity after taxes, % (ROE) 2 Expenses/income ratio, % 3 Loan loss level, % 4 Gross non-performing assets, % 5 Level of provisions for doubtful receivables, % 6 Core funding ratio, % 7 Equity/assets ratio, % 8 Core Tier 1 capital ratio, % 9 Earnings per share before dilution, % 10 Equity capital per share, EUR 11 Market price per Series A share, EUR Market price per Series B share, EUR Number of shares outstanding (not own shares) thousands Working hours re-calculated to full-time equivalent positions 1 2 3 4 5 Deposits from the public and public sector entities, including bond loans and ­certificates of deposit (Profit for the report period attributable to shareholders / Average shareholders’ ­portion of equity capital) x 100 Expenses / Income Impairment losses on loan portfolio and other commitments / lending to the public (Non-performing loans more than 90 days) / lending to the public) x 100 -3 20 11 -47 Impairment loss provisions / doubtful receivables Lending to the public / Deposits including certificates of deposit, index bonds and debentures issued to the public and covered bonds issued 8 (Equity capital / Balance sheet total) x 100 9 (Core Tier 1 capital / Capital requirement) x 8 % x 100 10 Shareholders’ portion of earnings for the period/ Number of shares adjusted for share issue 11 Equity capital/Number of shares on closing day 6 7 Bank of Åland Plc Year-end Report, January–December 2012 6 Summary statement of financial position Bank of Åland Group Dec 31, 2012 Dec 31, 2011 % EUR M Assets Cash Debt securities eligible for refinancing with central banks Claims on credit institutions Claims on the public and public sector entities Debt securities Shares and participations Shares and participations in associated companies Derivative instruments Intangible assets Tangible assets Other assets Accrued income and prepayments Deferred tax assets Total assets 133 66 100 305 104 2,906 45 7 1 20 11 33 45 26 3 3,637 125 129 2,737 198 3 1 20 11 32 46 26 4 3,400 -20 6 -77 96 -37 0 -5 1 -3 1 -30 7 Liabilities and equity capital Liabilities to credit institutions Liabilities to the public and public sector entities Debt securities issued Derivative instruments Other liabilities Accrued expenses and prepaid income Subordinated liabilities Deferred tax liabilities Total liabilities 375 2,127 760 15 68 28 64 16 3,451 230 2,147 659 14 63 30 58 20 3,220 63 -1 15 9 8 -12 11 -20 7 Equity capital and minority interest Share capital Share premium account Reserve fund Fair value reserve Unrestricted equity capital fund Own shares Retained earnings Shareholders’ interest in equity capital 29 33 25 3 24 0 69 183 29 33 25 10 24 0 56 178 0 0 0 -68 0 Minority interest in capital Total equity capital 3 186 3 181 23 3 3,637 3,400 7 Total liabilities and equity capital 20 3 Bank of Åland Plc Year-end Report, January–December 2012 7 Summary income statement Bank of Åland Group Q4 2012 Q3 2012 % Q4 2011 % 2012 2011 % -3 20 12.1 8.3 -18 11 41.2 32.7 43.1 38.7 -4 -16 -100 70 86 10.1 10.8 0.0 14.5 1.2 110.4 1.9 -0.7 0.9 13.4 1.8 99.2 -100 8 -34 11 -18 -6 -20 49 -30 -14 -52.3 -20.6 1.5 -8.1 -14.5 -94.0 -60.0 -20.9 1.8 -6.7 -17.3 -103.1 -13 -2 -18 21 -16 -9 EUR M Net interest income Net commission income Net income from securities transactions and foreign exchange dealing Net income from financial assets available for sale Net income from investment properties IT income Other operating income Total income 9.9 9.2 10.2 7.7 8.4 10.9 0.0 3.7 0.6 42.7 1.1 -0.6 0.0 3.5 0.1 22.0 -100 6 94 0.7 -1.3 0.8 2.2 0.3 23.0 Staff costs Other administrative expenses Production for own use Depreciation/amortisation Other operating expenses Total expenses -13.7 -5.4 0.3 -2.6 -3.8 -25.2 -12.3 -4.3 0.3 -2.0 -3.2 -21.5 11 24 10 34 21 17 -16.7 -5.8 0.4 -1.8 -5.5 -29.3 Profit before loan losses etc. 17.5 0.5 -6.3 16.4 -3.9 Impairment losses on loans and other ­commitments Net operating profit -3.1 14.5 -1.0 -0.5 -0.8 -7.1 -6.4 10.0 -1.8 -5.7 Income taxes Profit for the period 0.6 15.1 0.3 -0.2 2.6 -4.5 -75 2.2 12.2 0.4 -5.3 Attributable to: Non-controlling interests Shareholders in Bank of Åland Plc 0.2 14.9 0.2 -0.3 0.2 -4.7 32 0.6 11.6 1.2 -6.5 Earnings per share 1.03 -0.02 0.80 -0.54 56 -0.34 -47 Bank of Åland Plc Year-end Report, January–December 2012 8 Summary statement of other comprehensive income Q4 2012 Q3 2012 Profit for the period 15.1 -0.2 Cash flow hedge Assets available for sale Valuation differences Income tax on other comprehensive income Other comprehensive income -1.6 2.1 -6.7 -0.1 -6.3 1.1 -0.6 -0.3 0.3 Total comprehensive income for the period 8.8 0.1 Attributable to: Non-controlling interests Shareholders in Bank of Åland Plc 0.2 8.6 0.1 -0.1 Bank of Åland Group % Q4 2011 % 2012 2011 -4.5 12.2 -5.3 0.6 1.0 -0.2 1.5 -1.6 3.6 -8.1 -0.5 -6.5 0.7 -0.2 -0.2 0.3 5.6 -5.0 0.6 5.0 1.2 -6.2 % EUR M 94 -49 -12 -3.1 73 0.2 -3.2 32 -47 Bank of Åland Plc Year-end Report, January–December 2012 9 Income statement by quarter Bank of Åland Group Q4 2012 Q3 2012 Q2 2012 Q1 2012 Q4 2011 EUR M Net interest income Net commission income Net income from securities transactions and foreign exchange dealing Net income from financial assets available for sale Net income from investment properties IT income Other operating income Total income 9.9 9.2 10.2 7.7 9.6 7.6 11.5 8.0 12.1 8.3 8.4 10.9 0.0 3.7 0.6 42.7 1.1 -0.6 0.0 3.5 0.1 22.0 0.7 0.2 0.0 3.6 0.5 22.3 -0.2 0.2 0.0 3.7 0.1 23.3 0.7 -1.3 0.8 2.2 0.3 23.0 Staff costs Other administrative expenses Production for own use Depreciation/amortisation Other operating expenses Total expenses -13.7 -5.4 0.3 -2.6 -3.8 -25.2 -12.3 -4.3 0.3 -2.0 -3.2 -21.5 -13.0 -5.7 0.5 -1.8 -3.7 -23.7 -13.2 -5.2 0.4 -1.7 -3.8 -23.5 -16.7 -5.8 0.4 -1.8 -5.5 -29.3 Profit before loan losses etc. 17.5 0.5 -1.4 -0.2 -6.3 Impairment losses on loans and other commitments Net operating profit -3.1 14.5 -1.0 -0.5 -1.5 -3.0 -0.9 -1.1 -0.8 -7.1 Income taxes Profit for the period 0.6 15.1 0.3 -0.2 0.9 -2.0 0.4 -0.7 2.6 -4.5 Attributable to: Non-controlling interests Shareholders in Bank of Åland Plc 0.2 14.9 0.2 -0.3 0.1 -2.2 0.1 -0.8 0.2 -4.7 Bank of Åland Plc Year-end Report, January–December 2012 10 Statement of changes in equity capital Bank of Åland Group EUR M Equity capital, Dec 31, 2010 Comprehensive income for the period Dividend paid Other changes in equity capital attributable to minority interests Share issue Purchases of own shares Equity capital, Dec 31, 2011 Comprehensive income for the period Dividend paid Purchases of own shares Other Equity capital, Dec 31, 2012 Noncontrolling Unrestricted Share Cash Fair Shareholders’ interests’ Share equity premium Reserve flow Own value Translation Retained portion of portion of capital capital fund account fund hedge shares reserve difference earnings equity capital equity capital 23.3 0.0 5.8 24.5 29.1 24.5 33.3 33.3 25.1 25.1 0.0 0.0 0.0 -0.1 -0.1 -1.2 1.3 8.0 62.9 153.8 0.6 154.5 0.5 -0.2 -6.5 0.0 -6.2 0.0 1.2 -1.2 -5.0 -1.2 0.0 30.3 2.0 0.0 2.0 30.3 1.8 7.8 56.4 -0.1 177.9 0.0 2.6 -0.1 180.6 2.7 -8.1 11.6 0.0 5.0 0.0 0.6 0.0 5.6 0.0 0.5 68.4 -0.2 0.0 182.8 0.0 3.2 -0.2 0.0 186.0 -0.2 29.1 24.5 -0.5 32.8 25.1 -1.2 -0.2 Total 4.5 -0.3 Bank of Åland Plc Year-end Report, January–December 2012 11 Summary cash flow statement Bank of Åland Group Dec 31, 2012 Dec 31, 2011 10.0 16.5 -16.8 -2.3 -96.3 -5.7 15.7 -1.2 -3.5 -60.4 EUR M Cash flow from operating activities Net operating profit Adjustment for net operating profit items not affecting cash flow Gains/losses from investing activities Income taxes paid Changes in assets and liabilities in operating activities -88.9 -54.9 Cash flow from investing activities Cash flow from financing activities Exchange rate differences in cash and cash equivalents Change in cash and cash equivalents 2.3 144.8 2.8 60.9 -0.5 -66.8 0.7 -121.5 Cash and cash equivalents, January 1 Cash and cash equivalents, December 31 Change in cash and cash equivalents 184.7 245.6 60.9 306.2 184.7 -121.5 Bank of Åland Plc Year-end Report, January–December 2012 12 Notes to the consolidated interim report 1. Corporate information The Bank of Åland Plc (Ålandsbanken Abp) is a Finnish public limited company, organised in compliance with Finnish legislation and with its Head Office in Mariehamn. The Bank of Åland Plc is a commercial bank with a total of 18 offices. Through its subsidiary Crosskey Banking Solutions Ab Ltd, the Bank of Åland Group is also a supplier of modern banking computer systems for small and medium-sized banks. The Head Office of the Parent Company has the following registered address: Bank of Åland Plc Nygatan 2 AX-22100 Mariehamn. Åland Finland A copy of the consolidated financial statements can be obtained from the Head Office or from the Internet website ­­www.alandsbanken.fi. The shares of the Bank of Åland Plc are traded on the Nasdaq OMX Helsinki Oy (Helsinki Stock Exchange). The consolidated financial statements for the financial year ending December 31, 2012 were approved by the Board of Directors on February 15, 2013 and will be submitted to the 2013 Annual General Meeting for adoption. The Annual General Meeting has the opportunity to adopt or refrain from adopting the financial statements. 2. Basis for preparation and essential accounting principles BASIS FOR PREPARATION The Interim Report for the period January 1–December 31, 2012 has been prepared in compliance with the International Financial Reporting Standards (IFRSs) that have been adopted by the European Union (EU). The Year-end Report does not contain all information and notes required in annual financial statements and should be read together with the consolidated financial statements for the year ending December 31, 2011. ESSENTIAL ACCOUNTING PRINCIPLES The essential accounting principles used in preparing the Year-end Report are the same as the essential accounting principles used in preparing the financial statements for the year ending December 31, 2011. 3. Estimates and judgements Preparation of financial statements in compliance with IFRSs requires the Company’s Executive Team to make estimates and judgements that affect the recognised amounts of assets and liabilities, income and expenses as well as disclosures about commitments. Although these estimates are based on the best knowledge of the Executive Team on current events and measures, the actual outcome may diverge from the estimates. Bank of Åland Plc Year-end Report, January–December 2012 13 4. Capital adequacy Bank of Åland Group Dec 31, 2012 Dec 31, 2011 Tier 1 capital Supplementary capital Total capital base 152.9 73.3 226.2 145.5 75.3 220.7 Capital requirement for credit risks Capital requirement for operational risks Capital requirement for market risks Total capital requirement 98.1 14.1 0.0 112.2 123.0 14.1 1.4 138.5 16.1 10.9 10.9 12.8 8.4 8.4 EUR M Total capital ratio. % Tier 1 capital ratio. % Core Tier 1 capital ratio, % On February 13, 2012, the Finnish Financial Supervisory Authority approved the Bank’s application to be allowed to calculate the capital requirement for credit risk according to the Internal Ratings Based (IRB) approach for the Finnish household portfolio. Comparative figures are calculated according to the standardised approach. The calculation for the IRB approach did not apply the 80 per cent floor rule. Taking this transitional rule into account, the total capital ratio was 14.6 per cent and the Tier 1 capital ratio 9.8 per cent. Bank of Åland Group Dec 31, 2012 Dec 31, 2011 Equity capital according to the balance sheet 186.0 186.6 Intangible assets Property revaluation upon transition to IFRSs Surplus value in pension liability according to IAS 19 Fair value reserve Proposed dividends including subsidiaries 50% of expected losses according to IRB beyond those recognised Deferred tax assets Translation differences Fair value, financial liabilities Cash flow hedge Core Tier 1 capital -10.9 -7.8 -5.4 -4.5 -2.9 -3.2 -0.6 0.3 0.8 1.2 152.9 -12.0 -8.0 -5.1 -1.8 0.0 0.0 -0.8 -7.8 0.5 0.0 145.5 EUR M Bank of Åland Plc Year-end Report, January–December 2012 14 5. Segment report The Bank of Åland Group reports operating segments in compliance with IFRS 8, which means that operating segments reflect the information that the Group’s Executive Team receives. In order to match the Bank of Åland’s internal reporting to the Group’s Executive Team, segment reporting in the Year-end Report for the period January–December 2012 has been changed. The comparative period has been restated to correspond to the new segment report. The “Åland” business area includes office operations in Åland and equities trading operations in Mariehamn. The “Finnish Mainland” business area includes office operations on the Finnish mainland, Ålandsbanken Asset Management Ab and equities trading operations on the Finnish mainland, including Ålandsbanken Equities Research Ab (merged with the Bank on December 14, 2012). The “Sweden” business area includes the operating units Ålandsbanken Abp (Finland) svensk filial (the Swedish branch of the Bank of Åland Plc), Ålandsbanken Asset Management AB (until its divestment on October 26, 2012) plus Ålandsbanken Fonder AB and Alpha Management Company S.A. The “Crosskey” business area includes Crosskey Banking Solutions Ab and S-Crosskey Ab. “Corporate and eliminations” include all central corporate units in the Group, intra-Group eliminations and the subsidiaries Ålandsbanken Fondbolag Ab and Ab Compass Card Oy Ltd. The figures for 2011 have been restated in such a way that they are comparable with the figures in the 2012 segment report. Bank of Åland Group 2012 EUR M Åland Finland Sweden Crosskey Corporate and eliminations Total Net interest income Commission income Other income Nonrecurring income 1 Total income 11.8 6.7 0.6 1.0 20.0 17.3 13.4 0.3 0.0 31.0 11.3 11.1 1.0 12.9 36.3 -0.1 0.0 27.8 0.0 27.6 0.9 1.5 -7.1 0.0 -4.6 41.2 32.7 22.6 13.9 110.4 Staff costs Other expenses Internal allocation of expenses Restructuring expenses Total expenses -4.1 -4.3 -7.4 -0.1 -15.8 -8.7 -7.7 -12.1 0.0 -28.4 -12.3 -7.0 -10.6 -0.6 -30.4 -13.6 -11.7 0.0 -0.4 -25.7 -12.5 -11.1 30.0 0.0 6.4 -51.2 -41.7 0.0 -1.1 -94.0 Profit before loan losses etc. 4.2 2.5 5.9 1.9 1.9 16.4 Impairment losses on loans and other commitments Net operating profit -3.6 0.6 -2.7 -0.1 0.2 6.1 0.0 1.9 -0.4 1.4 -6.4 10.0 Income of EUR 13.8 M from divestment of the Swedish subsidiary, which had been emptied of operations; capital gain of EUR 1.0 M upon divestment of the associated company Ålands Företagsbyrå and impairment losses of EUR 0.8 M on the Bank’s shareholding in Burgundy. 1 Bank of Åland Group 1 2011 EUR M Åland Finland Sweden Crosskey Corporate and eliminations Total Net interest income Net commission income Other income Nonrecurring income 1 Total income 14.3 6.6 0.6 0.0 21.5 19.5 16.9 0.1 0.0 36.6 9.0 14.2 1.4 -1.1 23.6 0.0 0.0 31.2 0.0 31.2 0.2 1.1 -14.9 0.0 -13.6 43.1 38.7 18.5 -1.1 99.2 Staff costs Other expenses Internal allocation of expenses Restructuring expenses Total expenses -4.1 -3.0 -9.0 0.0 -16.1 -9.3 -7.4 -15.0 -0.2 -31.8 -13.4 -9.9 -11.9 -5.2 -40.4 -13.8 -13.1 0.0 0.0 -26.9 -13.9 -9.5 35.9 -0.3 12.2 -54.5 -42.8 0.0 -5.7 -103.1 Profit before loan losses etc. 5.3 4.8 -16.9 4.2 -1.4 -3.9 Impairment losses on loans and other commitments Net operating profit 0.1 5.5 -2.4 2.4 0.2 -16.6 0.0 4.2 0.2 -1.2 -1.8 -5.7 Impairment loss of EUR 1.1 M on the Bank’s shareholding in Burgundy. Bank of Åland Plc Year-end Report, January–December 2012 15 6. Managed assets Bank of Åland Group Dec 31, 2012 Dec 31, 2011 % 867 1,991 1,433 4,292 757 1,798 1,260 3,814 15 11 14 13 362 338 7 EUR M Fund unit management Discretionary asset management Other asset management Total managed assets Of which own funds in discretionary and other asset management 7. Deposits from the public and public sector, including bonds and certificates of deposit issued Bank of Åland Group Dec 31, 2012 Dec 31, 2011 % 1,652 475 2,127 1,568 579 2,147 5 -18 0 186 134 320 189 208 397 -2 -35 -19 2,447 2,544 -4 EUR M Deposit accounts from the public and public sector Sight deposits Time deposits Total deposit accounts Bonds and subordinated debentures 1 Certificates of deposit issued to the public 1 Total bonds and certificates of deposit Total deposits 1 This item does not include debt securities subscribed by credit institutions. Bank of Åland Plc Year-end Report, January–December 2012 16 8. Lending to the public and public sector by purpose Bank of Åland Group Dec 31, 2012 Dec 31, 2011 % 74 55 140 334 178 22 108 14 36 35 996 63 57 95 335 187 19 109 13 45 36 958 18 -4 48 0 -4 13 -1 9 -20 -3 4 1,251 309 126 202 1,889 1,161 294 126 177 1,757 8 5 0 14 7 21 21 22 22 -5 -5 2,906 2,737 6 EUR M Companies Shipping Wholesale and retail trade Housing operations Other real estate operations Financial and insurance operations Hotel and restaurant operations Other service operations Agriculture, forestry and fishing Construction Other industry and crafts Total, companies Private individuals Home loans Securities and other investments Business operations Other household purposes Total, households Public sector and non-profit organisations Total, public sector and non-profit organisations Total lending 9. Impairment losses and doubtful receivables Bank of Åland Group Q4 2012 Q3 2012 % Q4 2011 % 1.1 2.0 0.0 3.1 1.0 0.0 0.0 1.0 Dec 31, 2012 Sep 30, 2012 % Dec 31, 2011 % 12.7 10.6 3.1 16.1 9.7 1.1 -21 9 12.5 7.7 1.1 2 38 -1.1 5.3 3.6 108 0.44 18.6 0.64 67 0.56 25.0 0.86 71 0.5 19.3 0.70 EUR M Individual impairment losses Group impairment losses Reversals Recognised in income statement Gross doubtful receivables Individual impairment losses Group impairment losses Net doubtful receivables Level of provisions for doubtful receivables, % Doubtful receivables as % of total Of which > 90 days past due Non-performing receivables as % of total 1.0 0.0 -0.1 0.8 -26 -4 Bank of Åland Plc Year-end Report, January–December 2012 17 10. Off-balance sheet commitments Bank of Åland Group Dec 31, 2012 Dec 31, 2011 % 15 69 88 195 367 19 90 80 188 377 -21 -23 10 4 -3 EUR M Guarantees and pledges Unutilised overdraft limits Unutilised credit card limits Other commitments 11. Restructuring reserve Bank of Åland Group Dec 31, 2012 New reserve Utilised Withdrawn Dec 31, 2011 1.0 0.1 0.0 1.1 0.6 0.1 0.0 0.7 -2.9 -0.5 -0.1 -3.4 -0.3 0.0 0.0 -0.4 3.6 0.5 0.1 4.2 EUR M Staff costs Rent IT Total 12. Goodwill Bank of Åland Group Dec 31, 2012 Dec 31, 2011 % 1.4 1.4 1.4 1.4 0 0 EUR M Opening balance Closing balance 13. Net interest income Bank of Åland Group Q4 2012 Q3 2012 % Q4 2011 % Credit institutions and central banks The public and public sector entities Debt securities Other interest income Total 0.3 17.4 1.1 0.1 18.9 0.3 19.3 1.7 0.3 21.5 16 -10 -36 -52 -12 0.6 20.8 2.0 0.6 24.0 -53 -16 -46 -79 -21 Interest expenses Credit institutions and central banks The public and public sector entities Debt securities Subordinated liabilities Other interest expenses Total -1.5 -4.8 -2.0 -0.4 -0.3 -9.0 -1.4 -6.2 -2.8 -0.4 -0.5 -11.3 4 -21 -31 -1 -37 -20 -0.8 -6.3 -3.8 -0.5 -0.5 -11.9 83 -23 -49 -14 -40 -25 9.9 10.2 -3 12.1 -18 EUR M Interest income Net interest income Bank of Åland Plc Year-end Report, January–December 2012 18 14. Commission income Bank of Åland Group Q4 2012 Q3 2012 % Q4 2011 % Deposits Lending Payment intermediation Mutual fund commissions Management commissions Securities commissions Other commissions Total 0.2 0.7 2.0 2.8 2.3 2.6 0.5 11.1 0.2 0.6 1.8 2.2 1.7 2.0 0.6 9.2 -1 14 8 25 35 26 -4 20 0.2 0.1 1.8 2.1 2.2 3.2 0.5 10.3 6 8 32 4 -21 3 8 Commission expenses -1.9 -1.6 23 -1.9 -2 Net commission income 9.2 7.7 20 8.3 11 Q4 2012 Q3 2011 % Q4 2011 % -0.7 1.4 0.6 -0.8 1.1 0.3 10 25 0.1 2.5 2.6 -46 -75 EUR M 15. Income taxes Bank of Åland Group EUR M Taxes for the period and prior periods Change in deferred tax assets/liabilities Income taxes 16. Dividend Bank of Åland Group Dec 31, 2012 Dec 31, 2011 euro Proposed dividend for 2012: EUR 0.15 per share Final dividend for 2011: EUR 0.00 per share 2,163,023 0 Bank of Åland Plc Year-end Report, January–December 2012 19 17. Derivative contracts Bank of Åland Group EUR M Value of underlying property Interest rate derivatives Forward contracts Swap contracts Option contracts Purchased Written Currency derivatives Forward contracts Interest rate and currency swap contracts Option contracts Purchased Written Equity derivatives Option contracts Purchased Other derivatives Total Dec 31, 2012 For hedging purposes Dec 31, 2011 Other For hedging purposes Other 0 336 0 51 224 505 224 39 16 0 0 16 15 10 10 15 55 262 8 3 55 237 7 4 0 0 0 0 0 0 0 0 118 13 800 0 13 90 149 0 1,195 0 0 300 The equity derivatives that were purchased hedge option structures that are embedded in bonds issued to the public. Bank of Åland Plc Year-end Report, January–December 2012 20 18. Maturity breakdown of claims and liabilities Bank of Åland Group EUR M Dec 31, 2012 < 3 months 3 –12 months 1– 5 years > 5 years Not classified by maturity Total Claims Cash Debt securities eligible for refinancing with central banks Claims on credit institutions Claims on the public and public sector entities Debt securities Shares and participations Shares and participations in associated companies Derivative instruments Intangible assets Tangible assets Other assets Accrued income and prepayments Deferred tax assets Total claims Liabilities Liabilities to credit institutions Liabilities to the public and public sector entities Debt securities issued Derivative instruments Other liabilities Accrued expenses and prepaid income Subordinated liabilities Deferred tax liabilities Equity capital Total liabilities 133 133 6 104 10 237 52 305 104 268 25 395 20 1,521 722 2,906 45 534 425 1,758 162 52 160 1,891 142 233 70 4 484 774 7 7 1 20 11 33 45 26 3 145 1 20 11 33 45 26 3 3,637 375 63 15 68 28 4 2,195 360 24 672 37 99 16 186 311 2,127 760 15 68 28 64 16 186 3,637 Bank of Åland Plc Year-end Report, January–December 2012 21 Bank of Åland Group EUR M Claims Cash Debt securities eligible for refinancing with central banks Claims on credit institutions Claims on the public and public sector entities Debt securities Shares and participations Shares and participations in associated companies Derivative instruments Intangible assets Tangible assets Other assets Accrued income and prepayments Deferred tax assets Total claims Liabilities Liabilities to credit institutions Liabilities to the public and public sector entities Debt securities issued Derivative instruments Other liabilities Accrued expenses and prepaid income Subordinated liabilities Deferred tax liabilities Equity capital Total liabilities Dec 31, 2011 < 3 months 3 –12 months 1– 5 years > 5 years Not classified by maturity 66 Total 66 9 129 57 41 18 125 129 350 71 333 92 1,207 35 847 3 2,737 198 3 1 20 11 32 46 26 4 145 1 20 11 32 46 26 4 3,400 626 482 1,282 200 1,790 163 284 402 18 91 865 30 230 0 2 2,147 659 14 63 14 63 30 5 2,153 692 34 143 18 51 20 181 362 30 58 20 181 3,400 Bank of Åland Plc Year-end Report, January–December 2012 22 19. Interest rate refixing periods Bank of Åland Group EUR M Assets Liabilities Difference between assets and liabilities Dec 31, 2012 < 3 months 3–6 months 6–12 months 1–5 years > 5 years Total 2,435 2,721 343 223 390 200 556 458 81 55 3,806 3,657 -286 120 190 99 26 149 < 3 months 3–6 months 6–12 months 1–5 years > 5 years Total 2,721 2,727 410 420 396 294 463 400 59 67 4,050 3,909 -5 -10 101 63 -8 141 Bank of Åland Group EUR M Assets Liabilities Difference between assets and liabilities Dec 31, 2011 Shows the Bank’s interest rate-related assets and liabilities, including derivatives at underlying value, according to the interest rate refixing date. 20. Hours worked, recalculated to full-time equivalent positions Bank of Åland Group Q4 2012 Q3 2012 % Q4 2011 % 381 199 0 26 12 5 3 0 387 199 0 25 13 6 3 0 -2 0 0 12 -8 -100 4 -8 -17 0 0 340 217 94 24 12 6 4 -100 626 633 -1 697 -10 Bank of Åland Plc Crosskey Banking Solutions Ab Ltd Ålandsbanken Sverige AB Ålandsbanken Asset Management Ab Ab Compass Card Oy Ltd Ålandsbanken Fondbolag Ab Ålandsbanken Fonder AB Ålandsbanken Equities Research Ab Total number of positions, recalculated from hours worked 8 0 -17 From December 1, 2011, most of the operations of Ålandsbanken Sverige AB were transferred to Ålandsbanken Abp (Finland) svensk filial, the Swedish branch of Bank of Åland Plc. This means that hours worked in the branch are reported as part of Bank of Åland Plc. 21. Assets pledged for covered bonds Bank of Åland Group Dec 31, 2012 Sept 30, 2012 665 665 533 533 % Dec 31,2011 % EUR M Assets pledged for covered bonds Total 25 25 0 0 Bank of Åland Plc Year-end Report, January–December 2012 23