An Overview of Attestation Services in India

advertisement

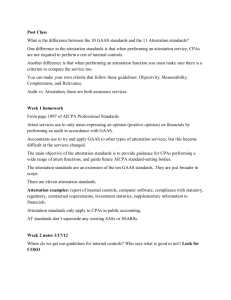

AUDITING 430 An Overview of Attestation Services in India The attestation function is a core competence area of chartered accountant professionals. The society at large is relying on the attestation services for ensuring that the public funds are utilised properly. In case where scams are discovered and millions of dollars gets into wrong hands, we should realise that either there were no attestation services utilised or, if they were, then there were lapses. The need of the hour is to ensure that a significant section of economic activities in the country come under the ambit of independent attestation services. If all the financial transactions are audited properly, no scam can take place in the country, and by ensuring proper utilisation of funds we can improve the lot of our citizens. New Dawn of Accountancy Profession in India After India got Independence in the year 1947, the national leaders realised the need of an organised accounting profession to contribute towards the economic growth and development of the country. Therefore, The Institute of Chartered Accountants of India (ICAI) was established as a statutory body under the Chartered Accountants Act, 1949 (Act No. XXXVII of 1949) for regulating the profession of chartered accountants in India. CA. K. L. Chandak (The author is a member of the Institute. He can be reached at eboard@icai.org) 54 THE CHARTERED ACCOUNTANT Significance of CAs in Attestation Services The key role of profession of chartered september 2010 accountants involves checking of all types of financial statements and certifying them. It inter-alia includes services in the nature of Statutory Audit, Internal Audit, Inspection Audit, Tax Audit, Stock Audit, Certification and allied various other attestation services. Since the establishment of ICAI in the year 1949, only the practicing members who are holding either the part time or full time certificate of practice, are empowered to attest and certify various financial statements which are then relied upon by the society/stakeholders. Thus, in a way, this entrusts an absolute exclusivity to chartered accountants in the field of attestation services as described above. AUDITING 431 Expertise in the Field of Attestation Services The primary area of expertise rendered to a student of chartered accountancy is with respect to auditing and accounts. But due to exceptional quality of the course, the student gains substantial expertise in the allied areas of the Companies Act, Income Tax, Wealth Tax, Gift Tax, Service Tax, Excise & Customs, Sales Tax, FEMA and lot of other enactments which directly or indirectly affects financial transactions. The reason for such a vast course being that a chartered accountant has to take a view in totality and need to be capable of understanding the larger picture before forming a view on the micro topic. This provides him ability to understanding complex situation involving various enactments effecting a certain transaction and ensures that the position is reflected as desired and any violation of any provisions can be highlighted. Expanded Area of Services in Various Allied Areas As the path to chartered accountancy enables a professional student clear At the time of setting up of the ICAI, it was thought beyond doubt that the attestation services shall be carried out and treated as profession and not as a business. Therefore, there was no scope for advertisement, etc., for attestation services. Even the size of name board was kept to a limited size just to reach the location of the member and not for his publicity. It was presumed that the clients will avail the services of a professional by considering the experience, credibility, integrity and capability. This basic theme was very critical as the attestation services were considered the need of the society at large. edge on various peers, the services of chartered accountants are being availed by many sectors in India as well as abroad both in private- and public-sector companies as well as in the administration of the Central and State Governments. These sectors not only look forward to their expertise in attestation services, but utilise the overall capability of the chartered accountants. Since the setting up of the Institute more than 60 years ago, till date about 165,000 candidates have qualified as chartered accountants. Nearly 50 per cent thereof are in service and a significant number thereof have occupied eminent positions in their respective organisations such as chairperson at regulatory bodies, chairperson of banks and insurance companies, members of ITAT, etc. The remaining about 50 per cent members are in full time practice. Because of their expertise, they not only render attestation services but have engaged themselves in other areas such as providing services in the field of Accounting, Taxation, Company Law Matters, Financial Consultancy, Corporate Governance, Due Diligence, Transfer Pricing and various other areas. Need for Attestation Services With the rapid economic development in the country in the last 63 years, large sums are being spent on its developmental projects both in private as well as in public sector and therefore so far as economic activities are concerned they have increased manifold. Billions are being spent every year by the Central Government, the State Governments and municipal corporations, panchayats, etc., on various developmental projects and on providing civic amenities as well as on the administration. Private sector in the country has also grown tremendously. Indian industrialists are expanding throughout the world. India produces 900,000 engineers annually and the total number of CAs has reached only to about 165,000 over a period of 61 years. For any project where the services of engineers are required, there must be a need for the services of a chartered accountant, although not be in same ratio/ framework. Where there is expenditure whether revenue as capital, there is a need of the services of the chartered accountant to check the transaction to control any misuse or misappropriation of funds. Thus, both in the private as well as in the public sector there are ample opportunities for work for CAs. And if entire spectrum of financial transactions in the country is brought under the ambit of audit, it is for sure that the current strength of CAs will be far insufficient to carry out just the attestation services. Attestation Services: Serving the Society At the time of setting up of the ICAI, it was thought beyond doubt that the attestation services shall be carried out and treated as profession and not as a business. Therefore, there was no scope for advertisement, etc., for attestation services. Even the size of name board was kept to a limited size just to reach the location of the members and not for their publicity. It was presumed that the clients will avail the services of a professional by considering the experience, credibility, integrity and capability. This basic theme was very critical as the attestation services were considered the need of the society at large. Just like the code of conduct of medical profession doesn’t allow a doctor to carry on his profession like a business, CAs are expected to follow the dignity of their profession to the society. Let’s understand the criticality of distinction between profession and september 2010 THE CHARTERED ACCOUNTANT 55 AUDITING 432 While the Institute has been trying to help the members in developing other practice areas, it is equally important to note that the basic area of operation or dominance for CAs is the attestation services. Thus, we should do our best to ensure that a significant section of economic activities in the country move under the ambit of independent attestation services and the entire work is distributed evenly among the members at large and not concentrated with few players. business at this stage. The basic motive behind profession is to provide service to the society while maintaining complete integrity and trust and, thus, while the professional will charge for the service, the motive will not be to earn abnormal profits. On the other hand, a business focuses primarily on making profits and while it may be servicing society indirectly, that’s not the primary objective of a businessman. For instance, due to his profession, a doctor is expected to treat the patient with right medicine and not refer medicines purely for making money from the pharma company. Similarly, when a bank relies upon audited financial statements for lending to a company, its social money at the bank which is at stake. If CAs consider this as a way of making money from any given opportunity, they will be tempted to sign wrong certificates which will help the company mislead the bank. Thus, CAs should strictly maintain the dignity and high standards in the profession to maintain social respect. No Compromise in Attestation Function The society at large is relying on the attestation services for ensuring that 56 THE CHARTERED ACCOUNTANT the public funds are utilised properly. In case where scams are discovered and millions of dollars gets into wrong hands, we should realise that either there were no attestation services utilized or, if they were, there were lapses. In such cases, the society starts to feel that the chartered accountants are not performing their duties which negate the entire purpose of having an independent eye. It is very important for the entire profession to ensure that the quality of attestation is so high that any stakeholder should be able to completely rely on the same without a doubt. This will ensure that the public as well as private finances are utilized in the manner they are supposed to. There is a strict need for the chartered accountants to follow Code of Ethics in letter and spirit for everlasting reliability of the profession and continued trust of society at large. Due to the environment of intense competition, there may be situations in which few members may find it difficult to earn in proportion to their skills and hardwork. In such situations, some of the members may get ready to take up an assignment at a lower remuneration which may not justify the time/skills required to perform the same. This may result in compromise of quality on that assignment, which is completely unacceptable for the sake of profession. The concentration of work with larger firms may be one of the reasons for smaller firms/individual practitioner not getting allocated sufficient work / value for their work. While the large firms are welcome for the infrastructure they introduce in the system, we must not ignore the fact that the attestation services is all about individual responsibility and an individual practitioner can perform the same with same (or better) quality. We all must ensure that the quality levels are not compromised upon and thus society should be able to respect september 2010 all CAs for their skills, quality and integrity. Ensuring Quality of Attestation Services We as professional members need to brainstorm as to how to ensure an environment that none of the members is ready to compromise on the quality. As a backgrounder, the primary object of establishment of our Institute as an autonomous body through an Act of Parliament 61 years ago was to regulate the accountancy profession in India and thereby to mean to have a proper check on its members to ensure that various attestation services which are being rendered suit the needs of the society. To achieve this object a disciplinary committee is effectively working in the Institute takes disciplinary actions against errant members. Need to Put More Emphasis on Attestation Services Coming back to the basic question of why are the members diversifying to other areas from the core attestation services. As we discussed above, many members feel that the overall pie of the assignments available in the economy are not sufficient and some members do not get sufficient work. This induces them to other practice areas. While the Institute has been trying to help the members in developing other practice areas, it is equally important to note that the basic area of operation or dominance for CAs is the attestation services. Thus, we should do our best to ensure that a significant section of economic activities in the country move under the ambit of independent attestation services and the entire work is distributed evenly among the members at large and not concentrated with few players. Sometimes, it is noticed at the study circles, that the value addition for CAs gets limited to understanding the AUDITING 433 technology for filing TDS returns and VAT. While members of the Institute are willing to take up additional activities, let’s not ignore the fact that this is not our core area of competence and we have a much larger canvas to work and serve the society. The Institute is taking active steps to ensure that there are ample new opportunities for members to take up attestation services and that there are set processes to ensure proper distribution of the same among all members with healthy competition. Further, there is a need to more strictly ensure the quality of deliverables from members, meeting the highest norms and conforming to related standards. This fact should be communicated to the stakeholders at large to re-build the credibility which was somewhat lost after the Satyam episode. It’s an ongoing process where dialogues need to undergo between the Government and the Institute, and the Institute and various stakeholders. Enhancing the Value of Attestation Services The value of attestation services can be enhanced in the following ways: (1) By putting more emphasis on attestation services as the area of core competence for CAs – Diversification to other areas of professional expertise can be accorded a second priority and other services can be treated as incidental. (2)By expediting disciplinary actions against errant members. (3)By educating stakeholders about the importance of getting their accounts audited (4)By giving more importance to individual’s knowledge, skills, experience, integrity and credibility instead of the size of the firm and infrastructure. (5)By ensuring allocation of attestation work in a justifiable and equitable manner – There should be a mechanism whereby as far as the entire audit assignments available in the country be allotted to the maximum number of chartered accountants in practice in a justifiable manner based on the skills, knowledge, experience, integrity, credibility of the members and not on infrastructure and size only. It is for this reason that a ceiling has been fixed as to the number of audits a firm can audit under the provisions of the Companies Act, 1956. (6)By putting more stress on moral and ethical standards for CAs – Framing number of Accounting Standards or enforcing stringent Rules and Regulations alone would not serve the desired purpose unless the principles of high moral values are adopted to ensure integrity of our members. (7)By ensuring that the profession is not deviating from the path originally thought. What Practicing Members can Contribute (1) Ensure that attestation is a profession of service to the Society: Practicing members should know that this is a If all the financial transactions are audited properly no scam can take place in the country. Corruption shall also be eliminated altogether and if corruption is eliminated India can become one of the advanced countries in the world. ICAI and its members can play a significant role in the elimination of corruption and at the same time through proper utilisation of funds we can improve the conditions of our citizens. (2) (3) (4) (5) profession of service to the society where service is first and profit is secondary motto. Keeping this in mind, they should render their services. Ensure high moral character, ethical standards and integrity: While rendering attestation services, members must ensure high moral character, ethical standard and integrity that alone can bring good results. Do not try to snatch the work of others: Without communicating the previous member, no member should accept any attestation work. Render the services without favour and fear: While rendering services CAs’ report thereon should be without favour and fear so as to ensure the public confidence. Proper utilisation of your experience, knowledge and skill: While working on attestation services, CAs should utilise their full skills, knowledge and experience. Conclusion The need of the hour is to ensure that the credibility of attestation services is retained and to ensure that all financial transactions taking place in the Government sector as well as all transactions of private sector in which public funds are involved are brought under the ambit of audit by an independent auditor who should be a practicing member of ICAI. If all the financial transactions are audited properly no scam can take place in the country. Corruption shall also be eliminated, altogether and if corruption is eliminated, India can become one of the most advanced countries in the world. ICAI and its members can play a significant role in the elimination of corruption and, at the same time, through proper utilisation of funds, we can improve the conditions of our citizens.n september 2010 THE CHARTERED ACCOUNTANT 57