ROI, Residual Income and EVA

advertisement

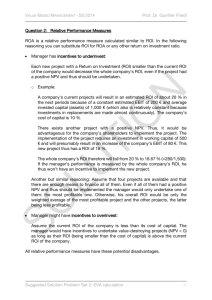

Performance Measurement Using IncomeRelated Measures Types of Performance Centers Type of Ctr Cost Income Investment Manager Controls: Costs Revenues Investments D D D D D D Functional organization President VP Manufacturing VP Sales Controller Type title here Etc. Divisional organization: President/CEO Plastic Products Div. VP Manufacturing Electronics Division VP Sales Accounting Food Services Div. VP Etc. [Each fairly autonomous. The assumed structure for ROI!] Etc. ROI=(Net Income)/(Invested Capital) Problems of definition and measurement. NET INCOME Definition ! Absorption-costing? with/without allocation of noncontrollable costs ! Contribution approach? with/without allocation of noncontrollable costs Measurement ! Historical cost basis? ! Some definition of current cost? Replacement cost Current market (exit) value? Inflation index adjustment? INVESTED CAPITAL Definition(what to include) Conceptually, include the assets used to generate the income in the numerator. Total assets available? Total assets employed (omit, e.g., construction in progress)? Wkg Capital + other assets, i.e., Assets- ST. Liab.? Shareholders' Equity??? Measurement of invested capital: Historical book value? Original Cost? Net of deprec? (what kind?) Current value? Replacement? Current mkt (exit)? Inflation index? COMPONENTS OF ROI Sales Invested Capitol x NI Sales = ROI ù ù Capital turnover Profit margin (Also called Return on Sales) This is the "DuPont" method. Emphasizes that both or either factor can be changed to improve ROI E.G., T/O Housewares 2 Groceries 10 Mgn ROI 10% 20% 2% 20% Different ROI's are appropriate for evaluating.... Managers vs. Segments Purpose: Raise, Bonus Retention, expansion What to Controllable Items traceable Include items to the segment Residual Income Dysfunctional effect of ROI: can lead to a lack of “goal congruence.” E.G., Corporate mgt. wants 15% min. return on investment. Div. A currently earns 19% Div. B currently earns 14% Div. C currently earns 16% Investment opportunity: chance to invest $100,000 that will earn 16%($16,000/yr). Lack of goal congruence: Corporate mgt. wants to invest Div. A or C mgrs reject. Residual Income overcomes the conflict: Income for the year $16,000 Less imputed interest 15,000 at 15% Residual Income $ 1,000 (Same regardless of division. Any mgr. should view investment the same way) Why has RI not replaced ROI? Economic Value Added (EVA) All material below taken from Esa Mäkeläinen's Master's thesis at the Helsinki School of Economics, 1998 Background of EVA EVA is not a new discovery. $ variation of residual income $ Stern Stewart & Co. trademarked “EVA” $ often called Economic Profit (EP) to avoid trademarking problems $ In the 1970s or earlier RI failed get wide publicity or become popular $ However EVA, practically the same concept with a different name, has done it in the recent years. Furthermore the spreading of EVA and other residual income measures does not look to be on a weakening trend. Main theory behind EVA EVA measures whether the operating profit is enough compared to the total costs of capital employed. It is net operating profit after taxes (NOPAT) subtracted with a capital charge: EVA = NOPAT - CAPITAL COST EVA = NOPAT - COST OF CAPITAL x CAPITAL employed Or equivalently, if rate or return is defined as NOPAT/CAPITAL, this turns into a perhaps more revealing formula: EVA = (RATE OF RETURN - COST OF CAPITAL) x CAPITAL Where: 1. 2. 3. Rate of return = NOPAT/Capital Capital = Total balance sheet minus non-interest bearing debt (i.e., accounts payable) in the beginning of the year Cost of capital = Cost of Equity x (% of capital from equity) + Cost of debt x (% of capital from debt) x (1-tax rate). Cost of equity capital is the opportunity return from an investment with same risk as the company has. Cost of debt is naturally more straightforward, and includes the tax shield due to tax allowance on interest expenses. If ROI is defined after taxes then EVA can be presented with familiar terms to be: EVA = (ROI - WACC) x CAPITAL EMPLOYED