Aegon Retirement Choices: Investor Protection Guide

advertisement

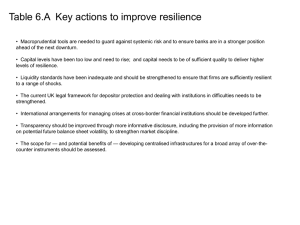

For adviser use only – not approved for use with clients Investor protection through Aegon Retirement Choices and One Retirement This guide outlines how we protect your clients’ money and, should the worst happen, illustrates the level of protection your client can expect to receive through Aegon Retirement Choices (ARC) and One Retirement. Contents: As easy as one, two, three 3 Protection at a glance 4 Aegon’s responsibilities 6 Investment providers’ responsibilities 7 FSCS responsibilities 7 Who can claim? 8 FSCS limits 9 Page 2 of 11 As easy as one, two, three Whether your client invests through ARC or One Retirement they’ll receive three levels of protection. Protection level How it works Aegon – level 1 Aegon has a responsibility to clients to manage their assets responsibly. This is why we separate clients’ assets from our own. This makes sure that in the event of us defaulting, all or most client assets are still owned by the client, so can’t be used to settle creditor claims. Doing this protects the assets for the client. Exceptions to this could be if investments are trading within an institutional share class, or if re-insurance on investments has taken place. Investment providers – level 2 There are various regulatory measures in place that most investment providers must follow to operate within the UK. These measures are aimed at helping to protect investors’ assets. Examples of these measures are the regulatory liabilities for OEICs (Open-ended investment companies) to: • separate clients’ assets from the manager’s own assets; and • make sure the structure and management of the funds are in line with the Financial Conduct Authority (FCA) guidelines. These guidelines are in place to make sure the assets are protected from misuse, or the firm defaulting. Financial Services Compensation Scheme – level 3 The FSCS (Financial Services Compensation Scheme) protects investors’ assets by funding certain shortfalls if a company is unable, or likely to be unable, to meet claims against it. The FSCS will only become involved if a company is: • FCA or Prudential Regulation Authority (PRA) (or previously, FSA, FIMBRA or the PIA) authorised; and • unable, or likely to be unable, to meet claims against it. Page 3 of 11 Protection at a glance Through ARC and One Retirement your client can access a range of investments with various levels of complexity. The measures taken to protect your client’s assets could depend on the type of investment. Take a look at the table below to find out how each type of investment is generally treated. Investment type Level 1 Aegon Level 2 Investment provider Level 3 FSCS Cash Assets are ring fenced from the investment provider’s own assets. Funds are protected up to £85,000 per eligible claimant per authorised firm. • Funds are held separately from our own assets. • Depending on the product, funds are managed in accordance with the FCA’s Conduct of Business Sourcebook rules (COBS), Markets in Financial Instruments Directive (MiFID) or client money rules which prohibit the misuse of clients’ money. Insured funds (internal funds) Funds are insured and have governance and management protocols which you can find at aegon.co.uk/funds/ governance Scottish Equitable Funds are protected plc ring fences the for 100% of total assets within these assets held. funds from their own. Insured funds (external fund links) Insured funds with external fund links (EFLs) are monitored by us to check they’re managed in line with the underlying fund manager’s objectives. These are monitored in line with our governance and management protocols which you can find at aegon.co.uk/ funds/governance Funds are ring fenced from the underlying investment provider’s own assets. Some funds are protected up to 100% of total assets held. If reinsurance takes place no protection is offered. (Reinsurance is where an insured fund buys units within another insured fund). Collectives (retail) Funds are ring fenced from our own assets. Funds are ring fenced from the investment provider’s own assets. Some funds are protected up to £50,000 of total assets held. Page 4 of 11 Investment type Level 1 Aegon Level 2 Investment provider Level 3 FSCS Collectives (institutional) Funds are owned by us, so no protection is provided and in the event Aegon became insolvent these assets could be made available to creditors. As a large company Aegon may be classified as a creditor and can claim against the investment provider’s own assets as a creditor, if suitable. As these funds are held in the name of the nominee companies (see below), claims can’t be made to the FSCS as Aegon is classified as a large company. Exchange traded funds (ETFs) Funds are ring fenced from our own assets. Funds are ring fenced from the investment provider’s own assets. (Loan credits on ETFs may not be protected unless specifically stated.) No protection offered. Equities Funds are ring fenced from our own assets. Not applicable. No protection offered. Structured products Funds are ring fenced from our own assets. The underlying structure and setup of the product may vary, this could impact the level of assurance and protection offered. Protection depends on the structure and setup of the product. Guarantees Funds are ring fenced from our own assets. Funds are ring fenced from the investment provider’s own assets. Funds are protected for 100% of total assets held. See our guarantees section. Page 5 of 11 Aegon’s responsibilities The Aegon SIPP (available through ARC) and One Retirement account are pensions provided under the Aegon Self-invested Personal Pension Scheme. This is a trust based personal pension scheme, with Aegon Pension Trustee Limited (APT) as the trustee. The assets of the scheme are owned by APT, separating them from the assets of Scottish Equitable plc. Aegon Investment Solutions Limited (AISL) is responsible for the management of ARC’s ISA and General Investment Account (GIA). APT and AISL have appointed nominee companies to hold the assets on their behalf. The nominee companies are: • SIPP and One Retirement – Aegon SIPP Nominee Limited • ISA – Aegon Nominee 3 (ISA) Limited • GIA (net) – Aegon Nominee 2 (Net) Limited • GIA (gross) – Aegon Nominee 1 (Gross) Limited Aegon Investment Solutions Limited As the manager of our ISA and GIA, AISL is responsible for making sure that the operational management of these products is in line with the MiFID and Client Assets (CASS) regulations. These regulations make sure that the relevant investment restrictions apply to ISAs, and clients’ assets are protected and responsibly administered. AISL separates clients’ assets from Aegon’s own assets to ensure that if in the event Aegon was to default, the clients’ assets would be protected from any possible creditors or outstanding liabilities. Aegon Pension Trustees Limited It’s the responsibility of APT, and Scottish Equitable plc as the scheme administrator, to make sure all assets held or managed by Aegon are in line with the FCA’s COBS regulations, and that we take the necessary measures to protect our clients’ assets. These measures can include: • carrying out regular due diligence on banks and fund managers; • making sure clients’ assets are not used to fund other activities; • making sure the record keeping of clients’ assets are correctly managed; and • holding clients’ assets separately from our own so if in the event Aegon defaulted, clients’ assets would be protected from any possible creditors or outstanding liabilities. Page 6 of 11 Investment providers’ responsibilities With many investments, the legal structure required to manage the investment ensures greater protection of clients’ assets, such is the case with collectives that operate in line with the Financial Service and Markets Act 2000 (FSMA). Collective fund schemes have a responsibility to appoint a depositary who is independent to the fund’s board or the fund’s authorised corporate director. The depositary is responsible for ensuring the assets are segregated from the fund manager’s own assets and oversees the safe custody of these assets. Like collectives, unit trusts appoint a trustee who has similar responsibilities to that of a depositary for a collective and who’s responsible for ensuring the fund manager keeps to the fund’s investment objective and safeguards the trust’s assets. FSCS responsibilities The FSCS is an independent body set up under the FSMA. The FSCS deals with claims against authorised firms regulated by the FCA or PRA. This usually happens because a firm has stopped trading and doesn’t have enough assets to meet claims, or is in insolvency. This is described as being in default. The primary role of the FSCS is to protect policyholders. They work with insolvency practitioners, responsible for the ongoing administration of the firm and the settlement of claims, to determine their involvement to make sure that policyholders have clear instructions on how to make a claim, and what to do if they need immediate assistance. The FSCS can also provide funds to meet protected claims. This can include returning premiums if a firm is unable to. In some cases, funds from the insolvent firm may be available to pay some of the amount due to a client. If the amount paid is less than the FSCS compensation limit, then the client can make a claim on the FSCS for compensation for the balance in line with the FSCS compensation rules. The FSCS can also try to arrange (or help with) a transfer of some of the business to other providers, if this is cost effective and practical. Page 7 of 11 Who can claim? The table below provides a summary of who can make a claim. Overseas financial services institutions and large companies can’t make claims. Investor type Qualifying criteria Private individuals Only a natural or legal person as outlined by the Interpretation Act 1978 qualifies for FSCS protection. Companies Only smaller companies qualify for making a claim to the FSCS. A smaller company must meet two of the following criteria (as set out in section 247 of the Companies Act 1985 or section 382 of the Companies Act 2006 as applicable): • Turnover: not more than £6.5 million. • Balance sheet total: not more than £3.26 million. • Total number of employees: not more than 50. Mutual or unincorporated Only mutual associations or unincorporated associations with net assets of less than £1.4 million (or its equivalent in any other association currency at the relevant time) can qualify for FSCS protection. Charities Charities can be set up as limited companies, or mutual or unincorporated associations. In each case the qualification criteria for FSCS protection is the same as for companies and mutual or unincorporated associations. Trusts Trustees of estate planning type trusts qualify for FSCS protection, as long as they’re based in the UK. Full details of who’s eligible to benefit from the FSCS protection can be found in the FCA’s compensation rules. Page 8 of 11 FSCS limits The Aegon SIPP and One Retirement The Aegon SIPP and One Retirement account can hold many different types of assets. Whether the FSCS gets involved in claims depends on the investments held, and who’s actually in default. The Aegon SIPP and One Retirement account are insurance contracts and can be protected up to 100% of the claim without limit if the client is invested in in-house insured funds. If the client is invested in non-insured investments the level of protection provided may vary depending on the underlying investment type. If a mis-selling claim is involved then it’s dealt with as advice relating to investment, and is subject to the investment limit of £50,000. Insured funds External fund links Aegon’s insured funds are either in-house funds managed by Scottish Equitable plc or EFLs offered by a selection of UK fund managers. For an EFL, it could be possible for either Scottish Equitable plc or the EFL provider to be in default. If Scottish Equitable plc defaulted, the assets of the EFL would still be classed as an asset of the Aegon SIPP or One Retirement account and so would be protected from liquidators. In-house funds If Scottish Equitable plc defaulted, in-house insured fund holdings would still be classed as an asset of the Aegon SIPP or One Retirement account, and would be protected from liquidators. If Scottish Equitable plc was in default, an insolvency practitioner wouldn’t view them as belonging to Scottish Equitable plc because an independent custodian holds the assets of the insured funds separately from Scottish Equitable plc’s assets. Instead, they would be viewed as assets of Aegon SIPP Nominee who holds them for APT (the trustee of the pension scheme), so would be protected. However a new fund manager may have to be found to manage the funds. For an EFL, the assets are held separately from the fund manager’s own assets. The FCA requires a fund manager to appoint a depositary (who is responsible for keeping assets of an investment fund secure). The depositary must appoint a custodian to act on their behalf. As a result, the assets are held separately from the EFL manager’s own assets in case they become insolvent. If the assets are misappropriated (for example in cases of fraud where the assets are stolen) this would result in Scottish Equitable plc being barred from claiming under the FSCS due to the FCA’s large company rules. In this situation Scottish Equitable plc would be able to bring a claim against the firm and its administrators in an attempt to recover the value of the lost assets. This would be in line with its legal agreement with the firm in default when the external fund link was first established. There’s no guarantee we would recover all or any of the value of the lost assets. Page 9 of 11 Self-invested assets Equities If the provider of a self-invested asset became insolvent Scottish Equitable plc, as the scheme administrator, will make a claim against the liquidator of the provider and on any compensation scheme. The compensation for equities depends on the shares held. Unless the shares were Aegon shares, their value wouldn’t be affected by Aegon becoming insolvent. Aegon SIPP Nominee Limited hold the assets of a SIPP separate from the Aegon business. So, in the event of Aegon being declared insolvent, the nominee will still hold any shares as a SIPP asset. Their value wouldn’t be affected and SIPP assets wouldn’t be paid to any liquidator. If the underlying provider is subject to the FSCS, then a claim could be made. If the provider isn’t based in the UK (the Channel Islands and the Isle of Man are classed as not being in the UK), then any compensation scheme will be a local one and not the FSCS. If the underlying investment falls within the FSCS investment sub-scheme (for example, an OEIC or unit trust) and the provider of that investment becomes insolvent, protection is limited to a maximum of £50,000. This protection is per investor. However, the FCA requires a fund manager to appoint a depositary who’s responsible for keeping the assets of an investment fund secure. The depositary then appoints a custodian to act on their behalf. This arrangement means that the assets would be held separately from the fund manager’s own assets, offering a strong level of protection in the event of the fund manager’s insolvency. Institutional collectives Investments made in institutional collectives wouldn’t qualify for any compensation from the FSCS, as the assets belong to Aegon SIPP Nominee Limited. If a fund or asset manager becomes insolvent, Aegon SIPP Nominee Limited would be barred from claiming under the FSCS under the FCA’s large company rules. Discretionary fund management It’s the actual investment that dictates if cover is available through the FSCS, rather than whether the services of a discretionary fund manager (DFM) have been used. A DFM should be clear about the compensation that the individual could receive before making an investment. In the event of a DFM’s default, the investments would still be held by APT or AISL and so would be protected depending on the type of investment. Trustee Investment Plan A Trustee Investment Plan falls under the insurance contract definition (pensions), so is protected to the level of 100% of the value of the whole claim, without limit. Workplace SIPP For a group pension scheme under ARC, each member’s benefit would be treated separately on its own merits. A claim would be made in respect of each member and not as a single scheme. Deposits The money held in your client’s cash facility is a deposit. In the event that the deposit taker is unable to meet its obligations the maximum compensation limit is £85,000 (gross). This limit applies per eligible claimant per authorised firm. The FSCS would aggregate all monies of that individual in assessing any compensation due, including any other private savings held with the deposit taker. Any outstanding loan amounts, such as commercial properties, held by the deposit taker will be excluded from the claim process and won’t be used to offset the claim limit. Page 10 of 11 ISA and GIA ARC’s ISA and GIA are managed by AISL. As part of this arrangement these assets are ring fenced and held in the name of a nominee company mentioned above to help protect clients assets. This means that these assets aren’t available for the defaulting firm’s creditors to settle outstanding debts. However in the event that a default occurs and the FSCS is required to support claims the limits described below apply. Deposits The money held in your client’s cash facility and your Cash ISA is a deposit. In the event that the deposit taker is unable to meet its obligations the maximum compensation limit is £85,000 (gross). This limit applies per eligible claimant, per authorised firm. The FSCS would aggregate all monies of that individual in assessing any compensation due, including any other private savings held with the deposit taker. Any outstanding loan amounts, such as commercial properties, held by the deposit taker will be excluded from the claim process and won’t be used to offset the claim limit. Retail collectives For investment claims the FSCS can pay up to a maximum £50,000 per person, per firm. Institutional collectives Investments made in institutional collectives wouldn’t qualify for any compensation from the FSCS as the assets belong to AISL. If a fund or asset manager becomes insolvent, AISL would be barred from claiming under the FSCS under the FCA’s large company rules meaning these assets have no protection or recourse available to the individual investor. Equities The situation for equities depends on the shares held. Unless the shares were Aegon shares, their value would not be affected by Aegon becoming insolvent. AISL ring fences all these investments from the Aegon business. So, in the event of Aegon being declared insolvent, AISL as the nominee will still hold any shares, and their value would be unaffected. If the company whose shares are held in the ISA and/or GIA defaults or the share price loses value, it affects the value of the shares. There wouldn’t be any compensation in this case from the FSCS. Page 11 of 11 International bonds This section relates to international bonds sold through Aegon Ireland plc. Aegon Ireland plc Aegon Ireland plc is authorised by the Central Bank of Ireland and regulated by the FCA for the conduct of UK business. As Aegon Ireland is based in Ireland it complies with the European Life Directives. What protection do clients get from the FSCS? If Aegon Ireland (as an insurer in the European Economic Area) became unable to meet its liabilities, a policyholder who was habitually a UK resident when the contract started will be covered by the provisions of the Financial Services Compensation Scheme (FSCS). Insurance business of this type is generally covered for 100% of the value of the whole claim, without limit. Trustees Under the FCA rules, trustees of estate planning type trusts are covered by the FSCS if they are UK based. Trustees of pension and retirement funds are eligible to make a claim on a long-term insurance contract if they’re: • a trustee of a personal pension or stakeholder scheme (which isn’t an occupational pension scheme); or • a trustee of a small self-administered scheme or an occupational scheme of an employer. Secure retirement income It’s important to know that any guarantee is based on the ability of the issuing insurance company – in this case Scottish Equitable plc – to pay it. If, for example, that company no longer existed, then the guarantee(s) would be affected. If we become unable to meet our liabilities and if you’re habitually a UK resident when the contract started you’ll be covered by the provisions of the Financial Services Compensation Scheme (FSCS). Insurance business of this type is generally covered for 100% of the value of the whole claim, without limit. To find out more about ARC and One Retirement, please speak to your usual Aegon representative. We’re proud to be the Lead Partner of British Tennis. For Financial Advisers Only. Aegon is a brand name of Scottish Equitable plc (No. SC144517) and Aegon Investment Solutions Ltd (No. SC394519) registered in Scotland, registered office: Edinburgh Park, Edinburgh, EH12 9SE. Both are Aegon companies. Scottish Equitable plc is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. Aegon Investment Solutions Ltd is authorised and regulated by the Financial Conduct Authority. Their Financial Services Register numbers are 165548 and 543123 respectively. © 2015 Aegon UK plc C 290935 ARC 270403 12/15