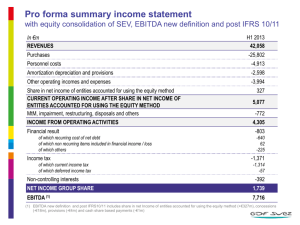

Placing EBITDA into Perspective

advertisement