ICDS on Leases: Income Computation & Disclosure Standards

advertisement

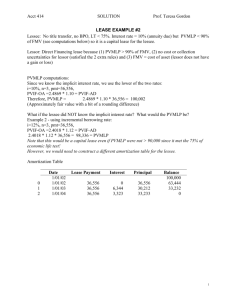

Income Computation and Disclosure Standards (ICDS) on Leases Nidhi Bothra Executive Vice President Vinod Kothari Consultants Pvt Ltd. 1006 – 1009, Krishna 224 AJC Bose Road Kolkata – 700017 Phone 033-22811276/ 22813742/7715 E-mail – corplaw@vinodkothari.com 601-C, Neelkanth, 98 Marine Drive, Mumbai 400002 Phone 022-22817427 E-mail: bombay@vinodkothari.com www.vinodkothari.com Email: nidhi@vinodkothari.com Copyright • The presentation is a property of Vinod Kothari Consultants Pvt. Ltd. No part of it can be copied, reproduced or distributed in any manner, without explicit prior permission. • In case of linking, please do give credit and full link Income Computation and Disclosure Standards(ICDS) Introduction Section 145 of the Income Tax Act, 1961 (I.T. Act) provides that the Central government (CG) may notify in the official Gazette, ICDS to be followed by any class of tax payers or in respect of any class of income. Aligned to the above provision, CG constituted a committee in December 2010 to suggest accounting standards for tax compliance under income tax laws. The Committee recommended 18 standards for harmonizing the Accounting standards issued by the Institute of Chartered Accountants of India (ICAI AS) with the tax laws and released a draft of 14 standards , which were released for public comments in Oct, 2012. Finally the Central Board of Direct taxes (CBDT) released revised draft of 12 ICDS for comments from public and various stakeholders , to be submitted by 8th February, 2015. According to the Ministry, ICDS is applicable for computation of income chargeable under the head 'profits and gains of business or profession' or 'income from other sources' and not for the purpose of maintenance of books of accounts. The 12 Income Computation Disclosure Standards released by CBDT and the corresponding Accounting Standards issued by ICAI are : Accounting Policies (ICAI AS 1) Valuation of Inventories(ICAI AS 2) Construction Contracts(ICAI AS 7) Revenue Recognition (ICAI AS 9) Tangible Fixed Assets (ICAI AS 10) The Effects of Changes in Foreign Exchange Rates (ICAI AS 11) Government Grants (ICAI AS 12) Securities (ICAI AS 13) Borrowing Costs (ICAI AS 16) Leases (ICAI AS 19) Intangible Assets (ICAI AS 26) Provisions, Contingent Liabilities and Contingent Assets (ICAI AS 29) Overview of Leases The lessor grants the lessee the right to use the asset in exchange for a series of lease payments. Leasing refers to an arrangement wherein lessor intends to lease out an asset to lessee for a certain period of time in exchange for lease rentals. Lease transactions are governed by Accounting Standard 19 (accounting for leases) as issued by the ICAI. AS 19 provides classification of leases either as an operating lease (i.e. a lease in which the risk and reward are not transferred to the lessee) or as a financial lease. Accounting treatment under AS 19 Operating Lease In the books of Lessor Assets given shall be recorded in balance sheet as Fixed Asset Depreciation on the asset shall be recognized in the profit and loss account In the books of Lessee Lease rentals receivable during lease period shall be recognized in profit and loss on a Lease rentals receivable during lease period shall be recognized in profit and loss on a straight line basis straight line basis Accounting treatment under AS 19 Financial Lease In the books of Lessee In the books of Lessor Assets are recognized in the balance sheet as receivable instead of fixed asset Assets so acquired are recognized in the balance sheet as an asset and as a liability Depreciation on the leased asset will be charged to profit and loss account Lease payments required to be paid should be segregated into principle component and finance charges Taxation on Leasing – Points of dispute in AS and the I. T. Act (1/1) AS 19 provides that in financial leases, lessee shall recognize the asset in its books and claim depreciation. However, claim for depreciation under the I. T. Act is allowed only when it satisfies the dual conditions of ownership and usage of the asset. CBDT in its Circular No. 2/2001 dated 9th February 2001, has clarified that the claim for depreciation in case of lease transaction will not have any implications due to the accounting standard issued by ICAI. Further Supreme Court in the case of ICDS Ltd., has also affirmed that depreciation claim in a leasing transaction will be allowed to the lessor. Taxation on Leasing – Points of dispute in AS and the I.T. Act (1/2) ICDS harmonizes the anomaly in the dual treatment of depreciation in accountancy and taxation by incorporating features of AS 19 and clearly states the following: Leases shall be classified either as an operating lease or a financial lease by satisfying the conditions of risk and reward ; Conditions for classifying a lease as a financial lease are similar to the one provided in AS 19; Para 10 of ICDS on Leases provides that where a lease qualifies to be a financial lease, lessee shall recognize the asset in its books and hence eligible to claim depreciation on the same ICDS for Lease transactions (corresponding to ICAI AS-19) – Salient Features (1/1) ICDS provides for uniformity of definitions and requires a joint confirmation to ensure the consistency in classification of lease as operating lease or financial lease between both the lessor and lessee. Though the standard clearly provides that in case of financial leases, lessee will be entitled to claim depreciation, section 32 of the Act needs to be amended to insert any subsection or explanation to provide a reference to this standard on leasing transaction; ICDS for Lease transactions (corresponding to ICAI AS-19) – (1/2) The Committee has also recommended amendments in the income tax provisions relating to transfer, block of assets, ownership etc in line with the provisions of this ICDS provisions. ICDS states that sale and lease back transaction will be governed by the provisions of the I.T. Act, hence explanation 4A to section 43 will come into picture. Thus, in such case the cost of acquisition of the buyer/lessor shall be the written down value of the asset of seller/lessee. AS 19 provides a different treatment to the same.