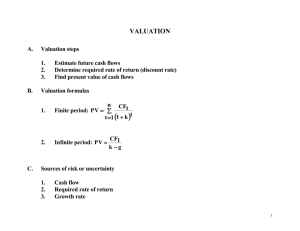

12 The Capital Budgeting Decision

advertisement