Economic

Bulletin

2015

Quarterly Economic Publication

The Economic Bulletin 2015 is published by Italchamber- Finland within

the activities of the General Secretariat of Italchamber Finland.

Pierre Collura

Head of the Editorial Board

SUOMALAIS-ITALIALAINEN KAUPPAKAMARIYHDISTYS RY

ITALCHAMBER – FINLAND

Copyright © 2015

By Italchamber Finland

All rights reserved. No part of this publication may be reproduced,

stored in a retrieval system, or transmitted, in any form or by any means,

electronic, mechanical, photocopying, or otherwise without the prior

consent of Italchamber Finland.

The Economic Bulletin is available at:

www.italchamber.fi

© ITALCHAMBER Finland

2

Table of Contents

Foreword ............................................................................................................................................................4

Best Wishes to President Mattarella ............................................................................................................5

EconomicSnapshot: Finland ............................................................................................................................6

Gross Domestic Product ...........................................................................................................................7

Inflation Rate .................................................................................................................................................8

Unemployment Rate ....................................................................................................................................9

Balance of Trade........................................................................................................................................ 10

EconomicSnapshot: Italy ............................................................................................................................... 11

Gross Domestic Product ........................................................................................................................ 12

Inflation Rate .............................................................................................................................................. 13

Unemployment Rate ................................................................................................................................. 14

Balance of Trade........................................................................................................................................ 15

Editorial ............................................................................................................................................................ 16

FINLAND 2015 ECONOMIC OUTLOOK ........................................................................................ 16

Tables ...................................................................................................................................................... 18

Featured Articles ........................................................................................................................................... 20

Single Supervisory Meachanism .............................................................................................................. 20

The function ........................................................................................................................................... 20

The membership ................................................................................................................................... 21

Sources: .................................................................................................................................................... 21

ITALY ECONOMIC OUTLOOK 2015 ............................................................................................... 22

Sources.................................................................................................................................................... 23

Fiera Milano: EventCalendar........................................................................................................................ 24

Fiera Milano: EventCalendar........................................................................................................................ 25

© ITALCHAMBER Finland

3

Foreword

I am delighted to present this second edition of the Economic Bulletin, edited by ItalchamberFinland.

The Economic Bulletin is a valuable instrument to monitor the main events concerning Finnish

and Italian business, financial and economic situation, providing some useful insights for an

introductory analysis.

Furthermore, the Economic Bulletin is also a visible sign of the increased commitment of

Italchamber-Finland to play a decisive role incontributing and providing support to the FinnishItalian commercial developments and deliver result to its business community. Among the

waste number of activities and initiatives recently played, I shall mention the recent creation of

an Italian stand at the Nordic Travel Fair (Matka). For the first time after several years,

Italchamber’s contribution has permitted an Italian participation to such commercial fair. Thanks

to Italchamber-Finland’s action, Expo Milan 2015 has joined the above fair as official exposer.

The above facts represent an objective evidence of the commitment of Italchamber-Finland’s

team to provide added-value.

I am sincerely thankful to the Editorial Board of Italchamberfor the valuable work done.

With kindest personal regards,

Avv. Dario Alessi

President of Italchamber-Finland

© ITALCHAMBER Finland

4

Best Wishes to President Mattarella

Da parte di Italchamber Finland auguri al di successo al Presidente Mattarella, che possa rappresentare

il momento della crescita economica e morale di un popolo unito dentro e fuori dall’Italia.

From Italchamber Finland we wish success to President Mattarella, may he represent the time of

economic and moral growth of a united nation within and outside of Italy.

© ITALCHAMBER Finland

5

EconomicSnapshot:

Finland

© ITALCHAMBER Finland

6

Gross Domestic Product

The volume of Finland’s gross domestic product increased in April to June by 0.2 per cent from

the previous quarter. Compared with the second quarter of 2013, GDP adjusted for working

days contracted by 0.1 per cent. The second quarter had one fewer working day than one year

previously.

In the third quarter, the volume of exports grew by 2.2 per cent from the previous quarter and

by 0.9 per cent year-on-year. Imports increased by 2.4 per cent from the previous quarter and

by 3 per cent year-on-year.

In the third quarter, the volume of private consumption went down by 0.3 per cent from the

previous quarter and by 0.2 per cent from twelve months back. Gross fixed capital formation,

or investments, grew by 0.5 per cent from the previous quarter but fell by 3.5 per cent yearon-year.

SOURCE: http://tilastokeskus.fi/til/ntp/2014/03/ntp_2014_03_2014-12-05_tie_001_en.html

© ITALCHAMBER Finland

7

Inflation Rate

The year-on-year change in consumer prices calculated by Statistics Finland was 0.5 per cent in

December. In November, it stood at 1.0 per cent. The inflation slowed down particularly

because prices of petrol and light fuel oil went down. In 2014, the average inflation rate was 1.0

per cent

In December, consumer prices were pushed up most from the previous year by risen rents,

increases in the retail prices of tobacco products, and price increases in maintenance services of

blocks of flats. The rising of consumer prices was curbed most in December by fallen prices of

liquid fuels, entertainment electronics and used cars from the year before. From November to

December, consumer prices fell by 0.1 per cent, primarily due to decreases in the prices of

liquid fuels.

SOURCE: http://tilastokeskus.fi/til/khi/2014/12/khi_2014_12_2015-01-14_tie_001_en.html

© ITALCHAMBER Finland

8

Unemployment Rate

According to Statistics Finland’s Labour Force Survey, the number of unemployed persons in

November 2014 was 215,000, which was 6,000 higher than one year ago. The unemployment

rate was 8.2 per cent, having been 7.9 per cent in November of the year before. There were

9,000 fewer employed persons than in November of the previous year. The number of persons

in disguised unemployment in the inactive population was 12,000 higher than one year earlier.

In November 2014, the number of employed persons was 2,422,000, which was 9,000 lower

than a year earlier (margin of error ±33,000). The number of employed persons decreased in

the private sector and grew in the local government sector compared with November 2013.

In November 2014, the employment rate, that is, the proportion of the employed among

persons aged 15 to 64, stood at 67.3 per cent, having been 67.8 per cent one year earlier.

Men’s employment rate was 68.0 per cent and women’s 66.6 per cent. Adjusted for seasonal

and random variation, the trend of the employment rate was 68.2 per cent.

SOURCE: http://tilastokeskus.fi/til/tyti/2014/11/tyti_2014_11_2014-12-23_tie_001_en.html

© ITALCHAMBER Finland

9

Balance of Trade

The value of Finnish exports decreased by six per cent and the value of imports decreased by

one per cent in November compared with the year before. The value of Finnish exports in

November was almost 4.5 billion euros and the value of imports was almost 4.6 billion euros.

The trade balance showed a deficit of 115 million euros in November. Calculated from January

to November there was a deficit of 1.7 billion euros. Under the same period in the year 2013,

the balance of trade showed a deficit of over 1.8 billion euros. In 2013 the trade balance for

November had a surplus of 121 million euros.

Exports to EU member states decreased by six per cent in November while exports to non-EU

countries also decreased by six per cent. Imports from EU-countries decreased by three per

cent while imports from non-EU countries increased by two per cent. Calculated from the

beginning of the year, exports to EU increased by four per cent, but decreased to non-EU

countries by seven. During the same period imports from EU member states rose by two per

cent, but from other countries imports fell by four per cent.

SOURCE:

http://www.tulli.fi/en/releases/ulkomaankauppatilastot/tilastot/ennakko/201411/index.html?bc=5

555

© ITALCHAMBER Finland

10

EconomicSnapshot:

Italy

© ITALCHAMBER Finland

11

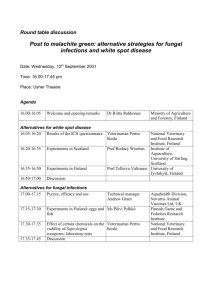

Gross Domestic Product

388000

387500

387000

386500

386000

385500

385000

384500

384000

383500

2013 I

II

III

IV

2014 I

II

III

In the third quarter of 2014 the seasonally and calendar adjusted, chained volume measure of

Gross Domestic Product (GDP) decreased by 0.1 per cent with respect to the second quarter

of 2014 and by 0.5 per cent in comparison with the third quarter of 2013.

Compared to the second quarter of 2014, final consumption expenditure remained stationary,

gross fixed capital formation decreased by 1.0 per cent and imports by 0.3 per cent, while

exports increased by 0.2.

With respect to the third quarter of 2013, final consumption expenditure increased by 0.4 per

cent and exports by 1.3 per cent, while gross fixed capital formation decreased by 3.1 per cent

and imports by 0.7 per cent.

SOURCE: http://www.istat.it/en/archive/140558

© ITALCHAMBER Finland

12

Inflation Rate

108,0

107,8

107,6

107,4

107,2

107,0

106,8

Index b=100

106,6

106,4

106,2

January

February

March

April

May

June

July

August

September

October

November

December

January

February

March

April

May

June

July

August

September

October

November

December

106,0

2013

2014

In November 2014, the Italian consumer price index for the whole nation (NIC) declined by

0.2% compared with the previous month and rose by 0.2% with respect to November 2013

(0.1 higher than in October 2014). The flash estimate was confirmed.

The inflation registered a speed-up which was mainly due to the reversal of trend of

Unprocessed food prices (+0.8%, from -0.2% in October 2014); to a lesser extent,

contributions derived from other product typologies. This dynamics was partially offset by the

widening of the annual decrease of prices of Non-regulated energy products (-3.1%, from -2.2%

in the previous month).

Excluding unprocessed food and energy, core inflation was stable at 0.5% whereas, excluding

energy, the inflation was 0.6%, up from 0.4% in October 2014.

The annual rate of change of prices of Goods was -0.4% (from -0.3% observed in October

2014) and the annual rate of change of prices of Services was 0.9%, up from 0.7% registered in

the previous month. As a consequence, the inflationary gap between Services and Goods

increased by 0.3 percentage points with respect to October 2014.

Core inflation measured by Italian HICP was stable at 0.5% and the inflation calculated excluding

energy, food, alcohol and tobacco was stable at 0.6%. Excluding energy, the inflation rose to

0.6% (from 0.4% in the previous month) instead.

SOURCE: http://www.istat.it/en/archive/145134

© ITALCHAMBER Finland

13

Unemployment Rate

13,6

13,4

13,2

13

12,8

12,6

12,4

12,2

2013

November

October

September

August

July

June

May

April

March

February

January

December

November

12

2014

In November 2014 22.310 million persons were employed, -0.2% compared with October

2014. Unemployed were 3.457 million, +1.2% with respect to the previous month.

Employment rate was 55.5%, -0.1 percentage points with respect to October 2014,

unemployment rate was 13.4%, +0.2 percentage points over the previous month, and inactivity

rate was 35.7%, unchanged over October.

Youth unemployment rate (aged 15-24) was 43.9%, +0.6 percentage points in a month, youth

unemployment ratio in the same age group was 12.2%, +0.3 percentage points over the

previous month.

SOURCE: http://www.istat.it/en/archive/144199

© ITALCHAMBER Finland

14

Balance of Trade

40000,00

38000,00

36000,00

34000,00

32000,00

30000,00

28000,00

Exports (€ mil)

Imports (€ mil)

26000,00

24000,00

22000,00

20000,00

Istat presents data on Italy's foreign trade as well as unit value and volume indices (base year

2010=100) referring to October 2014.

In October 2014 seasonally-adjusted data, compared to September, increased by 0.4% for

outgoing flows and decreased by 0.9% for incoming flows. The growth in exports is the

synthesis of an increase for EU countries (+1.8%) and a decrease for non EU countries (-1.2%).

Imports decreased for EU countries (-0.7%) and non EU countries (-1.1%). Over the last three

months, seasonally-adjusted data, in comparison with the previous three months, increased by

1.2 for exports and decreased by 0.4% for imports.

In October 2014, compared with the same month of the previous year, trade increased by 2.9%

for exports (+4.7% for EU area and +0.8% for non EU countries) and decreased by 1.6% for

imports (+3.1% for EU and -7.7% for non EU countries). The trade balance in October

amounted to +5.4 billion Euro (+1.4 billion Euro for EU area and +4.0 billion Euro for non EU

countries)

© ITALCHAMBER Finland

15

Editorial

FINLAND 2015 ECONOMIC OUTLOOK

By Gianfranco Nitti

Winter is upon us, and most of us need an extra dose of vitamins. Metaphorically speaking, this

is also the case for large parts of the world economy where the economic performance has

again made the bank Nordea revise down the expectations in their fresh economic forecasts.

One such dose of vitamins could be the recent dramatic and unexpectedly sharp oil price

decline which could become a crucial catalyst for growth in the world economy, which we

expect to gain strength in coming years.

“Given the relatively weak international trends, growth conditions have been tough for the

Nordic countries, which are all quite reliant on foreign trade. Nonetheless, both Sweden and

Norway have delivered relatively decent growth rates, not least driven by a strong upturn in

domestic demand while Denmark and Finland have been the laggards in the Nordic growth

race. This will not change in the years ahead where we expect overall growth in the Nordic

region to rise from 1.4% this year to 1,9% in 2016”, says Helge J. Pedersen, Nordea’s Global

Chief Economist.

Finland is still stuck in recession. The slowdown in Russia hits the Finnish economy harder

than the other Nordic countries, and in light of the serious structural problems that Finland is

also struggling with, Nordea sees a risk of new growth disappointments.

From OECD

According to OECD forecasts, output is set to contract for the third year in a row in 2014.

Rising unemployment and mounting uncertainties are undermining business and consumer

confidence.

Fiscal tightening is also weighing on economic activity. The upturn in both domestic and foreign

demand is projected to be slow, as subdued income growth holds back consumption, global

growth remains sluggish and ample spare capacity delays a pick-up in investment.

© ITALCHAMBER Finland

16

The implementation of the government’s structural reform programme to increase labour force

participation and public sector efficiency is critical to ensuring fiscal sustainability over the

longer term, as age-related spending increases.

According to ETLA, Research Institute of the Finnish Economy, the euro area recovery is slow

and Finland’s GDP will grow by 0.8 per cent in 2015. Here’s its summary:

The world economy will grow slowly in the near future

Rapid growth in emerging economies is subsidizing, the US is the main engine of world growth

The euro area is recovering slowly, the Russian economy is falling into a slump and the

Ukrainian crisis is creating uncertainty

Finland's GDP will contract by 0.4 per cent in 2014 and grow by 0.8 per cent in 2015

The volume of exports is expected to grow by a couple of per cent in 2015

Private consumption will start to grow in 2015 by a half per cent fuelled by an upturn in

consumer confidence and employment

Private investment will start to increase by a couple of per cent in 2015 in the wake of a

recovery in demand

The unemployment rate rose to 8.7 per cent in 2014 and remains at that level also in 2015

The general government deficit relative to GDP will remain below the three per cent ceiling, but

the debt ratio will climb above 60 per cent

President of the European Central Bank Mario Draghi visited Finland at the end of November

2014 and gave a speech to the Finnish Parliament and at the Helsinki University.

In his speech at the Finnish Parliament, President Draghi highlighted that, over the past crisis

years, the ECB has acted forcefully to safeguard price stability and to contribute to financial

stability in the euro area as a whole. In particular, the ECB has taken several non-standard

measures to ensure the transmission of its monetary policy to the economy. The latest

unconventional measures announced by the ECB (the targeted long term refinancing operations

(TLTROs), and the covered bond and ABS purchase programmes) will have a sizeable impact

© ITALCHAMBER Finland

17

on our balance sheet, which we expect to move towards its early 2012 dimension. This will

ensure the necessary degree of monetary accommodation and contribute to a gradual recovery

and a return of inflation to levels closer to below, but close to, 2%. If, however, it becomes

necessary to further address risks of too prolonged a period of low inflation, the Governing

Council is unanimous in its commitment to using additional unconventional instruments within

its mandate.

Accountability and transparency are the essential elements balancing the independence of a

central bank, especially in times where unconventional measures are being taken. The ECB

regularly publishes a variety of data on the execution of monetary policy operations and the

liquidity conditions of the Eurosystem. (i.e. the SMP, the Covered Bonds Programmes and the

ABS Purchase Programme portfolios). Additionally, the Governing Council committed to the

publication of an account of monetary policy discussions.

As regards fiscal policy and structural reforms, while the Stability and Growth Pact should

remain the anchor for confidence in sustainable public finances, a comprehensive strategy is

needed to put the euro area economy back on track. This involves further sharing of

sovereignty, i.e a leap forward from common rules to common institutions. The upcoming

report commissioned by the Euro Summit on the future of economic governance will present a

good starting point for further reflection.

Tables

Source, OECD, Nordea

© ITALCHAMBER Finland

18

Key forecast Finland

2011

2012*

2013*

2014F

2015F

2016F

Consumer priceindexchange, %

3.4

2.8

1.5

1.1

1.3

1.6

Wagelevelchange, %

2.7

3.3

2.4

1.3

1.1

1.7

Unemployment rate, %

7.8

7.7

8.2

8.7

8.7

8.5

Current account surplus, % of GDP

-1.5

-1.9

-2.0

-1.3

-1.6

-1.6

Industrial output change, %

3.2

-2.8

-3.0

-0.9

2.3

2.9

Euribor 3-month, %

1.4

0.6

0.2

0.2

0.2

1.1

EU27 countries, GDP change, %

1.6

-0.4

0.1

1.2

1.5

1.7

- EMU-countries

1.5

-0.7

-0.4

0.9

1.3

1.5

EU27 countries, change in CPI, %

3.1

2.6

1.5

0.5

1.1

1.5

EMU-countries1)

2.7

2.5

1.4

0.5

1.1

1.5

Finland’s EMU surplus, % of GDP

-1.0

-2.1

-2.3

-2.8

-2.5

-1.7

Finland’s EMU-debt, % of GDP

48.5

52.8

56.2

60.3

62.8

64.2

* preliminary

1) Harmonized index

Source: Statistics Finland, ETLA

© ITALCHAMBER Finland

19

Featured Articles

Single Supervisory Meachanism

The purpose of the Single Supervisory Mechanism (SSM) is to bestow upon the European

Central Bank (ECB) the powers to monitor the financial stability of banks located in

participating states, starting from the 4th November 2014. This mechanism is part of the efforts

directed to the strengthening of the Economic and Monetary Union (EMU). The proposal of a

Council Regulation establishing the SSM was developed by the European Commission during

the summer of 2012, and subsequently published on the 12th September 2012.

The Single Supervisory board consists of 23 members: 17 representatives of bank supervisors

of member states, plus one chairman, one vice-chairman and four ECB representatives. The

decisional process is designed so that the supervisory board drafts supervisory a decision, and

subsequently the formal one is to be taken by the Governing Council, the ECB’s ultimate

decision-making body.

The function

This monitoring regime is enacted by conducting stress tests on financial institutions and, in the

case the test identifies problems, the ECB has the power to intervene in order to rectify the

situation. The purpose of the stress test is to determine whether a credit institution has enough

capital to withstand the impact of adverse developments, such as a financial crisis. The stress

© ITALCHAMBER Finland

20

testused in the SSM was designed by the European Systemic Risk Board, in cooperation with

the National Authorities, the European Banking Authority (EBA) and the ECB. According to the

parameters of the test, banks are required to maintain a CET1 ratio of 8% under the baseline

scenario, while a minimum of a CET1 ratio of 5,5% under adverse scenario.

On the 26th October 2014, the ECB has published the first comprehensive supervision review,

which covered 130 of the most significant credit institutions of the Eurozone states. The

supervision report included: the results of an Asset Quality Review (AQR) and the assessment

of potential capital short falls under the baseline scenario and the adverse scenario.

The membership

Not all members of the EU will participate in the Single Supervisory Mechanism. The EU

Treatise bestows upon the ECB jurisdiction only over the Eurozone, hence it cannot enforce

measures in a non-Eurozone state. Therefore the participation is automatic for Eurozone

states, while non-Eurozone EU Members can enter a close cooperation agreement with the

ECB. As of the 3rd November 2014, no request to enter the close cooperation agreement has

been notified in line with the procedure ECB/2014/510. However, the ECB has received

informal expression of interest from a number of non-Eurozone EU Member states.

Sources:

http://ec.europa.eu/economy_finance/euro/emu/index_en.htm

http://ec.europa.eu/finance/general-policy/banking-union/single-supervisorymechanism/index_en.htm

http://europa.eu/rapid/press-release_IP-12-953_en.htm

http://europa.eu/rapid/press-release_MEMO-13-780_en.htm?locale=en

http://www.economonitor.com/blog/2012/09/first-the-governance-then-the-guarantees/

http://www.investopedia.com/terms/b/bank-stress-test.asp

https://www.bankingsupervision.europa.eu/home/html/index.en.html

https://www.ecb.europa.eu/ecb/history/emu/html/index.en.html

https://www.ecb.europa.eu/press/pr/date/2014/html/pr141026.en.html

© ITALCHAMBER Finland

21

ITALY ECONOMIC OUTLOOK 2015

According to the forecast published by the OECD in November 2014, Italy’s economy, after

the contraction occurred for most of 2014, is projected to regain its growth by mid-2015 and

advance further in 2016. The monetary policy support of the European Central Bank’s (ECB)is

expected to ameliorate financial conditions and improve a renewal of bank lending, which

should raise investment. The estimatedrecovery of Italy’s export market will also support a

stronger growth. Furthermore, fiscal policy will have a small impact 2015 from the overall

perspective, as tax reductionswill be offset by spending cuts. Moreover, the unemployment rate

will start to drop in 2016, but is forecasted to maintain its high levels, while wage gains look set

to remain modest.

In an attempt to support economic growth, the government has delayed fiscal consolidation and

has completed some steps in its comprehensive programme of structural reforms. The

extremely high public debt ratio poses a significant vulnerability, and as growth improves higher

tax revenues should be channeled entirely to deficit reduction.

According to Reuters, Italy is preparing to cut its economic outlook for 2015 and raise its

targets for the budget deficit. Furthermore, the economy will contract by 0.2 percent or 0.3

percent this year, compared with the current official forecast made in April for it to expand 0.8

percent. The target for the budget deficit, calculated as a percentage of gross domestic product

(GDP), will be raisedof 0.2 percent, from 2.6 to 2.8 percent, remaining at the same level as last

year and inside the European Union's 3 percent ceiling, the source said.

© ITALCHAMBER Finland

22

According both to the aforementioned release of the OECD and the Italian employers'

association Confindustria the forecast for eurozone's third largest economy will contract by 0.4

percent in 2015. Moreover, the revisions of the Treasury to its outlook will be much sharper expected GDP growth drops to around 0.5 percent from 1.3 percent.

In accordance with the relaxation of its fiscal stance, the Italian government is hoping to

postpone its commitment to achieve the goals for a balanced budget in structural terms adjusted for the business cycle and one-off factors - to 2016 from 2015.

The coalition of Matteo Renzi's government got some breathing space in regards of the public

finances when ISTAT – the national statistics bureau – revised up the level of GDP due to

methodological changes.

On the 16th January 2015, according to the Bank of Italy economic bulletin the forecast for

Italy's gross domestic product (GDP) growthfor the year2015got slashed to just 0.4% from an

earlier prediction of 1.3% while the budget measures which helped avoid an even deeper

recession got some praise. In its quarterly outlook, the central bank estimated that the

economy in 2014 lost 0.4% compared to one year earlier, and suggested matters could have

been considerably worse if not due to the budget measures that included programs to aimed to

stimulate growth which helped the country to avoid a prolonged recession.

Besides the cut to the economy’s growth outlook for 2015 from its July forecast, the Bank of

Italy stated that it expects in 2016 the economy should improve by 1.2%.However, for the

present moment, "considerable uncertainty remains" and a restart of business investments must

be encouraged if growth is to be achieved.

"The intensity of the recovery in investments will be crucial," the Bank of Italy stated. The

forecast is similar to others made recently.In late December, the Prime Minister Matteo Renzi

forecasted that GDP would likely average -0.4% in 2014 but added he was confident there

would be a turnaround in the year ahead.

In the aforementioned report, based on a continued sluggishness throughout this year, the

central bank warned that deflation will be a persistent problem –an issue that can be identified

also across the eurozone.

Sources

http://www.ansa.it/english/news/2015/01/16/bank-of-italy-slashes-2015-gdp-forecast-praisesgovt_b05d68f2-afa0-4beb-a193-ef7a9a6573a4.html

http://www.bancaditalia.it/pubblicazioni/bollettino-economico/2015-1/boleco_1_2015.pdf

http://www.oecd.org/eco/outlook/italy-economic-forecast-summary.htm

http://www.reuters.com/article/2014/09/25/italy-economy-idUSR1N0QW00A20140925

© ITALCHAMBER Finland

23

Fiera Milano: EventCalendar

FEBRUARY

Name

Schedule

MILANO UNICA

04/06 FEB 2015

Borsa Internazionale del Turismo (BIT)

12/14 FEB 2015

MIPEL - The Bagshow

15/18 FEB 2015

theMICAM

15/18 FEB 2015

MYPLANT & GARDEN

25/27 FEB 2015

SIMAC TANNING-TECH

25/27 FEB 2015

LINEAPELLE

25/27 FEB 2015

MIPAP

28 FEB - 02 MAR 2015

SUPER

28 FEB - 02 MAR 2015

MIDO

28 FEB - 02 MAR 2015

MARCH

Name

Schedule

MIFUR - International Fur and Leather Exhibition

03/06 MAR 2015

3DPrint Hub

05/07 MAR 2015

CARTOOMICS

13/15 MAR 2015

HOBBY SHOW

13/15 MAR 2015

FA' LA COSA GIUSTA!

13/15 MAR 2015

BIKE4ME

13/15 MAR 2015

MADE EXPO

18/21 MAR 2015

MILANO AUTO CLASSICA

20/22 MAR 2015

© ITALCHAMBER Finland

24

Fiera Milano: EventCalendar

FEBRUARY

Name

Schedule

Labquality Days 2015

05/06 FEB 2015

Vene 15 Båt

06/15 FEB 2015

easyFairs® Fastfood& Café &Ravintola 2015

25/26 FEB 2015

easyFairs® Myymälä& e- commerce Helsinki 2015

25/26 FEB 2015

MARCH

Name

Schedule

Fillari 2015

06/08 MAR 2015

GoExpo 2015

06/08 MAR 2015

ValtakunnallisetKuntoutuspäivät 2015

09/10 MAR 2015

Sairaanhoitajapäivät 2015

12/13 MAR 2015

ChemBio Finland 2015

18/19 MAR 2015

Kevätmessut 2015

26/29 MAR 2015

Lähiruoka&luomu 2015

26/29 MAR 2016

© ITALCHAMBER Finland

25

SUOMALAIS-ITALIALAINEN

KAUPPAKAMARIYHDISTYS RY

ITALCHAMBER – FINLAND

DARIO ALESSI

President

dario.alessi@italchamber.fi

ANNALISA FLORE

Secretary General

annalisa.flore@italchamber.fi

+358 40 4810855

MIRO DEL GAUDIO

Deputy-Secretary General

miro.delgaudio@italchamber.fi

+358 50 3527101

VITO RAVO

Public Relations

vito.ravo@italchamber.fi

+358 40 7725737

PIERRE COLLURA

Head of the Editorial Board

pierre.collura@italchamber.fi

Temppelikatu 4A

00100 Helsinki

Finland

Business ID: 1525267-3

VAT No: FI15252673

Reg. No: 84.240

Tel. +358 9 4281 7000

Fax. +358 9 494 113

Mobile +358 40 4810855

email: info@italchamber.fi

www.italchamber.fi

PETTERI VILJAKAINEN

VicePresident

petteri.viljakainen@italchamber.fi

MARKUS HAKALA

VicePresident

markus.hakala@italchamber.fi

© ITALCHAMBER Finland

26