KPMG FLASH NEWS

KPMG IN INDIA

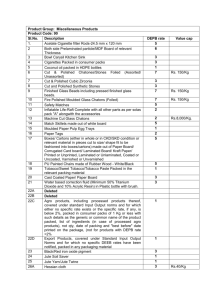

The Supreme Court rules that the face value should be reduced from the sale

value to arrive at taxable profit arising from sale of DEPB

23 February 2012

Recently, the Supreme Court of India in the case of

1

Topman Exports (the taxpayer) and other companies

held that when Duty Entitlement Passbook (DEPB) is

sold, face value should be reduced from sale value to

arrive at taxable profit arising from sale of DEPB under

Section 28(iiid) of the Income-tax Act, 1961 (the Act).

The Supreme Court also held that when the cash

assistance was received in the form of DEPB it was

taxable under Section 28(iiib) of the Act.

Facts of the case

•

The taxpayer is a manufacturer and exporter of

fabrics and garments. During the Assessment

Year 2002-2003, the taxpayer sold the DEPB and

DFRC (Duty Free Replenishment Certificate)

which had accrued on export of its products. While

filing the Return of Income, the taxpayer claimed a

deduction of INR 8.36 million under Section

80HHC of the Act.

Background

•

The Assessing Officer held that if the profit on

transfer of the export incentives was deducted

from taxpayer’s profits, the figure would be a loss

and there will be no positive income from the

export business and the taxpayer will not be

entitled to any deduction under Section 80HHC of

the Act.

•

The taxpayer was of the view that the profits on

the transfer of DEPB and DFRC were the

difference between the sale value and face value

of DEPB and DFRC and if these figures of profits

on transfer of DEPB and DFRC are taken, the

income would be positive and it would be entitled

to the deduction under Section 80HHC of the Act.

•

Under Section 28(iiib) of the Act, cash assistance

(by whatever name called) received or receivable

by any person against exports under any scheme

of the Government of India is by itself income

chargeable to income tax under the head ‘Profits

and Gains of Business or Profession’.

•

Under Section 28(iiid) of the Act, any profit on

transfer of DEPB is chargeable to income tax under

the head ‘Profits and Gains of Business or

Profession’,

___________

1

Topman Exports v. CIT (Civil Appeal no 1699 of 2012)

© 2012 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative

(“KPMG International”), a Swiss entity. All rights reserved.

Issues before the Supreme Court

•

Whether the face value of the DEPB shall be deducted

from the sale proceeds to calculate profits chargeable

under Section 28(iiid) of the Act?

•

Whether the face value of the DEPB is chargeable

under Section 28(iiib) of the Act?

•

DEPB is ‘cash assistance’ receivable by a person

against exports under the scheme of the

Government of India and falls under Section

28(iiib) of the Act. Accordingly, DEPB is

chargeable to income tax under the head ‘Profits

and Gains of Business or Profession’ even before

it is transferred by the taxpayer.

•

Under Section 28(iiid) of the Act, any profit on

transfer of DEPB is chargeable to income tax

under the head ‘Profits and Gains of Business or

Profession’ as an item separate from cash

assistance under Section 28(iiib) of the Act.

•

As DEPB has direct nexus with the cost of imports

for manufacturing an export product, any amount

realized by the taxpayer’s over and above the

DEPB on transfer of the DEPB would represent

profit on the transfer of DEPB.

•

The face value of the DEPB will fall under Section

28(iiib) of the Act, the difference between the sale

value and the face value of the DEPB will fall

under Section 28(iiid) of the Act. Accordingly, the

difference between the sale value and the face

value of the DEPB represent profit on transfer of

the DEPB.

•

The cost of acquiring DEPB is not nil because the

person acquires it by paying customs duty on the

import content of the export product and the DEPB

which accrues to a person against exports has a

cost element in it.

Taxpayer’s contentions

•

The object of granting DEPB to an exporter is to

neutralize the incidence of custom duties which has

been incurred on the import component of the export

product and this neutralization is achieved by grant of

duty credit of the amount specified in the DEPB

Scheme. Therefore there was direct relation between

the DEPB and the cost of inputs imported for

manufacture of export product.

•

If the intention of the legislature was to cover the entire

sale proceeds arising on transfer of DEPB under

Section 28(iiid) of the Act, then they would have used

the expression ‘sale proceeds’ instead of ‘profit on

transfer of DEPB’.

•

If the entire sale proceeds of the DEPB is treated as

profits arising on transfer of DEPB, then the taxpayer

will be taxed twice for the same income, once as ‘cash

assistance’ under Section 28(iiib) of the Act equivalent

to the face value of the DEPB and for the second time

as profit on transfer of DEPB under Section 28(iiid) of

the Act.

Tax department’s contentions

•

The taxpayer does not obtain any cost in obtaining the

DEPB. DEPB is an export incentive granted by the

Government under DEPB Scheme and it has no direct

relation with the cost of purchases made by the

taxpayer.

•

The taxpayer is not entitled to deduct the face value of

the DEPB from the sale proceeds for determining the

profit arising on transfer of DEPB. Accordingly, the

entire sale proceeds of the DEPB represent the profits

earned by the taxpayer on transfer of the DEPB.

Our comments

This is an important ruling by the Supreme Court

where it has held that the entire amount received on

the sale of DEPB does not represent profits

chargeable under Section 28(iiid) of Act. For

calculating profits, the sale value of the DEPB has to

be reduced by its face value.

Section 80HHC of the Act has been omitted from AY

2005-06. Accordingly, the decision of the Supreme

Court would be relevant for the pending cases.

Supreme Court ruling

•

Objective of DEPB is to neutralise the incidence of

customs duty on the import content of the export

products. Hence, it has direct nexus with the cost of the

imports made by an exporter for manufacturing the

export products. The cost of customs duty is neutralised

under the DEPB scheme, by granting a duty credit

against the export product and this credit can be utilised

for paying customs duty on any item which is freely

importable.

© 2012 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative

(“KPMG International”), a Swiss entity. All rights reserved.

www.kpmg.com/in

Ahmedabad

Safal Profitaire

B4 3rd Floor, Corporate Road,

Opp. Auda Garden, Prahlad Nagar

Ahmedabad – 380 015

Tel: +91 79 4040 2200

Fax: +91 79 4040 2244

Hyderabad

8-2-618/2

Reliance Humsafar, 4th Floor

Road No.11, Banjara Hills

Hyderabad 500 034

Tel: +91 40 3046 5000

Fax: +91 40 3046 5299

Bangalore

Maruthi Info-Tech Centre

11-12/1, Inner Ring Road

Koramangala, Bangalore 560 071

Tel: +91 80 3980 6000

Fax: +91 80 3980 6999

Kochi

4/F, Palal Towers

M. G. Road, Ravipuram,

Kochi 682 016

Tel: +91 484 302 7000

Fax: +91 484 302 7001

Chandigarh

SCO 22-23 (Ist Floor)

Sector 8C, Madhya Marg

Chandigarh 160 009

Tel: +91 172 393 5777/781

Fax: +91 172 393 5780

Chennai

No.10, Mahatma Gandhi Road

Nungambakkam

Chennai 600 034

Tel: +91 44 3914 5000

Fax: +91 44 3914 5999

Delhi

Building No.10, 8th Floor

DLF Cyber City, Phase II

Gurgaon, Haryana 122 002

Tel: +91 124 307 4000

Fax: +91 124 254 9101

Kolkata

Infinity Benchmark, Plot No. G-1

10th Floor, Block – EP & GP,

Sector V Salt Lake City,

Kolkata 700 091

Tel: +91 33 44034000

Fax: +91 33 44034199

Mumbai

Lodha Excelus, Apollo Mills

N. M. Joshi Marg

Mahalaxmi, Mumbai 400 011

Tel: +91 22 3989 6000

Fax: +91 22 3983 6000

Pune

703, Godrej Castlemaine

Bund Garden

Pune 411 001

Tel: +91 20 3050 4000

Fax: +91 20 3050 4010

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we

endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue

to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2012 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative

(“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and “cutting through complexity“ are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity.

© 2012 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative

(“KPMG International”), a Swiss entity. All rights reserved.