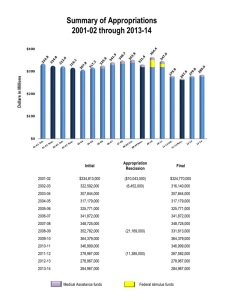

Vote Revenue - Supplementary Estimates of Appropriations 2014/15

advertisement

Vote Revenue APPROPRIATION MINISTER(S): Minister of Revenue (M57) APPROPRIATION ADMINISTRATOR: Inland Revenue Department RESPONSIBLE MINISTER FOR INLAND REVENUE DEPARTMENT: Minister of Revenue THE SUPPLEMENTARY ESTIMATES OF APPROPRIATIONS 2014/15 B.7 643 VOTE REVENUE Details of Appropriations and Capital Injections Annual and Permanent Appropriations 2014/15 Estimates Budget $000 Supplementary Estimates Budget $000 Total Budget $000 Management of Debt and Outstanding Returns (M57) Taking action where returns are outstanding and where payments are overdue, including providing people with assistance on the actions they need to take to meet their obligations. This includes collection on behalf of other agencies and external parties. 143,259 8,204 151,463 Policy Advice (M57) This appropriation is limited to the provision of advice (including second opinion advice and contributions to policy advice led by other agencies) to support decision-making by Ministers on government policy matters. 8,053 1,100 9,153 Services to Inform the Public About Entitlements and Meeting Obligations (M57) Providing information and assistance to customers on the application of the law. Responding to customer enquiries about tax and social support programmes. Adjudication on behalf of the Commissioner on proposed taxpayer assessments. Providing binding rulings and other statements on the interpretation and application of the law administered by Inland Revenue. Provision of services to Ministers to enable them to discharge their portfolio (other than policy decision-making responsibilities). 251,307 1,848 253,155 Services to Other Agencies RDA (M57) This appropriation is limited to the provision of services by Inland Revenue to other agencies, where those services are not within the scope of another departmental output expense appropriation in Vote Revenue. 3,060 - 3,060 Services to Process Obligations and Entitlements (M57) Registering tax payers, making tax assessments, assessing child support liabilities including providing a readily accessible inexpensive process for reviewing assessments, receiving and making payments to customers, processing applications and payments for social support programmes, collection of ACC Earners' levies, supplying information to other government agencies and accounting and reporting the collection of Crown revenue. 140,572 (7,065) 133,507 Taxpayer Audit (M57) Identifying risks to revenue and designing and undertaking audit activities accordingly. Managing litigation of disputed tax cases. 166,131 10,928 177,059 Total Departmental Output Expenses 712,382 15,015 727,397 Inland Revenue Department - Capital Expenditure PLA (M57) This appropriation is limited to the purchase or development of assets by and for the use of the Inland Revenue Department, as authorised by section 24(1) of the Public Finance Act 1989. 62,336 (29,336) 33,000 Total Departmental Capital Expenditure 62,336 (29,336) 33,000 267,000 (4,000) 263,000 1,300 - 1,300 Titles and Scopes of Appropriations by Appropriation Type Departmental Output Expenses Departmental Capital Expenditure Benefits or Related Expenses Child Support Payments PLA (M57) Child support payments to custodial persons who are not dependent on the state for financial support (expenses incurred pursuant to section 141 of the Child Support Act 1991). Child Tax Credit PLA (M57) Extra assistance for low to middle income families who are not dependent on the state for financial support (expenses incurred pursuant to section 185 of the Tax Administration Act 1994). 644 THE SUPPLEMENTARY ESTIMATES OF APPROPRIATIONS 2014/15 B.7 VOTE REVENUE 2014/15 Estimates Budget $000 Supplementary Estimates Budget $000 Total Budget $000 Family Tax Credit PLA (M57) Family Support payments made to beneficiaries and non-beneficiaries during the year (expenses incurred pursuant to section 185 of the Tax Administration Act 1994). 1,934,000 (77,000) 1,857,000 In-Work Tax Credit PLA (M57) Extra assistance for low to middle income families where the person works a minimum of 20 hours per week and does not have a partner, or a person and their partner work a minimum of 30 hours per week (expenses incurred pursuant to section 185 of the Tax Administration Act 1994). 494,000 18,000 512,000 13,000 - 13,000 KiwiSaver: Kickstart Payment (M57) To enable the one-off payment made on opening a KiwiSaver account for members who meet the required eligibility criteria as set in the KiwiSaver Act 2006. 171,000 60,000 231,000 KiwiSaver: Tax Credit (M57) To enable the payment of a tax credit to KiwiSaver members and the payment of residual tax credits to employers as set out in the Income Tax Act 2007. 643,000 - 643,000 13,000 3,000 16,000 Paid Parental Leave Payments (M57) This appropriation is limited to Paid Parental Leave Payments made to parents in accordance with the Parental Leave and Employment Protection Act 1987. 176,000 13,000 189,000 Parental Tax Credit PLA (M57) To enable payment of additional financial support to be made to working families for the eight week period following the birth of a child (expenses incurred pursuant to section 185 of the Tax Administration Act 1994). 19,000 2,000 21,000 4,000 100 4,100 3,735,300 15,100 3,750,400 10 10 20 Environmental Restoration Account Interest PLA (M57) This appropriation is limited to interest on Environmental Restoration accounts (expenses incurred pursuant to section 185 of the Tax Administration Act 1994). 2,000 - 2,000 Income Equalisation Interest PLA (M57) This appropriation is limited to interest on Income Equalisation Reserve Scheme accounts held by taxpayers in the farming, fishing or forestry industries (expenses incurred pursuant to section 185 of the Tax Administration Act 1994). 7,000 8,000 15,000 Total Non-Departmental Borrowing Expenses 9,010 8,010 17,020 Titles and Scopes of Appropriations by Appropriation Type KiwiSaver: Interest (M57) To enable the payment of interest on KiwiSaver contributions as set out in the KiwiSaver Act 2006. Minimum Family Tax Credit PLA (M57) Extra payment made to families where at least one parent is working for salary or wages (expenses incurred pursuant to section 185 of the Tax Administration Act 1994). Payroll Subsidy PLA (M57) This appropriation is limited to the payment of a subsidy to a payroll agent undertaking employers' payroll-related tax compliance activities on their behalf, section 185 of the Tax Administration Act 1994. Total Benefits or Related Expenses Non-Departmental Borrowing Expenses Adverse Event Interest PLA (M57) This appropriation is limited to interest on Adverse Event Income Equalisation Reserve accounts held by taxpayers in the farming and agriculture business (expenses incurred pursuant to section 185 of the Tax Administration Act 1994). THE SUPPLEMENTARY ESTIMATES OF APPROPRIATIONS 2014/15 B.7 645 VOTE REVENUE 2014/15 Estimates Budget $000 Supplementary Estimates Budget $000 Total Budget $000 1,162,098 18,258 1,180,356 Impairment of Debt Relating to Child Support (M57) This appropriation is limited to amounts relating to impairment arising from objective evidence of one or more loss events that occurred after the initial recognition of the debt, and the loss event (or events) has had a reliably measurable impact on the estimated future cash flows of the collective book of child support debt. 323,000 (71,000) 252,000 Impairment of Debt Relating to Student Loans (M57) This appropriation is limited to amounts relating to impairment arising from objective evidence of one or more loss events that occurred after the initial recognition of the loan, and the loss event (or events) has had a reliably measurable impact on the estimated future cash flows of the collective book of student loan debt. 100,000 182,000 282,000 Initial Fair Value Write-Down Relating to Student Loans (M57) This appropriation is limited to the initial fair value write-down of student loans. 668,000 (45,156) 622,844 Total Non-Departmental Other Expenses 2,253,098 84,102 2,337,200 Total Annual and Permanent Appropriations 6,772,126 92,891 6,865,017 Titles and Scopes of Appropriations by Appropriation Type Non-Departmental Other Expenses Impairment of Debt and Debt Write-Offs (M57) This appropriation is limited to bad debt write-offs for Crown debt and to amounts relating to impairment arising from objective evidence of one or more loss events that occurred after the initial recognition of the debt, and the loss event (or events) has had a reliably measurable impact on the estimated future cash flows of the Crown debt book. Capital Injection Authorisations 2014/15 Estimates Budget $000 Supplementary Estimates Budget $000 Total Budget $000 2,336 1,236 3,572 Inland Revenue Department - Capital Injection (M57) 646 THE SUPPLEMENTARY ESTIMATES OF APPROPRIATIONS 2014/15 B.7 VOTE REVENUE Supporting Information Part 1 - Vote as a Whole 1.2 - Trends in the Vote Summary of Financial Activity 2014/15 Supplementary Estimates NonDepartmental Departmental Total Estimates Transactions Transactions Transactions $000 $000 $000 $000 Total $000 Appropriations Output Expenses 712,382 15,015 - 15,015 727,397 3,735,300 N/A 15,100 15,100 3,750,400 9,010 - 8,010 8,010 17,020 2,253,098 - 84,102 84,102 2,337,200 62,336 (29,336) - (29,336) 33,000 - - N/A - - Output Expenses - - - - - Other Expenses - - - - - Capital Expenditure - N/A - - - 6,772,126 (14,321) 107,212 92,891 6,865,017 60,378,000 N/A (678,000) (678,000) 59,700,000 Non-Tax Revenue 1,533,000 N/A (173,000) (173,000) 1,360,000 Capital Receipts 1,259,000 N/A 181,500 181,500 1,440,500 63,170,000 N/A (669,500) (669,500) 62,500,500 Benefits or Related Expenses Borrowing Expenses Other Expenses Capital Expenditure Intelligence and Security Department Expenses and Capital Expenditure Multi-Category Expenses and Capital Expenditure (MCA) Total Appropriations Crown Revenue and Capital Receipts Tax Revenue Total Crown Revenue and Capital Receipts THE SUPPLEMENTARY ESTIMATES OF APPROPRIATIONS 2014/15 B.7 647 VOTE REVENUE Part 2 - Details of Departmental Appropriations 2.1 - Departmental Output Expenses Management of Debt and Outstanding Returns (M57) Scope of Appropriation Taking action where returns are outstanding and where payments are overdue, including providing people with assistance on the actions they need to take to meet their obligations. This includes collection on behalf of other agencies and external parties. Expenses and Revenue 2014/15 Estimates $000 Supplementary Estimates $000 Total $000 Total Appropriation 143,259 8,204 151,463 Revenue from the Crown 140,297 8,204 148,501 2,962 - 2,962 Revenue from Others Reasons for Change in Appropriation This appropriation increased by $8.204 million to $151.463 million for 2014/15 due to: a fiscally neutral adjustment of $4.700 million between departmental output expenses a net increase of $4.475 million represented by the return of ($1.008 million), additional funding of $6.300 million, and a transfer of ($817,000) from 2014/15 to 2015/16 for the business transformation programme, and a transfer of $384,000 from 2013/14 to 2014/15 for the mainframe project. Partially offset by: a transfer of ($1.061 million) from 2014/15 to 2017/18 and 2018/19 to align with the timing of capital expenditure for the business transformation programme, and a net reduction of ($294,000) represented by the additional funding of $7,000 and a transfer of ($301,000) from 2014/15 to 2015/16 for the child support scheme reform initiative. Policy Advice (M57) Scope of Appropriation This appropriation is limited to the provision of advice (including second opinion advice and contributions to policy advice led by other agencies) to support decision-making by Ministers on government policy matters. 648 THE SUPPLEMENTARY ESTIMATES OF APPROPRIATIONS 2014/15 B.7 VOTE REVENUE Expenses and Revenue 2014/15 Estimates $000 Supplementary Estimates $000 Total $000 Total Appropriation 8,053 1,100 9,153 Revenue from the Crown 8,051 1,100 9,151 2 - 2 Revenue from Others How Performance will be Assessed and End of Year Reporting Requirements 2014/15 Performance Measures The total cost per hour of producing outputs (see Note 1). Estimates Standard Supplementary Estimates Standard Total Standard $150 ($35) $115 Note 1 - The formula has been updated by Treasury to align it with the amended definition of policy advice costs. Reasons for Change in Appropriation This appropriation increased by $1.100 million to $9.153 million for 2014/15 due to additional funding for the business transformation programme. Services to Inform the Public About Entitlements and Meeting Obligations (M57) Scope of Appropriation Providing information and assistance to customers on the application of the law. Responding to customer enquiries about tax and social support programmes. Adjudication on behalf of the Commissioner on proposed taxpayer assessments. Providing binding rulings and other statements on the interpretation and application of the law administered by Inland Revenue. Provision of services to Ministers to enable them to discharge their portfolio (other than policy decision-making responsibilities). Expenses and Revenue 2014/15 Estimates $000 Supplementary Estimates $000 Total $000 Total Appropriation 251,307 1,848 253,155 Revenue from the Crown 249,846 1,848 251,694 1,461 - 1,461 Revenue from Others THE SUPPLEMENTARY ESTIMATES OF APPROPRIATIONS 2014/15 B.7 649 VOTE REVENUE Reasons for Change in Appropriation This appropriation increased by $1.848 million to $253.155 million for 2014/15 due to: a net increase of $7.573 million represented by the return of ($2.088 million), additional funding of $11.100 million, and a transfer of ($1.439 million) from 2014/15 to 2015/16 for the business transformation programme a net increase of $901,000 represented by the additional funding of $427,000, a transfer of $2.554 million from 2013/14 to 2014/15, and a transfer of ($2.080 million) from 2014/15 to 2015/16 for the child support scheme reform initiative a transfer of $450,000 from 2013/14 to 2014/15 for the salary trade-offs initiative additional funding of $342,000 for the cashing out research and development tax losses initiative a transfer of $267,000 from 2013/14 to 2014/15 for the mainframe project a transfer of $187,000 from 2013/14 to 2014/15 for the implementing student support changes initiative a transfer of $167,000 from 2013/14 to 2014/15 for the broadening the definition of income for student loan repayment purposes initiative, and additional funding of $133,000 for the KiwiSaver: removal of kick-start payment initiative. Partially offset by: a transfer of ($6.248 million) from 2014/15 to 2017/18 and 2018/19 to align with the timing of capital expenditure for the business transformation programme a transfer of ($224,000) from 2014/15 to 2015/16 for the paid parental leave payments initiative, and a fiscally neutral adjustment of ($1.700 million) between departmental output expenses. Services to Process Obligations and Entitlements (M57) Scope of Appropriation Registering tax payers, making tax assessments, assessing child support liabilities including providing a readily accessible inexpensive process for reviewing assessments, receiving and making payments to customers, processing applications and payments for social support programmes, collection of ACC Earners' levies, supplying information to other government agencies and accounting and reporting the collection of Crown revenue. Expenses and Revenue 2014/15 Estimates $000 Supplementary Estimates $000 Total $000 Total Appropriation 140,572 (7,065) 133,507 Revenue from the Crown 119,575 (7,065) 112,510 20,997 - 20,997 Revenue from Others 650 THE SUPPLEMENTARY ESTIMATES OF APPROPRIATIONS 2014/15 B.7 VOTE REVENUE Reasons for Change in Appropriation This appropriation decreased by ($7.065 million) to $133.507 million for 2014/15 due to: a fiscally neutral adjustment of ($10.300 million) between departmental output expenses a transfer of ($3.973 million) from 2014/15 to 2017/18 and 2018/19 to align with the timing of capital expenditure for the business transformation programme the return of ($1.431 million) relating to the simplifying filing requirements for individuals and record keeping requirements for businesses initiative, and a transfer of ($894,000) from 2014/15 to 2015/16 for the paid parental leave payments initiative. Partially offset by: a net increase of $4.425 million represented by the return of ($972,000), additional funding of $6.200 million, and a transfer of ($803,000) from 2014/15 to 2015/16 for the business transformation programme additional funding of $1.382 million relating to the complying with the Foreign Account Tax Compliance Act initiative a net increase of $962,000 represented by additional funding of $499,000, a transfer of $1.096 million from 2013/14 to 2014/15, and a transfer of ($633,000) from 2014/15 to 2015/16 for the child support scheme reform initiative a transfer of $784,000 from 2013/14 to 2014/15 for the mainframe project a transfer of $713,000 from 2013/14 to 2014/15 for the implementing student support changes initiative a transfer of $450,000 from 2013/14 to 2014/15 for the salary trade-offs initiative additional funding of $427,000 for the cashing out research and development tax losses initiative a transfer of $333,000 from 2013/14 to 2014/15 for the broadening the definition of income for student loan repayment purposes initiative, and additional funding of $57,000 for the KiwiSaver: removal of kick-start payment initiative. Taxpayer Audit (M57) Scope of Appropriation Identifying risks to revenue and designing and undertaking audit activities accordingly. Managing litigation of disputed tax cases. Expenses and Revenue 2014/15 Estimates $000 Supplementary Estimates $000 Total $000 Total Appropriation 166,131 10,928 177,059 Revenue from the Crown 165,866 10,928 176,794 265 - 265 Revenue from Others THE SUPPLEMENTARY ESTIMATES OF APPROPRIATIONS 2014/15 B.7 651 VOTE REVENUE Reasons for Change in Appropriation This appropriation increased by $10.928 million to $177.059 million for 2014/15 due to: a fiscally neutral adjustment of $7.300 million between departmental output expenses a net increase of $5.027 million represented by the return of ($1.332 million), additional funding of $7.300 million, and a transfer of ($941,000) from 2014/15 to 2015/16 for the business transformation programme a transfer of $234,000 from 2013/14 to 2014/15 for the mainframe project, and additional funding of $85,000 for the cashing out research and development tax losses initiative Partially offset by a transfer of ($1.718 million) from 2014/15 to 2017/18 and 2018/19 to align with the timing of capital expenditure for the business transformation programme. 2.3 - Departmental Capital Expenditure and Capital Injections Inland Revenue Department - Capital Expenditure PLA (M57) Scope of Appropriation This appropriation is limited to the purchase or development of assets by and for the use of the Inland Revenue Department, as authorised by section 24(1) of the Public Finance Act 1989. Capital Expenditure 2014/15 Estimates $000 Supplementary Estimates $000 Total $000 Forests/Agricultural - - - Land - - - Property, Plant and Equipment 20,000 (16,000) 4,000 Intangibles 42,336 (13,336) 29,000 - - - 62,336 (29,336) 33,000 Other Total Appropriation Reasons for Change in Appropriation This appropriation decreased by ($29.336 million) to $33 million for 2014/15. Capital expenditure on existing systems and infrastructure has been reduced, with capital funding held in reserves to contribute to Inland Revenue's transformation programme in future years. 652 THE SUPPLEMENTARY ESTIMATES OF APPROPRIATIONS 2014/15 B.7 VOTE REVENUE Capital Injections and Movements in Departmental Net Assets Inland Revenue Department Details of Net Asset Schedule 2014/15 2014/15 Supplementary Main Estimates Estimates Projections Projections $000 $000 Explanation of Projected Movements in 2014/15 Opening Balance 275,393 Capital Injections 2,336 275,393 Supplementary Estimates opening balance reflects the audited results as at 30 June 2014. 3,572 Capital injections of $2.336 million for the complying with the Foreign Account Tax Compliance Act initiative, and $1.236 million for the cashing out research and development tax losses initiative. Capital Withdrawals - (1,872) Capital withdrawal of $1.872 million for the complying with the Foreign Account Tax Compliance Act initiative. Surplus to be Retained (Deficit Incurred) - - Other Movements - - Closing Balance 277,729 277,093 THE SUPPLEMENTARY ESTIMATES OF APPROPRIATIONS 2014/15 B.7 653 VOTE REVENUE Part 3 - Details of Non-Departmental Appropriations 3.2 - Non-Departmental Benefits or Related Expenses Child Support Payments PLA (M57) Scope of Appropriation Child support payments to custodial persons who are not dependent on the state for financial support (expenses incurred pursuant to section 141 of the Child Support Act 1991). Reasons for Change in Appropriation The decrease in this appropriation of $4 million from $267 million to $263 million in 2014/15 is due to payments to custodial parents being slightly below the Budget forecast last year, reflecting lower than forecast growth. Family Tax Credit PLA (M57) Scope of Appropriation Family Support payments made to beneficiaries and non-beneficiaries during the year (expenses incurred pursuant to section 185 of the Tax Administration Act 1994). Reasons for Change in Appropriation The decrease in this appropriation of $77 million from $1,934 million to $1,857 million in 2014/15 is due to entitlements declining over time as average incomes increase. Previous Budget Initiatives increased the rate of attrition to entitlements caused by income growth and slightly stronger growth in wages has also contributed to the higher attrition rate this year. In-Work Tax Credit PLA (M57) Scope of Appropriation Extra assistance for low to middle income families where the person works a minimum of 20 hours per week and does not have a partner, or a person and their partner work a minimum of 30 hours per week (expenses incurred pursuant to section 185 of the Tax Administration Act 1994). Reasons for Change in Appropriation The increase in this appropriation of $18 million from $494 million to $512 million in 2014/15 reflects an increase in employment from the improving economy. End of Year Performance Reporting An exemption was granted under section 15D(2)(b)(ii) of the Public Finance Act 1989, as additional performance information is unlikely to be informative because this appropriation is solely for in-work tax credit payments under the Income Tax Act 2007. Performance information relating to the administration of the payment is provided under the Services to Process Obligations and Entitlements appropriation. In the Estimates of appropriations 2014/15 the exemption was incorrectly stated as under section 15D(2)(ii) of the Public Finance Act 1989. 654 THE SUPPLEMENTARY ESTIMATES OF APPROPRIATIONS 2014/15 B.7 VOTE REVENUE KiwiSaver: Kickstart Payment (M57) Scope of Appropriation To enable the one-off payment made on opening a KiwiSaver account for members who meet the required eligibility criteria as set in the KiwiSaver Act 2006. Reasons for Change in Appropriation The increase in this appropriation of $60 million from $171 million to $231 million in 2014/15 is due to higher than forecast new members to the scheme offset by the new policy initiative which sees the cessation of kick-start payments after Budget day. Due to uncertainty over the exact number of claims which will be received before cessation of eligibility there is also an allowance in 2014/15 for this. Minimum Family Tax Credit PLA (M57) Scope of Appropriation Extra payment made to families where at least one parent is working for salary or wages (expenses incurred pursuant to section 185 of the Tax Administration Act 1994). Reasons for Change in Appropriation The increase in this appropriation of $3 million from $13 million to $16 million in 2014/15 is due to an increased volume of claims seen year-to-date, reflecting increased eligibility and an improving outlook for employment. Paid Parental Leave Payments (M57) Scope of Appropriation This appropriation is limited to Paid Parental Leave Payments made to parents in accordance with the Parental Leave and Employment Protection Act 1987. Reasons for Change in Appropriation The increase in this appropriation of $13 million from $176 million to $189 million in 2014/15 is due to an improved outlook for employment and an assumed increase in the number of eligible cases. Parental Tax Credit PLA (M57) Scope of Appropriation To enable payment of additional financial support to be made to working families for the eight week period following the birth of a child (expenses incurred pursuant to section 185 of the Tax Administration Act 1994). Reasons for Change in Appropriation The increase in this appropriation of $2 million from $19 million to $21 million in 2014/15 is due to forecast growth in the uptake of the scheme. THE SUPPLEMENTARY ESTIMATES OF APPROPRIATIONS 2014/15 B.7 655 VOTE REVENUE Payroll Subsidy PLA (M57) Scope of Appropriation This appropriation is limited to the payment of a subsidy to a payroll agent undertaking employers' payroll-related tax compliance activities on their behalf, section 185 of the Tax Administration Act 1994. Reasons for Change in Appropriation The increase in this appropriation of $100,000 from $4 million to $4.100 million in 2014/15 is due to a slight increase in growth in the scheme. This growth may reflect provider advertising and improvements in the economy more generally. 3.3 - Non-Departmental Borrowing Expenses Adverse Event Interest PLA (M57) Scope of Appropriation This appropriation is limited to interest on Adverse Event Income Equalisation Reserve accounts held by taxpayers in the farming and agriculture business (expenses incurred pursuant to section 185 of the Tax Administration Act 1994). Reasons for Change in Appropriation The increase in this appropriation of $10,000 from $10,000 to $20,000 in 2014/15 is due to a small increase in the interest payable. Interest forecasts are rounded up to the nearest $10,000 in the main appropriation year. Income Equalisation Interest PLA (M57) Scope of Appropriation This appropriation is limited to interest on Income Equalisation Reserve Scheme accounts held by taxpayers in the farming, fishing or forestry industries (expenses incurred pursuant to section 185 of the Tax Administration Act 1994). Reasons for Change in Appropriation The increase in this appropriation of $8 million from $7 million to $15 million in 2014/15 is due to the forecast reduced dairy payout and drought-affected farmers in the eastern South Island. More funds are forecast to be deposited into the scheme in 2014/15 and this has a flow-on effect on the amount of interest that will be paid. 656 THE SUPPLEMENTARY ESTIMATES OF APPROPRIATIONS 2014/15 B.7 VOTE REVENUE 3.4 - Non-Departmental Other Expenses Impairment of Debt and Debt Write-Offs (M57) Scope of Appropriation This appropriation is limited to bad debt write-offs for Crown debt and to amounts relating to impairment arising from objective evidence of one or more loss events that occurred after the initial recognition of the debt, and the loss event (or events) has had a reliably measurable impact on the estimated future cash flows of the Crown debt book. Reasons for Change in Appropriation The increase in this appropriation of $18.258 million from $1,162.098 million to $1,180.356 million in 2014/15 is due to an allowance for volatility in the assumptions surrounding debt growth of $304.384 million. Excluding the allowance we are forecasting a reduction of $286.126 million. Impairment of Debt Relating to Child Support (M57) Scope of Appropriation This appropriation is limited to amounts relating to impairment arising from objective evidence of one or more loss events that occurred after the initial recognition of the debt, and the loss event (or events) has had a reliably measurable impact on the estimated future cash flows of the collective book of child support debt. Reasons for Change in Appropriation The decrease in this appropriation of $71 million from $323 million to $252 million in 2014/15 reflects lower child support penalty revenue forecasts. A reduction in penalty revenue leads to a reduction in impairment as the two are directly related. The $252 million figure in 2014/15 has an allowance for volatility in data and modelling assumptions of $30 million. Impairment of Debt Relating to Student Loans (M57) Scope of Appropriation This appropriation is limited to amounts relating to impairment arising from objective evidence of one or more loss events that occurred after the initial recognition of the loan, and the loss event (or events) has had a reliably measurable impact on the estimated future cash flows of the collective book of student loan debt. Reasons for Change in Appropriation The increase in this appropriation of $182 million from $100 million to $282 million in 2014/15 is due to the interim valuation of the scheme, current policy initiatives and an allowance for volatility in the data and modelling assumptions. The interim valuation of the scheme was completed in April 2015 and the final valuation as at 30 June 2015 will be based on additional roll forward data and June macro-economic assumptions. THE SUPPLEMENTARY ESTIMATES OF APPROPRIATIONS 2014/15 B.7 657 VOTE REVENUE Initial Fair Value Write-Down Relating to Student Loans (M57) Scope of Appropriation This appropriation is limited to the initial fair value write-down of student loans. Reasons for Change in Appropriation The decrease in this appropriation of $45.156 million from $668 million to $622.844 million in 2014/15 is due both to a decrease in lending forecasts and a more favourable effective interest rate, which reduces the initial fair value write-down relating to student loans. 658 THE SUPPLEMENTARY ESTIMATES OF APPROPRIATIONS 2014/15 B.7