Documenting Accounting Information Systems

advertisement

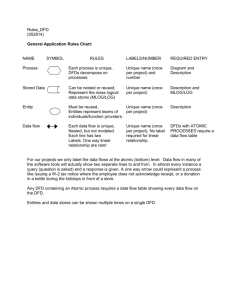

Chapter 3 Documenting Accounting Information Systems < Learning Objectives> After studying this chapter, the student should be able to: (1) Understand why documenting an AIS is important. (2) Prepare and utilize data flow diagrams to understand, evaluate, and design information systems. (3) Prepare and utilize flowcharts to understand, evaluate, and design information systems. 1. What is a documentation of an AIS? It explains how AISs operate and is therefore a vital part of any accounting system. IT describes the tasks for recording accounting data, the procedures that users must perform to operate computer applications, the processing steps that computer systems follow, and the logical and physical flows of accounting data through the system. tools used in the analysis, design, and documentation of systems Narratives, flowcharts, diagrams, and other written materials that explain how a system works. Covers the who, what, when, where, why, and how of data entry, processing, storage, output and system controls. Why we have to understand system techniques? a. As an accountant, you must be able to read documentation so that you can determine how the system works. b. Statement on Auditing Standards (SAS) No. 55 requires that independent auditors understand a client’s system of internal controls before conducting an audit. 2. Why documentation is important? a. Depicting how the system works. Studying and reviewing written descriptions of the inpits, processing steps, and outputs of the system make the job easier. b. Training users Documentation also includes the user guides, procedure manuals, and other operating instructions that help people learn how the AIS operates. c. Designing new systems Documentation helps system designers develop new systems in much the same way that blueprints help architects design buildings. 1 d. Controlling system development and maintenance costs Good documentation helps system designers develop object-oriented SW, that is, programs that contain modular, reusable code. This object-orientation helps programmers avoid writing duplicate programs and facilities changes when programs must be modified later. e. Standardizing communications with others Documentation techniques such as flowcharts and data flow diagrams are standard industry tools, and they are more likely to be interpreted the same way by all parties viewing them. f. Auditing AISs Documentation helps auditors determine the strengths and weaknesses of a system’s controls. g. Documenting business processes By mapping the business processes, documentation helps managers better understand the ways in which their businesses operate. 3. Systems Documentation Techniques a. Flowcharts Probably the most common systems technique. A symbolic diagram that shows the data flows and sequence of operations in a system Flowcharts use a standard set of symbols to describe the transaction processing procedures: The applicable standards for flowcharting symbols were established by the International Organization for Standardization (ISO) and the American National Standards Institute (ANSI). The most common flowcharting systems from the ANSI Bulletin are four groups of symbols: (1) Basic symbols, (2) Input/output symbols (3) Processing symbols, (4) Additional symbols Flowchart symbols in EXCEL Major flowchart symbols are available from EXCEL. To view the Drawing Toolbar of MS EXCEL, select the following options from the main menu: In EXCEL, “View/Toolbar/Drawing” Or you can also click directly on the Drawing icon in the Standard Toolbar. After the Drawing Toolbar appears, select “Autoshapes/Flowchart”. You can observe approximately 28 symbols. 2 (1) System Flowchart A graphical description of the relationship among the input, processing, and output in an information system. It typically depicts the electronic flow of data and processing steps in an AIS. (2) Program Flowchart A graphical description of the sequence of logical operations performed by a computer in executing a program. (3) Document flowchart A graphical description of the flow of documents between Dept. within a company. It concentrates on the physical flow of reports and documents. (4) Analytic Flowchart An analytic flowchart identifies all significant processing in an application, emphasizing processing tasks that apply controls. The flow of processing is depicted using symbols connected with flowlines. (5) Forms Distribution Flowchart A forms distribution chart shows the distribution of multiple copy forms within an organization. The emphasis is on who gets what forms rather than on how these forms are processed. B. Data flow diagram (DFD) A graphical description of the flows of data. DFD is used primarily in the systems development process, as a tool for analyzing an existing system or as a planning aid for creating a new system. A DFD is composed of four basic elements (symbols): 3 (1) Context Diagrams Designers typically first prepare a high-level DFD called a context diagram to provide an overall picture of an application or system. (2) Physical DFDs A context diagram shows very little detail. Systems designers usually elaborate on the elements in the context DFDs by decomposing them into more detailed levels. Physical DFDs show more detailed processes of the application. The first level of detail is called a physical DFD. The physical DFD focuses on physical entities such as the employees involved in the system, tangible documents, reports, inputs, and outputs that flow through the system. (3) Logical DFD A physical DFD illustrates which internal and external entities participate in a given system but does not give the users a good idea of what these entities do. A logical DFD addresses this requirement. Level 0 DFD: It shows only in broad terms what tasks a system perform. But most systems are more complex and therefore require more detail to describe them completely. Level 1 DFD: It contains more detailed processes for a specific task. Example: The following describe the customer payment process of Richmond Company. A/R Dept. receives customer checks and split it into the remittance data and the deposit (which includes the checks and deposit slip). Based on the remittance data, customers’ A/R accounts are updated. After updating the A/R, the receivables information is sent to the credit manager. Required: By identifying the two processes (customer payment and updating of A/R ), prepare a Data Flow Diagram to show the customer payment process. 4 C. Decision Table a Matrix presentation A tabular representation of decision logic. For any given situation, a decision table lists all the conditions (If) that are possible in making a decision. It also lists the alternative actions (Then). Decision Table consists of four parts: 1. Condition stub: outlines the potential conditions of the application, 2. Action stub: outlines the available actions that can be taken. 3. Condition entry: depicts the possible combinations of conditions likely to occur, 4. Action entry: outlines the action to be taken for each combination of conditions. < Example: Decision Table > A credit union pays interest to its depositors at the rate of 6 % per year. Accounts of less than $100 are not paid interest. Accounts of less than $1,000 are paid the normal 6 %, Accounts of $1,000 or more that have been with the union for more than one year get paid the normal 6 %, plus a bonus of 1 %. Decision Table to help the credit union decide how much interest to pay each account. Conditions Stub 1 Rules 2 3 Conditions: Account balance less than $100 Y N N Account balance less than $1,000 Account 1 year old or less . . Y . N Y N Condition Entries N N x x Action Entries Action Stub Actions: Pay no interest Pay 6 % interest Pay 7 % interest 4 x x 5 Problem 3-16 Amanda M is a regional manufacturer and wholesaler of high-quality chocolate candies. The company’s sales and collection process is as follows: Amanda M makes use of an enterprise-wide information system with EDI capability. No paper documents are exchanged in the sales and collection process. The company receives sales orders from customers electronically. Upon receipts of a sales order, shipping department personnel prepare goods for shipment and input shipping data into the IS. The system sends an electronic shipping notice and invoice to the customer at the time of shipment. Terms are net 30. When payment is due, the customer makes an electronic fund transfer for the amount owed. The customer’s information system sends remittance (payment) data to Amenda. Amenda M’s information system updates A/R information at that time. Handout Problem: Ch3 (1) An analyst wishes to document credit purchase authorization procedures in a decision table. A purchase order $50 is approved automatically. Purchases between $50 and $100 are given an authorization number. For purchase over $100, a “hold” is placed on the customer’s account in addition to an authorization number being assigned to the purchase. Required: Prepare a decision table. 6 Problem 3-13 The individual stores in the Mark Goodwin convenience chain prepare two copies of goods requisition form (GRF) when they need to order merchandise from the central warehouse. After these forms are completed, one copy is filed in the store’s records and other copy is sent to the central warehouse. The warehouse staff gets the order and files its copy of the GRF in its records. When the warehouse needs to restock an item, three copies of a purchase order form (POF) are filled out. One copy is stored in the warehouse files, one copy goes to the vendor, and third copy goes to the A/P department. Develop a document flowchart. 7 8