Seminar Strategies in Financial Markets

advertisement

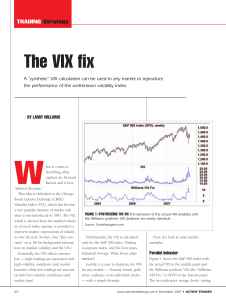

Seminar: Strategies in Financial Markets, 55868 School of Business Administration Hebrew University of Jerusalem Name: Doron E. Avramov, Ph.D, Professor of Finance Office: 5132 Mount Scopus, Jerusalem Web: http://pluto.huji.ac.il/~davramov/ Class Hours: Wednesday 15:30-17:15 Room: חדר עסקאות – מנהל עסקים דורון אברמוב; פרופסור למימון Course Description: From its inception the finance profession featured markets to be informationally efficient. That is to say that asset prices correctly, and at all times, reflect information available to investors. If markets are really efficient then the role of active investment management becomes virtually meaningless. In particular, one cannot beat the market on a risk adjusted basis– expect by luck. In efficient markets higher expected investment return is attributable to higher risk undertaken as well as often to pure luck, but not to managerial skill in market timing and stock picking. Thus, the preferred investment choice would be purchasing index mutual funds or market-wide ETFs which charge relatively low fees. During the past few decades the market efficiency concept has been challenged. Empirical studies have been demonstrating that prices of stocks, bonds, and commodities, as well as exchange rates often deviate from traditional economic theory in predictable ways, deviations that are termed "market anomalies." The major anomalies in the equity markets include the time-series and cross-sectional predictability of future stock returns by past stock returns, market capitalization, the book-to-market ratio, trading volume, accruals, volatility, credit risk, among many others, as well as the time-series predictability by macro variables such as the short-term interest rate, the term spread, the dividend yield, the credit spread, and most relevant to this seminar – by technical indicators such as trends and oscillators. Analyzing investment strategies that capitalize on asset return predictability is at the frontier of research in financial economics among practitioners and academics alike. Top academic journals in economics, finance, accounting, and statistics have hosted a plethora of papers analyzing anomalies in financial markets. Market anomalies have been thoroughly scrutinized by economists and quantitative analysts at worldwide investment companies, central banks, and market regulators. Nevertheless, there are still considerable theoretical and empirical debates on the nature of market anomalies. Whether or not markets are efficient is an open question that will never get resolved (Never say never.) Moreover, blindly investing in market anomalies could be harmful. For instance, the previously robust momentum trading strategy delivered a negative 80% return during 2009. Moreover, over 2011 the small cap value stocks returned 15.15% while the big cap growth stocks returned 17.89%. Over the past years, small cap value stocks considerably outperformed. In this seminar, you are required to answer all the three questions below. The due date is Sunday during the last week of the semester, i.e. 17/1/16. Submit your seminar through a power point file. Send the file to my email address davramov at huji.ac.il during the due date prior to class time. Notice that the first two questions are about timing while the last one is about stock picking. 1 Section 1 – Volatility VIX is the implied volatility index, also known as the fear index. You cannot directly buy long or sell short the VIX. However, you can bet on market volatility through ETNs or Exchange Traded Notes which are investment funds. VXX and VIXY, for one, are ETNs that seek to match the performance of the S&P 500 VIX Short-Term Futures Index. You may consider buying VXX or VIXY if you think that volatility is heading up. On the other hand, XIV and SVXY are ETNs seeking to match the inverse of the daily performance of the S&P 500 VIX Short-Term Futures index. You would consider buying such funds if you think that volatility is about to fall. a. Describe the empirical evidence about the relation between VIX and subsequent realized volatility. Three steps are required. First, describe the empirical evidence on that relation based on published work. Second, run time series regressions of actual volatility on lagged actual volatility and lagged VIX and analyze the slope coefficient of VIX and its significance. Use several lags, including one month, three months, six months, and one year. Third, compare average, volatility, and autocorrelation of each of those annualized measures. The VIX is already annualized. You compute actual volatility based on daily returns and then multiply the quantity by the square root of the number of trading days per year. b. Examine the performance of VXX and VIXY over the past five years. Use plots available at yahoo.finance or any other source you prefer. Could you explain such performance based on the VIX level? Could you explain it based on any other economic mechanism? (hint: try contango). c. Looking forward, does it make sense to invest in VXX or VIXY for the long run? Who, if anyone, should purchase volatility ETNs? d. Common sense suggests that volatility and inverse volatility fund returns are perfectly negatively correlated. Is it really the case? e. Suppose that five years back you invested $1000 in one of the volatility ETNs and you also invested the same amount in one of the inverse volatility ETNs. Plot the evolution of the $2000 invested wealth over time. What do you learn? f. Would it be correct to say that just like VXX and VIXY destroy value, in the same vein XIV and SVXY provide positive performance for the long run (at least, as long as the VIX does not hit extreme levels)? g. Design a trading strategy in which you use the VIX level to invest in XIV. h. Same as above but using the time series of XIV closing price. 2 Section 2 – Technical trading rules This question is based on daily returns on the S&P index. Focus on the last 20 years. a. Use both simple moving average as well as exponential moving average (EMA) to implement trading strategies, switching between the S&P index and cash. You can make your own decision about the length of the moving average. b. Same as above but using the MACD histogram which is the difference between the MACD line and the Signal line. The MACD line is constructed as follows. Calculate a 12-day EMA and a 26-day EMA. The difference between the 12-day EMA and the 26-day EMA establishes the MACD line. The signal line is the 9-day EMA. c. While the moving average as well as the MACD-histogram attempt to identify a trend, oscillators aim to identify a change in trend. There are different sorts of oscillators. Pick one and implement a market timing strategy based on that one. Section 3 – Momentum in US Sectors Momentum is the tendency of past winner (loser) stocks to outperform (underperform) in the future. In addition, there are various sectors in the US economy – such as real estate, consumer goods, energy, among others. Identify at least 12 US sectors and find an ETF implementing momentum using stocks belonging to that particular sector. Compare the performance of that ETF to two benchmarks: (i) The sector itself as represented through a sector ETF (e.g., XLF and XLK are both ETFs investing in financial and technology stocks, respectively). (ii) The market index. Does momentum work? Explain in great detail. Grade Components: Class Participation (30%): There will be class sessions from time to time. I will communicate with you through email announcements. It is mandatory to attend all those scheduled sessions. In general, you are responsible for class lectures as well as any announcements, discussions, or remarks. Project (70%): As described above. On-line resources and databases: Below you can find a partial list of main international and local databases which are available at HUJI. Yahoo.finance Reuters Data Stream – Financial data for all companies traded at the major stock exchanges. The access to this data base is at the trading room or at the social sciences library. Reuters 3000 – Real time data, news, and recent developments for all companies traded at the major stock exchanges. Can be found only at the trading room. 3 Predicta – Historical data for stocks, bonds, mutual funds, beneficial owners and others (mainly local firms). Can be found at the trading room or at the social sciences library. A-Online (Super Analyst) – Financial data and real time trading data for Israeli companies (Traded at the TASE or in the US) which enables technical analysis. Can be found at the trading room or at the social sciences library. 4