Outline of Lecture 1 – Basic Economics Concepts

advertisement

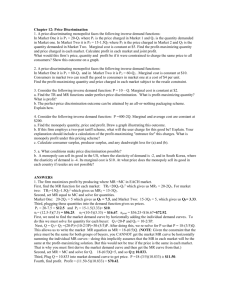

The objectives of firms Professional Development Course in Knowledge Enrichment for Senior Secondary Economics Teachers Outline of Lecture 2 –Microeconomics: The objectives of firms Topics covered: I. Consumers and producers surplus II. Pareto efficiency - Externality with graph analysis III. Profit maximizing output decision of perfect competitive firms IV. Profit maximizing output decision of monopoly V. I. Price discrimination Consumers and producers surplus Consumer Surplus Teaching advice Students will understand consumer surplus if you take the time to work through the example. If you start with this simple example, students will have no trouble understanding how to find consumer surplus on a graph. It is important to stress that consumer surplus is measured in monetary terms. Consumer surplus gives us a way to place a monetary cost on inefficient market outcomes (due to government involvement or market failure). Marginal benefit to consumers, willingness to pay, consumer surplus, demand curve, law of demand and relative price (Alchian Generalization) and their relationship Definition of willingness to pay: the maximum amount that a buyer will pay for a good. Definition of consumer surplus: a buyers’ willingness to pay minus the amount the buyer actually pays. 1 The objectives of firms Using the Demand Curve to Measure Consumer Surplus - Consumer surplus can be measured as the area below the demand curve and above the price. How a Lower Price Raises Consumer Surplus - As price falls, consumer surplus increases. (a) Consumer Surplus at Price P0 Price A Consumer surplus P0 B C Demand 0 Quantity Q0 (b) Consumer Surplus at Price P1 Price A Additional consumer surplus to initial consumers Initial consumer surplus C P0 B P1 D Consumer surplus to new consumers F E Demand 0 Q0 Q1 Quantity Consumer surplus measures the benefit that consumers receive from the good as the buyers themselves perceive it. 2 The objectives of firms Producer Surplus Teaching advice You will need to take some time explaining the relationship between the producers’ willingness to sell and the cost of producing the good. The relationship between cost and the supply curve is not as apparent as the relationship between the demand curve and willingness to pay. Marginal cost of firms, minimum supply-price, producer surplus, supply curve and their relationship - Definition of cost: the value of everything a seller must give up to produce a good. - Definition of producer surplus: the amount a seller is paid for a good minus the seller’s cost. Using the Supply Curve to Measure Producer Surplus - Producer surplus can be measured as the area above the supply curve and below the price. How a Higher Price Raises Producer Surplus - As price rises, producer surplus increases. (a) Producer Surplus at Price P0 Price Supply P0 B Producer surplus C A 0 Q0 Quantity 3 The objectives of firms (b) Producer Surplus at Price P1 Price Supply Additional producer surplus to initial producers D P1 E F B P0 Initial producer surplus C Producer surplus to new producers A 0 II. Q0 Q1 Quantity Illustrate consumer surplus and producer surplus in a demand-supply diagram Pareto efficiency Teaching advice It would be a good idea to remind students that there are circumstances when the market process does not lead to the most efficient outcome. Examples include situations such as when a firm (or buyer) has market power over price or when there are externalities present. Pareto condition - An outcome is Pareto efficiency if it is not possible to improve the benefit of one without lowering the benefit of another. Conditions for efficiency: Maximization of total surplus; marginal benefit equals marginal cost Total Surplus = Consumer Surplus + Producer Surplus Total Surplus = (Value to Buyers – Amount Paid by Buyers) + (Amount Received by Sellers – Costs of Sellers) = Value to Buyers – Costs of sellers 4 The objectives of firms Consumer and Producer Surplus in the Market Equilibrium Price A D Supply Consumer surplus Equilibrium price E Producer surplus B Demand C 0 Quantity Equilibrium quantity Evaluating the market equilibrium: discussion about how the equilibrium of supply and demand maximizes total surplus in a market. - Total surplus is maximized at the market equilibrium. Price Supply Cost to sellers Value to buyers Value to buyers Cost to sellers 0 Equilibrium quantity Value to buyers is greater than cost to sellers. Value to buyers is less than cost to sellers. 5 Demand Quantity The objectives of firms The Deadweight Loss of Taxation Teaching advice Show the students that the nature of this deadweight loss stems from the reduction in the quantity of the output exchanged. Stress the idea that goods that are not produced, consumed, or taxed do not generate benefits for anyone. Tax Revenue Price Supply Price buyers pay Size of tax (T) Tax revenue (T × Q) Price sellers receive Demand Quantity sold (Q) 0 Quantity with tax Quantity Quantity without tax How a Tax Affects Welfare Price Price buyers = PB pay Supply A B C Price without tax = P1 Price sellers = PS receive E D F Demand 0 Q2 Quantity Q1 Without Tax With Tax Change Consumer Surplus A+ B + C A - (B + C) Producer Surplus D+E+F F - (D + E) Tax Revenue None B+D + (B + D) Total Surplus A+ B + C+ D+ E+ F A+ B + D+ F - (C + E) The area C + E shows the fall in total surplus and is the deadweight loss of the tax. 6 The objectives of firms Definition of deadweight loss: the net reduction in welfare from a loss of surplus by one group that is not offset by a gain to another group from an action that alters a market equilibrium. Divergence between private and social costs (benefits): market versus government solutions Definition of externality: the uncompensated impact of one person’s actions on the well-being of a bystander. Externalities and Market Inefficiency Definition of internalizing an externality: altering incentives so that people take account of the external effects of their actions. III. Profit maximizing output decision of perfect competitive firms Teaching advice Students have a difficult time understanding what a competitive market is. The use of the word “competition” in economics is much different than that in sports. This will lead students to often forget that these firms are generally unconcerned with the actions of their rivals. To help students understand price-taking behavior, use the example of common stock. Have your students assume that they inherited 1,000 shares of stock in a company well known in your area. Point out that these 1,000 shares may seem like a lot, but it is a very small proportion of the total number of shares outstanding. If the student wanted to know the value of a share, it could be obtained from a broker. At this market-determined price, the student could sell as few or as many shares as he wishes. At a price above this, no one would be willing to buy any. There is also no reason to charge a price below the current market price, because the student can sell any number of shares that he wishes at the current price. 7 The objectives of firms Definition of competitive market: a market with many buyers and sellers trading identical products so that each buyer and seller is a price taker. The Revenue of a Competitive Firm - Definition of average revenue: total revenue divided by the quantity sold. Total Revenue Average Revenue = Quantity - Definition of marginal revenue: the change in total revenue from an additional unit sold. (For competitive firms, marginal revenue equals the price of the good.) change in Total Revenue Marginal Revenue = change in Quantity Profit maximizing output decision of perfectly competitive firms Teaching advice Make sure that students realize that firms in perfect competition can only change their level of total revenue by varying their level of output because they have no ability to change the price. You may want to make it clear that, by definition, average revenue is always equal to price. But marginal revenue is equal to price only for firms who operate in perfectly competitive markets. Profit Maximization of a Competitive Firm Costs and Revenue The firm maximizes profit by producing the quantity at which marginal cost equals marginal revenue. MC MC 2 ATC P = MR 1 = MR 2 P = AR = MR AVC MC 1 0 Q1 Q MAX Q2 Quantity (The cost curves are required in the elective part, but not in the core part.) 8 The objectives of firms Meaning of profit as the difference between total revenue and total cost Profit maximizing choice of output for individual firms with given prices and marginal cost schedule The marginal cost schedule as the supply schedule of individual firms If: The Firm Will: P ≥ AVC Produce output level where MR = MC P < AVC Shut down and produce zero output Why perfectly competitive market is efficient? Explain in terms of consumer surplus and producer surplus Teaching advice - Market Structure elective only The graphs in this chapter often confuse students because they contain many different curves at the same time. Thus, the first time you draw the profit-maximizing decision of the firm, use only the marginal cost curve and the marginal revenue line. Then, after students feel comfortable with this, add average total cost (to teach students how to measure profit or loss). Last, add average variable cost to teach students about the short-run shutdown decision of a firm earning an economic loss. 9 The objectives of firms IV. Profit maximizing output decision of monopoly Teaching advice After having seen profit-maximization for a perfectly competitive firm, students generally do not have difficulty understanding that a monopolist will maximize profit where marginal revenue equals marginal cost. However, students do have trouble remembering to use the demand curve to find the monopolist’s price. Thus, be careful to review this point several times. Definition of monopoly: a firm that is the sole seller of a product without close substitutes. Compare monopoly versus perfectly competitive firm Monopoly Versus Competition Monopoly Is the sole producer Faces a downward-sloping demand curve Is a price searcher Reduces price to increase sales Competitive Firm Is one of many producers Faces a horizontal demand curve Is a price taker Sells as much or as little at same price A monopoly’s revenue A monopoly’s marginal revenue will always be less than the price of the good (other than at the first unit sold). 10 The objectives of firms Determination of price and output for individual firms with monopoly power The monopolist’s profit-maximizing quantity of output occurs where marginal revenue is equal to marginal cost. Profit Maximization for a Monopoly Costs and Revenue ` 2. . . . and then the demand curve shows the price consistent with this quantity. 1. The intersection of the MR curve and the MC curve determines the profit-maximizing quantity . . . B Monopoly price ATC A A D MC MR 0 Q QMAX Quantity Q Why a monopoly does not have a supply curve A supply curve tells us the quantity that a firm chooses to supply at any given price. But a monopoly firm is a price searcher; the firm sets the price at the same time it chooses the quantity to supply. It is the market demand curve that tells us how much the monopolist will supply because the shape of the demand curve determines the shape of the marginal revenue curve (which in turn determines the profit-maximizing level of output). 11 The objectives of firms A Monopoly’s Profit Profit = (P – ATC) x Q The Monopolist’s Profit Costs and Revenue MC Monopoly price A B Profit = (P – ATC) x Q Monopoly profit Average total cost ATC D C D MR 0 QMAX Quantity Efficiency implications: Deadweight loss (Illustrate in terms of consumer surplus and producer surplus) Teaching advice Remind students that total surplus is the area between the demand curve and the marginal cost curve. It should be clear that surplus is not realized for quantities of output between the monopoly output and the socially efficient output. Here, the monopolist places a wedge between price and marginal cost and the quantity sold ends up being short of the optimum level. 12 The objectives of firms The Inefficiency of Monopoly Price MC Deadweight loss Monopoly price D MR 0 V. Monopoly Efficient quantity quantity Quantity Price discrimination Note: The Economics Curriculum (S4-S6) only requires students to know (i) the meaning of price discrimination, (ii) types of price discrimination: first, second and third degree, and (iii) the conditions for different types of price discrimination. Students are not required to know the price and output determination (and hence efficiency implications.) Meaning of price discrimination Price discrimination is the practice of charging different prices to different consumers for the same good. First degree price discrimination First-degree price discrimination / Perfect price discrimination describes a situation where a monopolist knows exactly the willingness to pay of each customer and can charge each customer a different price. - There is no deadweight loss in this situation. 13 The objectives of firms First Degree Price Discrimination $/Q Pmax MC C P1 Under uniform pricing: - Profit is the area between MC & MR - Consumer surplus is the area of PmaxP1C PC D = AR Under perfect price discrimination: - Profit increases to include the shaded area MR 0 Q1 Quantity QC Second degree price discrimination Practice of charging different prices per unit for different quantities of the same good or service. Second-Degree Price Discrimination * Different prices are charged for different quantities or ‘blocks’ of the same good. Under uniform pricing: - Price = P0 - Quantity = Q0 * Different prices are charged for different quantities or “blocks” of same good. $/Q P1 P0 Under perfect discrimination: - Without Three discrimination: blocks with different prices PP=1P Q =PQ , 0Pand 2, & 3 0. With second-degree discrimination there are three blocks with prices P1, P2, & P3. P2 AC MC P3 D MR Q1 1st Block Q0 2nd Block Q2 Q3 3rd Block 14 Quantity The objectives of firms Third degree price discrimination Practice of dividing consumers into two or more groups with separate demand curves and charging different prices to each group Third-Degree Price Discrimination * Consumers are divided into two groups, with separate demand curves for each group. Consumers are divided into two groups, with separate demand curves for each group. $/Q MRT = MR1 + MR2 P1 MC = MR1 at Q1 and P1 •QT: MC = MRT •Group 1: more inelastic •Group 2: more elastic •MR1 = MR2 = MCT •QT control MC MC P2 D2 = AR2 MCT MRT MR2 D1 = AR1 MR1 Q1 - Q2 QT Quantity MRT = MR1 + MR2 QT: MC = MRT Group 1 is more inelastic (P1, Q1) Group 2 is more elastic (P2, Q2) MR1 = MR2 = MCT QT control MC Conditions for different types of price discrimination Examples of price discrimination: Movie tickets; Airline prices; Discount coupons; Financial aid; Quantity discounts 15