GEI Commodity Chains..

advertisement

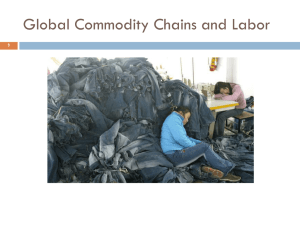

Commodity-Chains in Global Perspective Lecture Organization 1. The Market: Sales to the United States The Source: Producers in the Non-Western world The Intermediaries: Global Corporate Connections 2. Commodity chain dynamics: Concentration of ownership Struggle: Western Buyers versus NonWestern sources 3. Commodity logic: Consumer spaces: Retail giants in the West Commodity Chains: Linking West and Non-West Value and Resource Use The Apparel Industry: a knowledge test ?? What percentage of US apparel is controlled by the top 5 firms? What are they? Percentage of apparel controled by top 5 firms = 068% Firms: year 2000 data Wal-Mart Sears Kmart Dayton Hudson (target, mervyn’s, dayton’s, hudson’s, marshall field) JC Penney Next 24 firms = 30% Same trend in other first world nations Year 2010 data 1. Commodity chains: Basic concepts a. Consumption and production are linked through a web of sites b. Nodes and links c. Each node and link has social, economic and environmental consequences social=affects lives through work relations, economic = wealth is accummulated, ecological = production activities affect the environment 2. Producer Driven Commodity Chains Producer-driven commodity chains are managed by the product producers. Retail owners have little control over the structure of the chain itself 3. Buyer-Driven Commodity Chains 4. Power: who controls the commodity chain? Who determines how things (nature, labor) are valued in production? Is this ‘natural’? History of the commodity Commodities in Nature Buyer-Driven Chains are controlled by retailers or larger intermediary purchasers (Wholesalers) Triangle Manufacturing/Sourcing: the foreign producer becomes a middle merchant who then contracts most or all production to firms in other regions/countries Gereffi Struggle: Buyer- versus producer-driven chains, Who will wrest control of manufacturing? Who will advance 'up the ladder' to brand manufacturing independence: OEM (original equipment) manufacturing, or ‘full-package’ manufacture, then to OBM (Own Brand) manufacture as foreign companies begin to produce their own brands. Branded apparel manufactures: widely recognized brands that carry out no manufacturing whatsoever: ‘born global’ with outsourcing always overseas. Struggle a. a tension exists between foreign OBM manufacturing and first world retail firms who are moving ‘vertical retail’ production with own brand shops (e.g. the gap) b. This tension is evident in the struggle over ‘up-grading’ where foreign manufacturers try to gain a larger share of the value-added in the apparel industry Conclusion 1. Commodity chains are increasingly global in scope 2. The location of the different nodes, however, is constantly changing 3. Commodity chains embed power relations: the nodes each contain real people with interests in the location of brand name manufacture 4. the struggle is over who will run the brand name game. JC Penny’s is instructive in this regard. They were snubbed by Liz Claiborne for distribution early on, but have since developed their own brands and have come back strong (e.g., Arizona jeans)