The Rise of Groupon: AN Ecosystem Analysis of an Internet Sensation

advertisement

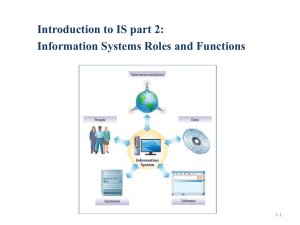

THE RISE OF GROUPON: AN ECOSYSTEM ANALYSIS OF AN INTERNET SENSATION Vasilios Alexiou & Andrew Benson Entrepreneurship & Innovation Strategy October 10, 2011 Part I: The Rise of Groupon Andrew Mason had just moved, bringing along with him his belongings and, importantly, his cell phone. The phone received clear reception at Mason’s previous home; but now, in an outlying suburb of Chicago, Mason could barely make or receive calls. He called his provider and asked to be let out of his contract. The provider refused—that is, unless Mason was willing to part ways with $200. Mason insisted, claiming his service was not satisfactory. The provider stood firm. Finally, exasperated and realizing he needed the $200 to help support his student life, Mason gave up and remained with the provider. An idea occurred to Mason. With enough collective action, a company could be overwhelmed by customers and muscled into changing its actions. All that was needed was a group forum and a critical mass of users to reach a “tipping point” that would force the targeted organization to change its ways. Mason ran with the idea. In November 2007 he started ThePoint.com, a website that would serve as the nerve center for mass movements. Fast forward one year. In November of 2008, after realizing that the users on ThePoint.com were responsive to discounts at brick-and-mortar stores that would “tip,” or activate, with enough interest, Mason launched Groupon (a combination of the words “group” and “coupon”). The idea was simple: Groupon would negotiate deep discounts (50-90%) from local merchants in Chicago who were looking to drum up sales, offer those discounted prices to the Groupon’s growing fan base in the form of a “Daily Deal” email and on Groupon.com, and then split the revenues 50/50 with the merchants. For instance, Groupon would convince a spa to offer a treatment that normally sells for $100 for just $50, and then split that discounted revenue equally, so that Groupon and the spa end up with $25 apiece. By the start of 2011, Groupon claimed over $700 million in annual revenues, offered local daily deals in nearly 300 markets around the world, rejected a $6 billion offer from Google, and owned the title of “fastest growing company in corporate history.” Part II: Groupon’s Ecosystem An end-to-end analysis of Groupon’s ecosystem, or value chain, will help us better understand Groupon’s phenomenal growth. Figure 1, below, diagrams the critical participants 1 (in blue) in Groupon’s ecosystem. We will discuss each participant’s role, along with the manner in which Groupon has aligned these actors in its favor. Figure 1 Merchants Regulators Competing Sites Groupon Advertisers Search Engines Online Affiliates Consumers Social Media Merchants Merchants, who are Groupon’s source of revenue, range from spas and restaurants to helicopter instructors and zoos. The main draw for merchants in working with Groupon is the vast number of members Groupon has convinced to sign up for its daily deal emails (at no cost to members). At roughly 35 million members strong, Groupon’s base is the largest such community among daily deal sites, putting the company firmly in the lead. Whereas in the beginning Groupon cold-called merchants to run deals, now merchants clamor to be on Groupon: the firm accepts only one in eight merchant requests to run a deal with the site. All of this, despite most merchants sharing 50% of their gross revenue with Groupon and breaking even—or losing money—on most deals. Merchants see a loss on a deal as an advertising cost toward the acquisition of new customers. 2 Additionally, Groupon works closely with merchants from the moment Groupon considers offering deals in a city. The company researches target cities thoroughly to ensure that there are enough establishments that would appeal to the Groupon subscriber base, and that these merchants could handle the increased flow of traffic that Groupon deals would send their way. Furthermore, Groupon works with merchants to prepare them for the bump in customers, from providing daily estimates of traffic, to calculating the % of deals that will be redeemed, to capping the number of deals that can be sold on Groupon.com. Nevertheless, many merchants are beginning to look at competing sites that are more likely to accept their deals and offer more favorable revenue sharing terms. Consumers As mentioned above, the millions of consumers who receive Groupon’s daily emails are the key attraction for merchants wishing to increase their volume or advertise their business. There are two main reasons why Groupon has been able to accumulate the largest consumer base among daily deal sites: first, they have a “first mover” advantage in most of the North American cities within which they operate; and second, they have spent almost all of their income on online marketing aimed at attracting consumers (for example, in the first half of 2011, Groupon reportedly spent $345 million in online marketing). Furthermore, Groupon effectively monetizes its subscribers by fostering an “impulse buy” mentality on its site. Most deals are available for only two days or less, and typically must be redeemed within 3-6 months after purchase. Recently, Groupon has added “Groupon Now” deals to its site, which are even more impulsive: most deals are available for only a few hours, and must be redeemed by the end of the day. Advertisers As mentioned in the “Consumers” section, Groupon spends heavily on advertising to consumers. There is no secret to how Groupon aligns advertising to its tactical strategy of being a first mover: they simply outspend the competition. Their online channels of communication include search engine paid ads, social media placements and owned content, and online affiliates (such as blogs and traditional websites) who receive up to a 15% commission for every deal that originates from their linked site. 3 Competing Sites Groupon has employed a two-pronged approach in combating the hundreds of competing daily deal sites that have popped up in the last three years. Domestically, and as mentioned in the “Advertisers” section, Groupon remains the leader due to its brand awareness (i.e. from their first mover advantage) and deep pockets for advertising. Internationally, however, Groupon also spends heavily on acquiring, rather than fighting, competitors. While the financial impact is burdensome on the company, the result within the market is often a near-immediate position of leadership for the company. Regulators Finally, class-action lawsuits against Groupon have prompted state-level government action regulating the terms and use of the deals Groupon sells. These lawsuits claim that the short expiration date (usually within 3-6 months of sale) that Groupon places on deals violates many states’ gift card or gift certificate laws, which typically state that vouchers can be redeemed up to five years after purchase. Consequently, the promotional value of deals may have to be honored beyond their promotional period, which would affect merchants and Groupon, both of whom benefit greatly from sold but unredeemed deals (the fate of 20-40% of all deals sold). Currently, Groupon has cases pending across the US regarding this matter. Part III: Challenges Fiscal Despite its rapid growth and heightened anticipation of its IPO, Groupon still faces considerable obstacles and challenges. Retailers need to remain confident that there are tangible benefits related to offering high discounts on services and products. In addition to the discount, retailers are sharing as much as 50% of their already discounted revenues with Groupon. Retailers are discounting reoccurring sales for new organic sales. Unfortunately this strategy may not be sustainable on an ongoing basis. The sales margins earned from attracting new customers can be low because new customers are attracted simply by the lure of a great deal for consumption of an otherwise non-essential product. These new customers are converted to perpetual deal seekers who will not return to the same retailer to generate 4 reoccurring sales unless another compelling deal or discount is offered in similar fashion. Additionally, existing premium customers are given the ability to shop at a discount and purchase items for which they would have originally paid full price. Retailers can sometimes lose out twice because the discounts provided raise the expectations of new and existing customers and decrease their willingness to pay. This sales strategy creates a precedent from which it is extremely difficult to retreat. The mature markets where retailers have historically experienced success through their partnerships with Groupon also appear to be the markets most susceptible to stagnated growth. Boston is the second oldest North American market in which Groupon operates. Although Groupon’s growing popularity can be measured by the increase in the number of merchants, subscribers and total dollar value of gross billings, the amount of revenue generated per subscriber, has dramatically decreased. During the second quarter of 2009 Groupon had 66 merchants, 17,069 subscribers, and was generating an average of $41.00 in gross billings per subscriber. For the second quarter of 2011, Groupon had 667 merchants and 944,024 subscribers but generated an average of only $13.00 in gross billings per subscriber. Over this same time period the number of Groupons sold per 1000 customers decreased by 17.6%. Although the number of participants and the number of transactions within the Boston ecosystem increased, the relative value added per relative participant is obviously being destroyed. Similar characteristics exist in Groupon’s first and largest market which is Chicago. Over the same time period subscribers have grown from 36,891 to 1,888,348 and merchants have grown from 67 to 1,228. However, it is evident that degradation has occurred in merchants’ ability to capture equivalent value in proportion to the number of subscribers who buy Groupons. Average cumulative Groupons sold has increased from 2.5 to 5.9, yet the average gross billings per subscriber has dropped from $43.00 to $15.00. These figures illustrate an unfavorable financial perspective that is not beneficial to Groupon or merchants. One would not expect a market to mature so quickly within two years and before the company has become publicly owned. Examination of Groupon’s financial statements yields additional concerns about the company’s fiscal health. Groupon’s quarterly net losses have gone from $1.6 million at the end 5 of December 31, 2009, to a maximum of $336 million during December 31, 2010. Losses for the most recent quarter were $101 million for June 30, 2010. At the end of June 30, 2011, Groupon had $225 million of cash on its balance sheet. Although Groupon is generating losses on its income statement the company is still creating increases in cash due to its positive earnings cycle. Groupon collects the cash from the products and services that it sells immediately when customers make a purchase on the web site. Groupon does not have to pay the merchant until well after the web sale, which is when the customer actually redeems the Groupon that she purchased. One business analyst, Henry Blodget, explained: “Right now, Groupon is growing so quickly that this ‘float’ creates positive cash flow even though the company is losing money. The trouble is that the cash Groupon generates from the Groupon sales is not all Groupon's to keep. It owes a big chunk of that cash to the merchants it sells Groupons for. And at the end of Q2, Groupon owed a lot more cash to merchants than it had on hand.” As of June 30, Groupon owed $392 million to merchants for older Groupons. This is considerably greater than the $225 million that the company had on its balance sheet at the end of the same accounting period. Groupon’s working capital deficit at the end of the last three quarters indicates a growing trend. The deficits were -$197 million, -$229 million, and $304 million respectively. A situation like this is permissible as long as the company continues to rapidly grow and sell more Groupons than it is currently liable for. However, if Groupon suffers from another economic downturn, or if the company simply loses sales to increased competition, then Groupon would be vulnerable to significant liquidly issues because the company would have to instantly pay more in liabilities than the cash that it has on hand. Competitive Landscape Groupon’s rapid growth has attracted the attention of large and small companies wishing to capitalize on opportunities in this fairly new market. Large competitors such as Living Social and Google Offers have the financial resources that allow them to engage in price wars with Groupon. Living Social received a $175 million dollar investment from Amazon and raised $400 million in venture capital funding in April of this year. This money is expected to be used for television advertising. Google Offers appears to be on the offensive by using the tactic of a pricing war. PrivCo LLC claims that Google and other competitors plan to charge merchants fees 6 lower than the 50% benchmark that Groupon has been using. It is reported that Google is offering as little as a 30% fee, which is expected to force Groupon to lower its fee. “Groupon's recent amended and updated IPO filing (S-1) filed on August 9th demonstrates this fact: gross margins dropped from 41.9% in the first quarter by over 3 percentage points to 38.8% in just this three-month period. In 2010, Groupon's average fee was 45.2%. It remains to be seen how low Groupon can reduce its fee before its business model becomes completely unsustainable to allow the company to compete. Local competition has also proven to be a force to consider because of the relationships that existing media outlets have with local businesses. Recently New York Magazine introduced daily deals and according to Compete.com, New York Magazine can leverage the pre-existing 1.96 million unique visitors who traveled to its web site in June of 2011. Similarly the LA times had 7.4 million users, the Philadelphia Inquirer 1.6 million and the San Francisco chronicle 3.1 million during the same time period. “PrivCo LLC estimates that Groupon had no more than a mere 50,000 to 150,000 visitors in any of these major markets in the same period, and similarly has relatively smaller penetration in any of its hundreds of local markets”. Such conditions make it difficult to complete with the entrenched establishments that already occupy these metropolitan areas. Conclusion Groupon has experienced torrid growth since it began operations in Chicago in 2008. However there is sufficient evidence to speculate why the company’s IPO has been delayed. The company faces strategic, financial, competitive and legal obstacles that threaten to topple its business model. Groupon continues to focus on growth as evident in its international expansion in countries such as Germany and the UK, where average gross billings per customer continue to grow. As Groupon opens operations in different countries it will have to adjust its strategy to comply with local laws, withstand fierce competition, and adhere to the cultural preferences of consumers abroad. Groupon faces further adoption risk from merchants in the U.S. pending the outcome of its class action lawsuit. Although an eventual IPO will provide Groupon with cash it can use to expand its sales force or absorb losses from decreased fees, much skepticism remains as to whether the company can sustain its current growth and 7 success under the operation of its current business model. Although the creation of Groupon proved to be an innovative concept, the company offers little in terms of a competitive advantage that cannot be duplicated. The company acts as a conduit to facilitate business rather than as a producer of a specific product. Investors should expect Groupon to act as a market participant but not as a market dominator. 8 Sources Associated Press, The. “Groupon Says It May Cut Back on Marketing Costs.” Businessweek, 7 October 2011. http://blog.yipit.com/2011/08/10/new-filing-reveals-groupons-oldest-marketsgot-even-worse/ (http://www.businessweek.com/ap/financialnews/D9Q7LTAG1.htm). Blodget, Henry, “Don’t Mean to be Alarmist, But Groupon is Running Low on Cash.” Business Insider, August 17, 2011. Accessed 8 October, 2011. (http://www.businessinsider.com/groupon-low-on-cash-2011-8?op=1). Groupon amended SEC S-1 company filing. October 7, 2011. Accessed 8 October, 2011 (http://www.sec.gov/Archives/edgar/data/1490281/000104746911008408/a2205238zs1a.htm). Mason, Andrew, “Welcome to The Point.” The Point Blog. 26 September, 2007. Accessed 8 October, 2011 (http://blog.thepoint.com/2007/09/). O’Dell, Jolie, “The History of Groupon.” Forbes Magazine blog. 7 January, 2011. Accessed 8 October, 2011 (http://www.forbes.com/sites/mashable/2011/01/07/the-history-of-groupon/). PR Newswire, issued by PrivCo Media LLC. “Groupon IPO in Jeopardy.” August 10, 2011. Accessed 8 October,2011. (http://www.prnewswire.com/news-releases/groupon-ipo-injeopardy-due-to-increasing-local-competition-pricing-pressure-and-legal-threats-new-reportfrom-privco-media-llc-127491488.html). Steiner, Christopher. “Meet the Fastest Growing Company Ever”. Forbes Magazine, 30 August, 2010. Vacanti, Vinicius, “New Filing Reveals’ Groupon’s Oldest Markets Got Even Worse.” Yipit. August 10, 2011. Accessed 8 October, 2011 (http://blog.yipit.com/2011/08/10/new-filingreveals-groupons-oldest-markets-got-even-worse/). 9