Terms of Reference Study on the Eastern

advertisement

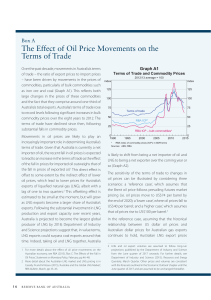

Terms of Reference Study on the Eastern Australian Domestic Gas Market Background Australian gas markets are undergoing a significant period of development. In particular, the eastern Australian gas market is undergoing a period of substantial transformation, with the development of Coal Seam Gas (CSG) and the associated creation of an east coast Liquefied Natural Gas (LNG) export industry. Once the LNG plants come into operation (expected from 2014) there will be a massive increase in demand for gas in the eastern Australian market, with total demand forecast to rise from 697 petajoules per annum (PJ/a) in 2012 to 1,395 PJ/a in 2015 and 2,386 PJ/a in 2020 (Gas Statement of Opportunities 2012). The Commonwealth’s National Energy Security Assessment and follow up consultation with industry indicated that this increase in demand could lead to a period of tightening between the demand for and the supply of gas from around 2015. While the LNG industry is helping to expand Australia’s gas market by bringing on new gas supplies and greater pipeline infrastructure, the timing of these activities and the increasing exposure to international markets is creating considerable uncertainty in relation to the availability and cost of domestic gas. Specific uncertainties include the extent, duration and significance of any potential tightness in gas supply in the eastern market in the critical period between 2015 and 2020 and how any tightness will manifest itself, in particular the degree of contracting risk faced by consumers. Current information on the gas market is limited, with information gaps around forecast domestic supply of gas, particularly given the commercial sensitivities. Some major industrial users of gas have reported they are unable to secure domestic gas supply contracts during this period at any price. Others are reporting being offered short term contracts at much higher prices than existing contracts. While many gas producers are reporting that they are willing to sign gas contracts but it is a question of price and term. There is also limited information about the relationship between international and domestic supply conditions and pricing and how this interaction will play out over time. This Study will help address this information asymmetry and inform Government’s decision making with respect to effective resource management and development of both the domestic and LNG market. Specifically, the Study aims to provide analysis of the expected gas demand-supply situation and identify potential constraints on domestic supply availability over the period 2015-2020 and its consequences for the price of gas. International linkages will also be considered. 1 Gas Market Study Objective The Study will be a joint project between the Department of Resources, Energy and Tourism and the Bureau of Resource and Energy Economics. The objective of the Study is to produce a comprehensive report on Australia’s gas markets, the state of play and barriers to domestic gas supply, focusing on eastern Australia but including analysis of the operation of the West Australian gas market. It is intended to provide a comprehensive view of the level of activity and competitive structure within the domestic supply industry covering tenement holders, upstream producers, pipeline owners/managers and shippers. It will also seek to estimate the current level of demand, price for gas and volumes of both short and long-term gas contracts. Importantly, it will also explicitly consider linkages between these domestic gas market variables and international markets and thereby facilitate exploration of the impact on the domestic gas market of alternative international market scenarios. The Study will utilise a scenario approach to identifying market trends over the period 20132023, to provide a clear picture of the demand-supply situation in the eastern Australian gas market over the 10 year period with a particular emphasis on the period of 2015-2020. In addition, the Study will seek to identify the potential constraints on domestic supply availability. This may include physical barriers (eg pipeline constraints) or non-physical (eg regulatory barriers) and the implications of competition with international gas demand and supply. An array of potential policy responses to mitigate any identified constraints and options to assist in improving the market dynamics to respond to emerging price signals will also be considered. Study Scope Building on an understanding of the developments in Australia’s gas markets over the previous two decades, the Study will include scenarios over the time period 2013-2023 drawing on the following data: gas reserves; gas production rates; gas market demand (including but not limited to short and long-term gas contracts); pipeline capacity; wholesale and retail gas market prices; and state and federal government regulatory and policy settings regarding gas field developments. As the supply and demand dynamics of the eastern gas market are interlinked with the export LNG market, the Study and scenarios will consider market trends for the international gas market, especially in the Asia-Pacific region. The scenario-based Study will also need to account for the following market conditions: general macroeconomic environment; LNG project developments; 2 conventional, shale, tight and CSG gas development and production rates; and gas market infrastructure developments. Stakeholders and Consultation It is proposed an industry reference group be set up comprising relevant stakeholders, particularly gas users and producers, to put their views, experience and expectations about the development of Australia’s gas markets forward. Other Commonwealth agencies and state and territories governments will be kept informed throughout the project’s development. Timing The project is expected to commence mid 2013 with a final report to be completed by the end of 2013. The report would be made public by the Minister for Resources and Energy in consultation with the Prime Minister. 3