Self-similarity, Heavy Tails and Long

advertisement

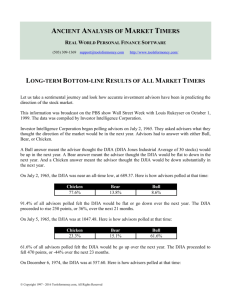

Self-similarity, Heavy Tails and Long-range Dependence as Measures for Financial Market Inefficiency - the Case of Bulgaria 1 Boyan Lomev and Ivan Ivanov Department of Statistics and Econometrics, Faculty of Economics and Business Administration, Sofia University “ St. Kliment Ohridski”, 125 Tzarigradsko chaussee blvd., bl.3, Sofia 1113, Bulgaria, e-mail: lomev@feb.uni-sofia.bg e-mail: i_ivanov@feb.uni-sofia.bg The notion for Market Efficiency – so called efficient market hypothesis implies that security prices fully reflect all available information. The random walk process is a restrictive version of the weak form of the efficient market hypothesis and assumes that successive returns are independent and identically (normally) distributed. In that work several deviations of log-returns of Bulgarian Stock Exchange index from normal distribution are explored – namely: Heavy Tails; Long-range Dependence; Possibility for Forecasting on the basis of historical information. The data consists of daily quotes of Bulgarian Stock Exchange index SOFIX and six major world indices: DAX, DJIA, Hang Seng, NASDAQ, FTSE100 and NIKKEI for the period 2002-2008. The heavy tails of the indexes are studied through the following methods: Histograms Empirical Moments Maximum/Sum Ratio Mean Excess Function GARCH modeling Empirical histograms for SOFIX and DJIA are presented below on Figure 1 as an illustration together with theoretical histogram for the normal distribution. 1 This paper was financially supported under the Sofia University “St. Kl. Ohridski” research project 2009. Soffix DJIA 450 160 400 140 350 120 300 100 250 80 200 60 150 100 40 50 20 0 -0.25 -0.2 -0.15 -0.1 -0.05 0 0.05 0.1 0.15 0.2 0.25 0 -0.08 -0.06 -0.04 -0.02 0 0.02 0.04 0.06 0.08 Figure 1. It is seen, that SOFIX has much more clearly expressed leptokurtosis than DJIA. All other approaches also clearly show that SOFIX differ substantially from the other indexes. For instance GARCH Models can explain the heavy tails for all Indexes except SOFIX. The correlation function for standard ARIMA(p,d,q) processes decays rapidly. There is a class of processes with fractional integration order d and if 0≤d≤0.5 then we have a long-range dependence [1]. The long range dependence was studied by several methods, based on time and frequency analysis of the data. In Table 1 results obtained by Whittle method [2] are presented. Table 1 SOFIX DAX DJIA Hang Seng NASDAQ FTSE100 NIKKEI d=0.0987 d=-0.0355 d=-0.0579 d=-0.017 d=-0.0613 d=-0.0824 d=-0.0096 The other methods give similar results, confirming that only SOFIX can be considered to express long-range dependence. Possibility for Forecasting is an important evidence for inefficiency. If the process is a Random walk, then the best forecast for the return is zero (or the best forecast for the price is previous value). At that stage we use methods from Chaos theory, based on the reconstruction of the phase space and searching for similarities in the trajectory [3, 4]. Obtained results for several local predicting functions are presented in Table 2. Table 2 Forecasting Method MSE Closer Neighbor 0.0004131 Mean Neighbors Forecast 0.0003907 Linear Forecast 0.0003612 Quadratic Forecast 0.0012486 Statistical Mean Forecast 0.0004291 Zero Forecast 0.0004068 We see that forecasting with linear local approximation function gives the smallest mean square error (MSE) and thus confirms the principle predictability of SOFIX quotes. In conclusion we can say that our study clearly shows inefficiency of the Bulgarian Financial Market which is not following a random walk and possess long-range memory. [2] Hosking,J.R.M. Fractional differencing, Biometrika, 68,165-176, 1981. [2] Taqqu,M., V.Teverovsky On Estimating the Intensity of Long-Range Dependance in Finite and Infinite Variance Time Series,A practical Guide to Heavy Tails, ed. Adler,R., M.Taqqu, Birkhauser, Boston,177-217, 1998. [3] Takens, F., Detecting strange attractors in turbulence,Warwick Lecture Notes in Math., vol 898, Springer pp.366-381, 1980. [4] Farmer, J. и J.Sidorowich, Predicting chaotic time series, Physical review letters,1987